Download the Complete Report Here

The ONE Group Hospitality, Inc. (STKS)

Traffic Led Comparable Sales Recovery and Benihana Synergies Continue to Drive Margin Expansion and Free Cash Flow Improvement

Traffic Led Comparable Sales Recovery and Benihana Synergies Continue to Drive Margin Expansion and Free Cash Flow Improvement

- Key Takeaways

- Revenue and comparable sales were modestly impacted by softer traffic at certain STK mall locations and holiday timing shifts, though trends improved sequentially exiting the quarter.

- Benihana synergies, procurement efficiencies, and disciplined execution drove 100 bps of restaurant margin expansion and 12.1% Adjusted EBITDA growth despite ongoing closures.

- Traffic trends turned positive entering 2Q26 as loyalty, happy hour, and Power Lunch initiatives gained traction across brands.

- Portfolio optimization initiatives continued advancing, with five Grill conversions expected to reopen by year-end 2026 at attractive returns.

- Shares remain materially discounted relative to improving free cash flow generation, expanding margin visibility, and continued deleveraging potential.

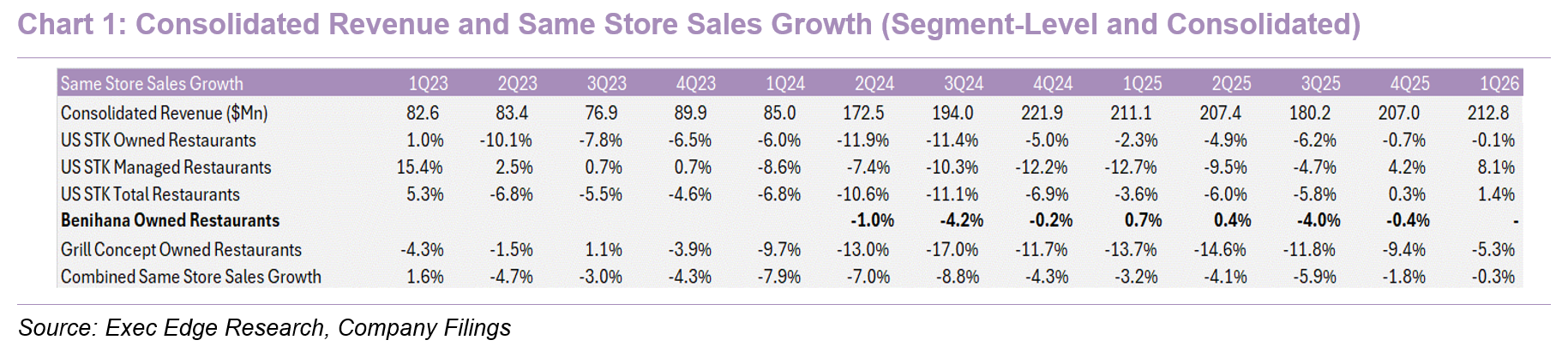

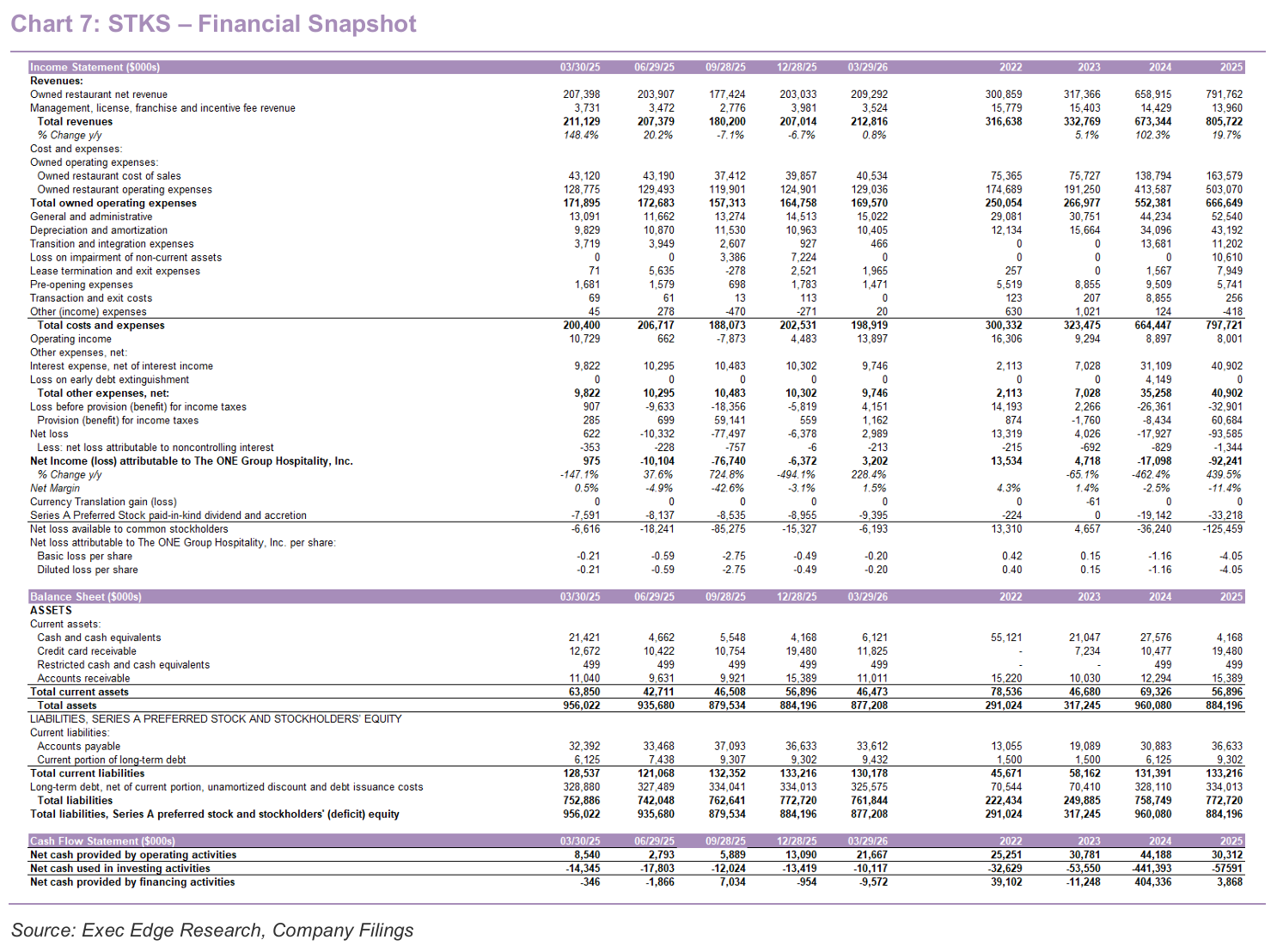

- Revenue and comparable sales were impacted by softer traffic at certain STK mall locations and holiday timing shifts, though trends improved sequentially exiting the quarter. STKS reported 1Q26 revenue of $212.8 million, up 0.8% y/y but below the guided range of $217-$221 million, while company-owned restaurant net revenue increased 0.9% to $209.3 million. Consolidated comparable sales declined 0.3%, representing an improvement from the 1.8% decline reported in 4Q25 and continuing the positive trajectory exiting fiscal 2025. Management noted that softer traffic at several mall-based STK locations and broader calendar-related timing shifts created modest pressure on quarterly performance relative to expectations, although momentum improved materially exiting the quarter. Importantly, management noted that comparable sales and transaction trends turned positive entering 2Q26, suggesting recent improvement is being driven increasingly by traffic rather than pricing.

- Franchise and incentive fee revenue moderated due to lower contributions from managed STK locations in North America. Management, licensing and incentive fee revenues decreased to $3.5 million in 1Q26 compared with $3.7 million in the prior-year quarter, reflecting exit of management agreement in Scottsdale, Arizona in 2Q25.

- Margins expanded meaningfully on procurement synergies, favorable beef sourcing, and disciplined cost management, while EBITDA growth and lower capex continued supporting free cash flow generation and deleveraging. Company-owned restaurant cost of sales improved 140 bps y/y to 19.4% of restaurant revenue from 20.8% in the prior-year period, driven by procurement synergies, menu optimization, favorable beef sourcing, operational efficiencies, and improved PMIX management. Operating income increased 30% y/y, while adjusted EBITDA grew 12.1%. Capital expenditures, net of tenant improvement allowances, declined 23% y/y as the company prioritized capital-efficient growth.

- Comparable sales and transaction trends turned positive entering 2Q26 across the broader portfolio, reinforcing confidence in the underlying trajectory of the business. Both STK and Benihana generated positive comparable sales entering 2Q26, while management highlighted positive transaction trends across the portfolio. Importantly, management noted that recent comparable sales improvement is being driven increasingly by traffic rather than pricing, representing a notable shift relative to broader industry trends. The quarter also benefited from approximately $8.3 million of incremental revenue associated with the fiscal calendar shift that moved New Year’s Eve into fiscal 2026, partially offset by approximately $1.8 million of lost revenue associated with closed Grill Concept locations.

- Benihana continued functioning as a stabilizing higher-margin asset within the broader portfolio while integration initiatives drove additional operational improvement. Benihana comparable sales were ~flat during 1Q26 following a 0.4% decline in 4Q25 and a 4.0% decline in 3Q25, reflecting stabilizing traffic and resilient guest demand. Restaurant operating profit margins at Benihana expanded 130 bps to approximately 21%, driven by procurement synergies, labor optimization, improved scheduling, and supply-chain efficiencies. The segment continues benefiting from procurement scale associated with the Benihana acquisition, particularly across beef sourcing and broader vendor consolidation initiatives.

- Grill Concepts trends continued improving sequentially. Grill Concepts comparable sales declined 5.3% in 1Q26 compared to declines of 9.4% in 4Q25 and 11.8% in 3Q25, representing the strongest quarterly performance since 2023. Importantly, management noted that transactions within the Grill portfolio turned positive during the quarter, suggesting that traffic stabilization efforts may be beginning to gain traction even as the company continues aggressively rationalizing underperforming locations.

- Commentary surrounding beef procurement and promotional strategy also provided additional insight into how STKS plans to manage commodity volatility through the remainder of 2026. While beef pricing remains contracted through September 2026, management acknowledged that the broader beef environment remains challenging heading into 4Q26. Rather than relying solely on pricing actions, the company is actively optimizing PMIX and promotional windows by emphasizing alternative cuts and reducing reliance on filet-heavy promotions. This approach could help mitigate future commodity pressure while preserving traffic momentum.

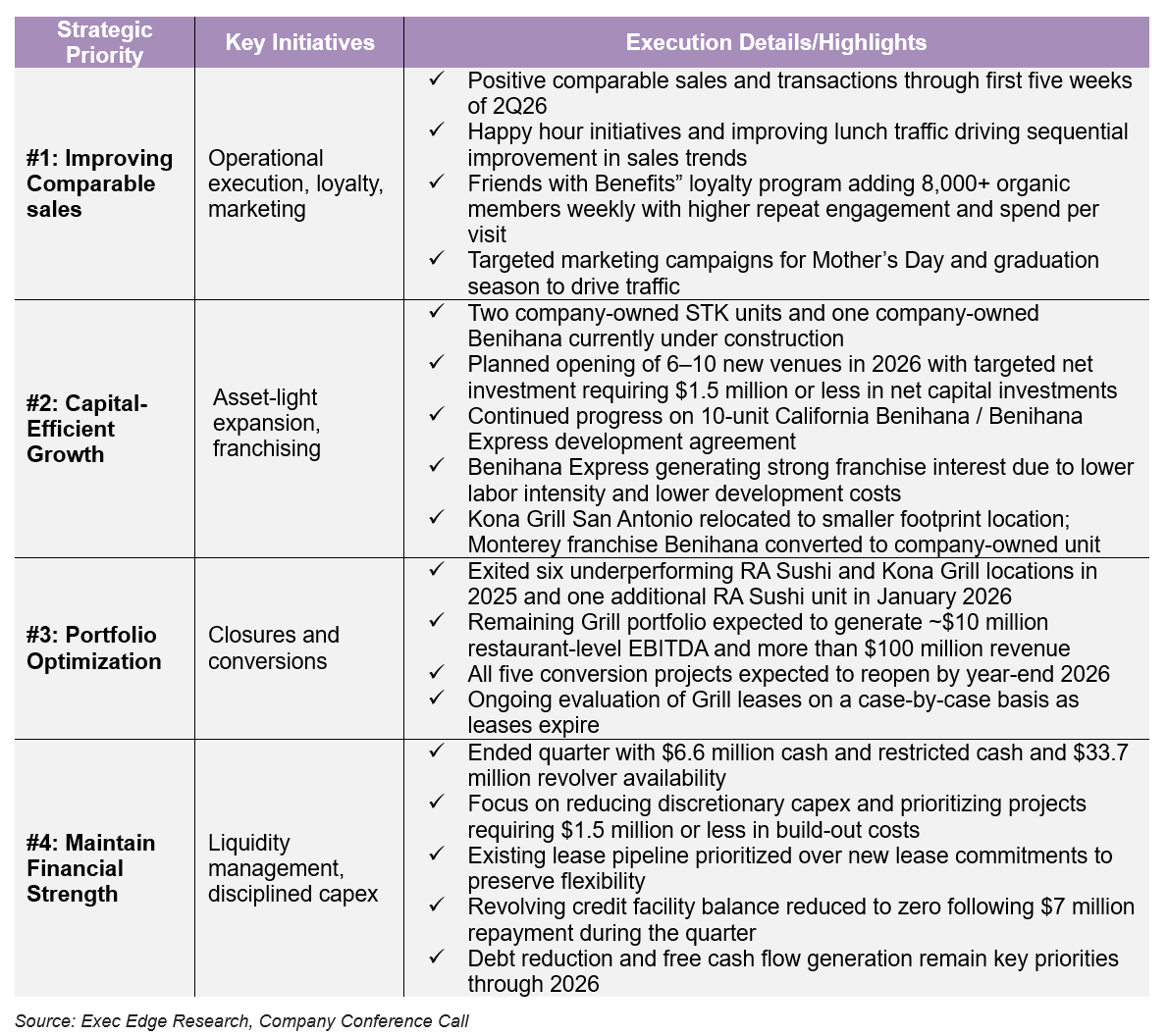

- Improving traffic trends and loyalty engagement across brands were supported by holiday demand, value initiatives, and seasonal menu innovation. STKS noted that Valentine’s Day 2026 represented a record sales day for the portfolio, while Easter sales increased high single digits y/y across brands, reflecting continued strength in celebration-based dining occasions. Through the first five weeks of 2Q26, the company reported positive comparable sales and transactions, with STK and Benihana generating positive comps and Grill Concepts sequentially improving. Happy hour initiatives, improving lunch traffic, operational enhancements, and encouraging early traction from Benihana’s newly launched “Power Lunch” offering featuring ~$15 price points and a 45-minute service guarantee were cited as key drivers of recent momentum. The Friends with Benefits loyalty program continues to scale, adding over 8,000 organic members weekly since launch, with loyalty members demonstrating higher spend per visit and repeat engagement relative to non-members. STKS also highlighted targeted marketing initiatives for upcoming Mother’s Day and graduation occasions, alongside continued seasonal innovation through quarterly food and beverage menu refreshes across all brands.

- Consumer demand trends remained broadly stable across markets, although modest softness persisted within Texas, specifically Dallas, due to elevated competitive intensity. Outside of Texas, performance trends remained relatively consistent across markets, while bookings entering Mother’s Day and graduation season remained strong. Reservation books also continued building positively entering 2Q26, supporting confidence in near-term sales guidance and suggesting experiential dining demand remains relatively resilient despite broader macro uncertainty.

- Traffic-driving initiatives across loyalty, marketing, events, and off-premise channels are becoming increasingly central to the STKS operating story rather than merely supporting comparable sales trends. Targeted marketing, lunch initiatives, and happy hour promotions are contributing directly to traffic growth and guest acquisition. Importantly, recent comparable sales improvement has been driven more heavily by traffic gains than pricing, representing an important distinction in the current restaurant environment.

- Off-premise and convenience-oriented initiatives also continue gaining traction and may represent an underappreciated longer-term growth opportunity. STKS highlighted strong demand for burger offerings, side items, and Benihana’s burrito-style off-premise products, while takeout and delivery currently remain only a low double-digit percentage of total sales. The company continues targeting higher off-premise mix over time through stronger curbside capabilities, product innovation, and reduced reliance on third-party delivery platforms, positioning off-premise as both an incremental revenue driver and customer acquisition channel.

- Capital-efficient expansion remains a key strategic focus, with disciplined development spending and a continued emphasis on high-return projects. STKS has two company-owned STK restaurants and one company-owned Benihana restaurant under construction, including an STK in Phoenix, a relocation of STK Downtown NYC, and a Benihana in Seattle. The company reiterated plans to open six to 10 new venues in 2026, while prioritizing projects requiring $1.5 million or less in net capital investment. 1Q26 capex, net of tenant improvement allowances, declined 22% y/y to $10 million, of which $6.5 million was allocated toward new restaurant construction, with the balance supporting existing locations, reflecting a continued focus on disciplined capital allocation and free cash flow generation.

- Franchise development and portfolio optimization initiatives continued to progress, supported by growing interest in the asset-light Benihana Express format. STKS continued progress on its 10-unit California Benihana and Benihana Express development agreement, while planned franchise and licensed Benihana Express locations in the Florida Keys remain on track. Management highlighted sustained franchise interest in the Benihana Express concept, driven by lower labor intensity, smaller footprints, and lower development costs relative to traditional teppanyaki formats. The format could also become an increasingly important long-term driver of capital-light growth and recurring franchise revenue. In January, the company also relocated its Kona Grill in San Antonio to a smaller-format location and converted a franchise Benihana in Monterey into a company-owned restaurant following the retirement of a long-term franchise partner, with both initiatives performing in line with expectations.

- Portfolio optimization and conversion initiatives remain ongoing, with management prioritizing operational execution and disciplined pacing of reopenings. STKS continues to convert lower-performing Grill locations into higher-performing STK and Benihana formats, having exited six underperforming Grill Concept locations during 2025 and one additional RA Sushi location in January 2026 that did not meet conversion criteria. The remaining Grill portfolio is expected to generate approximately $10 million in restaurant-level EBITDA and over $100 million in revenue. Five Grill locations were closed in January 2026 for conversion into STK or Benihana units, with construction currently underway and reopenings now expected by year-end 2026 versus the previously discussed July 2026 timeline. The revised timing is driven primarily by operational considerations, including training cycles and the sequencing of opening teams, rather than construction-related delays. Each conversion is expected to require $1-$1.5 million of investment and be EBITDA accretive, with management citing the Scottsdale RA Sushi-to-STK conversion as a proof point, where annualized sales increased by over $4 million to a run rate exceeding $7 million.

- Underlying profitability improved meaningfully during 1Q26, although preferred equity accretion continued weighing on earnings attributable to common shareholders. Net income attributable to STKS increased to $3.2 million from $1.0 million in the prior-year quarter. However, preferred stock accretion and paid-in-kind dividend expense of approximately $9.4 million resulted in a net loss attributable to common stockholders of $6.2 million, or $(0.20) per share.

- Adjusted EBITDA growth accelerated meaningfully during the quarter despite elevated marketing, technology, and operational investment spending. Adjusted EBITDA increased 12.1% y/y to $28.8 million from $25.7 million, while operating income increased approximately 30% to $13.9 million from $10.7 million. Importantly, transition and integration expenses declined materially to approximately $0.5 million from $3.7 million in the prior-year quarter as the Benihana integration nears completion.

- General and administrative expense increased during the quarter as STKS continues investing behind infrastructure, technology, and customer acquisition capabilities to support future scalability. G&A expense increased to $15.0 million from $13.1 million, while adjusted G&A excluding stock compensation increased to $13.9 million from $11.5 million. Adjusted G&A as a percentage of revenue increased to 6.5% from 5.4%, driven by salary inflation, technology investments, AI-related initiatives, audit expense, and elevated marketing investment.

- Restaurant-level profitability continued improving across the portfolio despite ongoing closure-related disruption and incremental investment spending. Restaurant operating expenses improved 40 bps y/y to 61.7% of restaurant revenue from 62.1%, reflecting labor optimization and improved scheduling efficiency. Restaurant Operating Profit excluding closed Grill locations increased 11% to $39.9 million, while Restaurant Operating Profit margins expanded 100 bps to 19.1%. STK restaurant-level margins expanded 280 bps to 21%, while Benihana restaurant-level margins improved 130 bps to approximately 21%, reflecting improving operating leverage and procurement synergies despite softer traffic at certain STK mall locations.

- Margin commentary remained constructive despite expected seasonal variability during 3Q26. STKS noted that 3Q historically represents the company’s lowest-margin quarter due primarily to seasonal volume dynamics. Nevertheless, the company maintained confidence in the broader margin outlook given continued momentum in cost of goods sold, procurement initiatives, and operational execution.

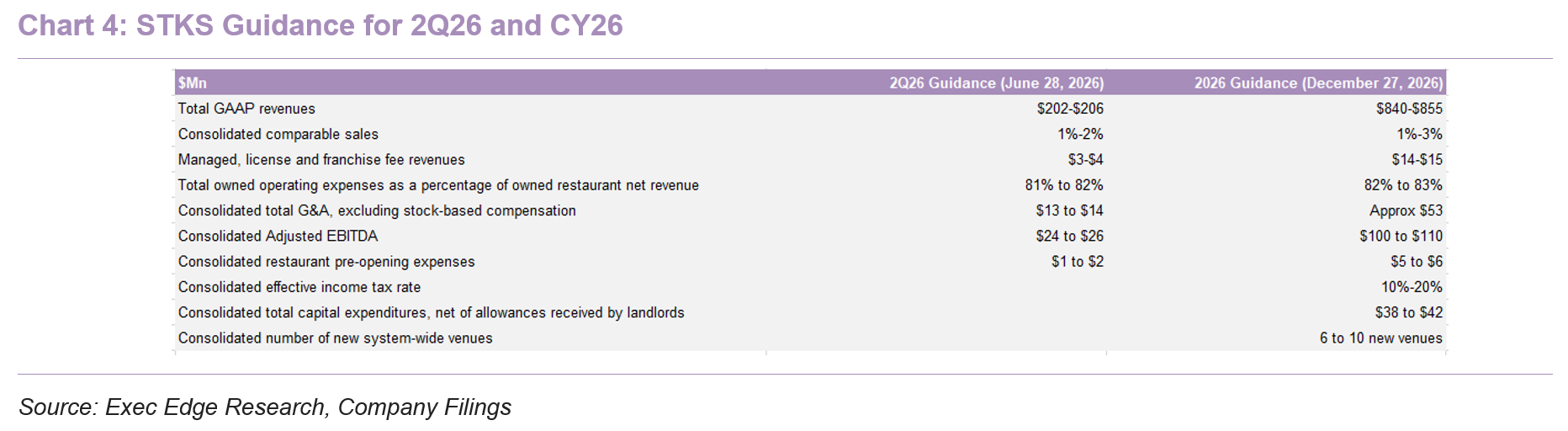

- Management maintained its broader 2026 outlook, with 2Q26 guidance reflecting continued confidence in traffic trends, margin progression, and synergy realization. For 2Q26, STKS guided toward revenue of $202 million-$206 million, consolidated comparable sales growth of 1%-2%, and adjusted EBITDA of $24 million-$26 million. Management also guided toward owned operating expenses of 81%-82% of restaurant revenue and adjusted G&A of $13 million-$14 million.

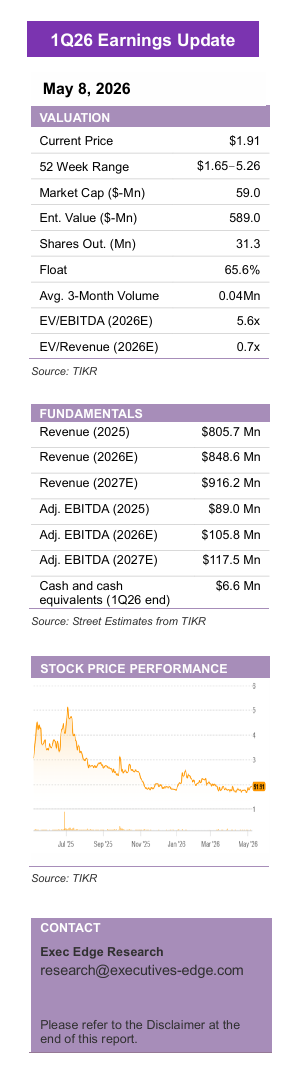

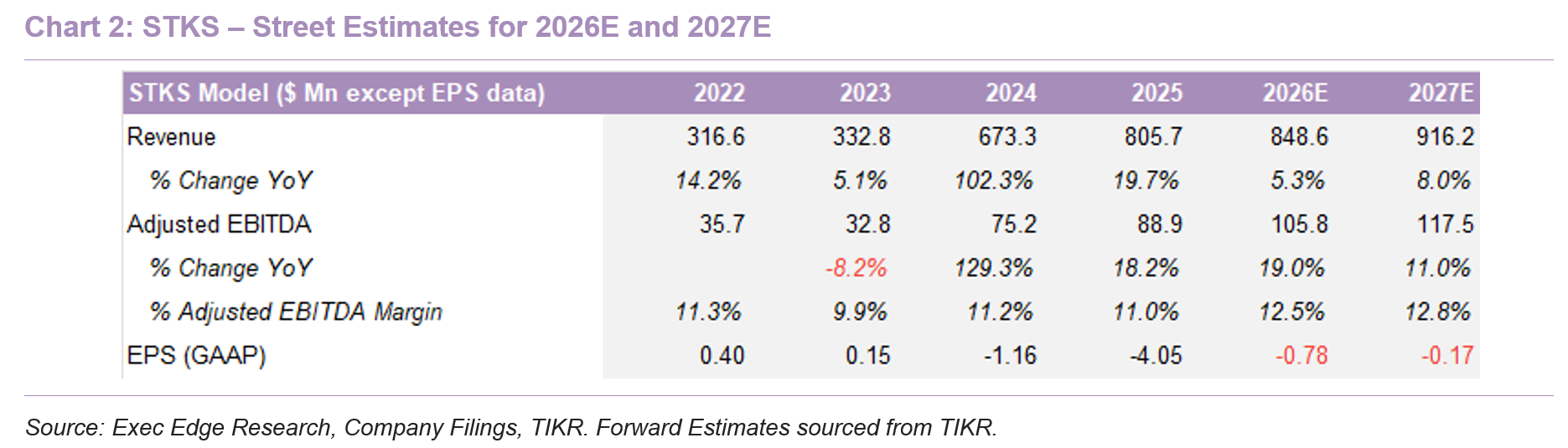

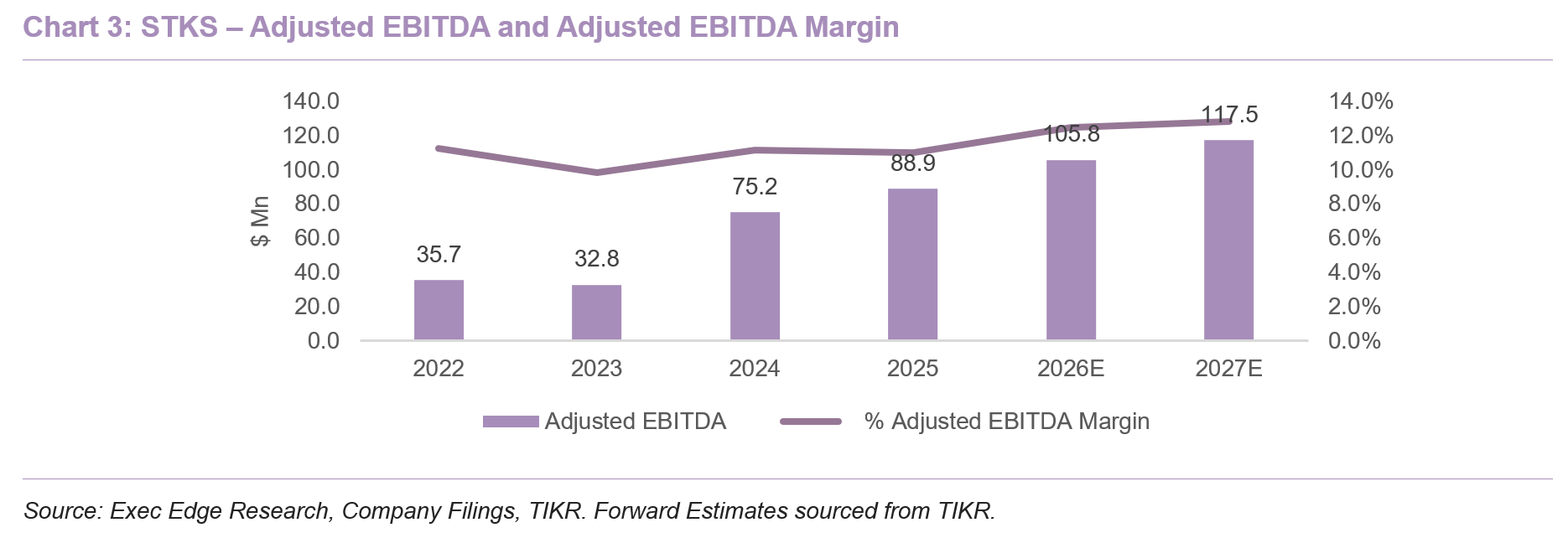

- Full-year guidance implies continued EBITDA growth and free cash flow improvement. For CY26, STKS reiterated guidance for revenue of $840 million-$855 million, consolidated comparable sales growth of 1%-3%, and adjusted EBITDA of $100 million-$110 million. Full-year capex guidance remains between $38 million and $42 million, while the company expects to open six to 10 new venues during 2026. Street estimates sourced from TIKR show STKS is expected to generate $848.6 million in revenue in 2026, followed by $916.2 million in 2027. Adjusted EBITDA is estimated to reach $105.8 million in 2026 and $117.5 million in 2027.

- Balance sheet flexibility improved meaningfully as management prioritized revolver paydown and debt reduction. STKS ended the quarter with approximately $6.6 million in cash and restricted cash alongside approximately $33.7 million available under its revolving credit facility. The company fully paid down its revolver during the quarter following ~$7 million of revolver repayments and ~$2 million of term-loan repayments. Total long-term debt declined to approximately $335 million from $343 million at year-end 2025.

- Working capital trends and free cash flow generation improved materially during the quarter and remain increasingly important as investors focus on deleveraging and liquidity flexibility. Operating cash flow increased sharply to approximately $21.7 million compared to roughly $9 million during the prior quarter, driven by improved profitability and collections associated with holiday credit card receivables. Credit card receivables declined from $19.5 million at year-end 2025 to $11.8 million during 1Q26, while accounts receivable declined from $15.4 million to $11.0 million. Inventory also declined modestly to $9.4 million from $9.8 million, suggesting improving procurement discipline and inventory management.

- Interest expense and financing pressure remain meaningful but are beginning to moderate as leverage gradually improves. Weighted-average interest rates improved to 10.2% from 10.9% in the prior-year period, reflecting lower benchmark rates and improving financing conditions. Management also reiterated that the company currently has no active leverage covenant under current revolver utilization levels, which preserves additional liquidity flexibility.

STKS – An Undervalued Full-Service Dining Player with Improving Fundamentals

- Valuation remains attractive. Please note that the following analysis is for illustrative purposes only and does not constitute a stock recommendation, price target, or a buy/sell/hold view. Based on our analysis, STKS appears undervalued within the full-service dining sector. This assessment is supported by multiple approaches, including historical (time-series) valuation and relative comparison against trading peers. While we do not assign a formal price target, the current valuation suggests potential for re-rating as fundamentals improve.

- Improving traffic trends, expanding margin visibility, and continued balance sheet discipline support a more constructive operating outlook and potential valuation re-rating. Comparable sales and transaction trends turned positive entering 2Q26 across STK and Benihana, suggesting improving underlying demand trends. Momentum in lunch traffic, happy hour initiatives, and loyalty engagement also continued improving during the quarter, while the Friends with Benefits platform continues driving higher repeat engagement and spend per visit. At the same time, contracted beef pricing through September 2026, ongoing procurement synergies, portfolio optimization initiatives, and disciplined cost controls continue improving margin visibility and free cash flow potential. With leverage gradually improving, integration expenses declining, and capital-efficient growth initiatives such as Benihana Express gaining traction, continued execution against these priorities could support further EBITDA expansion, improving free cash flow generation, and potential valuation re-rating over time.

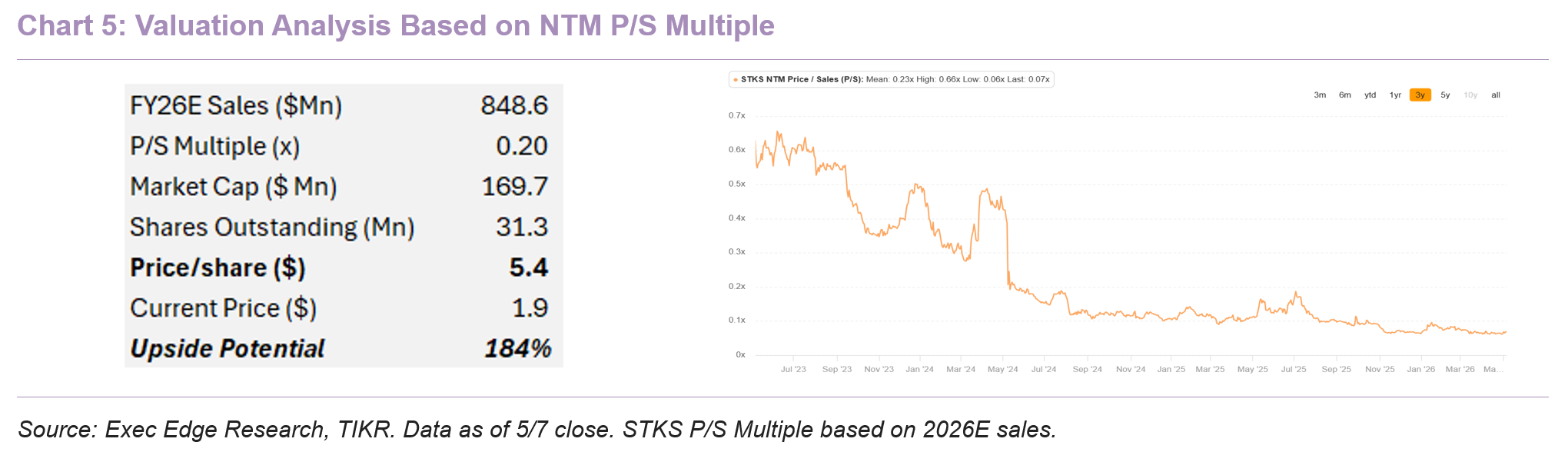

- P/S Multiple analysis. We analyzed STKS’ NTM P/S multiple and note that the stock is trading at its lowest multiple in the last three years. Current P/S multiple of 0.07x is well below the 3-year mean of 0.23x. As fundamentals strengthen, STKS could see multiple expansion over time. Conservatively, even if the stock was to re-rate to 0.20x P/S, STKS could be valued at $5.4/share, representing significant upside relative to current levels.

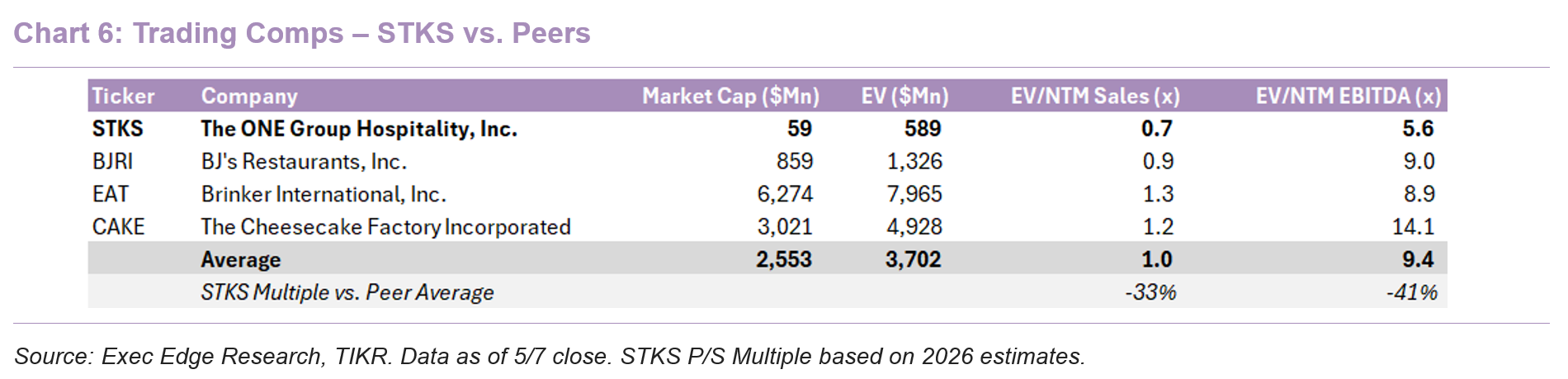

- Peer analysis (relative valuation). Peer valuation analysis also suggests undervaluation. As of 5/7 close, STKS was trading at 5.6x EV/NTM EBITDA, which is a ~40% discount to peer average of 9.4x. Its EV/NTM Sales multiple of 0.7x is also a discount to the industry average of 1.0x, suggesting room for re-rating.

Download the Complete Report Here

Read Exec Edge’s Initiation on The ONE Group Here

Subscribe to our Weekly Newsletter to Receive All Research

Contact: