Download the Complete Report Here

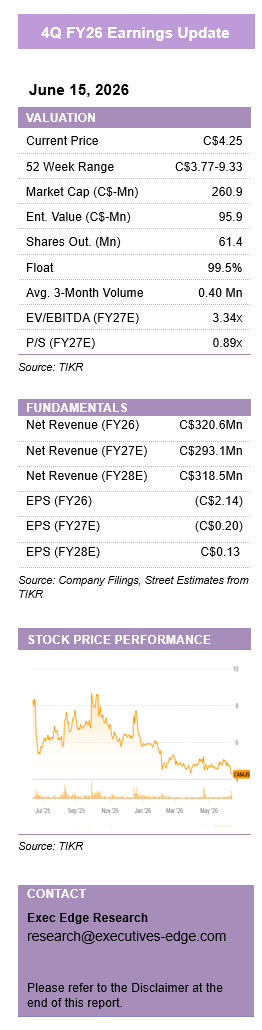

Aurora Cannabis Inc. (ACB)

Aurora Cannabis Inc. (ACB)

Y26 Beat Underscores Medical Cannabis Momentum; FY27 Reset Reflects Canadian Reimbursement Cut, but Long-Term Growth Remains on Track.

- Key Takeaways:

- FY26 topped management’s outlook, with net revenue up 11% to C$320.6 million and medical cannabis revenue up 18%.

- 4Q revenue grew 10% y/y to C$84.8 million, with medical cannabis reaching 91% of total net revenue.

- Bevo divestiture, consumer wind-down, and Safari acquisition sharpen ACB’s focus on higher-return global medical cannabis.

- FY27 reflects a pricing-driven reset as Canadian reimbursed pricing falls ~30%, despite continued Germany and Poland growth.

- Valuation remains attractive at 0.89x FY27E P/S, below ACB’s historical average and cannabis peer group.

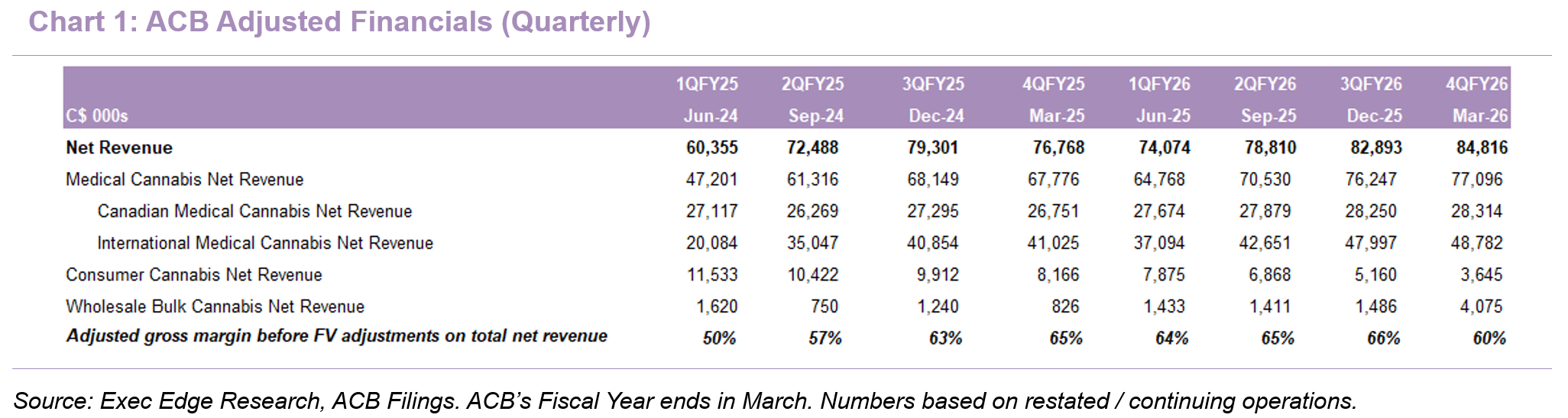

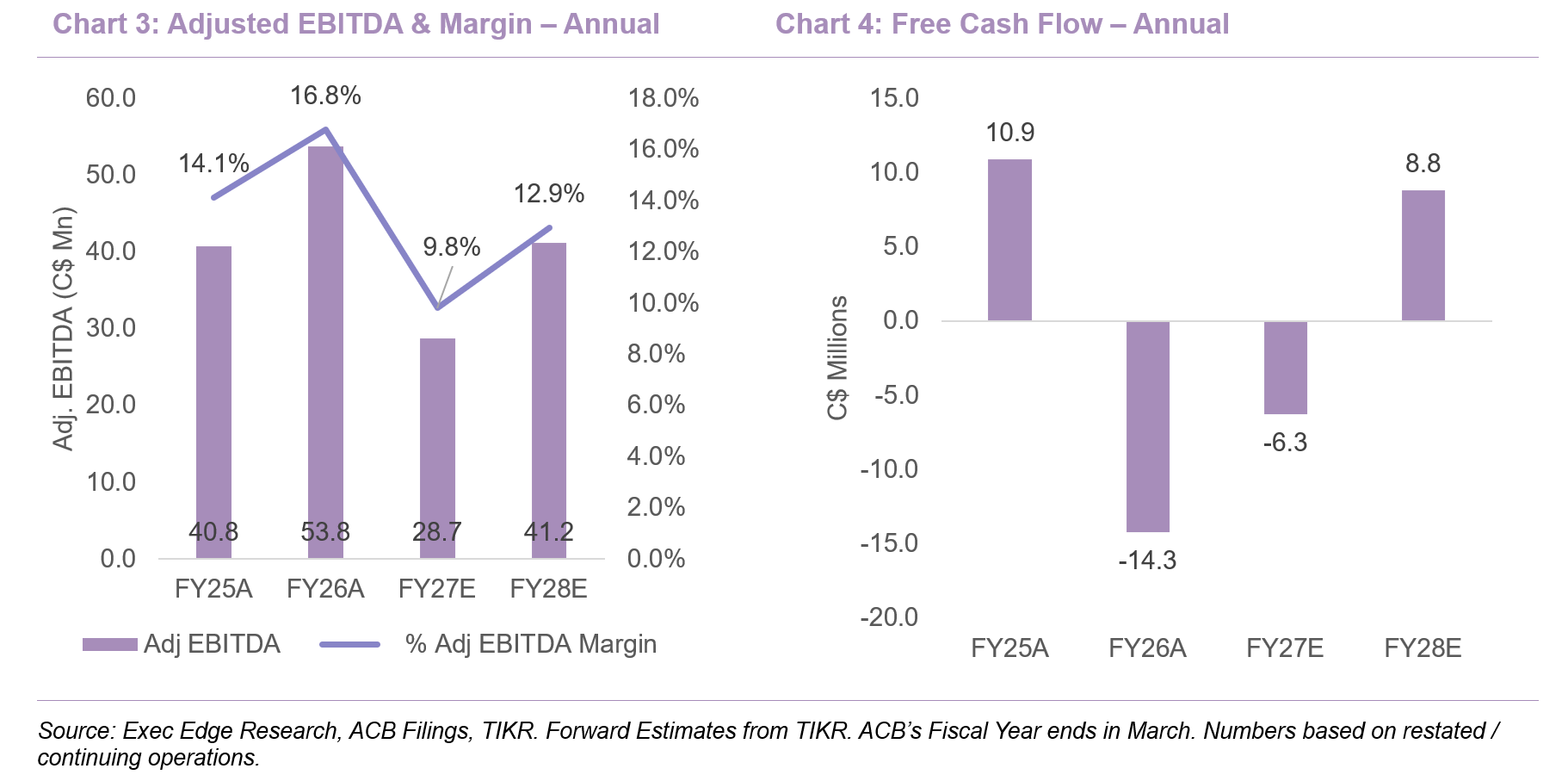

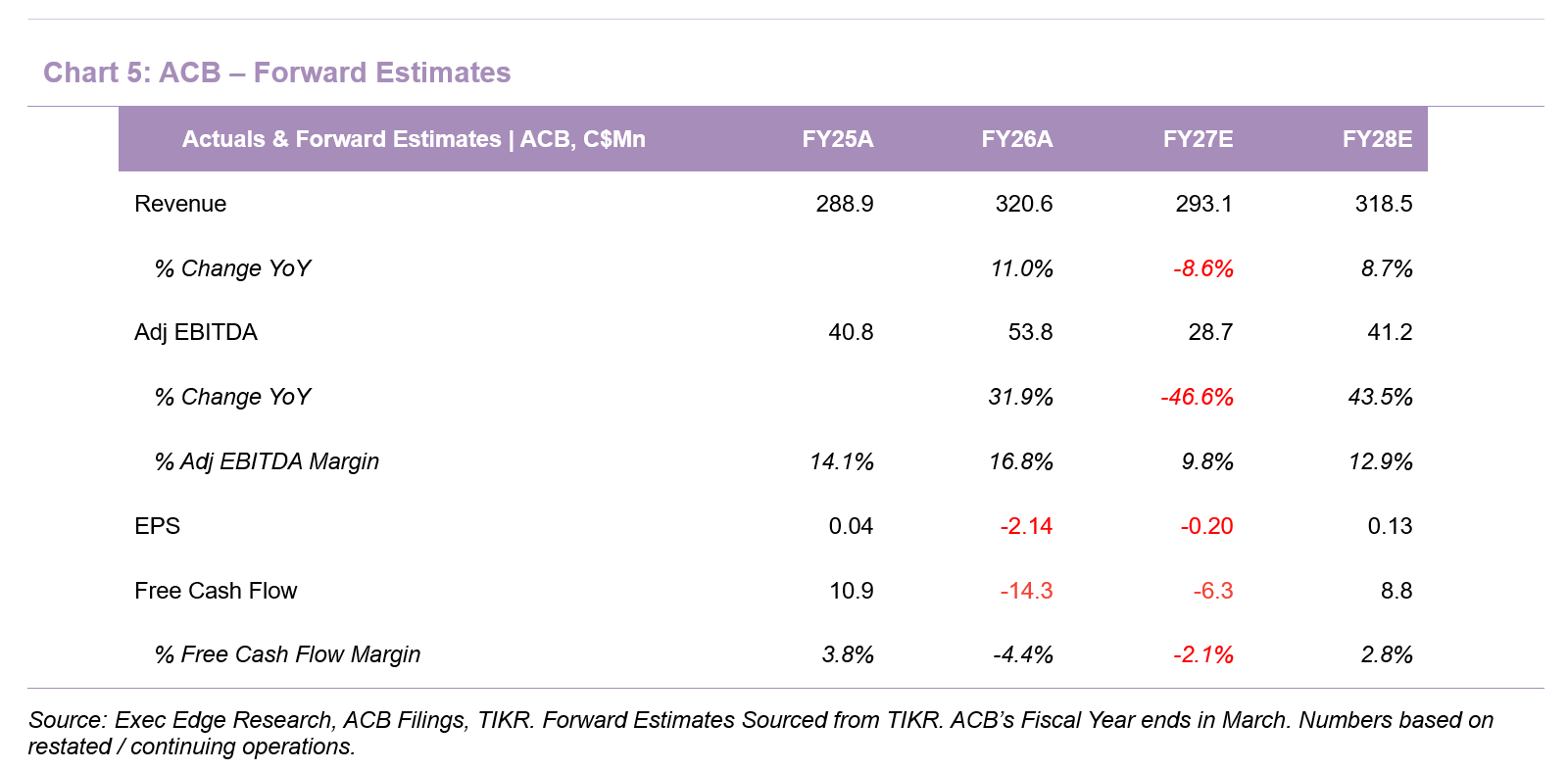

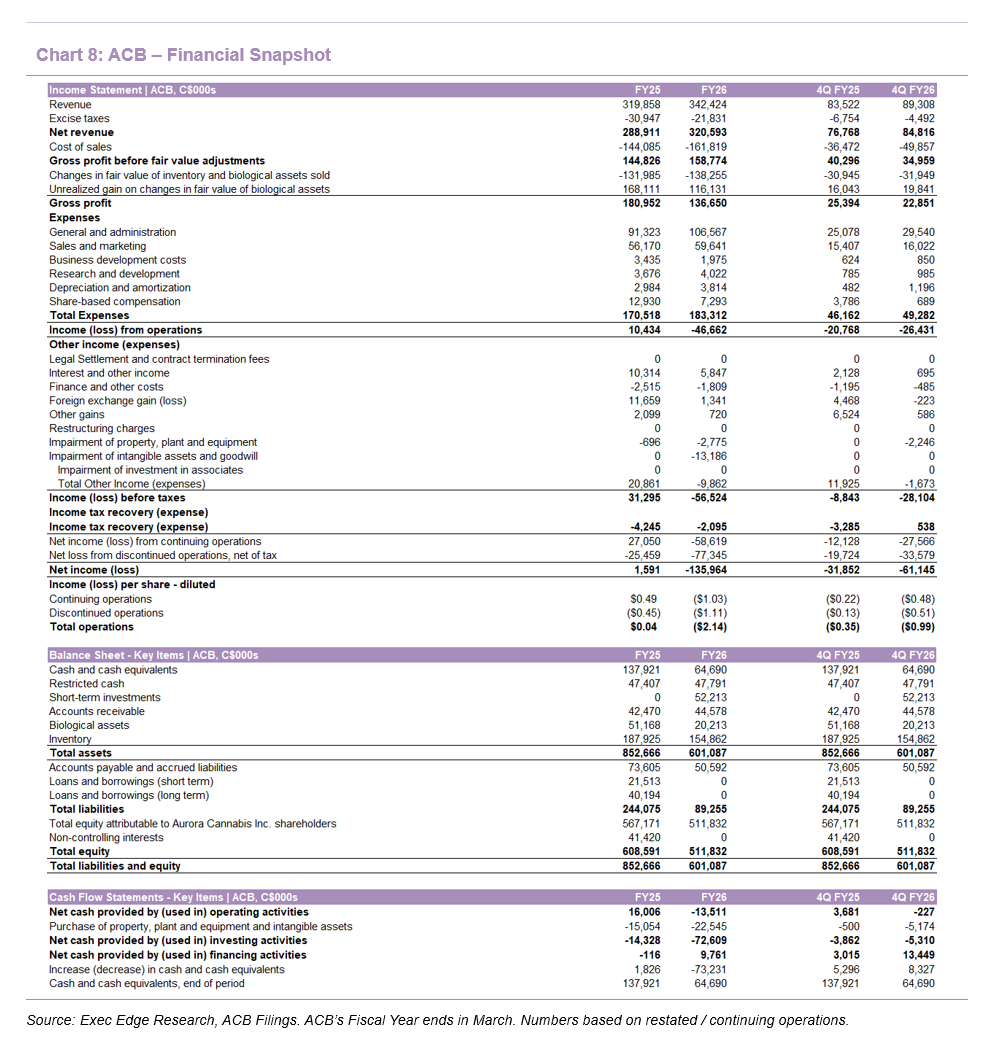

- FY26 topline exceeded management’s outlook, validating ACB’s global medical cannabis strategy. ACB reported FY26 net revenue of C$320.6 million, up 11% y/y, exceeding the top end of management’s prior outlook by approximately C$8 million. This beat was driven by double-digit growth in global medical cannabis and record annual medical cannabis net revenue of C$288.6 million, up 18% y/y from C$244.4 million. The performance reflected the effectiveness of the company’s medical-first strategy, with international medical cannabis revenue increasing C$39.5 million y/y to C$176.5 million and roughly 55% of annual net revenue generated outside Canada. Adjusted EBITDA also reached a record C$53.8 million, up 32% y/y.

- 4Q results were consistent with the strategic transition, with medical cannabis growth offsetting the planned consumer wind-down. ACB reported 4Q FY26 net revenue of C$84.8 million, up 10% y/y, led by 14% growth in medical cannabis revenue to C$77.1 million and 19% growth in international medical cannabis revenue to C$48.8 million. Medical cannabis represented 91% of consolidated net revenue versus 88% in the prior-year period, while 58% of total net revenue was generated outside Canada, reflecting the continued shift toward international medical markets. Consumer cannabis declined 55% y/y to C$3.6 million as ACB intentionally winds down lower-margin Canadian consumer exposure, with the exit from certain lower-margin Canadian consumer markets expected to be completed by the end of September.

- Margins remained strong at the medical segment level, but 4Q reflected mix pressure, strategic price reductions, and third-party sourcing costs. Consolidated adjusted gross margin before fair value adjustments was 60% in 4Q FY26, down from 65% in the prior-year period, while adjusted gross profit before fair value adjustments was essentially flat y/y at C$50.5 million versus C$50.2 million. Medical cannabis adjusted gross margin was 66%, down from 71% y/y, driven by lower-margin product mix, strategic price reductions in certain markets, and some third-party sourcing cost pressure.

- EBITDA softened in 4Q, but FY26 profitability still improved materially and came in within management’s guided range. Adjusted EBITDA was C$9.2 million in 4Q FY26, down 34% y/y from C$14.1 million and down 50% sequentially from C$18.4 million, consistent with prior expectations for a softer fourth quarter. For the full year, adjusted EBITDA increased 32% to a record C$53.8 million, highlighting the underlying earnings power of the medical cannabis platform even as 4Q absorbed transition costs.

- Adjusted SG&A increased 14% y/y in 4Q FY26 to C$40.3 million from C$35.4 million, reflecting a C$1.9 million expected credit loss tied to two customer insolvencies, higher headcount and contract labor in Europe and Australia, inflation-related labor costs, and higher public-company professional fees.

- 4Q FY26 adjusted net income declined 63% y/y to C$5.6 million from C$15.3 million, while net loss from continuing operations widened to C$27.6 million from C$12.1 million due primarily to a shift from C$11.9 million of other income in the prior year to C$1.7 million of other expense in the current period.

- Free cash flow remained positive at C$0.3 million in 4Q FY26, compared to C$5.2 million in the prior year, primarily reflecting lower gross profit before fair value adjustments.

- Adjusted gross margins remained industry-leading despite 4Q pressure from pricing actions and product mix. Consolidated adjusted gross margin before fair value adjustments was 60% in 4Q FY26 versus 65% in the prior-year period, while adjusted gross profit remained largely stable at C$50.5 million. Medical cannabis margin declined to 66% from 71%, while consumer cannabis margin decreased to 22% from 27%, reflecting strategic price reductions, lower-margin mix, and higher third-party sourcing costs.

- ACB maintains significant financial flexibility, supported by substantial liquidity, no loans or borrowings, and access to additional capital. ACB ended FY26 with approximately C$165 million of cash, cash equivalents, restricted cash, and short-term investments, with no loans or borrowings outstanding, while retaining a shelf prospectus that provides financing flexibility through 2028 and an ATM program authorizing the issuance of up to $100 million of common shares to support growth investments and potential M&A opportunities.

- The Safari Flower acquisition is an accretive strategic step that directly addresses EU-GMP capacity, third-party sourcing risk, and Germany-led growth. ACB acquired Safari Flower Company in April for C$26.5 million, consisting of C$15.0 million in cash, 2.4 million common shares, and C$2.0 million of contingent consideration tied to certain GMP certifications. Safari adds a 59,000-square-foot EU-GMP-certified indoor cultivation and manufacturing facility in Ontario, reducing reliance on third-party purchases and adding capacity for key international markets including Germany, Australia, Poland, and the U.K. Strategically, Safari is a capacity, quality, and margin-control acquisition that strengthens ACB’s EU-GMP production footprint and supports its Germany-led international growth strategy. The facility already operates under standards aligned with ACB’s GMP requirements, and management expects positive adjusted EBITDA contribution in FY27 with incremental benefits in FY28 and beyond as ACB introduces its proprietary genetics, cultivation practices, and existing international operating infrastructure to enhance productivity, profitability, and operating synergies over time.

- Recent product launches across Canada, Europe, Australia, and New Zealand reinforce ACB’s medical-first strategy and demonstrate the scalability of its global GMP platform. ACB expanded its portfolio across dried flower, pre-rolls, and edibles to address patient and prescriber demand for high-quality, consistent products. Importantly, these launches are not one-off events; they reflect the company’s ability to leverage its international GMP supply network to broaden product offerings, deepen penetration in key regulated markets such as Germany and Poland, and support continued growth across its global medical cannabis franchise.

- Germany remains ACB’s most important international growth market, supported by strong commercial execution, market leadership, constructive pricing in core and premium categories, and expanding EU-GMP production capacity. Germany was the largest contributor to international revenue growth in FY26, with ACB maintaining its leading market position despite increasing competition and pricing pressure in the value segment. Management remains constructive on the market, noting that ACB’s business remains concentrated in core and premium products, where pricing has been relatively stable and margins remain attractive, while value-segment pressure has increased amid broader market competition. Importantly, core, premium, and value categories are all continuing to grow, supported by a large and expanding medical market, while Germany’s focus on flower and oil limits exposure to lower-margin formats. Two of ACB’s proprietary cultivars ranked #1 and #3 by sales during the quarter, underscoring the strength of its product portfolio and brand positioning. ACB is also one of only three active in-country producers holding both production and R&D licenses under German cannabis regulations, reinforcing its competitive position. To support future demand, the company is expanding its Leuna facility, which is expected to double annual flower output after expected completion in 1H FY27, while enhancing product quality, improving cost efficiency, and strengthening its ability to serve medical cannabis markets across Europe.

- Australia remains a key international market, with management focused on driving mix improvement through higher-value product offerings. ACB continues to hold a leadership position in the market following the MedReleaf acquisition and views Australia as a large, strategically important medical cannabis market, albeit one characterized by more value-oriented pricing dynamics. Management is actively shifting sales toward core and premium products, leveraging one of the broadest product portfolios outside North America to capitalize on evolving physician and patient preferences. Recent product launches support this mix-shift strategy, while the company’s diversified international platform allows it to balance varying growth trajectories across global medical cannabis markets.

- Poland continues to emerge as a meaningful growth driver, supported by market leadership and strong commercial execution. ACB maintained its #1 market share position and successfully navigated the transition from telehealth-driven prescribing to clinic-based channels. Poland was the second-largest contributor to international growth in FY26 after Germany, with increased import limits and strong regulatory relationships supporting future expansion.

- ACB remains well positioned to capitalize on the expansion of emerging European medical cannabis markets. Management highlighted opportunities across France, Ukraine, Switzerland, Spain, and Austria, noting that its GMP-certified product portfolio, regulatory expertise, and established compliance infrastructure provide a competitive advantage as new jurisdictions open and existing markets continue to evolve.

- ACB’s proprietary genetics, regulatory expertise, and GMP capabilities remain key competitive advantages in highly regulated international medical cannabis markets. The company’s genetics platform supports higher yields, improved consistency, differentiated product attributes, and enhanced disease resistance, which together improve product quality, supply reliability, and cultivation economics. This matters in markets such as Germany and Poland, where product registrations, stability data, import permits, GMP certification, and ongoing regulatory compliance create meaningful barriers to entry. As international medical cannabis markets expand and regulatory standards rise, ACB’s integrated platform should continue to support market share retention, pricing resilience, and margin durability.

- Canadian medical cannabis reimbursement rates for veterans were reduced by ~30% effective April 1, 2026, creating a headwind for licensed producers with exposure to the channel. As part of a revised Veterans Affairs Canada (VAC) reimbursement framework, the maximum reimbursable amount was reduced from C$8.50/gram to C$6.00/gram in April, reflecting the government’s effort to better align reimbursement levels with prevailing market prices following years of industry price compression. Importantly, patient eligibility, prescription authorizations, and covered volumes remain unchanged, suggesting the policy primarily impacts realized pricing rather than underlying demand. Management indicated that the change translates into an approximately 30% reduction in reimbursement-related revenue and, given the largely fixed nature of production costs, is expected to negatively impact both topline growth and adjusted gross margins beginning in FY27. ACB further noted that the reimbursement change is the primary factor driving its expectation for adjusted gross margins to decline into the mid-to-high 50% range in FY27. Notably, early observations since the April 1 implementation suggest limited changes in patient purchasing behavior, with no material shift in product formats, price points, or prescribing patterns observed to date. While international growth, particularly in Germany and Poland, is expected to partially offset the pressure, the reimbursement revision remains the primary driver of ACB’s lower FY27 revenue and EBITDA outlook and should be viewed primarily as a pricing reset rather than evidence of weaker patient demand or operational execution.

- Potential U.S. cannabis rescheduling could create new long-term opportunities for established medical cannabis operators with GMP and regulatory expertise. On April 23, 2026, the U.S. Department of Justice issued a final order moving FDA-approved drug products containing marijuana and medicinal marijuana products subject to qualifying state-issued licenses from Schedule I to Schedule III, while a separate process remains ongoing to evaluate broader changes to marijuana’s federal status. Management views the development as a positive step toward a more federally regulated medical cannabis framework in the U.S. Given ACB’s position as one of Canada’s largest exporters of GMP-manufactured medical cannabis and its experience operating in highly regulated international markets, the company is well positioned to evaluate potential opportunities arising from further federal medical cannabis reform, although no specific U.S. strategy has been announced.

- ACB views potential U.S. federal cannabis reform as a long-term strategic opportunity across research, partnerships, and potential cross-border medical cannabis trade. While regulatory clarity remains pending, ACB highlighted three potential avenues for participation in the U.S. market. First, the company sees a significant opportunity in medical cannabis research, leveraging its decade-plus clinical, regulatory, and commercial experience to partner with universities, healthcare institutions, and private-sector organizations. Second, management identified potential partnership opportunities where ACB’s GMP-certified production capabilities and expertise in regulated medical cannabis markets could support U.S. healthcare and cannabinoid-based initiatives. Third, the company is evaluating the possibility of future import and export opportunities should federal regulations permit cross-border trade of medical cannabis products. While no specific U.S. market entry strategy has been announced, management believes ACB’s medical-focused operating model and international regulatory expertise position the company favorably as the regulatory framework evolves.

- FY27 guidance reflects a pricing-driven reset rather than any deterioration in ACB’s core operating execution, with Canadian reimbursement pressure more than offsetting international growth and portfolio cleanup. Management expects FY27 total net revenue to decline and be more in line with FY25 cannabis net revenue, following the Canadian medical reimbursement change effective April 1, 2026, partially offset by international growth driven by Germany and Poland. We note that the key issue is not operational execution, but pricing: the reimbursed rate for affected Canadian medical products is being reduced by approximately 30%, which directly pressures revenue and gross profit contribution from an otherwise high-quality direct-to-patient medical business. Adjusted gross margin before fair value adjustments is expected to be in the mid-to-high 50s, compared with 64% in FY26, as higher European revenue and the exit from lower-margin consumer and plant propagation businesses only partially offset lower Canadian medical reimbursement margins. Adjusted SG&A is expected to remain broadly in line with FY26, when adjusted SG&A was C$146.1 million, while adjusted EBITDA is expected to vary quarter to quarter and decline for the full year from FY26’s C$53.8 million record level. Overall, the FY27 setup reflects a pricing-driven reset rather than a change in the company’s international medical cannabis growth strategy, with Germany, Poland, Safari capacity, and the consumer/Bevo exits expected to support a cleaner growth base beyond the transition year.

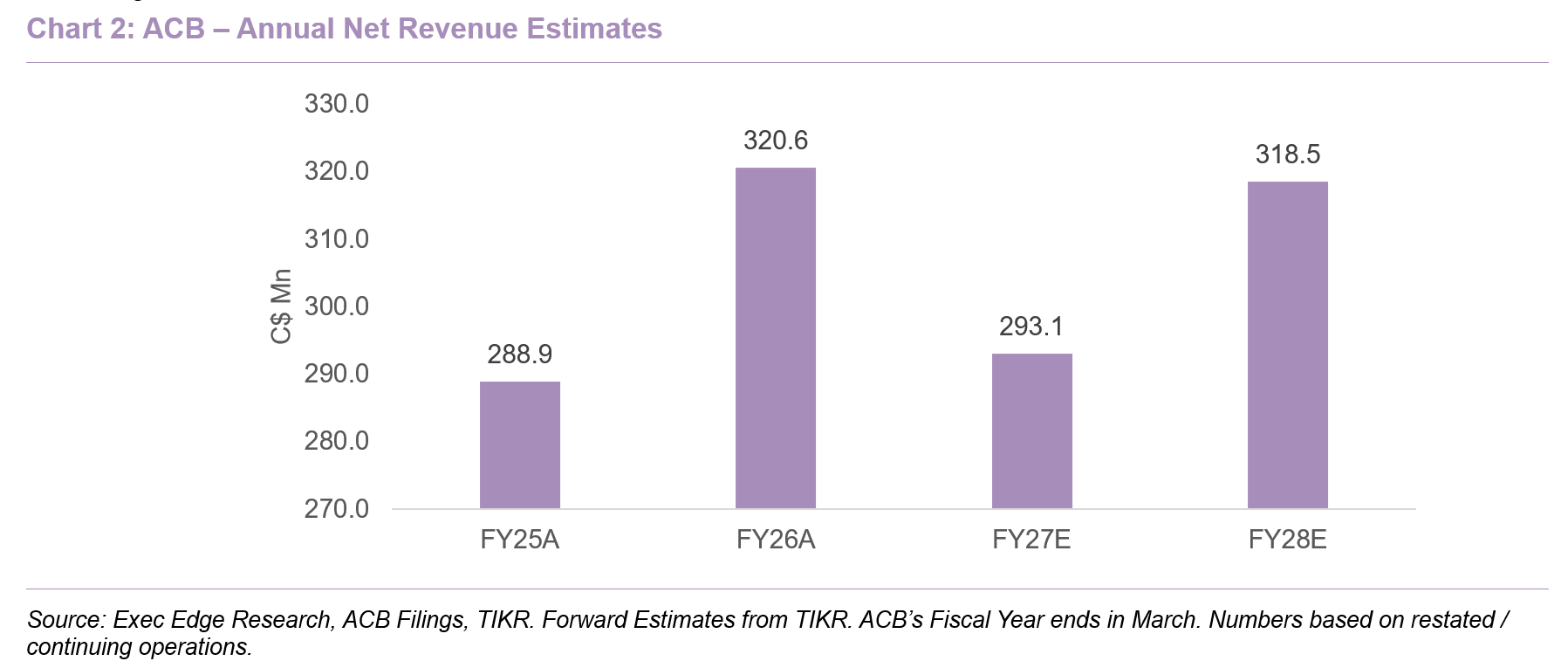

- Street estimates also reflect that FY27 is expected to be a transition year before growth reaccelerates in FY28. Based on Street estimates sourced from TIKR, revenue is projected to decline from C$320.6 million in FY26 to C$293.1 million in FY27E, reflecting the impact of lower Canadian medical reimbursement rates and the company’s exit from lower-margin businesses. Adjusted EBITDA is expected to decline to C$28.7 million from C$53.8 million in FY26, with margins compressing to 9.8% as the reimbursement changes flow through results. Looking further out, revenue is estimated to recover to C$318.5 million in FY28E, while adjusted EBITDA is expected to rebound to C$41.2 million, implying a margin of 12.9%, supported by continued international medical cannabis growth and operational improvements.

- Free cash flow is expected to improve gradually from the FY26 trough. Based on current Street estimates, free cash flow is projected at approximately negative C$6.3 million in FY27E, an improvement from negative C$14.3 million in FY26A, before returning to positive territory at roughly C$8.8 million in FY28E. The expected recovery reflects improving operating efficiency, a more focused business mix following the exit from lower-return businesses, and an increasing contribution from international medical cannabis markets as the FY27 reimbursement reset is absorbed.

- Overall, medium-term growth drivers remain intact despite near-term reimbursement-related headwinds. We believe ACB’s outlook through FY28 continues to be supported by: 1) expanding penetration across key international medical cannabis markets, particularly Germany, Poland, and Australia; 2) incremental EU-GMP capacity from the Safari Flower acquisition and Leuna facility expansion, supporting future supply growth and reduced third-party sourcing; and 3) continued operational improvements, proprietary genetics, and portfolio expansion across core and premium medical products, supporting margin resilience and long-term earnings growth.

Attractive Valuation for a Global Medical Leader

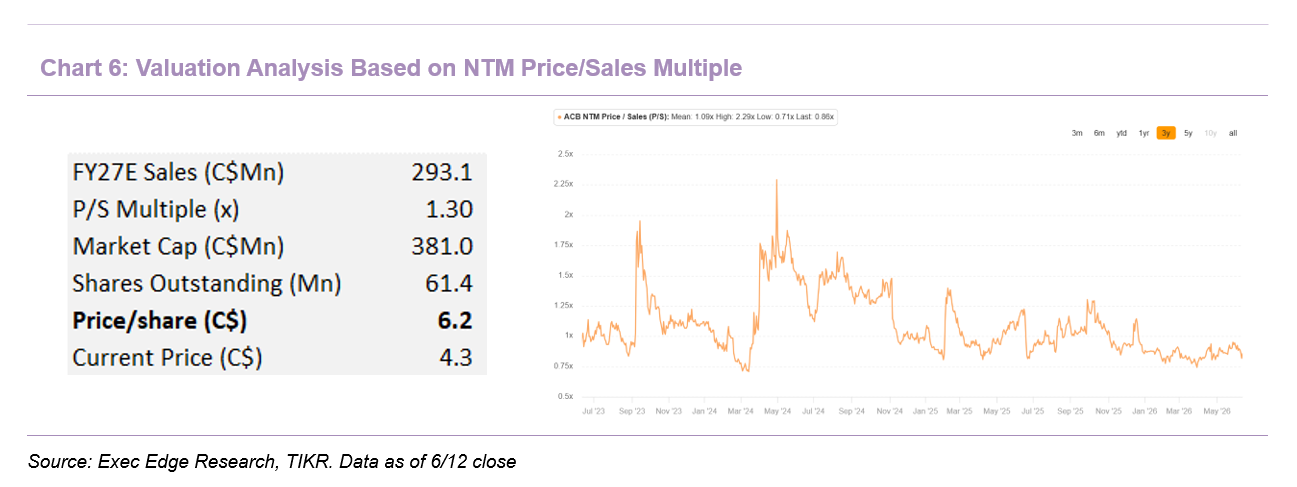

- Valuation remains attractive based on our analysis. The valuation discussion below is illustrative in nature and is not intended to represent a stock recommendation, price target, or a buy/sell/hold opinion. Our analysis incorporates multiple approaches, including historical valuation and peer comparisons. Any implied upside referenced is not a price target and is presented solely to provide context for relative valuation.

- Despite near-term reimbursement-related headwinds, ACB continues to trade at a meaningful discount to both its historical valuation and cannabis peers. We believe the current valuation fails to fully reflect ACB’s leadership position in global medical cannabis, no loans or borrowings, expanding international footprint, and improving long-term cash generation profile.

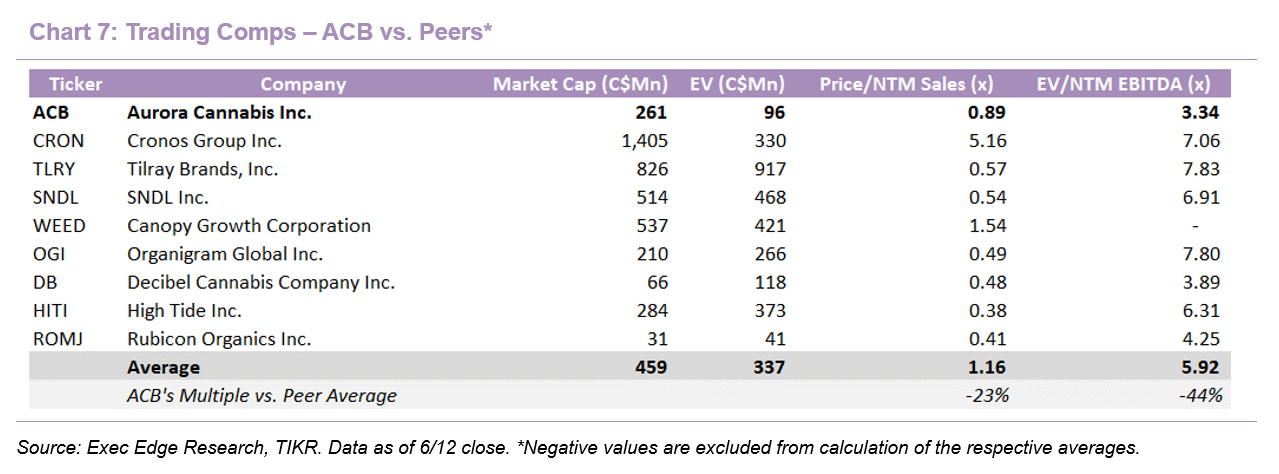

- On a forward basis, ACB trades at 0.89x NTM Price/Sales, representing an 18% discount to its three-year average multiple of 1.09x and a 23% discount to the peer group average of 1.16x. While the valuation discount has widened amid concerns surrounding Canadian reimbursement changes, management reiterated that patient demand remains stable and that the primary impact is pricing-related rather than volume-driven. We believe the market is currently discounting near-term earnings pressure while assigning limited value to ACB’s international growth platform. Applying a 1.3x NTM P/S multiple to FY27E revenue of C$293.1 million implies an equity value of approximately C$381.0 million, or roughly C$6.20 per share. The 1.3x multiple represents a modest premium to ACB’s three-year average multiple, reflecting the company’s strengthened international medical cannabis platform, improving earnings quality, and long-term cash flow potential. While we do not view this as a formal price target, it illustrates the valuation disconnect between Aurora’s current market value and its historical trading range.

- The discount is similarly evident on an earnings basis. ACB is currently valued at 3.34x FY27E EV/EBITDA, a level that we view as inconsistent with a business that is expected to deliver EBITDA growth, margin expansion, and positive free cash generation in FY28E. As the company sharpens its focus on higher-return global medical markets following the Bevo divestiture, we believe EBITDA visibility and quality should continue to improve.

- Overall, we believe current valuation levels inadequately reflect ACB’s long-term competitive positioning and improving quality of earnings. Key differentiators include: 1) leadership positions in Germany, Poland, and Australia; 2) a GMP-led operating model supported by proprietary genetics and regulatory expertise; 3) no loans or borrowings and approximately C$165 million of cash, cash equivalents, restricted cash, and short-term investments; and 4) a growing international medical cannabis platform capable of generating higher-margin and more predictable revenue streams. As near-term reimbursement-related headwinds are absorbed and international growth continues to scale, we believe there is scope for valuation multiples to move closer to historical levels.

Read Exec Edge’s Initiation on ACB Here

Subscribe to our Weekly Newsletter to Receive All Research

Contact: