Download the Complete Report Here

Cherry Hill Mortgage Investment Corp. (CHMI)

Cherry Hill Mortgage Investment Corp. (CHMI)

EAD Beat Shows Resilience Despite Book Value Pressure and Tough Macro; Yield and Valuation Remain Attractive

- Key Takeaways:

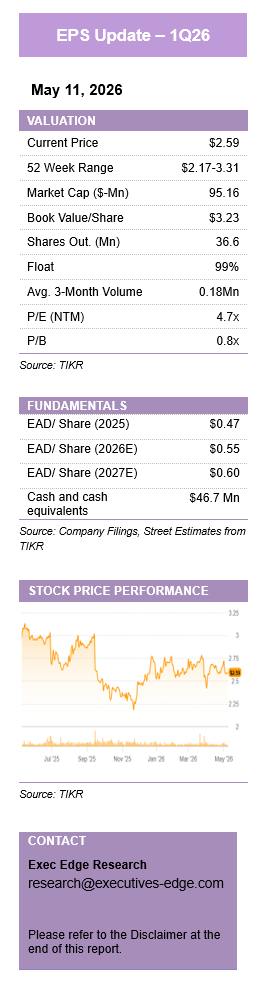

- EAD beat expectations at $0.14/share versus $0.12 consensus, improving from $0.11 in 4Q25.

- Book value declined 6.1% sequentially to $3.23 as geopolitical volatility widened mortgage spreads, though April BVPS rebounded nearly 2%.

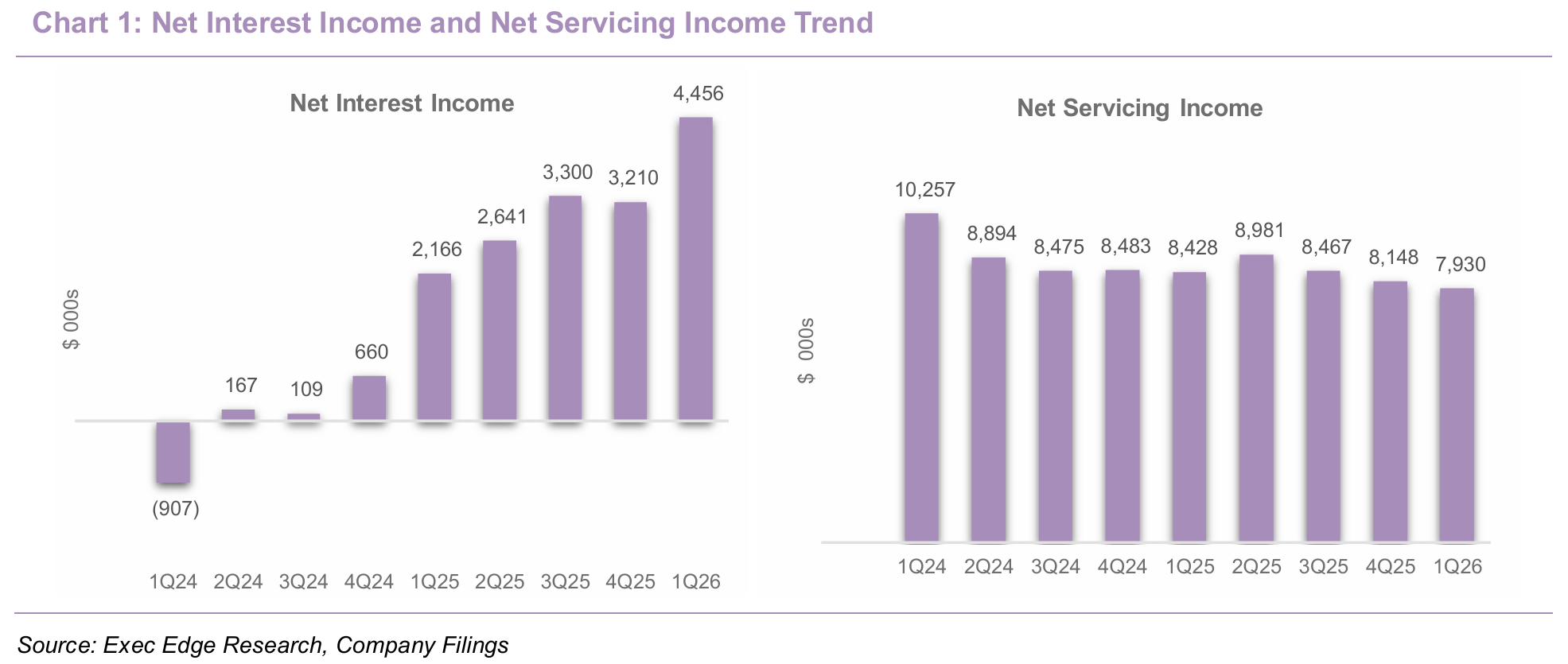

- NII improved 38.8% q/q to $4.5 million, supported by lower repo costs, improved dollar roll income, and 2.90% RMBS spread.

- MSR/RMBS portfolio remained resilient, with low prepayments and improved RMBS carry supporting core earnings despite spread volatility.

- Shares remain attractively valued at 4.7x NTM EAD, 0.8x P/B, and 15.4% dividend yield despite stronger core earnings coverage.

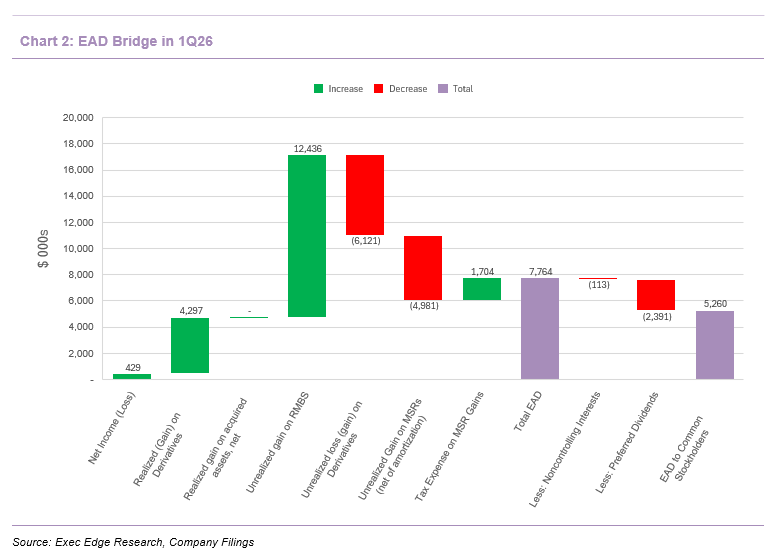

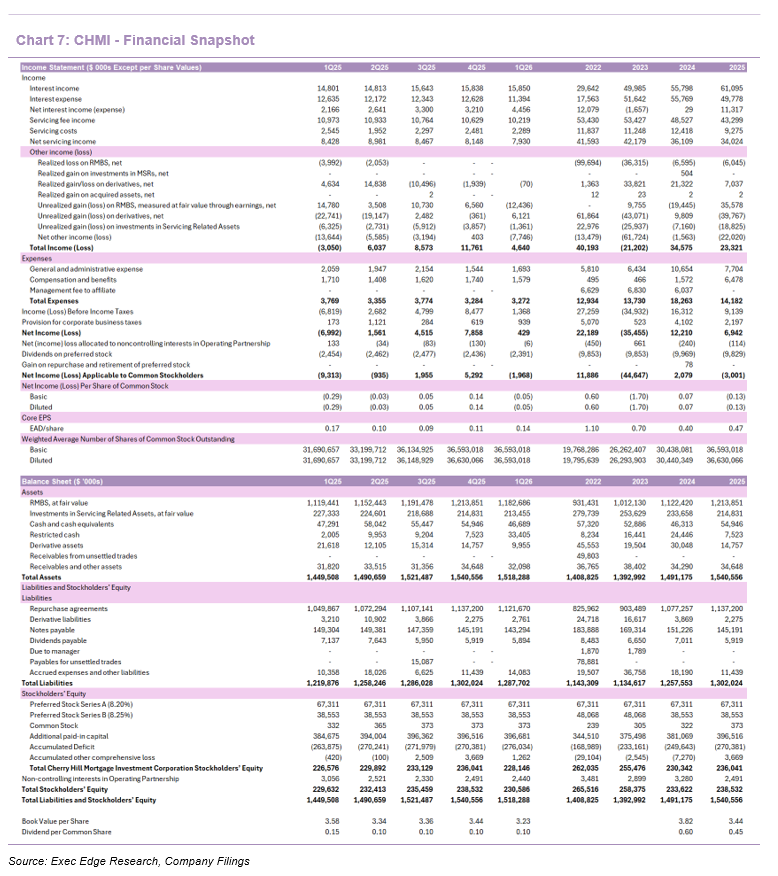

- Resilient core earnings beat expectations despite a volatile macro backdrop, with stronger EAD offsetting book value pressure. CHMI reported EAD attributable to common shareholders of $5.3 million, or $0.14/share, in 1Q26, ahead of Street estimates of $0.12/share and up from $3.9 million, or $0.11/share, in 4Q25. The stronger EAD performance reflected improved NII, lower funding costs, and better dollar roll income, allowing CHMI to cover the $0.10/share common dividend by approximately 1.4x versus 1.1x in the prior quarter. GAAP results were weaker due to mark-to-market pressure, with net loss applicable to common shareholders of $2.0 million versus net income applicable to common shareholders of $5.3 million in 4Q25.

- The GAAP decline was primarily driven by mark-to-market pressure, reflecting a $12.4 million unrealized loss on RMBS measured at fair value through earnings and a $1.4 million unrealized loss on investments in Servicing Related Assets, partially offset by a $6.1 million unrealized gain on derivatives. Book value per common share declined to $3.23 from $3.44, down 6.1% sequentially, while NAV including preferred stock declined $7.9 million, or 3.3%, compared with December 31.

- We view 1Q26 as a volatility-driven quarter rather than an operating deterioration. Management highlighted that the quarter turned abruptly in March after geopolitical escalation triggered higher oil and gas prices, higher inflation expectations, lower rate-cut expectations, wider mortgage spreads, and a flatter yield curve. CHMI entered the quarter with an environment that looked similar to late 2025, including relative stability and January spread tightening, but February and March reversed that setup as volatility rose and investor sentiment weakened. CHMI acted quickly to manage interest rate exposure and protect book value, and management believes the company performed well on a relative basis despite the 6.1% q/q decline in BVPS and negative 3.2% economic return. Importantly, subsequent market stabilization helped agency-focused REITs, and management disclosed that April 30 book value per share increased nearly 2% from March 31, excluding any 2Q dividend accrual, though spreads had softened after mid-April.

- Net interest income improved meaningfully as lower repo costs and better dollar roll income offset market volatility. NII increased to $4.5 million in 1Q26 from $3.2 million in 4Q25, a 38.8% sequential increase, with interest income essentially flat at $15.9 million versus $15.8 million and interest expense declining to $11.4 million from $12.6 million. The RMBS portfolio’s net interest spread expanded to 2.90%, while the RMBS financing rate declined to 3.78% from 3.99% at quarter-end, reflecting lower repo costs and improved dollar roll economics. This is important because the company generated stronger carry even as GAAP results were pressured by unrealized RMBS losses, underscoring the difference between recurring portfolio economics and mark-to-market volatility in a spread-widening quarter.

- Net servicing income remained resilient as the MSR portfolio continued to benefit from low prepayment activity and limited refinance incentives. NSI totaled $7.9 million in 1Q26 versus $8.1 million in 4Q25, reflecting servicing fee income of $10.2 million compared with $10.6 million sequentially and servicing costs of $2.3 million compared with $2.5 million. The MSR portfolio ended the quarter with $15.6 billion of UPB and a carrying value of $213.5 million, while MSR and related net assets represented approximately 41% of equity capital and approximately 21% of investable assets excluding cash. MSR net CPR averaged approximately 4.5% in 1Q26, down modestly from ~5.1% in 4Q25, and recapture remained de minimis because refinance incentives remain limited for the portfolio given its loan rate.

- Prepayment risk remains contained, and the quarter reinforced the stabilizing role of the MSR sleeve within CHMI’s hybrid structure. Mortgage rates averaged 6.1% during 1Q26, below the prior three-month average, which created a short refinancing window before the Iran conflict pushed mortgage rates back toward 6.4% by quarter-end. At current mortgage-rate levels, management estimates that approximately 14% of the mortgage universe is refinanceable, compared with roughly 30% if mortgage rates were to reach 5.5%. This is a modestly better near-term prepayment setup than the prior quarter, when approximately 19% of mortgages were refinanceable and MSR CPR was ~5.1%, and it supports continued servicing income durability if mortgage rates remain near the 6%-6.5% range.

- The RMBS portfolio continued to represent the majority of investable assets and remains central to upside if mortgage spreads stabilize. At quarter-end, RMBS represented approximately 79% of investable assets excluding cash and approximately 42% of equity capital, broadly consistent with the 4Q25 allocation. The RMBS portfolio, inclusive of TBAs, stood at approximately $807 million, in line with the prior quarter, while the RMBS portfolio had a book and carrying value of approximately $1.2 billion, a weighted-average coupon of 4.98%, and a weighted-average maturity of 27 years. RMBS CPR declined modestly to 8.0% from 8.5% in 4Q25, reflecting a portfolio that remained positioned toward the middle and higher portions of the coupon stack. While the $12.4 million unrealized RMBS loss drove the GAAP loss, the portfolio remains positioned to benefit if mortgage spreads retrace from stressed March levels and agency mortgage technicals remain supportive.

- Management continues to view current asset returns as attractive if volatility stabilizes, with levered RMBS returns in the mid-teens to high-teens range and MSR returns around 10%-12%. However, incremental deployment is likely to be funded through capital recycling rather than balance sheet expansion, as management emphasized that any new investment opportunity would need to be evaluated against existing asset classes on a risk-adjusted return basis.

- Hedge positioning helped mitigate the book value impact from rising rates and volatility, even though hedge gains did not fully offset RMBS spread marks. At quarter-end, CHMI held interest rate swaps with a notional amount of $833.7 million, TBAs with a notional amount of negative $384.3 million, Treasury futures with a notional amount of $6.0 million, and Eris SOFR swap futures with a notional amount of negative $59.5 million. On a notional basis, these positions equated to approximately $396 million of net hedge exposure across swaps, TBAs, Treasury futures, and Eris SOFR swap futures, and generated a $6.1 million unrealized derivative gain during the quarter compared with a $0.4 million unrealized derivative loss in 4Q25. Realized derivative loss narrowed substantially to only $0.1 million from $1.9 million in 4Q25. This hedge outcome supports management’s call commentary that CHMI managed interest rate exposure well in March, but also highlights the remaining sensitivity to mortgage basis widening, which hedges can reduce but not eliminate.

- The industry environment weakened sharply after a strong January, but management’s forward tone improved as April stabilization began to support agency mortgage performance. First quarter portfolio performance was shaped by GSE policy signaling, mortgage spread volatility, and changing central bank rate expectations, all of which were amplified by geopolitical risk late in the quarter. January performance benefited from sharp but temporary mortgage spread tightening, while February and March reversed those gains as volatility, higher rates, yield curve flattening, and weaker investor sentiment pressured mortgage spreads. Tighter SOFR spreads also weighed on portfolio performance, as escalating volatility pushed SOFR spreads continuously tighter through the quarter. Management noted that mortgage spreads versus 7-year swaps ended 1Q around 165 bps, had retraced to roughly 150 bps by the time of the call, could move toward 130 bps in a more stable environment, and could revisit 180 bps in a renewed widening scenario. Management also noted that mortgage supply should be reduced at current rate levels, while consistent demand from the GSEs should support mortgage technicals if volatility normalizes and the Iran conflict is resolved.

- Strategic partnership with Real Genius LLC remains on plan, providing longer-term digital origination and recapture optionality. CHMI’s investment in Real Genius, a Florida-based digital mortgage technology company, gives the company exposure to a proprietary direct-to-consumer mortgage platform that can support instant prequalification, automated documentation, and real-time loan tracking through a custom-built point-of-sale system. Management’s 1Q26 update was limited but constructive, stating that the partnership continues to progress in line with expectations. The strategic relevance is unchanged: if mortgage affordability improves and refinancing activity eventually returns, Real Genius could support borrower engagement, recapture economics, and digital origination optionality, complementing Aurora’s MSR capabilities and CHMI’s existing servicing-related asset strategy.

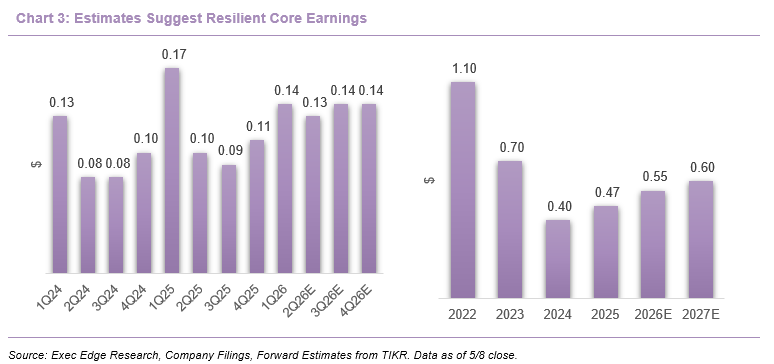

- 1Q26 reflected improved EAD momentum, with core earnings ahead of estimates despite book value volatility. EAD attributable to common shareholders increased to $5.3 million, or $0.14/share, from $3.9 million, or $0.11/share, in 4Q25, helped by stronger NII, lower interest expense, and improved dollar roll income. This compared favorably with Street estimates of $0.12/share. Current Street estimates indicate that EAD is expected to come in at $0.13/share in 2Q26. On an annual basis, Street estimates indicate an EAD of $0.55 per share in 2026, rising to $0.60 per share in 2027. (Source for Street estimates: TIKR)

- Positive outlook remains dependent on stabilization in volatility and mortgage spreads, but April book value improvement supports the near-term setup. Management expects markets to remain volatile in the near term until there is greater stability in the Middle East, but also indicated that any stabilization could support spread tightening and positive portfolio returns. The 2Q26 setup is therefore mixed but improved from March: book value increased nearly 2% through April 30, mortgage spreads had retraced from approximately 165 bps to 150 bps by the call, and management sees potential for spreads to move toward 130 bps if volatility normalizes. At the same time, management cautioned that spreads softened after mid-April and that any renewed escalation could push spreads wider again, potentially toward 180 bps. This makes 2Q26 book value direction highly sensitive to geopolitical clarity, rate volatility, and agency mortgage technicals.

- Operating expenses remained controlled after the normalization already seen in 4Q25, supporting EAD conversion. Total expenses were $3.3 million in 1Q26, essentially flat with $3.3 million in 4Q25, with G&A of $1.7 million and compensation and benefits of $1.6 million. The stable expense base follows the prior quarter’s ~30% q/q reduction in G&A after one-off personnel transition costs rolled off, reinforcing that internalization and expense discipline continue to support earnings quality.

- Liquidity remains adequate and leverage conservative, supporting funding stability through a volatile spread environment. CHMI ended the quarter with $46.7 million of unrestricted cash, compared with $54.9 million at 4Q25, and aggregate portfolio leverage of 5.5x compared with 5.4x sequentially. The company’s capital structure remained broadly stable, and management emphasized a prudent approach to incremental opportunities, with new investments evaluated against other asset classes on a risk-adjusted return basis. For CHMI, the relevant working-capital analogue is not inventory but liquidity, repo capacity, collateral flexibility, and asset allocation. On that basis, $46.7 million of unrestricted cash, 5.5x leverage, $1.2 billion of RMBS carrying value, and $213.5 million of MSR carrying value suggest sufficient flexibility to manage collateral and dividend obligations, but not an unconstrained balance sheet for aggressive expansion.

- We believe the $0.10 common dividend for 1Q26, which was fully covered by $0.14/share of EAD, reflects improved payout visibility despite book value pressure. Dividend coverage increased to approximately 1.4x from 1.1x in 4Q25, while the annualized dividend yield stood at 15.4% based on the May 8 closing price. The company also declared $0.5125/share on its 8.20% Series A preferred and $0.5978/share on its 8.250% Series B preferred, both paid on April 15. While valuation-driven volatility remains inherent in CHMI’s hybrid mREIT model, 1Q26 showed that distributable earnings can improve even in a difficult spread environment, provided funding costs decline and MSR prepayments remain contained.

Attractively Valued Amid EAD Resilience, Strong Dividend Yield and Discounted Book Value

- CHMI shares continue to screen undervalued relative to covered dividend yield, forward EAD, and discounted book value despite 1Q26 mark-to-market volatility. Please note that the following analysis is for illustrative purposes only and does not constitute a stock recommendation, price target, or buy/sell/hold rating. Our valuation assessment incorporates multiple approaches, including absolute time-series analysis and relative peer comparison. While we do not provide a formal price target for CHMI, the analysis below highlights the stock’s positioning across key valuation metrics and potential re-rating pathways.

- CHMI currently trades at a discount across core valuation metrics, suggesting valuation remains disconnected from resilient core earnings despite 1Q26 book value volatility. The stock trades at a 49% discount to its 3-year high NTM P/E multiple and a 15% discount to its 3-year P/BVPS multiple, reflecting investor caution around mortgage spread volatility, geopolitical uncertainty, and book value sensitivity rather than deterioration in distributable earnings. We believe the 1Q26 EAD beat, dividend coverage of ~1.4x, solid liquidity, disciplined 5.5x leverage, resilient MSR cash flows, and the nearly 2% April book value rebound collectively support the investment case.

- Rerating potential is tied less to aggressive balance sheet growth and more to sustained EAD coverage and book value stabilization, with key drivers including repo cost improvement, mortgage spread stabilization, MSR CPR remaining near mid-single digits, disciplined capital recycling into attractive RMBS/MSR returns, and longer-term optionality from Real Genius if refinancing activity improves.

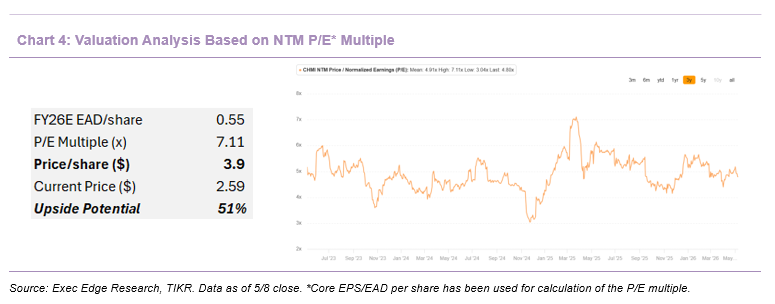

- Absolute valuation analysis indicates meaningful upside potential relative to historical trading ranges.

- CHMI currently trades at 4.7x NTM P/E, below its 3-year peak multiple of 7.1x. Applying the historical peak multiple to NTM EAD/share implies an illustrative value of approximately $3.9 per share.

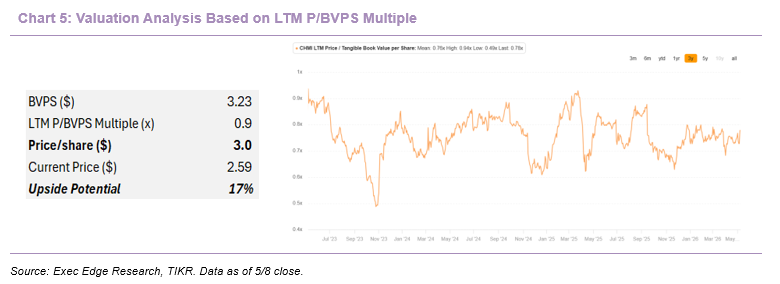

- On a book value basis, CHMI trades at 0.8x LTM P/BVPS, below its 3-year peak of 0.94x; applying the peak multiple to current book value implies an indicative valuation of approximately $3.0 per share. Together, these time-series analyses highlight the degree of multiple compression despite stronger EAD coverage, lower funding costs, and an April book value rebound following 1Q26 mark-to-market pressure.

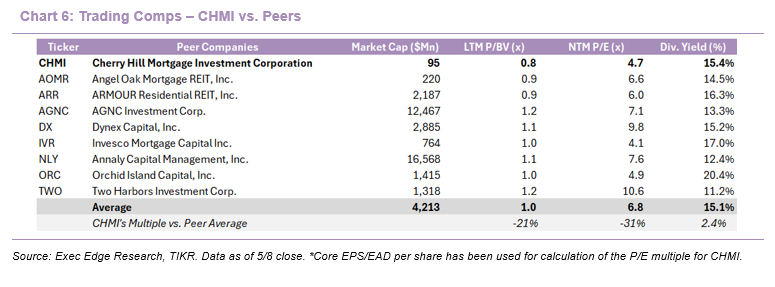

- Relative valuation further reinforces CHMI’s discounted positioning within the hybrid mREIT peer set. The company’s 4.7x NTM P/E represents a 31% discount to the peer average of 6.8x, while its 0.8x LTM P/BVPS similarly screens below sector averages. Conversely, CHMI’s 15.4% dividend yield (as of May 8 close) remains above the industry average of approximately 15.1%, underscoring the attractive income profile available at current valuation levels. Taken together, we view CHMI as attractively valued on both absolute and relative bases, with potential for multiple expansion as earnings visibility improves, book value stabilizes, and broader mortgage market conditions normalize.

Download the Complete Report Here

Read Exec Edge’s Initiation on Cherry Hill Here

Subscribe to our Weekly Newsletter to Receive All Research

Contact: