By Jarrett Banks

Despite coming off a strong quarter and a 2026 +20% profit growth guide, Corpay’s stock is down because of investor concerns about stablecoins. Exec Edge had the opportunity to sit down with Ron Clarke (CEO) and Peter Walker (CFO) to discuss their views on how the market is misreading the risk.

Exec Edge: Maybe we’ll start at the top, just for readers who are unfamiliar with Corpay. Walk us through what Corpay does.

Ron Clarke: At the simplest level, we’re a corporate payments company with a menu of digital payment programs to help businesses control their non-payroll spend. We provide programs for controlling employee walk-around spending, automating AP payments and converting and moving currencies around the world. Our solutions help companies better control all kinds of vendor-related expense.

Exec Edge: You’ve talked about growing your corporate payments business. Where do you see your strongest moat in the corporate payments and cross-border space?

Ron Clarke:The biggest moat we have are the various payment acceptance networks that we’ve built. For example, in corporate payments, what we call payables, where we help businesses automate AP workflow and pay their vendors. We’ve built networks…similar to the card networks, so we know who the vendors are, whether they accept cards, what their bank account information is, etc. We have built B2B vendor payment networks that are proprietary and advantaged.

Our proprietary networks have hundreds of thousands of vendors, and then the same in the cross-border business, we’re making payments on behalf of customers around the world. So, we have proprietary pipes (networks), and the compliance and licensing capabilities to move money to literally hundreds of countries around the world. The licensing is a massive regulatory moat.

The basis of our cross-border service offering is a core system that has integrated to hundreds of bank networks, in-country payment schemes and real-time payment networks around the world. We can essentially provide access to an entire global network of payment rails, including blockchain, stablecoin and digital wallets all through one point of integration to our technology, with the liquidity and licenses to support those flows globally.

Then we have the distribution, hundreds and hundreds of specialized sales people finding the businesses/customers that have all the money. Remember, we’re in the business of controlling spend, so you have to have clients that have spend. We have the clients, and their spend is over $400 billion annually. So, we have a lot of clients that move a lot of money or purchase a lot of things, and we have these network and regulatory moats that make it hard for other companies to compete.

Finally, we are excited about stablecoins and blockchain as a means to move money. Though in-country payments are essentially cost-less today, and real-time rails make payments instantaneous, blockchain and stablecoin provide the ability to move money in an “always on, 24/7” capacity. It also enables the ability to get money to exotic currencies more efficiently. That use case really doesn’t apply to our business as 90% plus of our fx revenue and volume is in G20 currencies.

Exec Edge: Do you think the market is misinterpreting the stablecoin opportunity as a headwind instead of a tailwind for Corpay, particularly for your cross border business?

Ron Clarke: Yes. In our cross-border business, which is our fastest growing business, the concern is that it’s going to be disrupted by stablecoins. What’s really missing in that narrative is that stablecoins provide a new, additional digital currency and money movement rail. I’d also point out that stablecoins are essentially the 4th generation of money movement capabilities…starting with the Swift network, then direct in country ACH schemes, then onto real time payments, and now tokenized currencies and blockchain. They all coexist today, and we expect stablecoin to increase its adoption over time.

We really make our money from FX conversion, risk management or hedging contracts, and foreign bank accounts. And the moat around the business is super strong in terms of the technology we have, the liquidity we have, etc. So people are confusing the rails, which is stablecoin/blockchain with FX conversion and hedging contracts capability. Stablecoins are a new pipe — we make money on what flows through the pipe, regardless of which pipe it is. We’re completely agnostic to the rail and means of funds transfer in that we simply optimize the rail to meet the customer need.

November of last year I shared our stablecoin strategy and we are making great progress executing it. We plan to host a cross-border investor teach-in after our earnings call in May to dive deeper into the business and our stable coin capabilities.

Exec Edge: So in other words, investors aren’t completely understanding the complementary nature of an infrastructure provider, like Circle or BVNK, which are similar to the Swift network?

Ron Clarke: We see Circle and BVNK as alternative infrastructure providers, just like Swift or the traditional ACH banking system

So, the difference between the “infrastructure providers” and us, is we’re users of these rails or infrastructure. We’re not a provider of the infrastructure. Having more suppliers of infrastructure is a good thing for Corpay, providing new, alternative ways to move money.

Again, it’s not competitive with what we do. Today, we simply use Swift or the banking system, and we are incorporating the stablecoin/blockchain rails.

Exec Edge: Let’s talk about that MasterCard partnership. Now, I understand they also own a piece of your cross-border payments business. Why?

Ron Clarke: The idea is that our cross-border business, which is approximately $1.5 billion in revenue this year, sells to different kinds of customers, corporate accounts and select verticals. The verticals include financial institutions, asset managers and digital currency. And so the idea is that we could make the financial institution segment much bigger, it’s probably under 10% of the business today, if we could get to meet more people in banks. We believe that nobody knows banks around the world better than MasterCard. We proposed going to market together where Mastercard introduces our service, Corpay brings in proprietary cross-border services, and the bank’s clients get to utilize our services. The partnership is tracking ahead of expectations with three new clients and a robust pipeline.

Mastercard acquired 3% of our cross border business, at approximate $13 billion valuation. Our partnership is exclusive, so Mastercard can’t go to another cross-border company to sell into banks.

Exec Edge: How does Mastercard’s BVNK acquisition impact the partnership?

Peter Walker: As Ron said, BVNK is a blockchain infrastructure business that sells to other users of that infrastructure. So Mastercard bought infrastructure. We sell services, and we have an exclusive partnership with Mastercard for currency exchange and hedging services. Our exclusivity with Mastercard protects that lane completely

Exec Edge: The historical performance of the stock has been impressive – up 10x since the IPO in 2010. In February of 2026 you delivered another beat and raise quarter and gave strong financial guidance, above analyst’s estimates for fiscal 2026. Yet the stock is off almost 20% in the last 30 days. What is the market missing?

Ron Clarke: We believe there is a disconnect between our financial performance and future growth prospects, and our valuation. For our stock to trade at approximately 6 turns below the equal weighted S&P, and yet be faster growing with higher margins, doesn’t make a lot of sense to us.

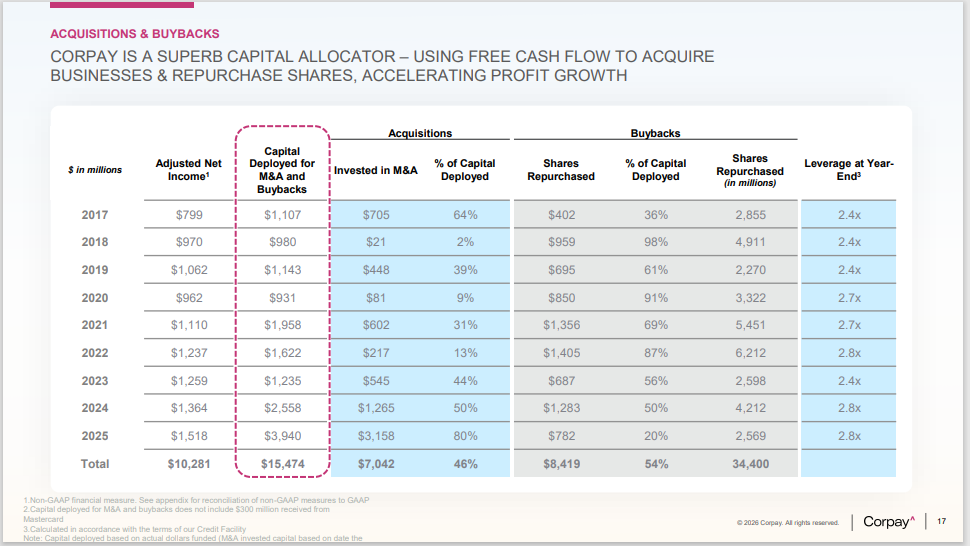

Exec Edge: Let’s talk M&A and capital allocation for a second. You guys have got a good track record. What’s the strategy and appetite for further M&A and how do you balance that with return capital to shareholders via buybacks?

Ron Clarke: Our capital allocation strategy is to overweight to corporate payments acquisitions. There a number of potential M&A targets in the corporate payment space. We also did mention on our recent earnings call that we’ll probably divest some additional non-corporate payments businesses to simplify the company, and to generate capital. Just another way to create liquidity for more share buybacks.

Although there are attractive businesses that we want to buy, there’s no better earnings to buy right now than CPAY at this price. We believe the stock is fundamentally mis-priced and under-valued, and we’re putting capital behind that view.

READ MORE

Swarmer IPO Rises 700% Following Exec Edge Research Initiation

Register for our weekly newsletter HERE

Contact:

Editor@IPO-Edge.com

Click HERE to follow us on LinkedIn