Download the Complete Report Here

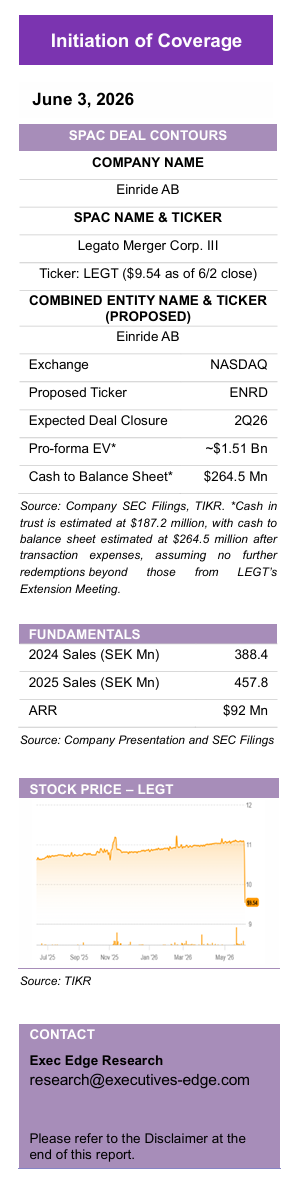

Einride AB (Proposed Ticker: ENRD)

Einride AB (Proposed Ticker: ENRD)

Integrated Freight Platform Scaling Contracted Demand into Electric and Autonomous Deployment

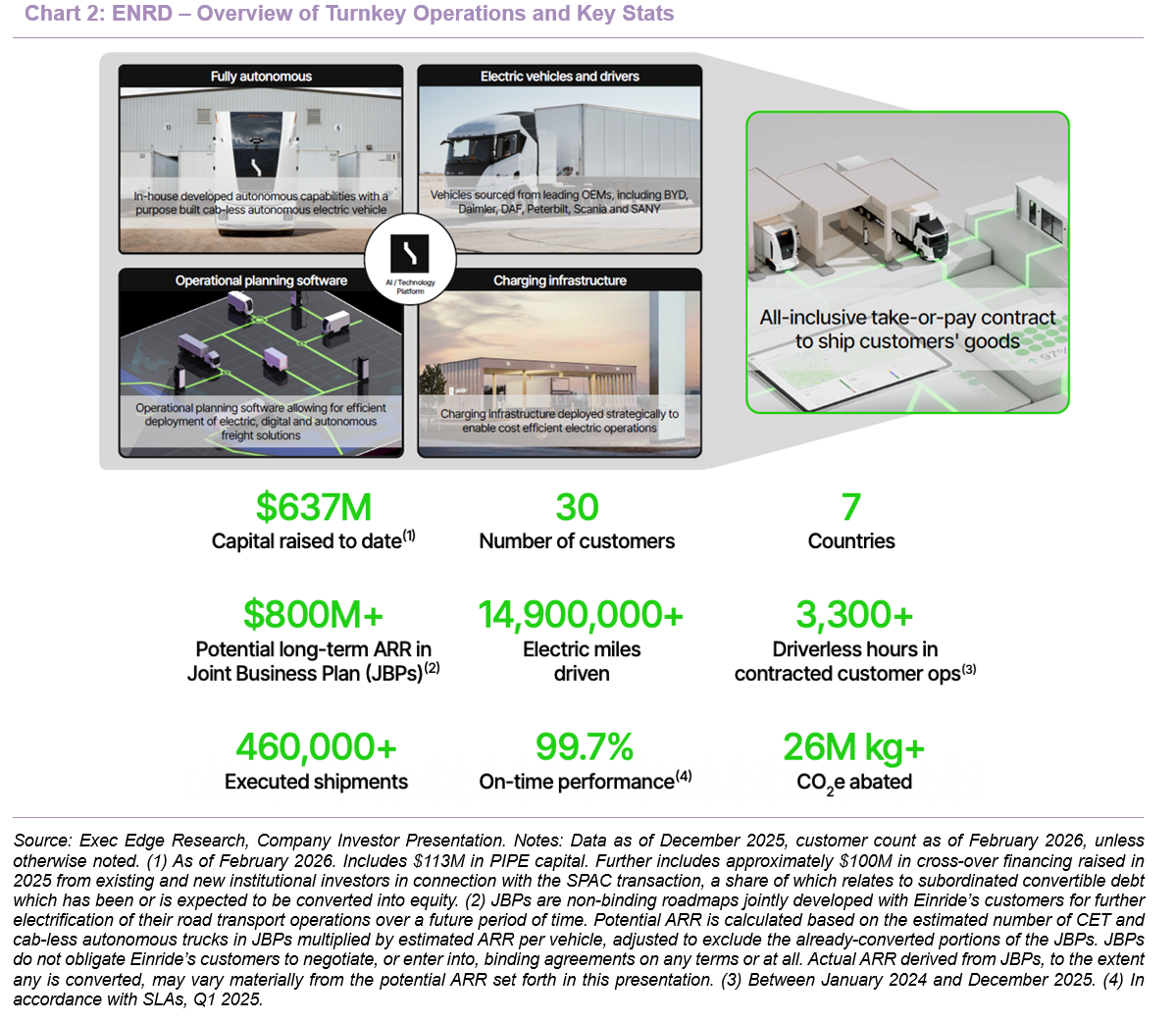

- Einride enters public markets as a commercial freight-technology platform with live electric and autonomous deployment traction. Founded in 2016 and headquartered in Stockholm, ENRD serves 30 customers across seven countries, with $49 million of run-rate operational revenue, $92 million of signed customer contract ARR, and $800 million+ of potential long-term ARR in JBPs. The company has already driven 14.9 million+ electric miles, executed 460,000+ shipments, abated 26 million kg+ of CO2e, and recorded 3,300+ driverless hours in contracted customer operations, differentiating ENRD from concept-stage autonomy platforms while providing a commercial base for scaling FCaaS, Saga AI, charging orchestration, and autonomous freight across North America, Europe, and the Middle East.

- The right-to-win is built around customer-embedded freight orchestration. Saga serves as ENRD’s AI-powered operating layer, connecting transportation systems, vehicles, chargers, route data, telematics, charging data, driver workflows, and emissions reporting. This is paired with FCaaS, which embeds electric freight capacity, charging, operations, maintenance, and software into customer networks through multi-year contracts, creating operational switching costs and compounding deployment data.

- Industry structure supports demand for ENRD’s model. Road freight remains large, fragmented, labor-constrained, energy-volatile, and increasingly reporting-intensive, creating demand for platforms that coordinate vehicles, routes, charging, drivers, autonomy, and customer reporting. ENRD is aligned with these trends through electric trucks, Saga AI, charging infrastructure, cab-less autonomous trucks, and ADS licensing, with autonomy initially focused on controlled, repeatable freight environments.

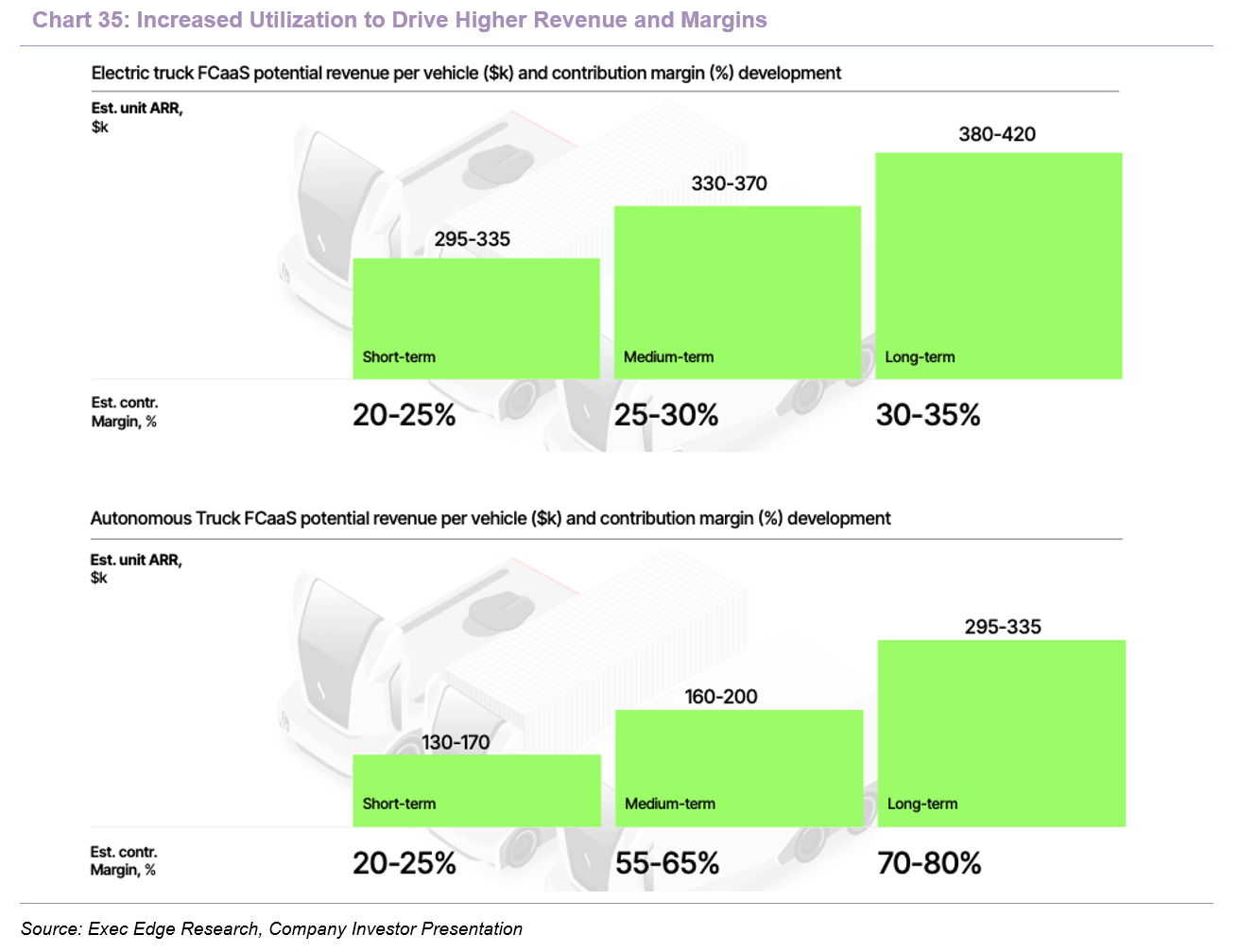

- Financial inflection depends on ARR conversion, utilization, and higher-margin autonomy/software mix. Revenue increased 18% y/y to SEK 457.8 million in 2025, while the business remains investment-stage, with net loss of SEK 1,721.7 million and operating cash use of SEK 741.7 million. The path to financial inflection depends on converting signed ARR and JBPs into deployed revenue, improving FCaaS utilization, and scaling electric, autonomous, and software-led revenue streams. Electric-truck FCaaS targets ~$380K-$420K of annual revenue per vehicle at scale, while autonomous and SaaS mix should improve contribution margin over time.

- Valuation is anchored by contracted demand and commercialization milestones. We do not have price target or stock recommendation on ENRD or LEGT. We do note that at an implied ~$1.51 billion pro forma EV, ENRD is valued at 16.4x EV / signed ARR based on $92 million of signed customer contract ARR. This screens below trucking autonomy peers despite ENRD’s broader software-plus-operations model, deeper shipper embeddedness, and integrated electric/autonomous freight execution. The SPAC transaction provides public-market entry into ENRD at a valuation that leaves room for potential re-rating as signed ARR converts, utilization improves, and autonomy/software revenue scales.

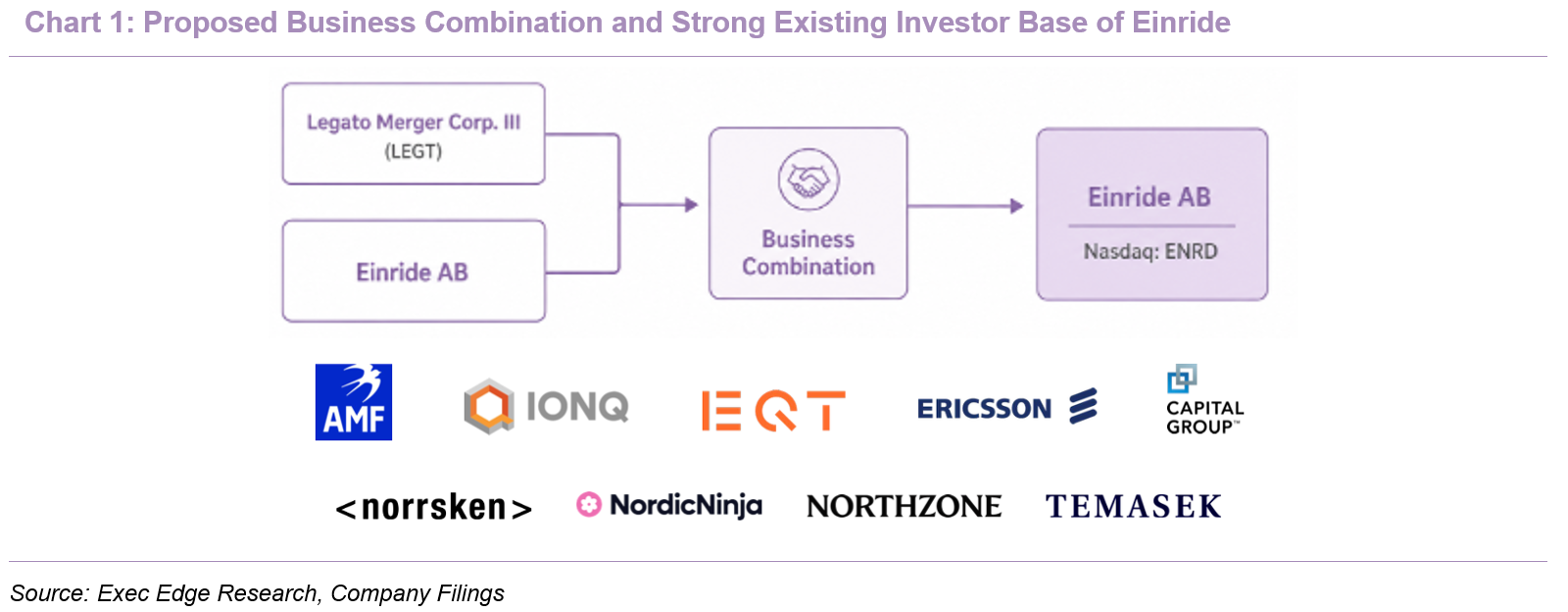

Company and SPAC Deal Overview

Legato Merger Corp. III (LEGT) + Einride AB = Einride AB (NASDAQ: ENRD)

- Einride AB is set to enter the U.S. public markets through a business combination with Legato Merger Corp. III, with the combined company expected to list on Nasdaq under the proposed ticker ENRD. Einride is a Swedish technology company focused on digital, electric, and autonomous freight operations for large shippers, while Legato III is a Cayman Islands SPAC whose public shares currently trade on NYSE American under LEGT. The transaction is structured through a merger of Legato III with Einride Cayman Sub Limited, a wholly owned subsidiary of Einride, after which Legato III will cease to exist and its securityholders will become securityholders of Einride. Einride enters the transaction with a strong existing investor profile, with select existing investors including AMF, IonQ, EQT, Ericsson, Capital Group, Norrsken, NordicNinja, Northzone, and Temasek, reinforcing institutional and strategic validation around the platform before its expected public listing. The F-4 registration statement was declared effective by the SEC on May 14, 2026, and the Legato III shareholder vote to approve the transaction is scheduled for June 4, 2026, for shareholders of record as of May 7, 2026. If the proposals at the June 4 Extraordinary General Meeting are approved, the transaction is expected to close shortly thereafter, subject to the satisfaction or waiver, as applicable, of all other closing conditions. The Nasdaq debut therefore remains a near-term capital markets catalyst, while final timing remains subject to closing mechanics. We refer to Einride with its proposed ticker ENRD throughout this report.

- The transaction values Einride at a $1.35 billion pre-money equity value and implies a pro forma enterprise value of ~$1.51 billion, with existing shareholders expected to retain majority ownership at closing. Assuming no further redemptions beyond those from LEGT’s Extension Meeting held on May 5, 2026, the transaction includes the $113.3 million PIPE and remaining Legato III trust cash of $187.2 million, resulting in estimated cash to the balance sheet of $264.5 million after estimated transaction expenses. Under this scenario, Einride shareholders would own 77.9% of pro forma equity, followed by Legato III public shareholders at 10.4%, PIPE investors at 8.7%, initial shareholders and affiliates at 2.9%, and BTIG at 0.1%. The transaction should provide Einride with a public-market listing and incremental balance sheet flexibility, while final cash proceeds and dilution remain sensitive to any additional redemptions, transaction expenses, warrants, and PIPE-related terms.

- The PIPE adds an important validation layer to the transaction, bringing in ~$113 million of committed capital from new and existing investors, including Stockholm-based EQT Ventures and a U.S. West Coast-based global asset manager. Together with the ~$100 million previously announced crossover financing, investors have committed ~$213 million of financing connected to the transaction. PIPE proceeds are expected to support Einride’s technology roadmap and global expansion, including autonomous deployments across North America, Europe, and the Middle East, as well as broader commercial applications of its intelligent freight platform. Key transaction sensitivities are likely to include final cash delivered at close, post-redemption float, warrant overhang, and the extent to which the added capital supports ENRD’s deployment ramp toward scale.

ENRD – A Turnkey Platform for Electric and Autonomous Freight Transformation

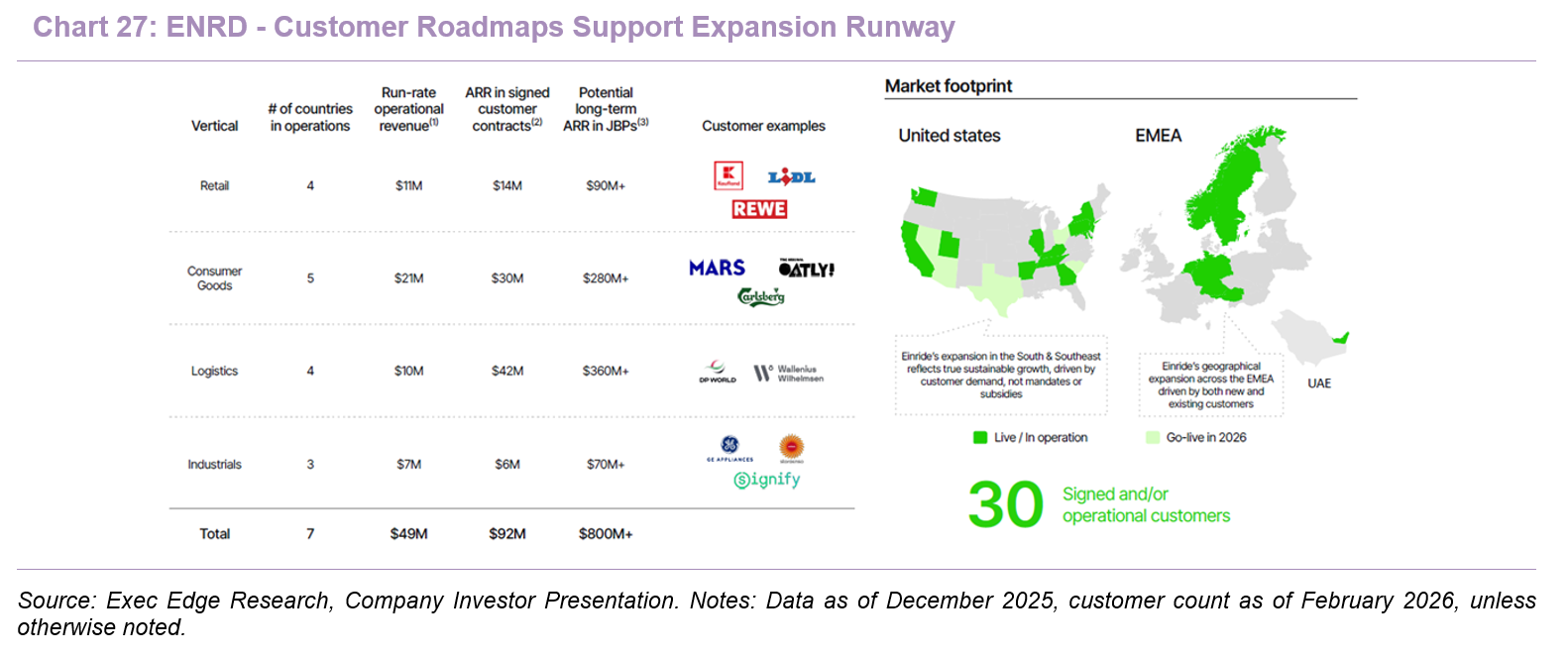

- Einride has built a turnkey freight technology platform designed to help enterprise shippers transition road freight from diesel and manual operations toward electric, autonomous, and digitally optimized capacity. Founded in 2016 and headquartered in Stockholm, ENRD operates across North America, Europe, and the Middle East, with 30 customers across seven countries. The company’s operating snapshot highlights commercial scale, sustainability, and execution quality, with $637 million of capital raised to date (inclusive of the $113 million PIPE and ~$100 million crossover financing), $800 million+ of potential long-term ARR in Joint Business Plans, 14.9 million+ electric miles driven, 460,000+ executed shipments, and 26 million kg+ of CO2e abated. ENRD has also logged 3,300+ driverless hours in contracted customer operations and 99.7% on-time performance, giving it a commercial footprint that is more operationally mature than a pure autonomy developer or an early-stage fleet electrification concept. Importantly, ENRD is not entering public markets as a concept-stage platform, with $49 million of run-rate operational revenue and $92 million of ARR in signed customer contracts. We view this mix of live freight execution, contracted revenue visibility, capital backing, and embedded customer expansion roadmaps as the core foundation of the ENRD investment case.

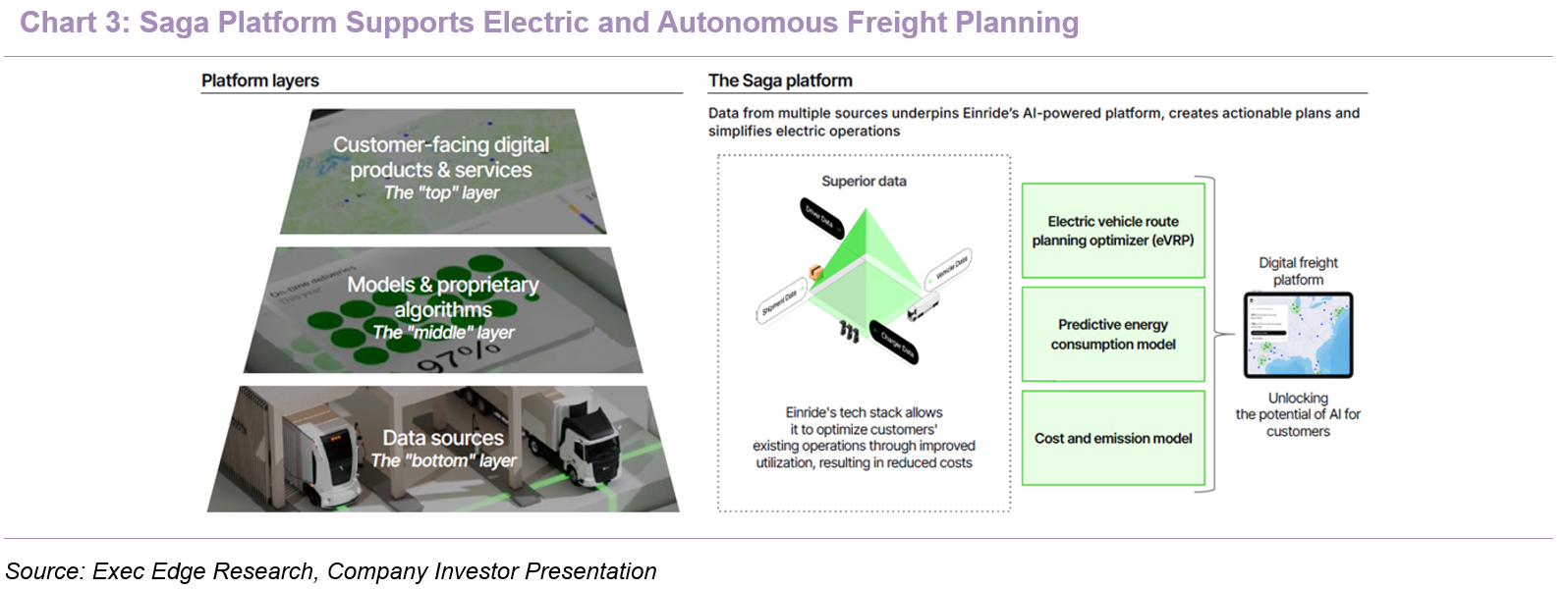

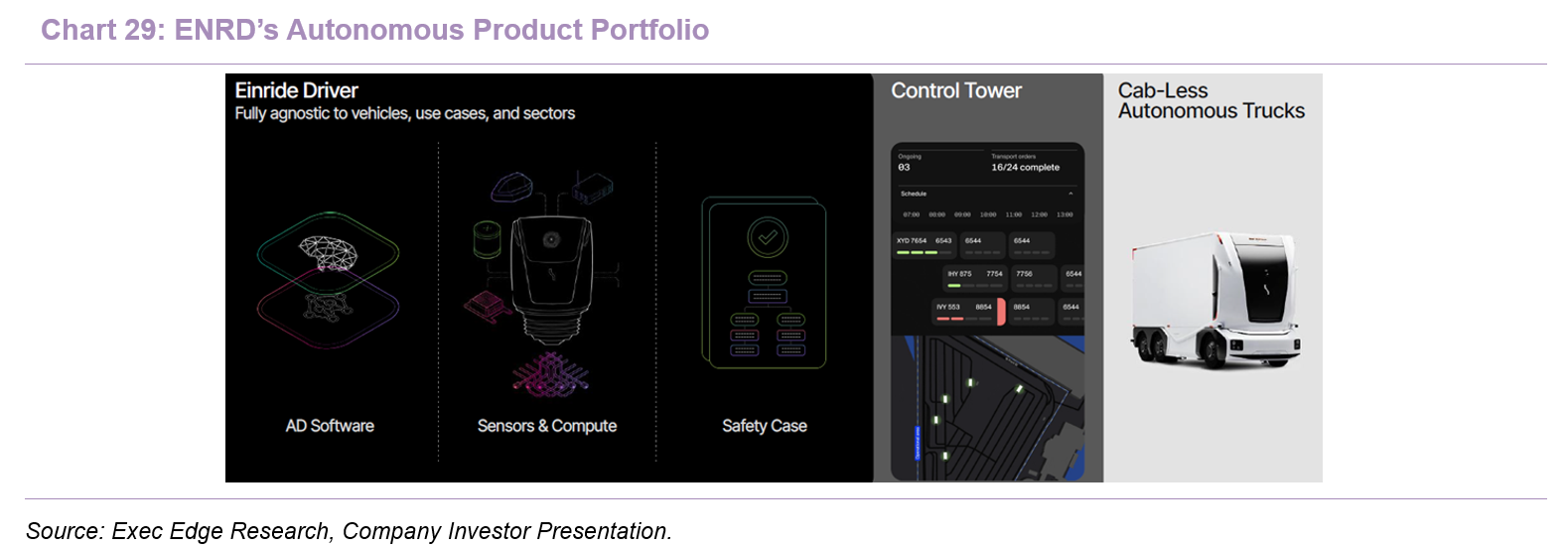

- ENRD’s solution is built around Saga, its AI-powered digital freight platform, which functions as the central operating layer for electric and autonomous freight deployments. Saga integrates with transportation management systems, vehicles, chargers, and external data sources such as route and weather inputs, allowing ENRD to design transport and charging plans for customers moving from diesel-based road freight to electric and autonomous capacity. The platform is organized across three layers: customer-facing digital products and services, AI models and proprietary algorithms, and underlying data sources gathered from real-world operations. For customers, the workflow begins with a data-led transformation program, where ENRD analyzes the customer’s transport network to identify routes that can be electrified immediately, routes that may be suitable for autonomous deployment, and areas where longer-term scale is possible. Saga then supports operational planning through Transport Suite, which helps planners, carriers, dispatchers, and drivers create and execute plans, manage vehicles, and track performance and emissions, and Charging Suite, which supports charger reservations, power prioritization, real-time charger status, energy use, and utilization visibility. The platform also incorporates models for electric vehicle route planning, predictive energy consumption, energy supply, and battery state-of-health, using transport order data, vehicle telematics, charging data, and driver app data.

- ENRD is also exploring quantum-enabled optimization with IonQ through a three-year partnership signed in May 2025, initially assessing 15 use cases across shipment scheduling, load building, energy trading, autonomous-truck safety, navigation, and quantum-key distribution. The work is focused on modularizing fleet-orchestration problems so quantum algorithms can target shipment allocation while accounting for real-world constraints across shipments, vehicles, drivers, and charging infrastructure. While still R&D-oriented rather than a near-term revenue driver, the partnership reinforces the strategic value of ENRD’s proprietary operating data and optimization layer.

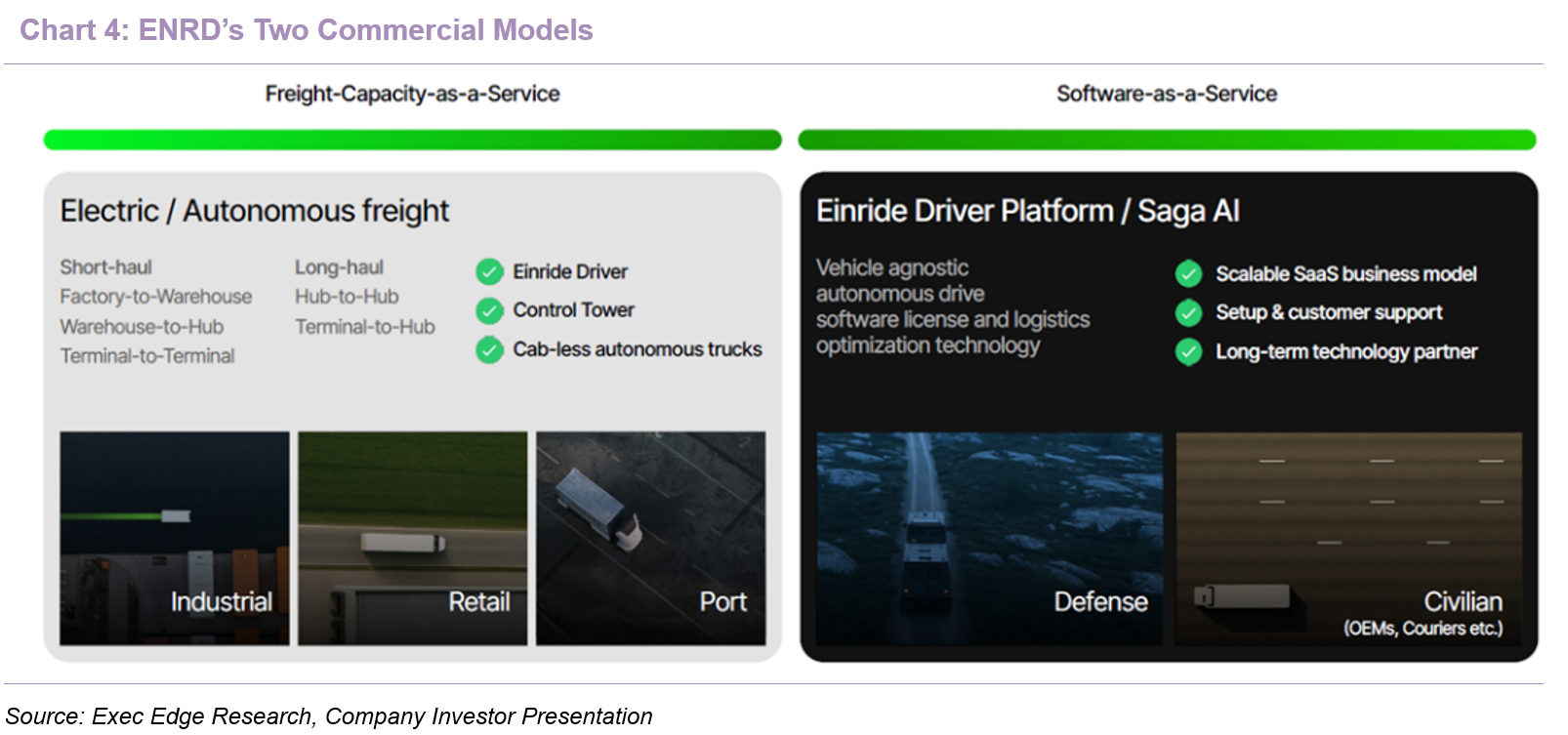

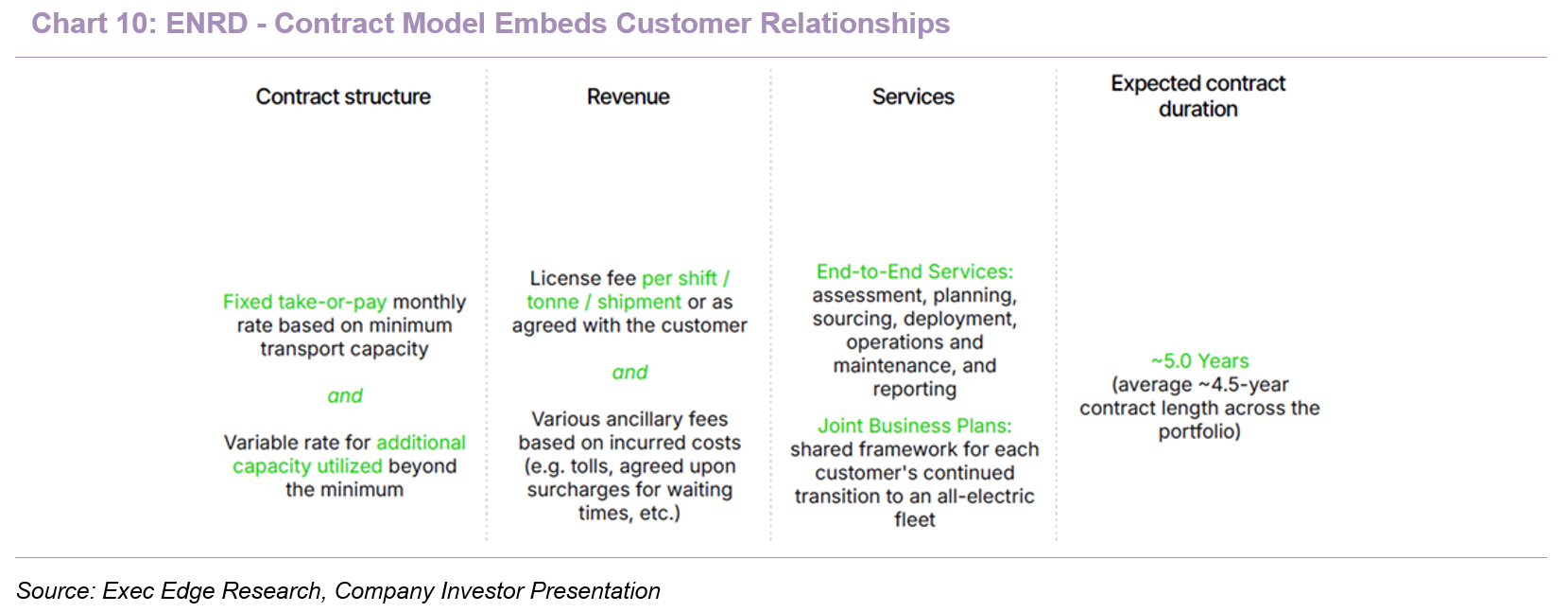

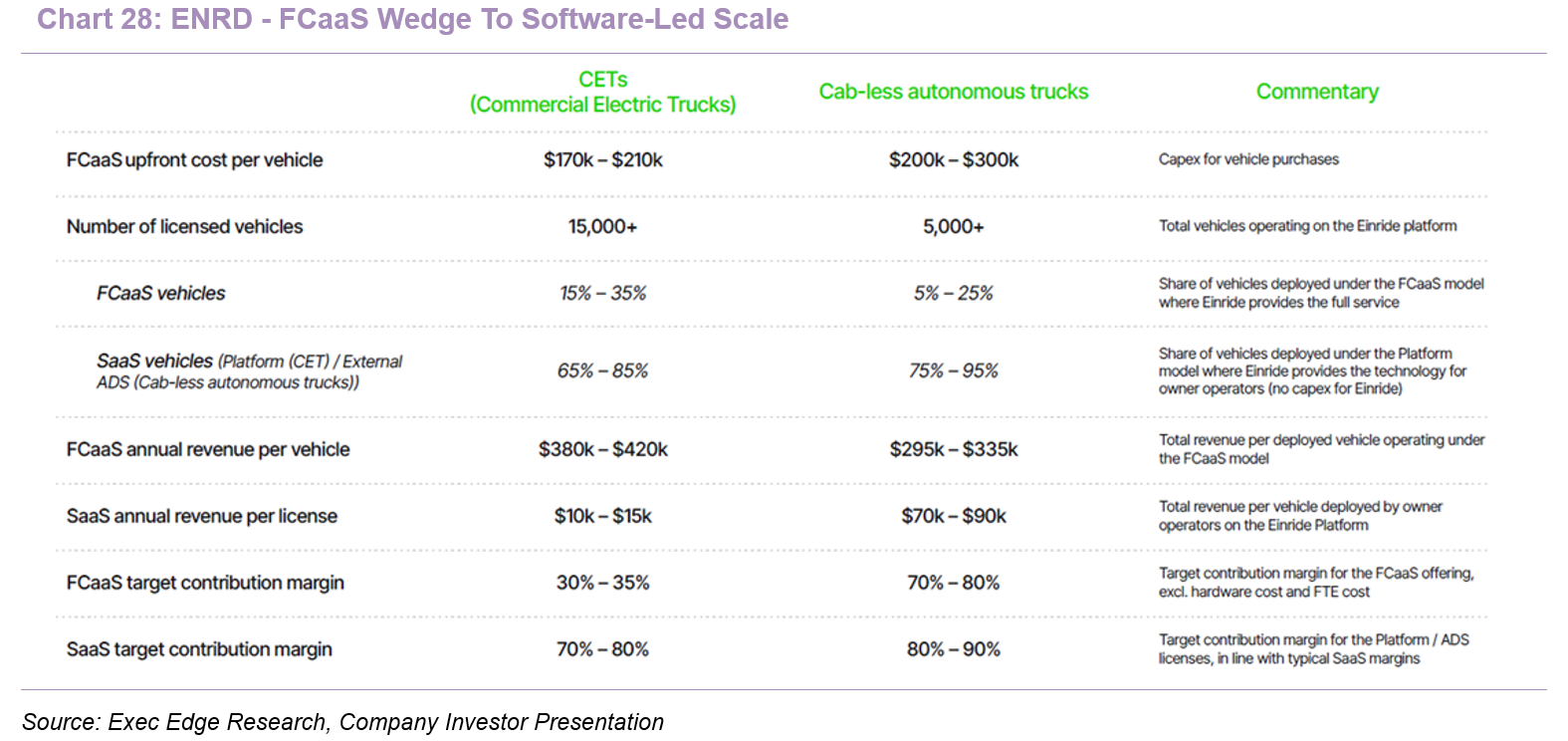

- The company offers its solution through two primary commercial models: Freight-Capacity-as-a-Service and Software-as-a-Service. FCaaS is the full-service model under which ENRD supports customers through the full road freight transition, including assessment, planning, sourcing, deployment, operations, maintenance, charging, driver services procured from carrier partners, technology, software, and reporting. Contracts are typically multi-year, generally three to five years, and structured on take-or-pay terms with fixed commitments from both parties. ENRD commits to deliver a specified amount of transport capacity, while the customer pays a fixed license fee per shift, tonne, shipment, or other agreed structure, with additional capacity available beyond minimum contracted volumes. FCaaS is currently deployed through commercial electric trucks and autonomous trucks, with electric vehicles sourced through a multi-OEM strategy that includes Daimler, Scania, and BYD. The SaaS offering, launched more recently, provides customers access to ENRD’s vehicle-agnostic technology, including Saga and the Einride Driver, while the customer and its carrier partners remain responsible for sourcing, deploying, and operating their own vehicles and charging infrastructure. Under the SaaS model, ENRD can provide the Einride Platform for digital freight planning and optimization, and the Einride Driver for autonomous operations across commercial transport, defense, and specialized civilian use cases. The SaaS structure is designed to let ENRD deploy its technology across a broader vehicle base while reducing the capital intensity associated with full FCaaS deployments.

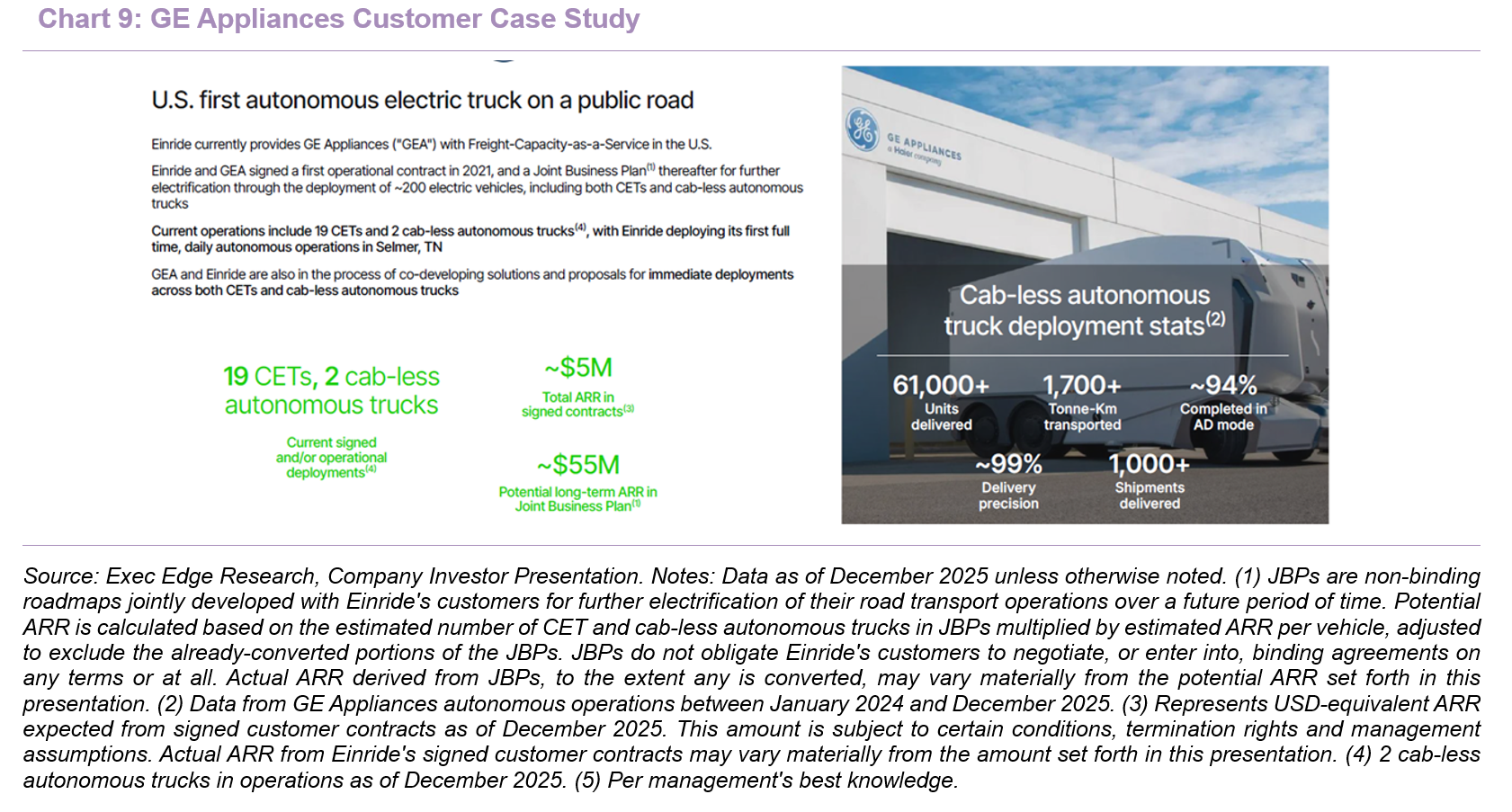

- ENRD serves leading enterprise customers across retail, consumer goods, logistics, and industrial verticals, with a commercial footprint spanning the U.S., EMEA, and the UAE. The company reports 30 signed or operational customers across seven countries, with customer examples including Carlsberg, DP World, GE Appliances, Heineken, Philips, Lidl, Mars, Oatly, Kaufland, PostNord, and REWE. ENRD also recently announced a U.S. partnership with Amazon to deploy 75 manually operated electric heavy-duty trucks and supporting charging infrastructure across five locations. The customer base is organized around both current deployments and longer-term transition roadmaps, with vertical-level exposure that includes $11 million of run-rate operational revenue in retail, $21 million in consumer goods, $10 million in logistics, and $7 million in industrials. The same customer verticals represent $92 million of ARR in signed customer contracts and $800 million+ of potential long-term ARR in Joint Business Plans. GE Appliances is a good example of the customer journey: ENRD currently provides FCaaS in the U.S., with 19 commercial electric trucks and two cab-less autonomous trucks in signed or operational deployments, while the relationship also includes a Joint Business Plan for further electrification through ~200 electric vehicles.

- The company’s safety and regulatory approach is centered on a documented safety case covering software, hardware, testing, assembly, operations, and organizational processes. ENRD positions safety as a system-level discipline, with the Einride Driver, Autonomous Truck, and Control Tower evaluated as an integrated operating environment rather than isolated technical components. Its safety case uses eight argumentation pillars, including safe automated driving system design, quality-controlled build processes, controlled release readiness, responsible deployment and operation, stakeholder safety, lifecycle safety, and delivery by a trustworthy organization. ENRD also references industry-standard frameworks, including ISO 26262, ISO/PAS 21448, ISO 21434, ISO 8800, and ISO 5083, for redundancy, cybersecurity, fail-safe, and fail-operational systems. Independent review is also part of the model, with Research Institutes of Sweden evaluating ENRD’s autonomous vehicle and software safety case. On the regulatory side, ENRD has built its deployment approach around early engagement with public-sector institutions and country-specific permitting regimes, with permits for autonomous heavy-duty vehicle operations across Sweden, Norway, Belgium, and the U.S., including engagement with NHTSA.

- Recent European milestones strengthen this regulatory-readiness narrative. ENRD operated a fully autonomous heavy-duty vehicle on a public road in Belgium at the Port of Antwerp-Bruges under the Belgian regulatory framework, and completed a cab-less electric autonomous border crossing at Ørje, Norway without a human driver onboard. The border-crossing demonstration is particularly relevant because ENRD integrated with Norway’s Digitoll digital customs solution through Q-Free, showing that autonomous freight execution requires driving autonomy, customs, infrastructure, and public-sector workflow integration. Taken together, ENRD’s safety-case-led and regulator-engaged approach helps bridge the gap between technical autonomy capability and permitted, customer-facing commercial freight operations.

- ENRD’s IP base spans patents, trademarks, registered designs, trade secrets, datasets, and technical know-how across autonomous vehicles, electric mobility, charging, software, and hardware. As of February 2026, ENRD and its subsidiary Einride Autonomous Technologies owned 15 granted patents and 19 patent applications, with portfolios covering fleet operations, the digital freight platform, cab-less autonomous heavy-duty vehicles, remote operations, energy management, battery utilization, and data management. The company also reported 62 active registered trademarks, six pending trademark applications, and 42 registered designs and applications. ENRD had approximately 300 full-time employees as of December 2025, mainly based in EMEA and the U.S., including ~100 employees dedicated to autonomous transport development. Its headquarters are in Stockholm, where it leases ~8,000 square feet of office space, with additional offices and industrial spaces in Gothenburg, Austin, Texas, and the UAE. ENRD’s supply chain strategy relies on partnerships with global OEMs and specialized suppliers, including vehicle OEMs, charging infrastructure partners, contract manufacturers, component suppliers, and providers of sensors and compute systems.

Right-to-Win

Data, Deployment, and Customer Embeddedness Create ENRD’s Freight Autonomy Moat

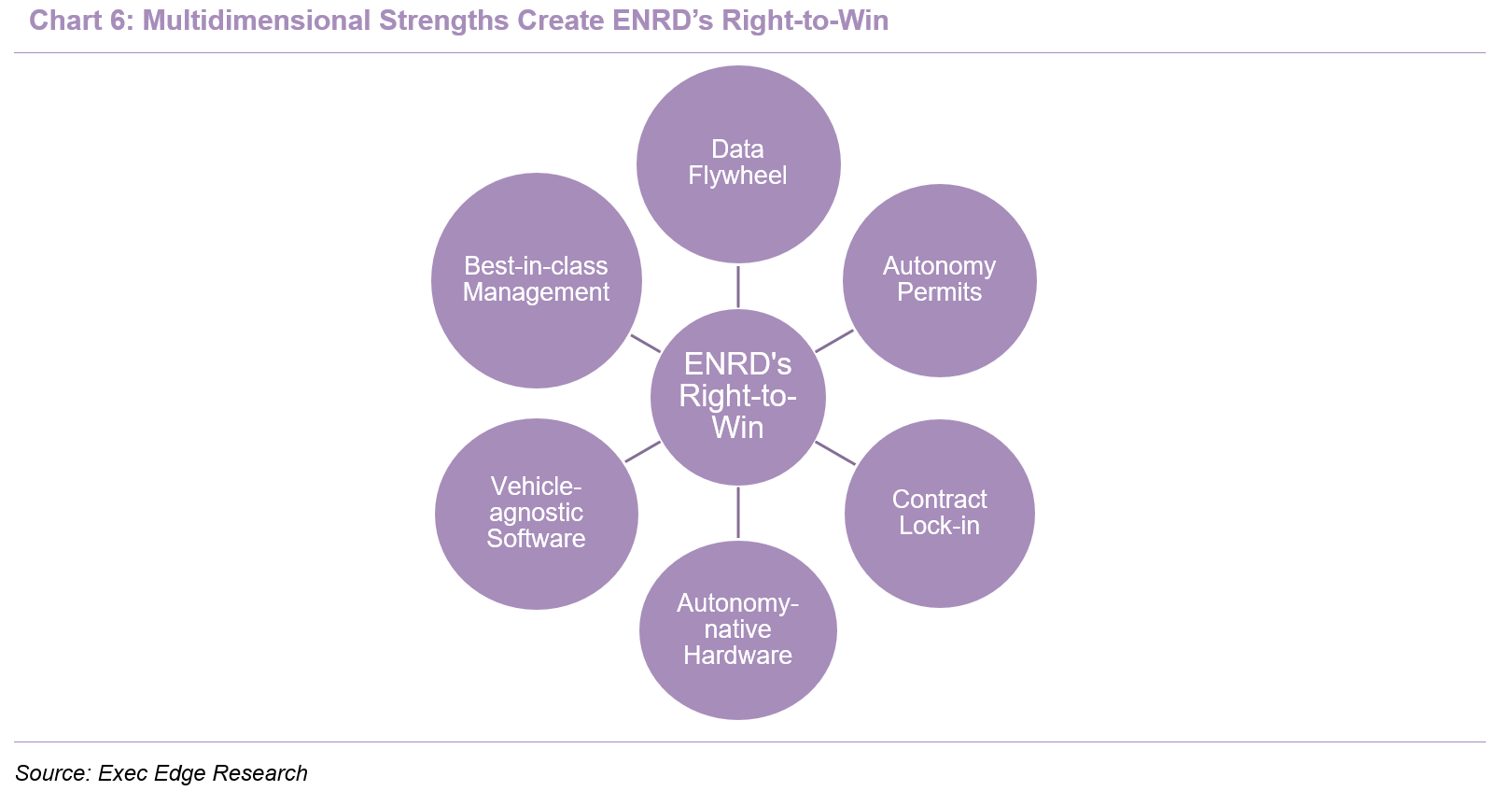

- We believe ENRD’s right-to-win is anchored in a set of moat elements required to scale electric and autonomous freight in real customer networks. The company combines a data-rich planning platform, commercial autonomous deployments, shipper-centric contracts, purpose-built cab-less hardware, vehicle-agnostic software, and an experienced leadership team with public-market and deep-tech execution depth. Together, these advantages create a business differentiated not only by technology, but by deployment capability, regulatory learning, customer embeddedness, and operating know-how. This combination should help ENRD defend its position as it converts early commercial traction into broader platform scale. We discuss each of these elements below.

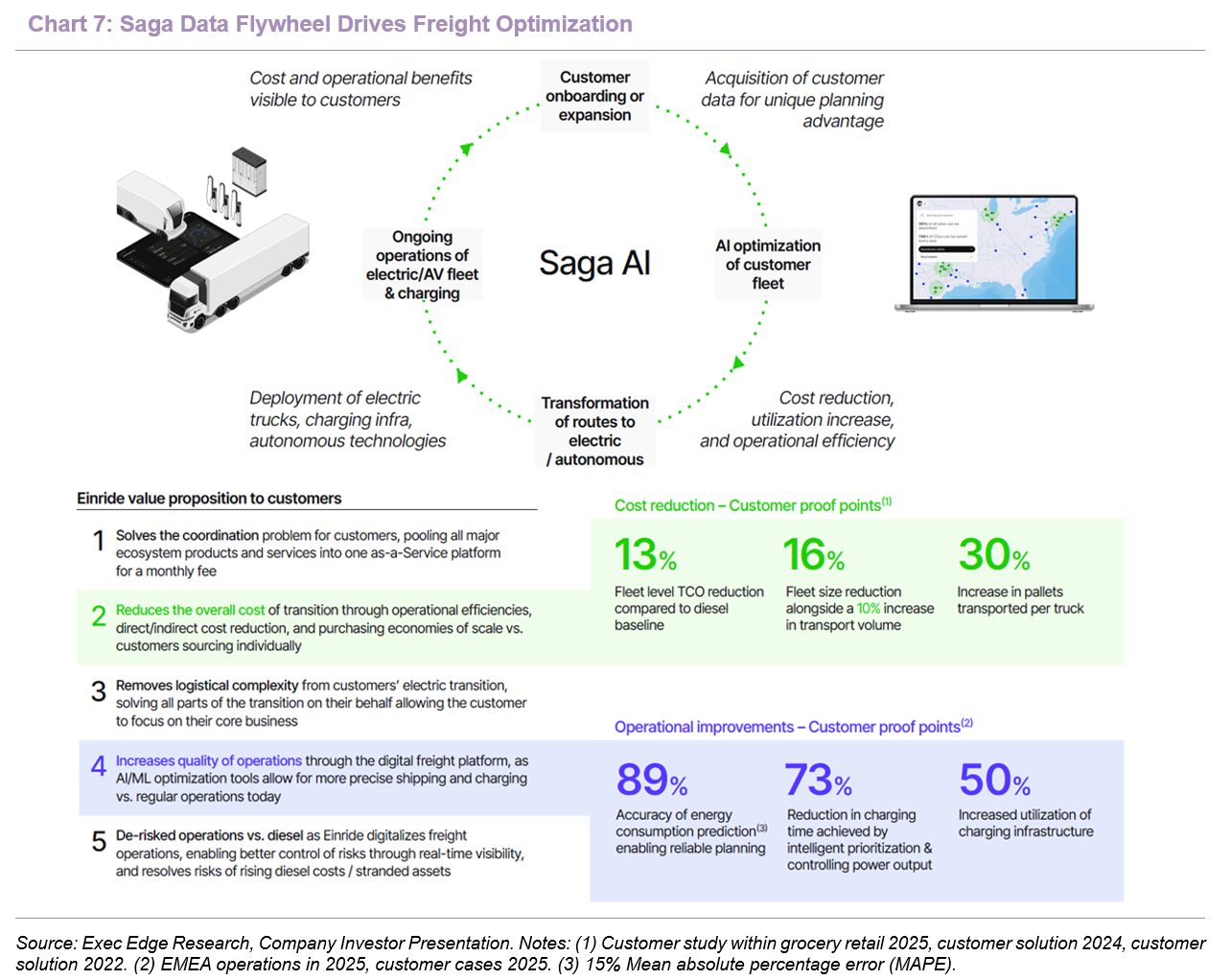

- ENRD’s data-rich platform turns freight electrification and autonomy from a hardware deployment challenge into a continuously improving optimization problem. Saga sits at the center of ENRD’s operating model, integrating transport-management data, vehicle telemetry, charging data, driver inputs, route and weather information, and autonomous sensor data into a single planning and execution layer. This combined data set is unusual because OEMs typically see vehicle data, transport companies see shipment and driver data, charging operators see charging data, and autonomous developers see sensor data, while ENRD brings these inputs together inside one platform. Saga then applies AI models and proprietary planning algorithms across route planning, energy consumption, energy supply, shipment selection, battery state of health, driver performance, emissions, cost, and pricing. ENRD’s reported operating metrics point to tangible optimization benefits, including a 13% fleet-level TCO reduction versus a diesel baseline in certain cases, a 16% reduction in fleet size alongside a 10% increase in transport volume, 30% more pallets transported per truck, 89% energy-consumption prediction accuracy, 73% reduction in charging time, and 50% higher charging-infrastructure utilization. These outcomes highlight why electric freight economics depend on coordinated decisions across routes, payloads, charging windows, vehicle availability, and energy cost, rather than simply procuring electric trucks. ENRD’s advantage is reinforced by a data flywheel: more contracted operations generate more proprietary operating data, richer data improves planning quality, better planning strengthens customer economics, and stronger customer economics can support deeper customer deployments. Over time, this positions Saga as the operating memory of ENRD’s freight network and a potential barrier for competitors without comparable access to multi-source freight, energy, vehicle, and autonomy data.

- The company’s autonomous freight track record combines customer deployments, regulatory engagement, and real-world operating data, creating an early operational advantage in a market where permission to operate is a strategic asset. ENRD reports 3,300+ driverless hours in contracted customer operations, 3,300+ autonomous tonne-km transported, and zero traffic incidents across autonomous operations. It also states that it was the first company to place a fully autonomous cab-less heavy-duty vehicle on public roads in Europe in 2019 and the U.S. in 2022, with permits in place to support further scaling. The GE Appliances deployment provides the clearest customer-level proof point: between January 2024 and December 2025, ENRD’s cab-less autonomous trucks delivered 61,000+ units, completed 1,000+ shipments, transported 1,700+ tonne-km, operated at ~94% autonomous drive mode, and achieved ~99% delivery precision. Autonomous freight does not scale through software performance alone; it also requires audited safety cases, regulator confidence, customer operating domains, trained operations teams, and repeatable field performance. ENRD’s safety case is built around ISO standards, has been verified through two independent audits by Sweden’s Research Institutes, and spans software, hardware, testing, assembly, operations, and safety culture. The regulatory backdrop remains fragmented, with no unified global framework for autonomous and electric transport, increasing the value of accumulated market-by-market deployment experience. In our view, ENRD’s moat is operational as much as technological: each permitted deployment can compound safety evidence, customer confidence, and domain-specific learnings that are difficult for lab-stage autonomy developers to replicate. As ENRD expands across routes, speeds, operating domains, and customer use cases, it is doing so from a foundation of live commercial operations rather than theoretical readiness.

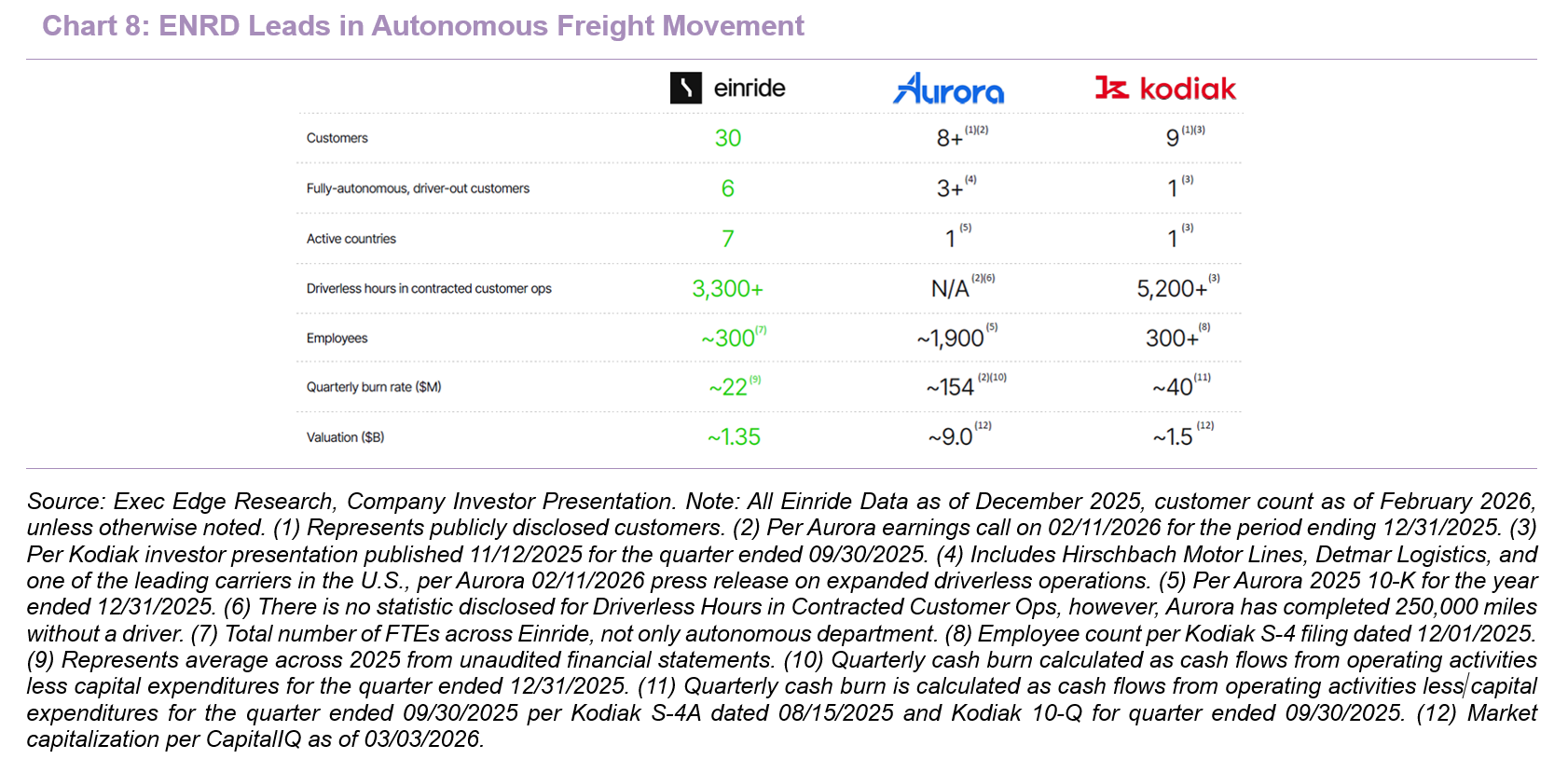

- Peer benchmarking highlights ENRD’s differentiated combination of commercial autonomy traction, customer breadth, and capital-efficient execution. The company’s investor presentation shows ENRD with 30 customers, six fully autonomous driver-out customers, seven active countries, and 3,300+ driverless hours in contracted customer operations, compared with Aurora at eight customers, three driver-out customers, one active country, and Kodiak at nine customers, one driver-out customer, one active country, and 5,200+ driverless hours. ENRD also appears meaningfully leaner, with ~300 employees and ~$22 million quarterly burn, versus Aurora’s ~1,900 employees and ~$154 million quarterly burn. The comparison suggests ENRD has achieved broader customer and geographic reach with materially lower organizational complexity and cash intensity than larger autonomy peers.

- Its shipper-centric contract model embeds ENRD directly into the freight networks of large blue-chip transport buyers, positioning it as an operating partner rather than a vendor of trucks, chargers, or software. The company serves 30 signed or operational customers across seven countries, with customer exposure across retail, consumer goods, logistics, and industrials, including leading names such as Carlsberg, GEA, PepsiCo, Mars, and DP World. The recently announced Amazon deployment adds another blue-chip validation point, with ENRD expected to deploy 75 manually operated electric heavy-duty trucks into Amazon’s U.S. freight network, supported by charging infrastructure and Saga AI-enabled execution for select loads. This customer network is strategically important because large shippers tend to operate complex, multi-site freight flows where electrification requires planning, charging access, operational discipline, and performance visibility. ENRD’s FCaaS model packages these requirements into an end-to-end service, covering assessment, planning, sourcing, deployment, operations, maintenance, charging, software, and reporting. Contracts are structured with fixed take-or-pay monthly capacity commitments, variable rates for additional utilization, and ancillary fees, with typical contract duration of 3-5 years and an average portfolio contract length of ~4.5 years. This creates revenue visibility for ENRD while giving customers a defined commercial framework for transitioning freight capacity over time. The model also supports customer lock-in because ENRD’s engagement begins with transportation data ingestion and a Transformation Program, then moves into JBPs, operational contracts, charging deployment, vehicle assignment, route planning, and performance reporting. Once ENRD has designed a customer’s freight roadmap and embedded its software, vehicles, charging processes, and operating routines into specific lanes, switching costs can rise beyond the contractual term alone. The resulting moat is both commercial and operational: ENRD’s blue-chip customer base supports credibility, its contract structure provides visibility, and its role as the operating interface can make the relationship increasingly difficult to displace as deployments scale from initial lanes into broader network transformation.

- ENRD’s autonomy-native hardware strengthens its right-to-win by designing for the driverless end state from inception, rather than retrofitting autonomy onto a conventional in-cab truck platform. ENRD’s cab-less autonomous trucks are built to operate without a driver from day one, supported by remote oversight through the Control Tower and redundancy across steering, braking, and power supply. According to the company, removing the cab eliminates unnecessary cost and space in a vehicle designed to operate without an onboard driver, while potentially creating additional room for battery capacity or storage. This is important because autonomous freight economics depend not only on software readiness, but on whether the vehicle architecture itself is optimized for the use case. ENRD’s purpose-built approach also supports its regulatory narrative, with redundancy, safety architecture, and remote oversight central to public-road permitting. The company has already placed fully autonomous cab-less heavy-duty vehicles on public roads in Europe and the U.S. and reports 3,300+ driverless hours in contracted customer operations. A further product milestone is the Gen 3 autonomous truck platform, which management expects to be production-ready by year-end, with container-transport capability, longer-range sensors, and expanded compute capacity designed to broaden future use cases. The resulting advantage is architectural and operational: ENRD is not simply automating a legacy truck platform, but building the vehicle, oversight system, and operating model around driverless freight from the ground up.

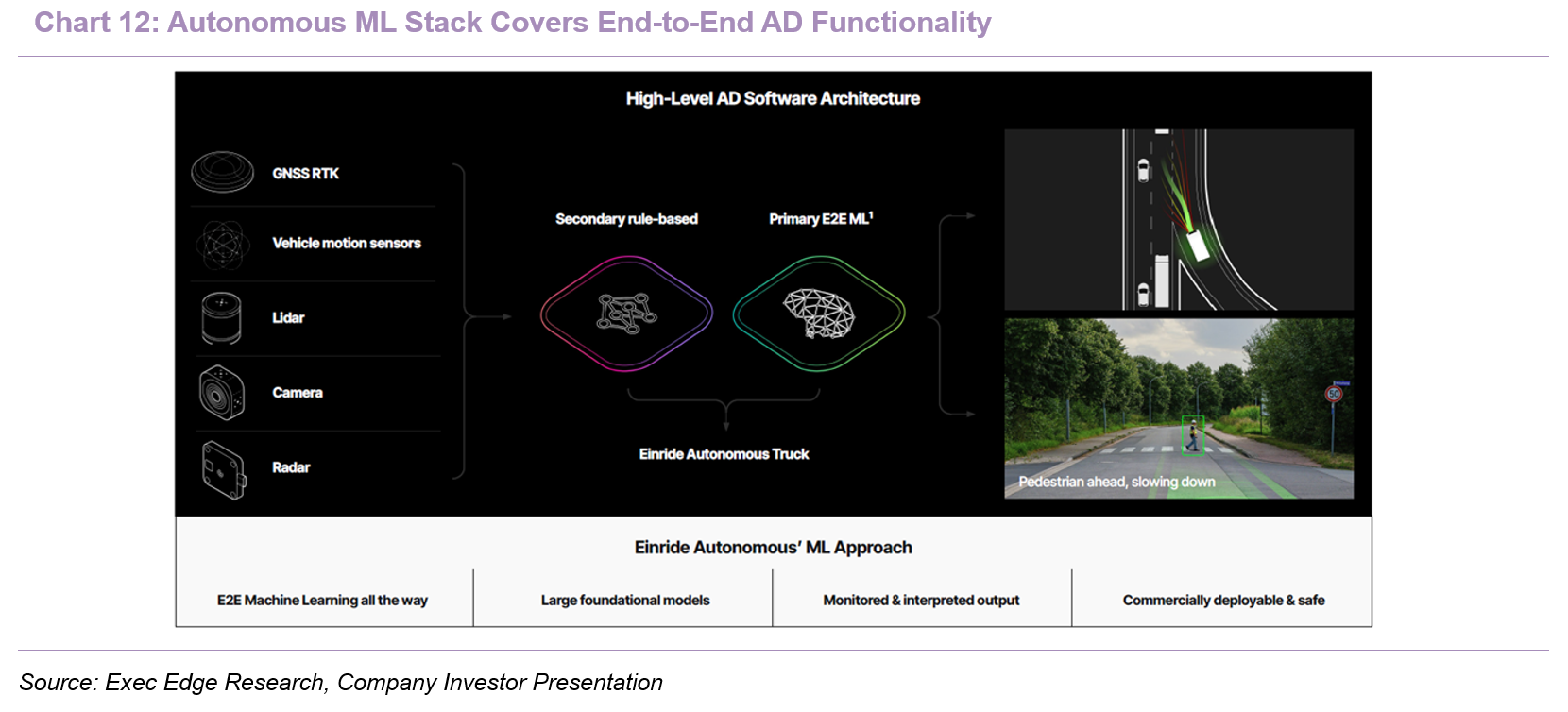

- A vehicle-agnostic software gives the Einride Driver a path to scale beyond the company’s own cab-less trucks. The autonomous driving stack is developed in-house and designed to operate across multiple vehicle platforms, with the F-4 filing describing it as vehicle-agnostic and one of ENRD’s most valuable intellectual property assets. The architecture combines LiDAR, cameras, radar, GNSS, vehicle motion sensors, a primary end-to-end machine-learning path, and a secondary deterministic rule-based layer that provides safety guardrails. ENRD also states that the stack is containerized, can run across different compute architectures, and can be deployed through over-the-air updates. That portability matters because autonomous freight adoption is unlikely to be confined to a single vehicle format or ownership model. Customers may want autonomous capability on their own assets or across commercial transport, defense, and specialized civilian applications without adopting ENRD’s full FCaaS model. Management is initially targeting fleet owners in specialized civilian and defense applications, with potential OEM-level opportunities over time as the autonomous stack proves portability across vehicle types. Vehicle-agnostic software gives ENRD a capital-lighter path to monetize autonomy through licensing, service fees, and customer-specific ODD development. The resulting advantage is deployment flexibility: ENRD can participate across more autonomy use cases than a hardware-tied provider while continuing to leverage the same operating data, safety-case discipline, and autonomous technology base.

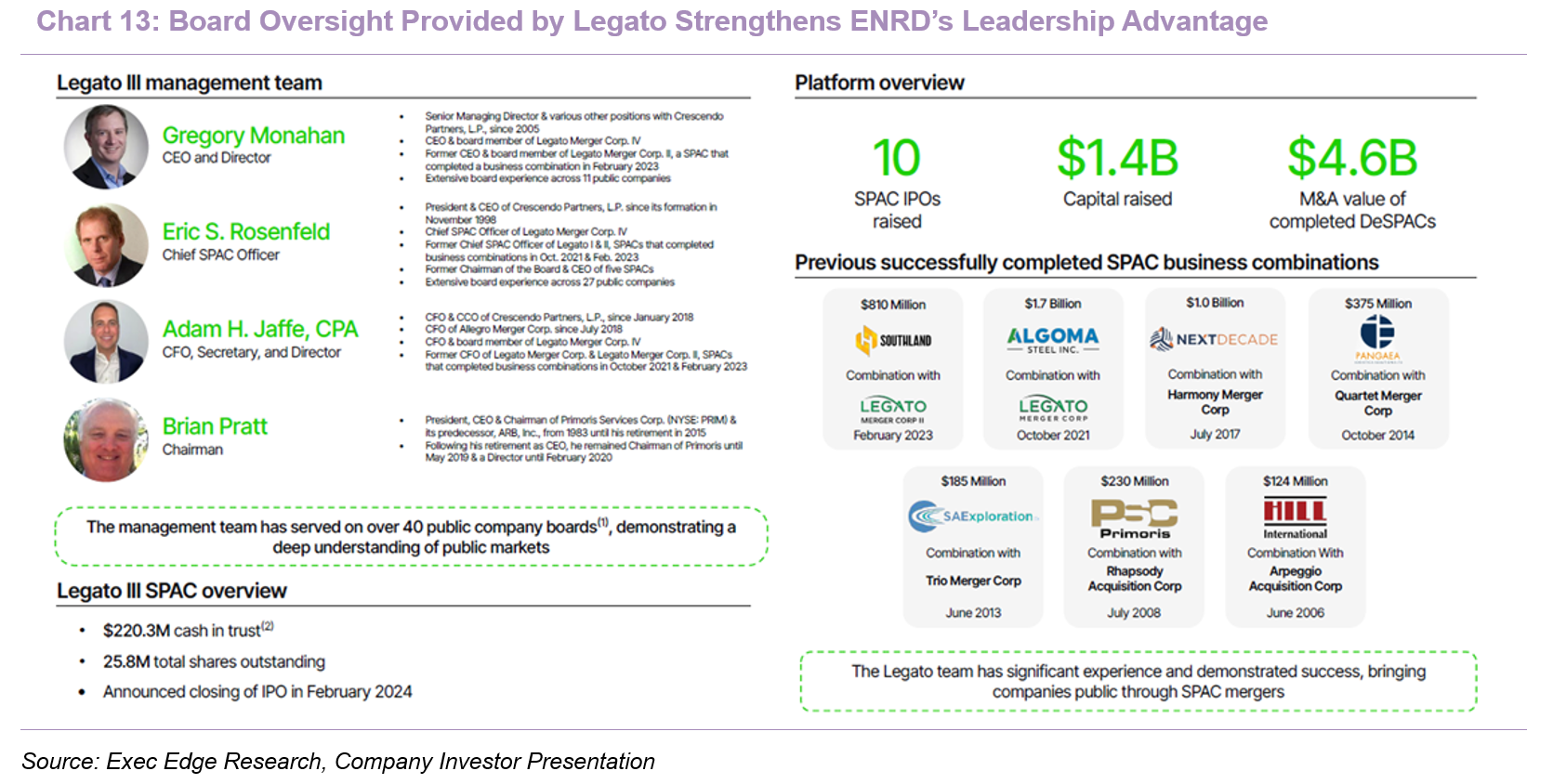

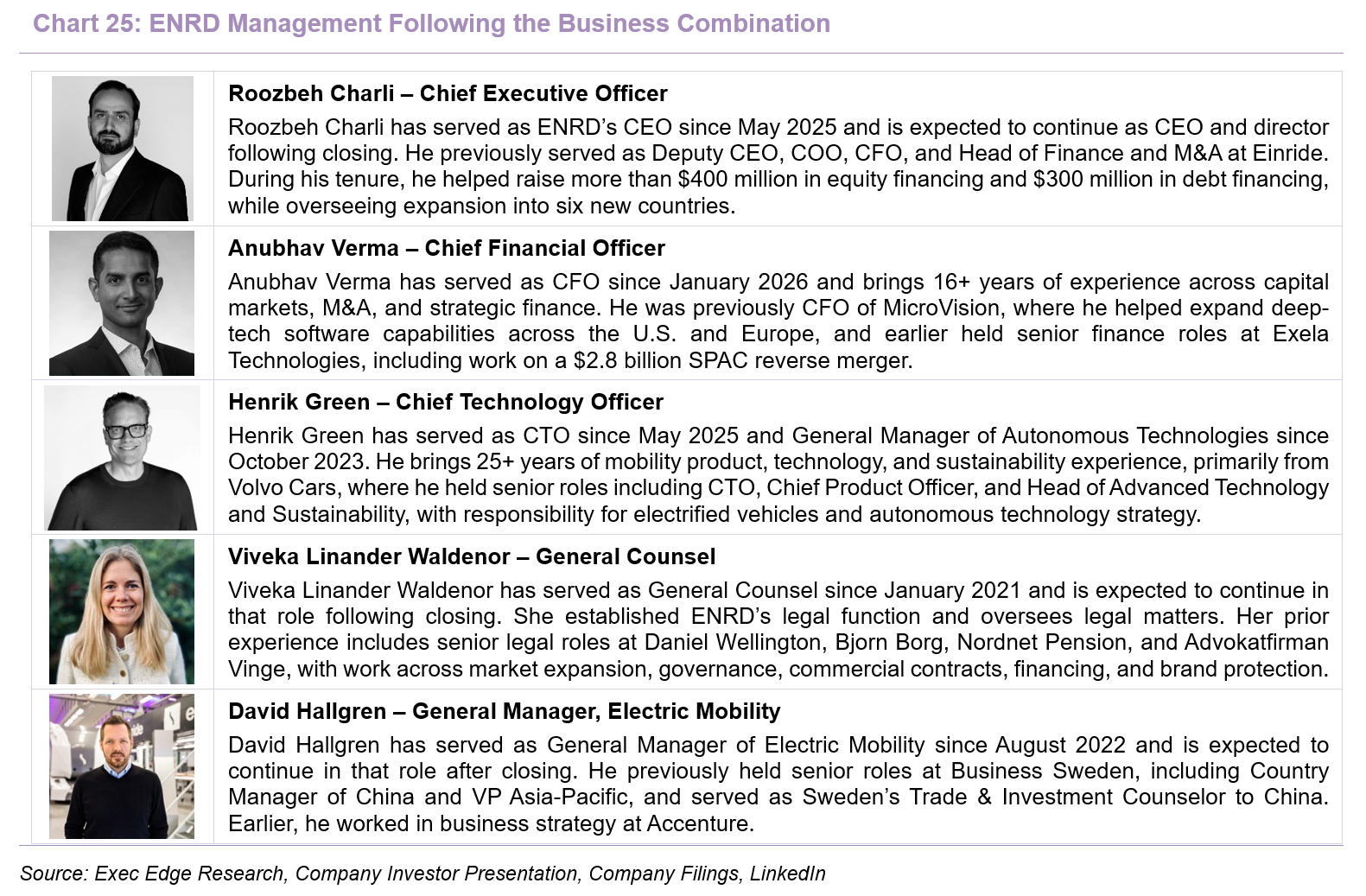

- ENRD’s management and board depth pairs company-specific operating experience with public-market, deep-tech, and governance expertise. CEO Roozbeh Charli brings continuity across ENRD’s scale-up, having served as Deputy CEO, COO, CFO, and Head of Finance and M&A before becoming CEO in May 2025; during his tenure, he helped raise more than $400 million in equity financing and $300 million in debt financing, while overseeing expansion into six new countries. CTO Henrik Green adds heavyweight automotive and autonomous systems leadership, including responsibility for ENRD’s autonomous technologies, a critical competency as the company moves from electric freight deployment toward broader autonomous commercialization. CFO Anubhav Verma strengthens the public-company readiness angle, with more than 16 years across capital markets, M&A, strategic finance, deep-tech software, LiDAR, automotive, industrial, and defense technology, including prior SPAC reverse-merger experience at Exela Technologies. Post-close, Legato III’s Eric Rosenfeld and Gregory Monahan are expected to join ENRD’s board, with Monahan expected to chair the audit committee and Rosenfeld identified as an audit committee financial expert. Recent board additions further strengthen the technology and dual-use governance profile, with former NVIDIA senior executive Gary Hicok expected to join the board, bringing more than 25 years of autonomous technology and platform-scaling experience, and General Keith B. Alexander appointed to the board, adding cybersecurity, military intelligence, public-company board, and defense-domain expertise as ENRD establishes a dedicated defense business. Legato’s transaction experience is also relevant, with the team credited with 10 SPAC IPOs, $1.4 billion of capital raised, and $4.6 billion of M&A value across completed de-SPAC transactions. Prior combinations across energy transition, infrastructure, automotive technology, and industrial platforms should add relevant public-market transaction experience as ENRD transitions from a private growth company to a Nasdaq-listed issuer. Overall, ENRD’s leadership bench appears well aligned with the company’s next phase: scaling customer deployments, commercializing autonomy, and operating as a listed deep-tech freight platform.

Industry Trends and Company Positioning

Fragmented Freight Market Strengthens ENRD’s Integrated Platform Opportunity

- Large, fragmented, and inefficient road freight market creates room for technology-led disruption. The road freight market is one of the largest segments of global logistics and remains structurally critical, with trucks providing flexible, point-to-point capacity across short-haul, regional, and long-haul routes. A recent market study by The Insight Partners shows that the global road freight transportation market is roughly $4.75 trillion in 2025 and is expected to grow at a CAGR of 4.8% to reach $7.27 trillion in 2034. The U.S. and Europe are large developed-market anchors within this opportunity. In the U.S., the American Trucking Associations reported that trucks moved 11.27 billion tons of freight in 2024 and generated $906 billion of gross freight revenue, representing 76.9% of total transportation-sector freight revenue. In the EU, Eurostat reported that road freight transport amounted to more than 13.1 billion tonnes and 1,867 billion tonne-kilometres in 2024. Taken together, these data points establish road freight as one of the largest pools of transportation spend globally, with high-volume corridors creating meaningful opportunities for improved asset productivity, network density, and technology-enabled coordination.

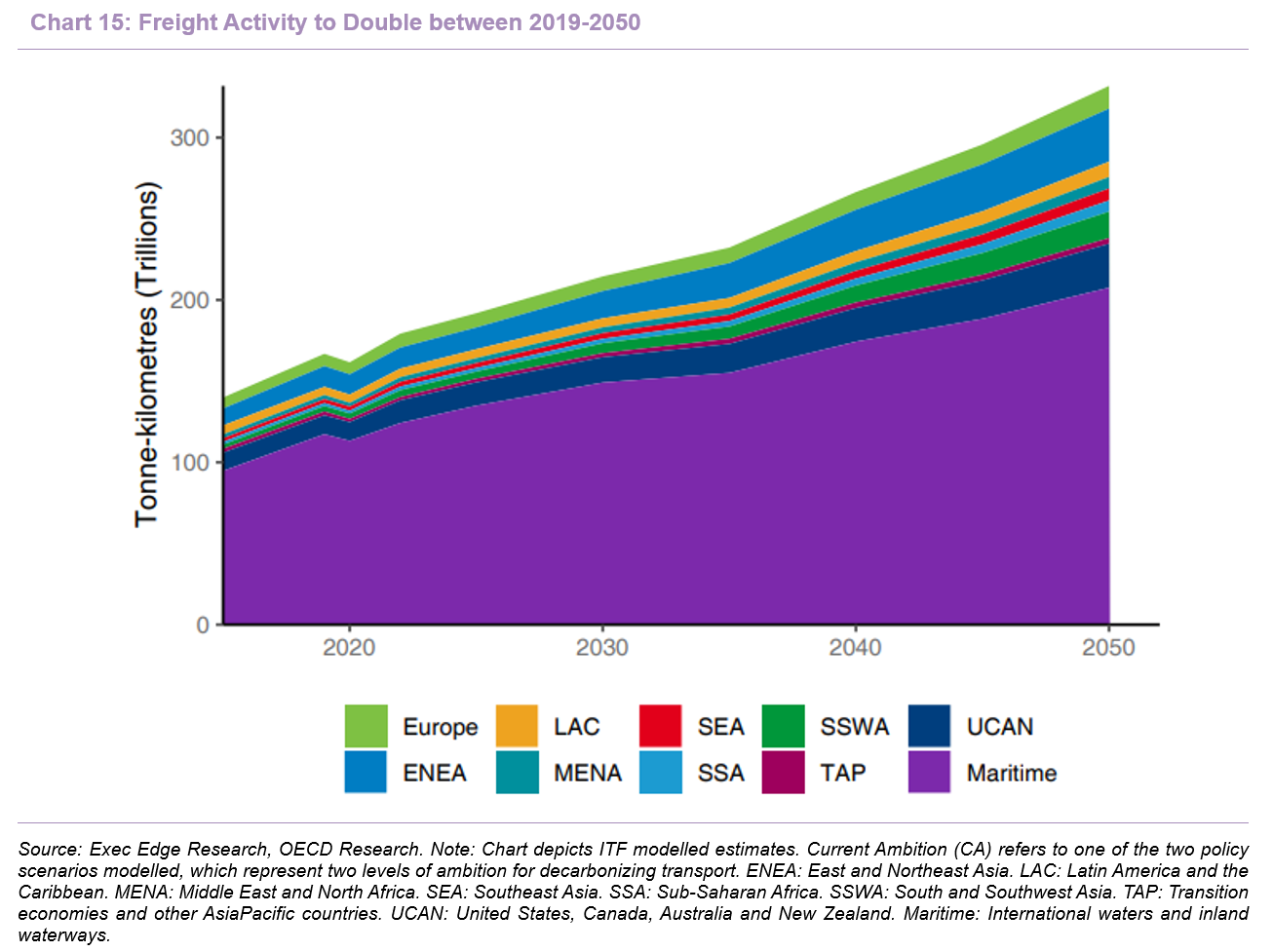

- Growth in road freight demand is being supported by structural freight intensity, higher-value supply chains, e-commerce, and the continued need for flexible point-to-point transport. The International Transport Forum expects global freight demand to roughly double by 2050 under its Current Ambition scenario, which is the scenario that assumes existing decarbonization policies continue along their current pathway rather than accelerating materially. In the U.S., the Bureau of Transportation Statistics’ Freight Analysis Framework forecasts that the real value of freight per ton will rise from $949 in 2024 to $1,256 in 2050, suggesting freight is expected to become more valuable on a per-ton basis even after adjusting for inflation. As freight becomes more valuable and time-sensitive, reliability, delivery precision, real-time visibility, and network resilience become more important. E-commerce and retail demand are also reshaping trucking requirements, increasing the need for more flexible and data-driven freight networks. According to Technavio Research, rising demand from e-commerce and retail, along with deeper penetration of last-mile logistics solutions, are key growth drivers for road freight transport in developed markets such as the U.S. and Europe. Trucking networks are therefore being asked to do more than move incremental freight; they must manage tighter delivery windows, more fragmented delivery points, and greater demand for real-time transparency. This increases the value of digital dispatch, route optimization, capacity matching, and integrated fleet management.

- Despite its scale, trucking remains structurally fragmented and inefficient, creating a large gap between gross market size and actual network productivity. In the U.S., ATA’s 2024 industry data showed that 95.5% of carriers operated 10 or fewer trucks and 99.6% operated fewer than 100 power units, indicating that capacity is spread across a long tail of small operators rather than concentrated in large, technology-enabled fleets. A power unit generally refers to the tractor or truck used to pull freight, distinct from the trailer. Fragmentation limits purchasing leverage, data scale, capital access, and the ability to coordinate capacity across regions. The cost structure is also under pressure. The American Transportation Research Institute reported that the average marginal cost of operating a truck was $2.260 per mile in 2024. Marginal cost per mile captures variable operating costs such as fuel, driver wages and benefits, maintenance, insurance, permits, tolls, tires, and equipment financing costs, making it a useful measure of fleet-level operating economics. ATRI also reported that non-fuel marginal costs rose 3.6% y/y to $1.779 per mile, the highest level in its dataset, even though lower fuel costs helped total operating cost decline modestly. The high fragmentation also means that the vast majority of capacity is managed by small and mid-sized fleets that lack the capital to invest in advanced optimization software or zero-emission assets.

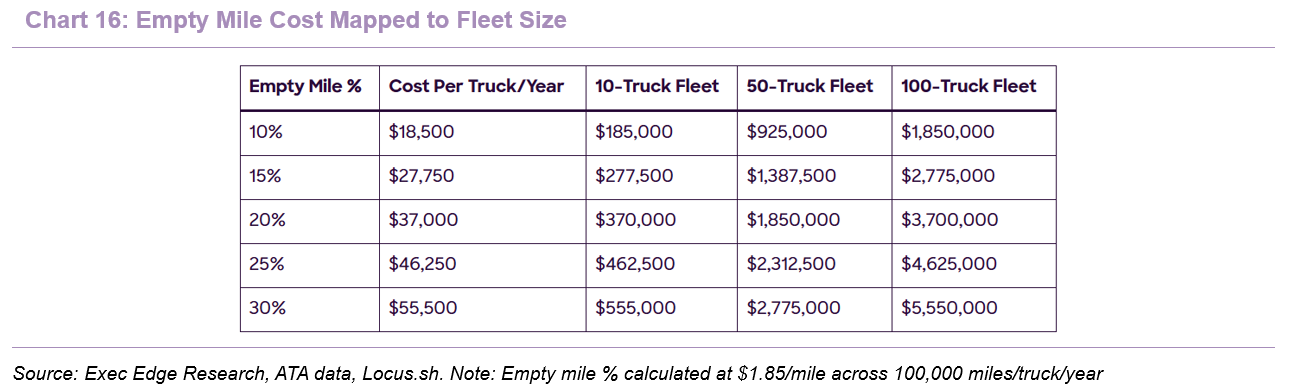

- The most visible symptom of this inefficiency is the empty miles phenomenon; industry estimates cited by Locus.sh suggest nearly one in three U.S. truck miles is driven without cargo. This translates to an estimated $30 billion in annual industry waste, with high-volume replenishment lanes in sectors such as FMCG particularly exposed to margin pressure from imbalanced outbound and inbound flows. These inefficiencies help explain why software, data, routing intelligence, and utilization tools are becoming more strategic in freight.

- ENRD is positioned to benefit from this backdrop because its model targets the coordination and productivity layer of road freight, rather than only selling vehicles into a fragmented carrier base. The company combines electric freight capacity, autonomous technology, charging infrastructure, and Saga, its AI-enabled operating system, into an integrated model designed to help enterprise shippers plan, deploy, and scale lower-emission freight networks. That matters in a market where the underlying pain points are not limited to truck availability; they include route design, energy planning, charging utilization, asset productivity, driver scheduling, regulatory compliance, and customer reporting. ENRD’s disclosed commercial traction suggests enterprise demand for this integrated approach, including more than 30 enterprise customers across seven countries, approximately $92 million of expected annual recurring revenue from signed customer contracts, and more than $800 million of potential long-term ARR through joint business plans with customers. The model is built for a freight market where vehicles, energy, autonomy, and execution increasingly need to be coordinated through one software-led system.

Energy Volatility Reinforces Demand for Smart Freight Infrastructure

- Fuel-price volatility remains a strategic risk for transportation buyers, with the current Iran / Hormuz disruption providing a live example of how geopolitical shocks can quickly flow into freight costs. The latest EIA Short-Term Energy Outlook, released May 12, 2026, assumes the Strait of Hormuz remains effectively closed until late May, with shipping traffic beginning to recover in June but not returning to pre-conflict levels until later in the year. EIA estimates that Iraq, Saudi Arabia, Kuwait, the UAE, Qatar, and Bahrain collectively shut in 10.5 million barrels per day of crude production in April, driving large inventory draws and limiting near-term price relief. Brent crude reached $138 per barrel on April 7, averaged $117 per barrel in April, and is forecast by EIA to remain around $106 per barrel in May and June. The volatility has already reached diesel markets, with U.S. No. 2 diesel averaging $5.501 per gallon in April 2026, up from $3.523 in January 2026.

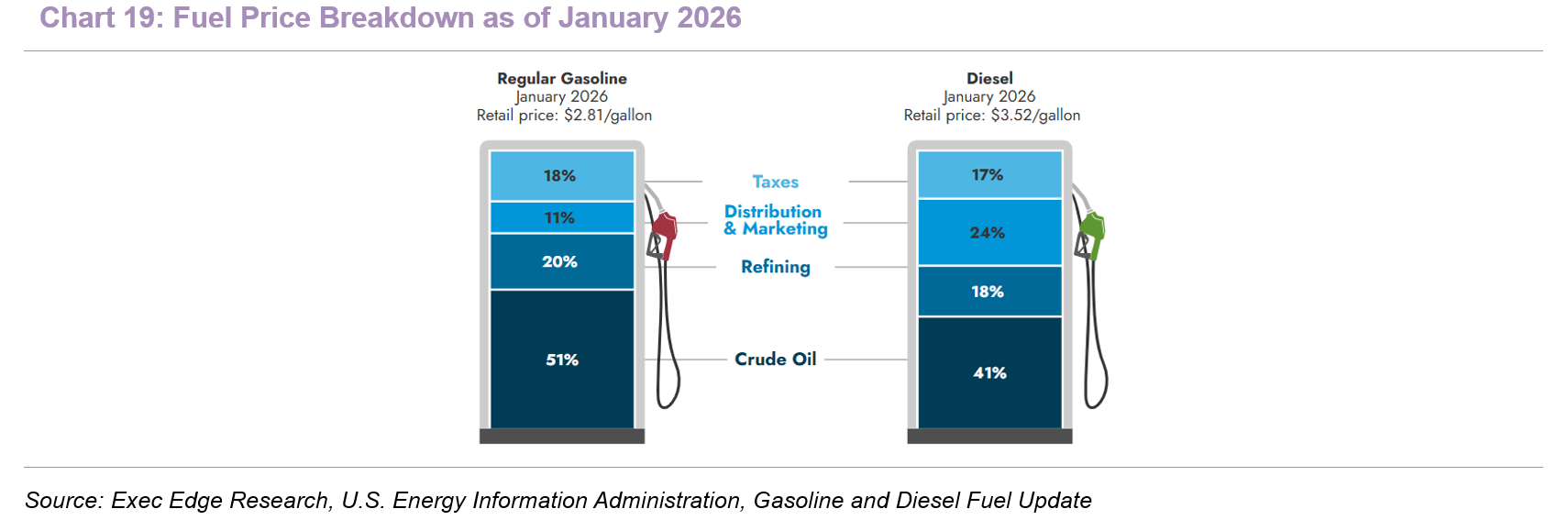

- For shippers, fuel volatility shows up quickly in freight budgets, carrier negotiations, and delivered product cost. Diesel remains a major trucking input, and EIA’s diesel price breakdown shows crude oil accounted for 41% of the January 2026 U.S. retail diesel price, with refining, distribution, marketing, and taxes making up the balance. That linkage helps explain why crude-market shocks can move quickly into trucking economics. Fuel surcharges are one of the main pass-through mechanisms: FedEx, for example, states that fuel surcharge percentages and trigger points can change without notice and ties diesel-based surcharge movement to the national U.S. on-highway diesel price. Recent logistics commentary points in the same direction. InTek Logistics noted that rising diesel prices can lift fuel surcharges and may also affect baseline freight rates, particularly in truckload markets, while Breakthrough warned that Middle East escalation had sharply increased crude, gasoline, and diesel prices, raising near-term fuel-price risk for transportation budgets. The result is a less predictable cost environment for shippers, with greater difficulty locking in freight economics across multi-quarter supply-chain plans.

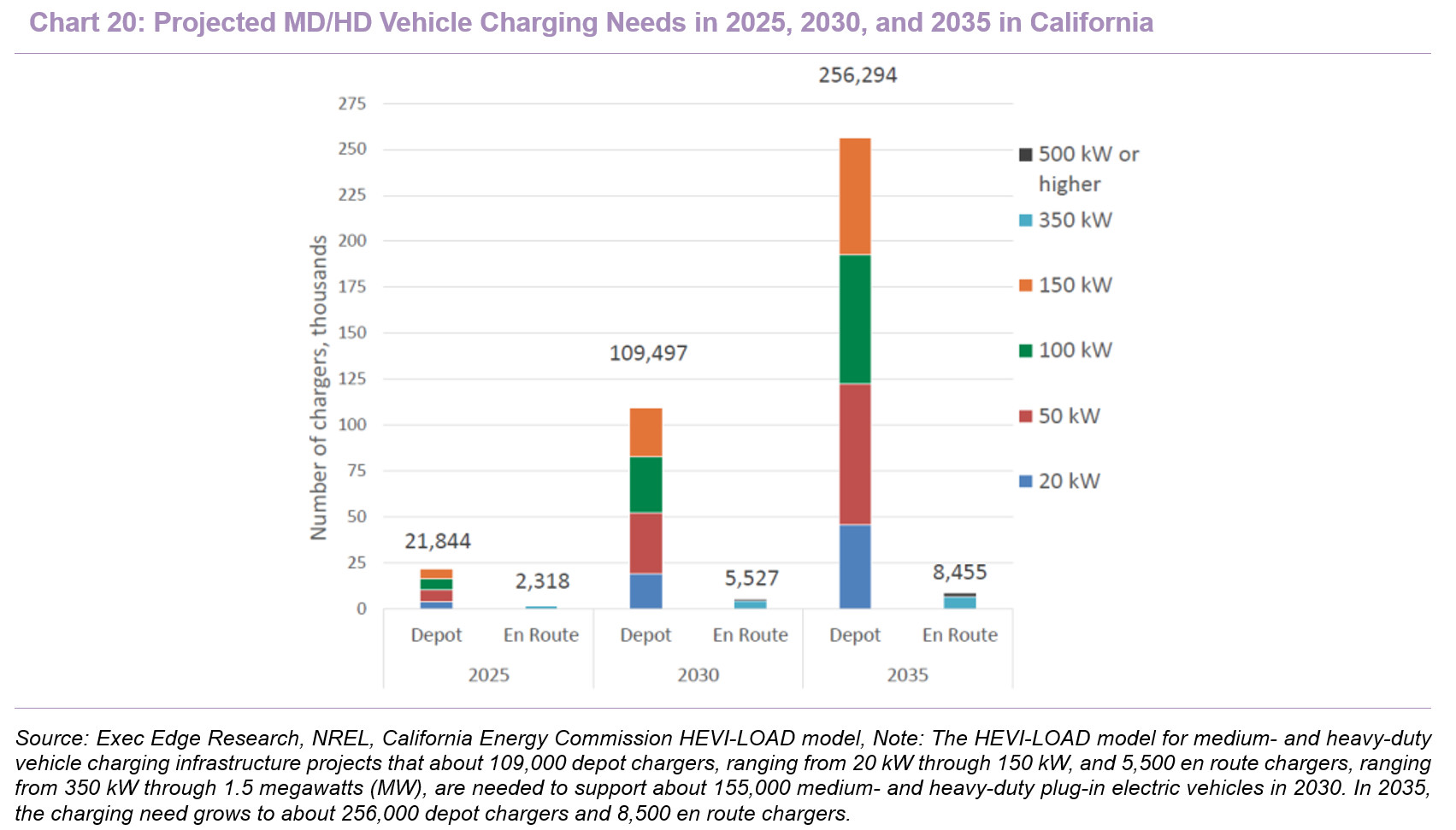

- We believe this energy volatility strengthens the case for smart charging infrastructure, particularly in freight applications where energy planning can be integrated with route planning, depot operations, and customer demand. Electrification does not remove energy-cost exposure, because electricity prices and demand charges can also vary, but it changes the nature of the exposure by allowing operators to plan charging windows, use depot charging, shift load to lower-cost periods, and optimize energy procurement around known route requirements. RMI estimates that managed charging during off-peak hours can reduce fleet electricity costs by up to 30%, while NREL has emphasized that depot charging is expected to be essential for medium- and heavy-duty (MD/HD) electrification because a large share of these vehicles operate within daily ranges compatible with depot-based charging. The infrastructure gap remains meaningful. McKinsey estimates Europe will need more than 300,000 public and private charge points for medium- and heavy-duty trucks by 2030, up from roughly 10,000 in 2024. The chart below reinforces that the next phase of freight electrification will be anchored in depot-based infrastructure rather than a passenger-EV-style public charging network. California’s charging-needs projection shows depot chargers accounting for approximately 95% of MD/HD chargers in 2030 and roughly 97% in 2035, underscoring why fleet operators need route-level energy forecasting, charging-site planning, and managed charging software before they can scale electric freight reliably. The next stage of freight electrification will therefore depend on more than charger deployment. It will require software that can forecast route-level energy needs, sequence charging, reduce peak-load costs, and coordinate vehicles, depots, utilities, and customer service commitments.

- ENRD is positioned to benefit because its model integrates electric trucks, charging infrastructure, and software-led energy orchestration rather than treating charging as a stand-alone asset. The company describes smart charging as the combination of smart energy, smart usage, and smart locations, with software connecting vehicle, route, and energy-system data to optimize charging requirements. Management has also stated that the goal of its charging infrastructure strategy is to provide the most efficient energy cost in customer operations. This makes ENRD’s infrastructure layer strategically relevant as shippers seek lower fuel-price exposure, better cost visibility, and partners capable of coordinating electrification across routes, depots, customer sites, and energy systems.

Driver Scarcity Supports ENRD’s Controlled-Lane Autonomy Strategy

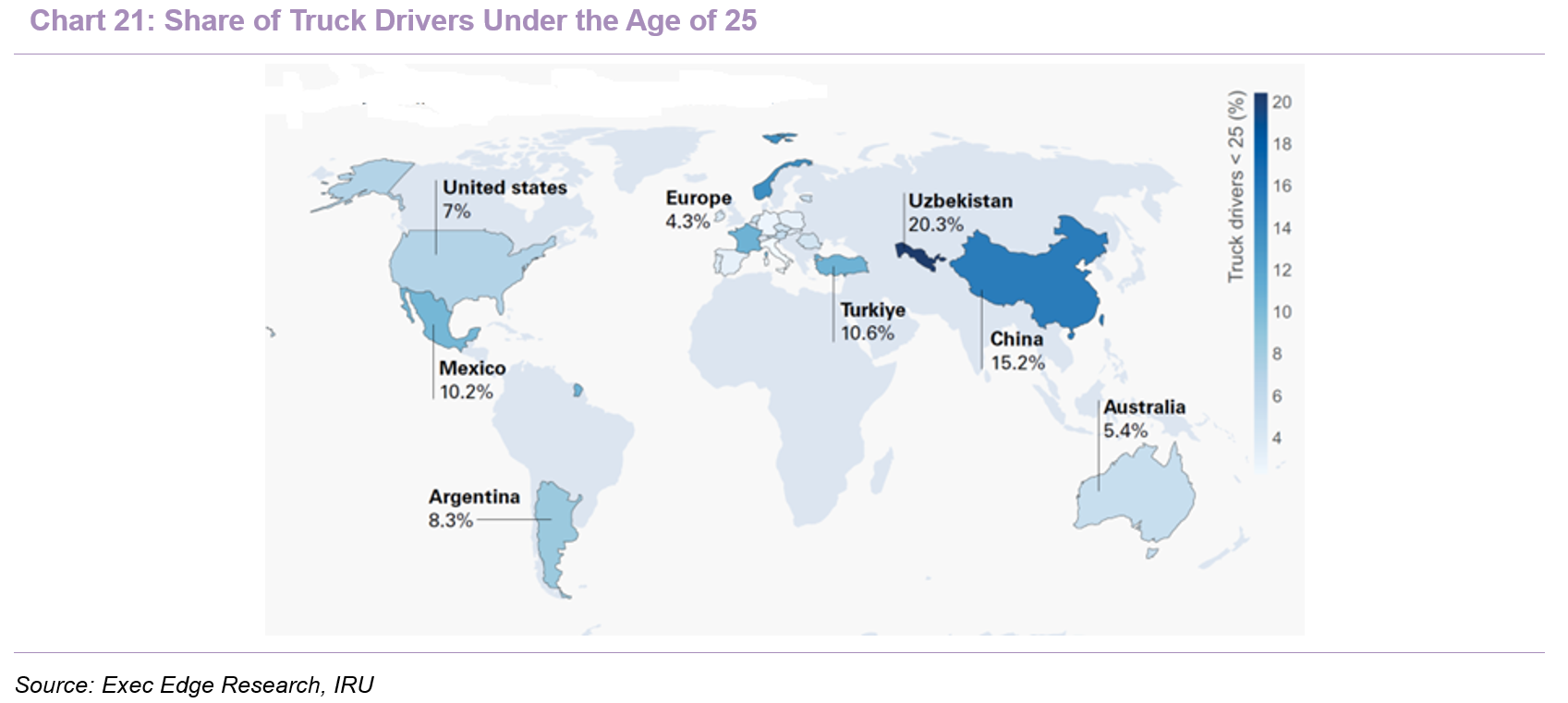

- Truck-driver availability has become a structural capacity constraint for road freight networks, with the shortage increasingly driven by demographics rather than only freight-cycle volatility. IRU’s 2024 Global Truck Driver Shortage Report found 3.6 million unfilled truck-driver positions across 36 countries representing 70% of global GDP, with more than 40% of companies in the countries studied reporting severe or very severe difficulty filling driver roles. The age profile suggests the gap could widen without a stronger inflow of new labor: drivers under 25 represent only 6.5% of the global driver workforce, while drivers over 55 account for 31.6%. IRU also forecasts 3.4 million drivers will retire by 2029 across the markets studied, including 17% of Europe’s current drivers. This creates a replacement problem for an industry whose service capacity is directly tied to driver hours, route coverage, and asset utilization. In the U.S., ATA reported 3.58 million professional truck drivers in 2024, while the Bureau of Labor Statistics projects 237,600 heavy and tractor-trailer truck-driver openings per year from 2024 to 2034, largely to replace workers who leave the occupation or retire. The result is a labor constraint that looks increasingly structural rather than purely cyclical.

- Driver recruitment friction and limited workforce participation compound the problem. The driver shortage is unlikely to be solved by wages alone, given the structural challenges of the role: extended time away from home, irregular schedules, safety risk, compliance burden, and limited appeal to younger workers. IRU’s driver shortage data emphasize that trucking companies face severe difficulty recruiting both young people and women, with women representing less than 7% of truck drivers in all countries covered by its analysis. That low participation rate matters because it limits the addressable labor pool at the same time the incumbent workforce is aging. In Europe, IRU’s 2024 survey estimated 426,000 unfilled truck-driver positions, and separate European Labour Authority analysis, citing IRU’s earlier work, found that 62% of European trucking companies reported severe or very severe challenges recruiting drivers. The same ELA analysis noted that Europe had 233,000 unfilled truck-driver jobs in 2023, equal to 7% of positions, showing that even during a weaker freight-demand period, vacancies remained material. Regulatory thresholds also slow replacement hiring in some regions because minimum age rules, training requirements, licensing, and cross-border qualification processes can delay entry into the profession. The result is a labor market where demand can recover faster than driver supply, increasing the strategic value of automation, remote operations, and route-level productivity tools.

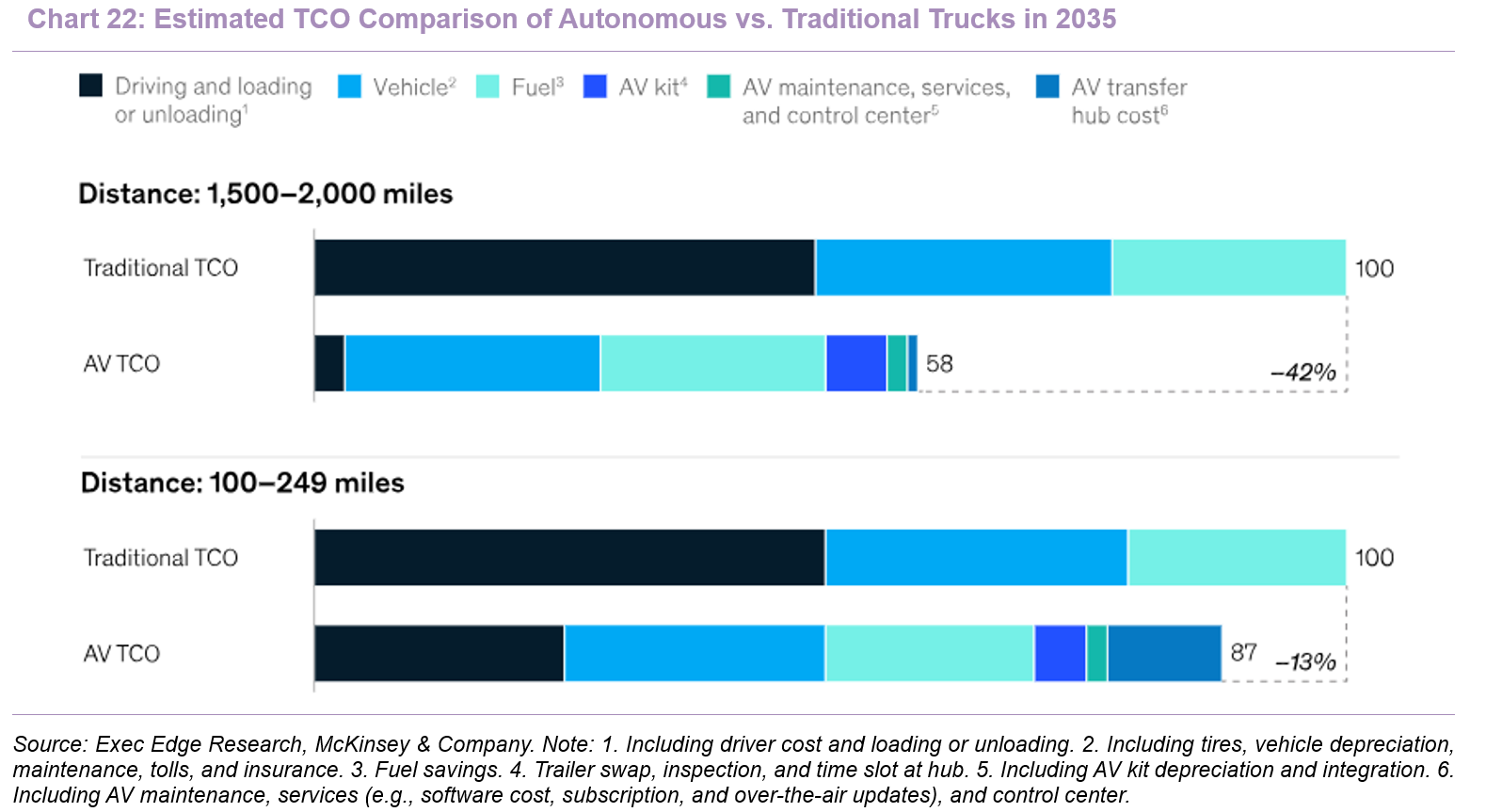

- We think driver scarcity increases the strategic value of autonomous trucks because onboard labor remains one of freight’s largest and least scalable cost inputs. Autonomous trucking does not eliminate the need for human oversight, maintenance, logistics planning, and remote operations, but it does reduce dependence on onboard drivers in defined operating domains, particularly repetitive middle-mile, yard, port, and hub-to-hub routes. McKinsey estimates the autonomous heavy-duty trucking market could reach ~$600 billion by 2035 across China, the U.S., and Europe, including $178 billion in the U.S. and $112 billion in Europe, which indicates that autonomy is becoming a meaningful prospective revenue pool rather than a narrow pilot category. The business case is strongest where freight lanes are repetitive, road conditions are well mapped, and operating environments can be controlled, allowing autonomous systems to improve asset availability and reduce labor exposure per mile. The chart below shows that by 2035, the autonomy business case will be most powerful in long-haul applications, where removing or reducing onboard driving time has a larger impact on total cost per mile. Autonomous TCO is estimated to be 42% below traditional TCO on 1,500-2,000 mile routes, compared with a 13% reduction on 100-249 mile routes, suggesting that long-distance, repeatable freight lanes are likely to be among the earliest high-ROI use cases. This makes driver scarcity a practical catalyst for autonomous freight adoption, especially in use cases where labor constraints are acute and operating domains can be clearly defined, validated, and repeated.

- ENRD is positioned to benefit from driver shortages through a near-term autonomy strategy focused on controlled, repeatable freight lanes rather than immediate long-haul disruption. ENRD’s current autonomous use case is concentrated in industrial environments, where factories, warehouses, and port-adjacent facilities create short, repetitive shuttle routes that are easier to map, monitor, permit, and scale. These controlled operating domains are an attractive starting point: they still face driver availability and labor-cost pressure, but carry lower execution complexity than open-ended long-haul networks with higher speeds, more variable traffic, and more complex interactions with other road users. ENRD’s GE Appliances deployment illustrates this deployment pathway, with two cab-less autonomous trucks in signed or operational deployment alongside a broader FCaaS relationship that includes 19 commercial electric trucks. Over time, management expects to expand autonomy into longer distances and higher speeds as its safety case, operating data, and regulatory footprint deepen. This positions ENRD’s opportunity less as an immediate leap to 1,500-mile autonomous routes and more as a staged autonomy playbook built first around controlled, repeatable freight corridors.

Emissions Reporting Pressure Makes Freight Decarbonization a Strategic Priority

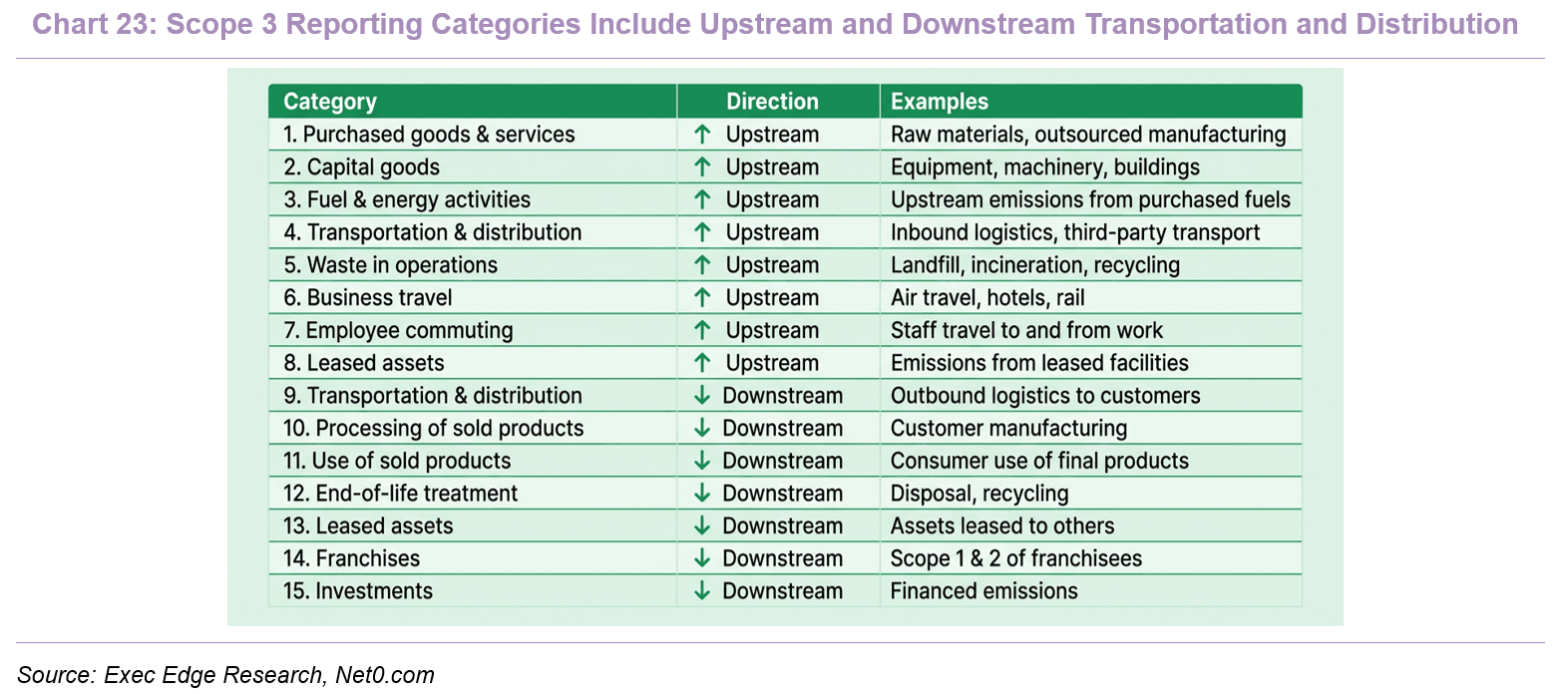

- Large shippers are facing rising compliance and reporting pressure around value-chain emissions, making freight transportation a more visible decarbonization lever. In Europe, the CSRD and ESRS E1 framework require in-scope companies to disclose gross Scope 1, Scope 2, and significant Scope 3 emissions, including upstream and downstream transportation. The EU’s 2026 simplification package narrows mandatory reporting to larger entities, but the direction of travel remains toward more structured emissions disclosure for major companies. In the U.S., California Senate Bill 253 adds another disclosure catalyst, with CARB confirming in 2026 that companies with more than $1 billion of annual revenue and business activity in California must begin Scope 1 and Scope 2 reporting in 2026, followed by Scope 3 reporting in 2027. Freight becomes directly relevant because upstream and downstream transportation sit within Scope 3 accounting, forcing large shippers to measure logistics-related emissions rather than treating freight as an outsourced operational issue. As reporting becomes more standardized, decarbonized freight procurement should increasingly move from a voluntary sustainability initiative to a compliance, data, and supplier-selection requirement for large retailers, manufacturers, and consumer goods companies.

- The pressure is also moving beyond disclosure into procurement behavior, as shippers need better freight-level data to credibly reduce Scope 3 emissions. Carbon Disclosure Project (CDP) notes that Scope 3 emissions are, on average, 26x greater than companies’ operational emissions, while its Supply Chain program requested environmental disclosure from approximately 45,000 suppliers in 2025. Science Based Targets initiative’s (SBTi) supplier engagement guidance similarly pushes companies with material Scope 3 exposure to set supplier engagement or reduction targets covering at least 67% of Scope 3 emissions when Scope 3 exceeds 40% of total Scope 1, 2, and 3 emissions. U.S. Environmental Protection Agency (EPA) SmartWay reinforces the same direction in freight, noting that shippers use freight emissions metrics to measure the environmental performance of carriers and logistics providers, and that diesel combustion produces roughly 20-22 pounds of CO2 per gallon. For logistics procurement, the implication is clear: shippers increasingly need partners that can measure, report, and reduce freight emissions at shipment or lane level. This should favor providers that combine transport execution with emissions data, route optimization, and verified operational performance.

- We believe fleet electrification remains the most practical near-term pathway for shippers seeking direct freight-emissions reduction, particularly on predictable regional and depot-based routes. IEA’s Global EV Outlook 2025 shows that global sales of electric medium- and heavy-duty trucks exceeded 90,000 units in 2024, up almost 80% y/y, although China accounted for more than 80% of global sales. Europe sold more than 10,000 electric trucks for the second consecutive year in 2024, while the U.S. sold more than 1,700 units, exceeding the cumulative number sold between 2015 and 2022. IEA also notes that electric heavy-duty model availability reached almost 800 models globally in 2024, with about 150 available in Europe and more than 140 in the U.S., suggesting OEM supply is broadening even if adoption remains early. The early use case is not full long-haul substitution. It is structured freight networks where route length, dwell time, charging access, and asset utilization can be planned. That fits the shipper need for measurable emissions reduction without waiting for the entire trucking market to transition at once.

- For ENRD, this trend supports demand for an integrated solution rather than a truck-only offering. Large shippers increasingly need freight decarbonization that is measurable, operationally reliable, and simple to procure, which aligns with ENRD’s Freight Capacity as a Service (FCaaS) model, Saga platform, emissions reporting, route planning, charging orchestration, and customer transformation programs. ENRD’s solutions can reduce customer transport-related CO2 emissions by up to 93% through connected electric trucks and up to 94% through autonomous trucks, while Saga provides visibility into operational performance and emissions. This makes Scope 3 reduction and reporting a core part of ENRD’s customer value proposition, particularly for blue-chip shippers facing rising disclosure, procurement, and supplier-accountability pressure.

Management Team

Roozbeh Charli-Led Continuity Supports ENRD’s Public-Market Scale-Up

- ENRD’s post-combination leadership structure combines operating continuity, capital markets experience, and founder-led board oversight. CEO Roozbeh Charli is expected to continue leading the company after serving across CFO, COO, Deputy CEO, and finance roles at Einride, while CFO Anubhav Verma adds public-company, M&A, and SPAC transaction experience. The board is expected to include founder Robert Falck as Chairman, preserving direct continuity with Einride’s technology and commercialization history. Legato III’s Eric S. Rosenfeld and Gregory Monahan are also expected to join the board, adding SPAC, governance, audit, and public-market experience as ENRD transitions to Nasdaq-listed company status. The result is a leadership structure well matched to ENRD’s next phase of listed-company execution.

Growth Strategy

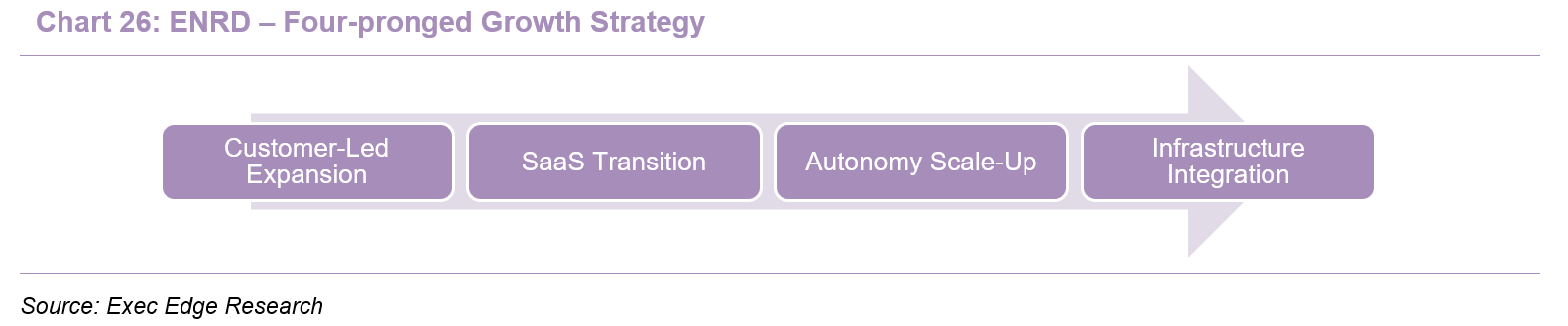

Scaling Freight Transformation Through Software, Autonomy, and Infrastructure

- ENRD’s growth strategy is anchored in converting customer freight-transformation roadmaps into contracted deployments, while expanding the software, autonomy, and infrastructure layers needed to scale with lower capital intensity over time. The company is using FCaaS to enter and prove customer networks, SaaS licensing to extend Saga AI and the Einride Driver across third-party fleets, autonomous deployments to increase operating leverage, and charging infrastructure to support reliable electric freight at scale. Together, these initiatives position ENRD to evolve from deployment-led growth toward a broader platform model.

- Convert Transformation Programs and JBPs into revenue-generating deployments. ENRD’s first growth priority is converting customer transformation programs and joint business plans (JBPs) into signed deployments, using data-led freight-network analysis as the bridge between strategic planning and revenue realization. The company begins customer engagements by ingesting transport data into Saga, identifying lanes that can be electrified immediately, routes where autonomous operations may become viable, and broader network areas where deployment can scale over a five-year horizon and beyond. This process follows a three-step journey: develop a holistic view, create a long-term plan, and execute on transformation, with $800 million+ of potential ARR in JBPs across logistics, consumer goods, retail, and industrials. ENRD has already translated part of this pipeline into $92 million of ARR in signed customer contracts as of February 2026, while management noted at the March Analyst Day that contracted ARR had increased by more than 50% over the prior six months. Recent developments support this land-and-expand strategy, including 2025 expansion into Austria through an existing customer, UAE entry through DP World, PostNord’s Norway expansion to 1.3 million electrified transport km annually, and Coop Sweden’s regional grocery deployment across 23 stores and 659,000+ annual transport km, with Coop and ENRD expecting ~912 tons of annual CO2 emissions removal once the deployment reaches full scale in 1H26. This creates a clear land-and-expand pathway, with JBPs defining the roadmap and signed deployments converting that roadmap into revenue visibility.

- Shift more deployments toward asset-light SaaS models. ENRD’s next growth lever is to deliver more customer deployments through software-led models, using the Einride Platform to optimize electric freight and the Einride Driver to support autonomous operations. While FCaaS remains the company’s primary ARR base today, ENRD expects a growing share of JBPs and future Transformation Program opportunities to move toward SaaS over time. The strategic importance is not just demand generation, but delivery model evolution: customers can operate their own vehicles while ENRD supplies the planning, optimization, reporting, and autonomous-driving technology layer. This should lower ENRD’s capital intensity as deployments scale, while preserving the software and data relationship at the center of the customer workflow. Management’s March Analyst Day materials frame this opportunity across four deployment settings, spanning FCaaS and technology licensing, including Saga AI licensing for customer- or third-party-owned electric trucks and ADS licensing for autonomous use cases. Over time, this could expand ENRD’s addressable market beyond shippers seeking a full turnkey service, while keeping the company embedded in the software layer that governs electric and autonomous freight execution.

- Expand autonomous and dual-use applications. ENRD’s third growth lever is to scale autonomous freight from proven commercial deployments into broader customer rollouts. The strategy is built around the Einride Driver, Control Tower, and cab-less autonomous trucks, allowing ENRD to offer driverless operations as part of an integrated freight transformation rather than as a standalone technology pilot. ENRD already has three Autonomous Trucks in active operations companywide, including two cab-less autonomous trucks in operations with GE Appliances as of December 2025, and has recorded more than 3,300 driverless hours in contracted customer operations. GE Appliances remains the clearest commercial proof point: between January 2024 and December 2025, ENRD’s autonomous trucks in the GE Appliances network delivered 61,000+ units, completed 1,000+ shipments, transported 1,700+ tonne-km, operated at ~94% autonomous drive mode, and achieved ~99% delivery precision. Management also indicated at the March Analyst Day that roughly 20 autonomous trucks were expected to be deployed over the next six months, suggesting ENRD is moving from selective deployments toward a broader operating ramp. The company’s regulatory footprint supports this path, with permits or operations across the U.S., Sweden, Norway, and Belgium, alongside ongoing engagement in the UAE.

- ENRD’s U.S. autonomy roadmap has also become more specific around Texas. In March 2026, ENRD announced its fifth NHTSA approval to operate autonomous vehicles on U.S. roads and described Texas as a core hub for U.S. autonomous freight operations. ENRD also signed an MoU with SH 130 Concession Company to position the Austin-San Antonio SH 130 corridor as a preferred autonomous freight corridor, with the collaboration covering safety validation, first- and last-mile connectivity, EV charging, specialized docking requirements, and potential Saga AI integration with SH 130’s digital ecosystem. This makes ENRD’s autonomy strategy more integrated than standalone: driverless operations are being scaled inside customer freight networks where the company already manages planning, charging, execution, and performance data.

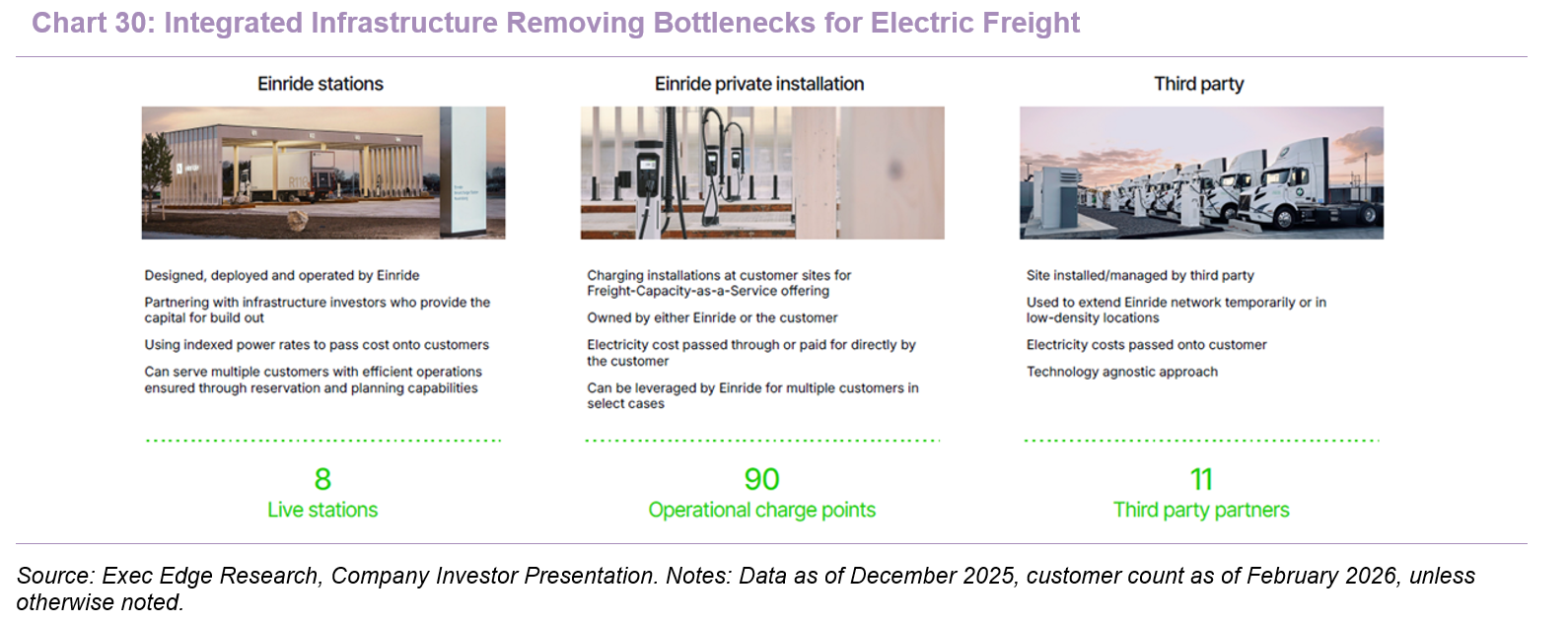

- Invest in a vertically integrated charging and infrastructure ecosystem. ENRD is investing in the infrastructure layer needed to remove one of the primary bottlenecks to electric freight adoption: reliable, heavy-duty charging access. The company is deploying its proprietary Smartcharger network, including private installations at customer facilities and larger charging hubs, to support vehicle uptime and reduce operational complexity for shippers operating in a still-fragmented public charging landscape. The Amazon partnership reinforces this infrastructure-led model, with ENRD expected to provide both electric trucks and supporting charging infrastructure across five U.S. locations, while Saga AI manages execution for select loads, including charging planning. ENRD also partners with third-party charging networks to broaden interoperability, extend coverage, and optimize energy access across customer routes. ENRD expects proceeds from the Legato III transaction, including the PIPE, to help fund this build-out. The SH 130 MoU broadens the infrastructure narrative from depot charging toward corridor-level autonomous freight infrastructure. ENRD and SH 130 plan to develop a blueprint for a next-generation rest stop designed for electric autonomous trucks, including high-capacity EV charging and specialized docking requirements, while also evaluating Saga AI integration with SH 130’s digital ecosystem. Although still early-stage, the initiative reinforces the view that autonomous electric freight will require coordinated infrastructure, software, and route operations rather than chargers alone. Over time, charging hub rollout should serve as a key indicator of ENRD’s ability to scale fleet deployments and support broader adoption of zero-emission freight networks.

- Near-term execution should be measured by ENRD’s ability to close the Legato transaction, continue expanding contracted ARR, convert JBPs into deployed revenue, scale autonomous truck deployments, and announce further dual-use or technology-licensing wins.

Fundamentals and Valuation

Contracted Demand and Unit Economics Support Path to Financial Inflection

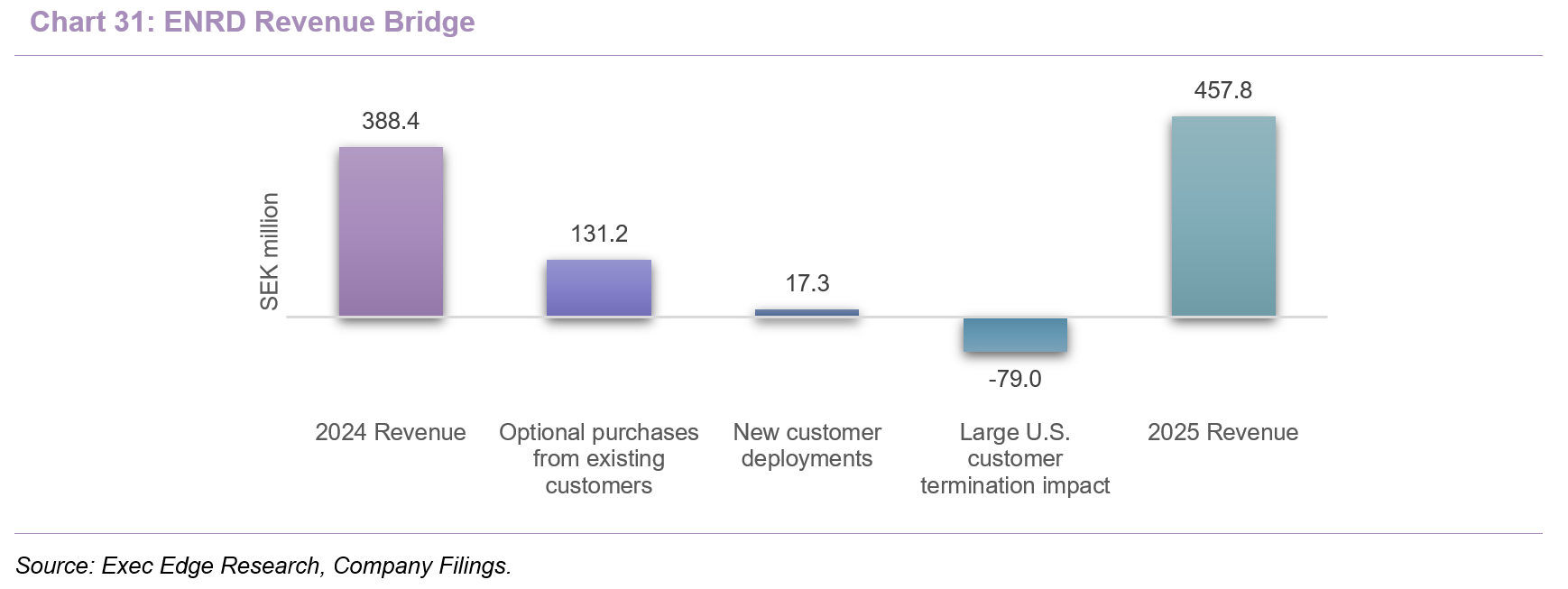

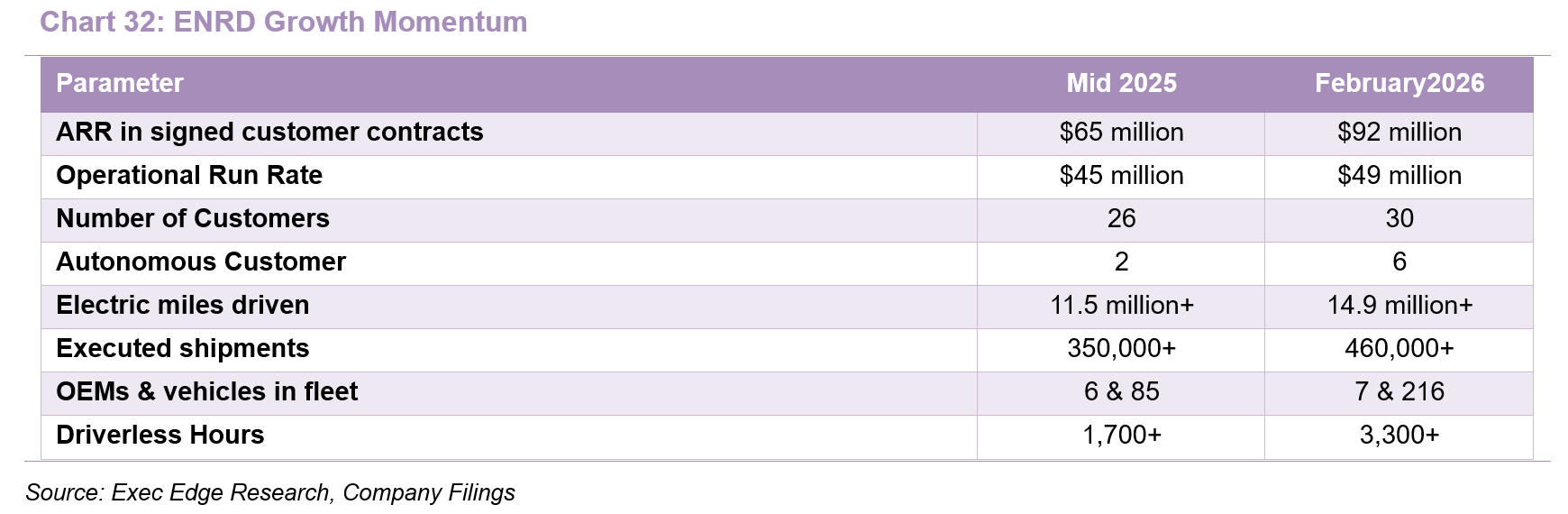

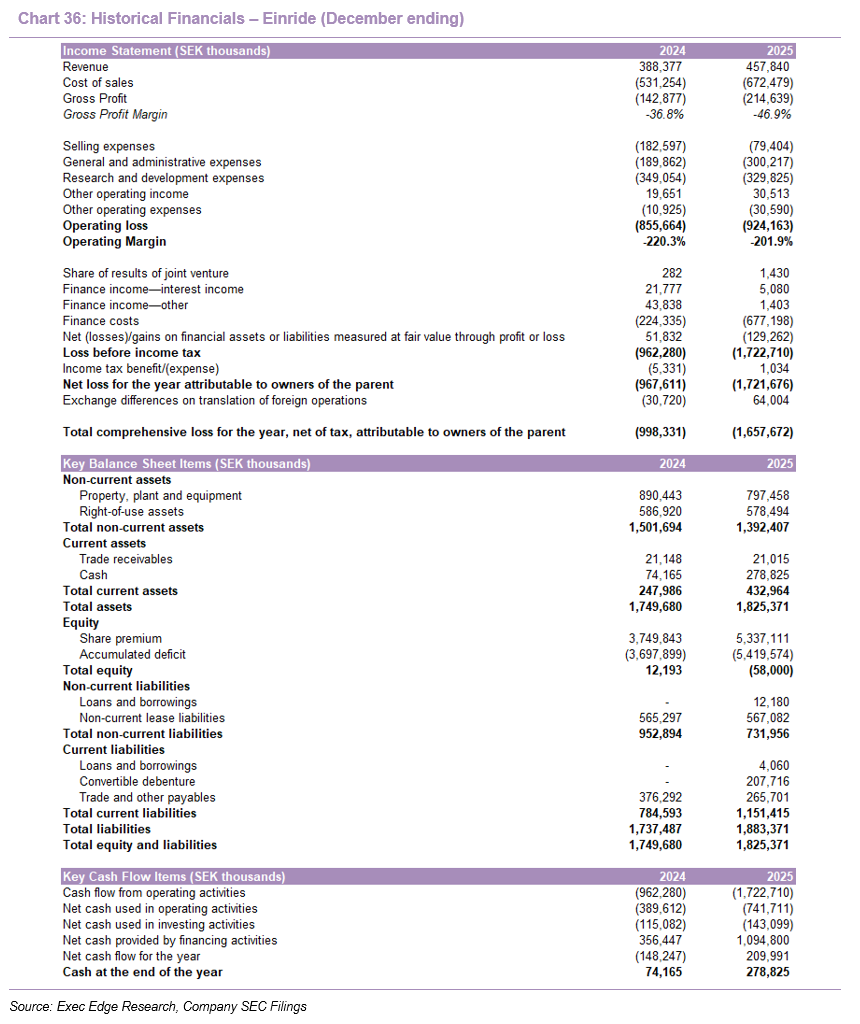

- ENRD’s 2025 financials show a business with meaningful commercial validation, though still early in converting signed demand and customer roadmaps into reported revenue. Revenue increased 18% y/y to SEK 457.8 million in 2025 from SEK 388.4 million in 2024. Growth was supported by SEK 131.2 million of optional purchases for additional capacity within the existing customer portfolio and SEK 17.3 million from new customer deployments, partly offset by a SEK 79.0 million headwind mainly tied to the March 2025 termination of a large U.S. customer contract. Excluding that terminated contract, revenue increased by SEK 128.6 million, or 39%, which better reflects expansion within continuing customer relationships. The more important investment lens, however, is the gap between reported revenue and the contracted / planned opportunity. Management has cited ~$92 million of ARR in signed customer contracts, of which ~$40-$50 million was deployed and flowing through reported revenue, alongside $800 million+ of potential long-term ARR in JBPs. As a result, ENRD’s current revenue base captures only part of the commercial opportunity already identified across its customer network, with execution now centered on converting signed ARR and JBP roadmaps into deployed, revenue-generating capacity.

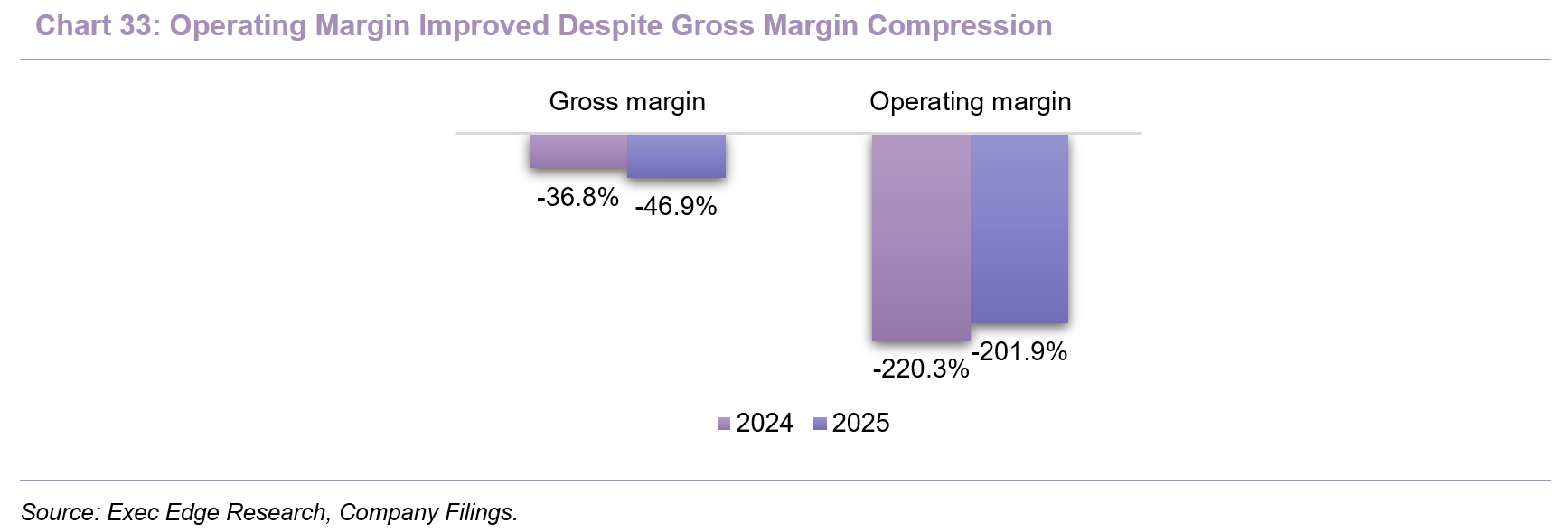

- Margin profile should improve as FCaaS deployments scale, fleet utilization recovers, and the business mix shifts toward autonomy and software-led revenue. Cost of sales increased 27% y/y to SEK 672.5 million, outpacing revenue growth and driving gross loss to SEK 214.6 million. Gross margin declined to -46.9% from -36.8% in 2024, reflecting higher volumes, new EMEA vehicle investments to support deployments, and U.S. fleet utilization that had not fully recovered following the large customer termination. Operating loss widened 8% to SEK 924.2 million, but operating margin improved to -201.9% from -220.3% as operating expense discipline partly offset gross margin pressure. Selling expenses declined 57% to SEK 79.4 million following cost-reduction initiatives, while R&D declined 6% to SEK 329.8 million. G&A increased 58% to SEK 300.2 million, largely reflecting business-combination costs and legal advisory fees, with underlying G&A described as broadly stable. Overall, the P&L reflects a company still investing ahead of scale, with near-term margins pressured by underutilization, deployment costs, and public-company preparation, but with clearer operating leverage potential as fleet density and software mix improve.

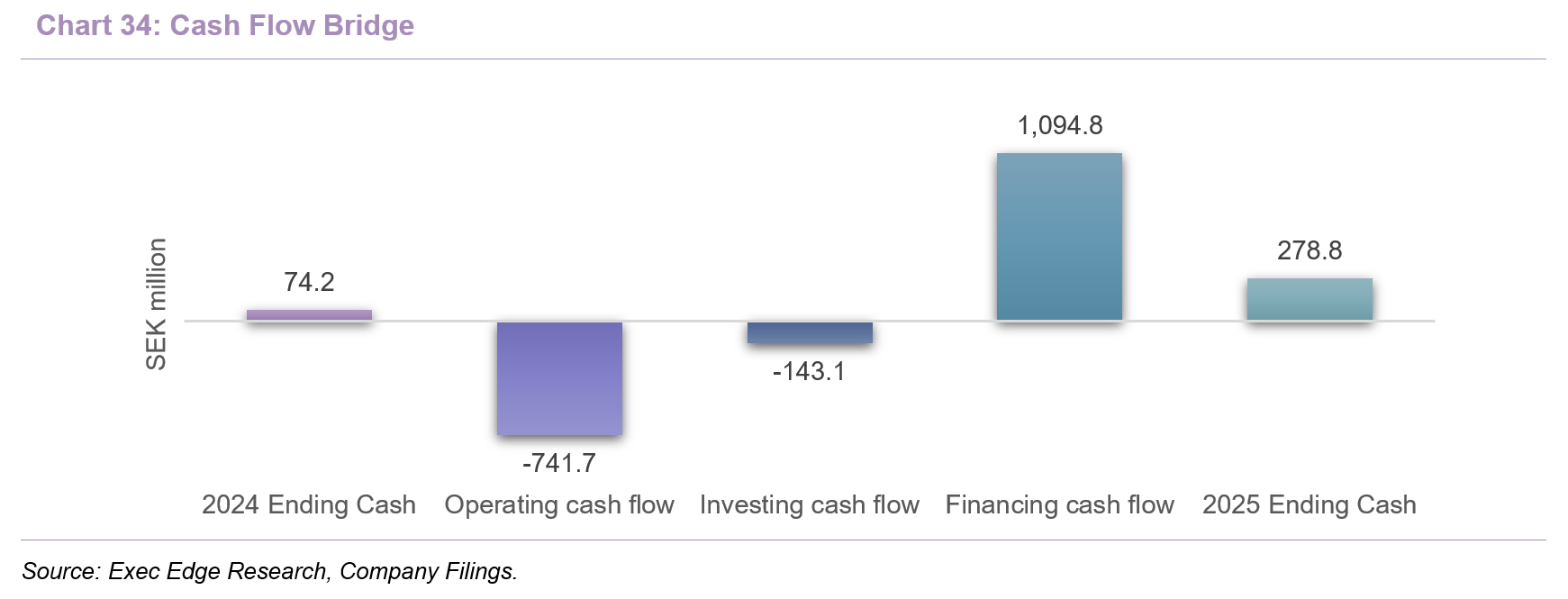

- The proposed transaction should enhance ENRD’s balance sheet flexibility as the company scales deployments and continues investing in product development. Cash increased to SEK 278.8 million at year-end 2025 from SEK 74.2 million in 2024, supported by SEK 1,094.8 million of financing cash inflow during the year. While ENRD remains in an investment-heavy phase, the Legato transaction is expected to strengthen liquidity, support continued development of the Einride Driver, and help fund the ramp of existing and new customer contracts. The key monitorable, in our view, is whether ENRD can pair visible commercial demand with sufficient capital and execution discipline to convert that demand into deployed revenue while reducing the cash intensity of growth.

- Cash flow remains investment-heavy, underscoring that ENRD is still funding the build-out of its platform rather than self-financing growth. Net loss increased to SEK 1,721.7 million in 2025 from SEK 967.6 million in 2024, while net cash used in operating activities increased to SEK 741.7 million from SEK 389.6 million. Investing cash outflow was SEK 143.1 million, broadly tied to continued property, plant, and equipment investment, while financing inflow increased to SEK 1,094.8 million, supported by equity / warrant proceeds, convertible debenture proceeds, and factoring facility activity. Cash ended the year higher, but the improvement was financing-led rather than operating-led. Management also expects continued losses and higher expenses as ENRD scales FCaaS, SaaS, autonomous trucks, charging infrastructure, R&D, regulatory compliance, and public-company functions. Against this backdrop, the transaction proceeds should provide useful runway, while lower cash intensity will depend on stronger utilization, ARR conversion, and a greater mix of software and autonomous revenue.

- Unit economics provide the clearest bridge from today’s losses to the potential financial model, but execution remains the key variable. Management indicated at Analyst Day that ENRD had roughly 200 trucks at customer sites, generating approximately $300,000 of annual revenue per truck and 20-25% contribution margin before asset cost. The medium-term path to cash flow breakeven is framed around roughly 1,500 trucks over the next 18-24 months, with long-term electric-truck FCaaS revenue per truck stabilizing around $400,000 and contribution margin moving toward 30-35%. Autonomy adds a second margin lever, with management discussing roughly 20 autonomous trucks expected to be deployed over the next six months. Management also framed autonomous trucks at ~20-25% contribution margin today, with revenue per truck expected to move toward ~$180,000 at cash flow breakeven as utilization improves and fleet monitoring costs decline. SaaS is the capital-light layer, with Saga AI licensing expected at $10,000-$15,000 per connected vehicle and ADS licensing framed at $70,000-$90,000 per deployed unit. In practice, the financial model improves as ENRD drives higher fleet utilization, adds more autonomous capacity, and layers software revenue onto a larger deployed base.

Contracted ARR and Commercial Autonomy Execution Support Valuation

- ENRD’s valuation appears constructive relative to commercial trucking autonomy peers, supported by contracted demand, multi-country deployment traction, and an integrated platform model. The following analysis is illustrative and should not be read as a price target or investment recommendation.

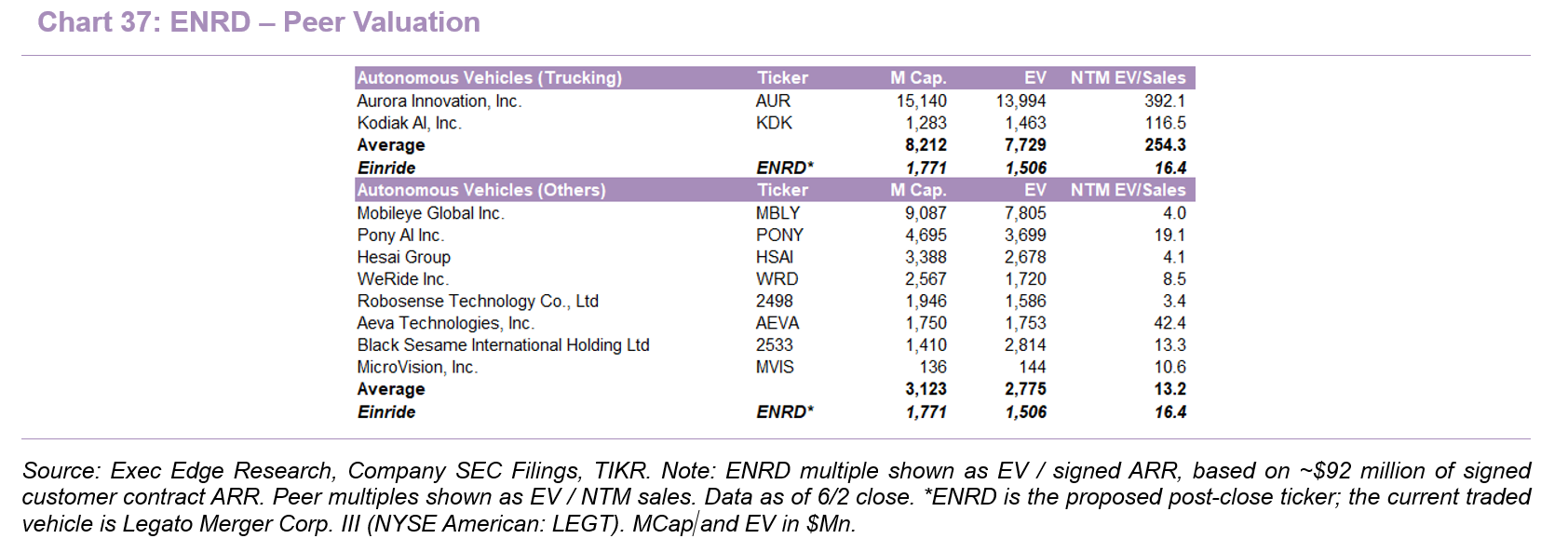

- ENRD is expected to enter the public markets at an implied equity value of $1.77 billion and enterprise value of ~$1.51 billion*. This is materially below Aurora at $15.14 billion EV and broadly in line with Kodiak at $1.28 billion EV. While each peer has a different operating focus, revenue base, and commercialization path, the comparison is useful because ENRD is not entering the market as a pre-commercial autonomy concept. The company has disclosed 30 customers, six fully autonomous driver-out customers, seven active countries, 3,300+ driverless hours in contracted customer operations, and a leaner operating footprint than larger autonomy peers. ENRD also brings a more integrated freight platform model than pure autonomy peers, combining Saga’s data layer, customer embeddedness, charging orchestration, cab-less hardware, and vehicle-agnostic software. ENRD therefore offers public-market exposure to commercial autonomous freight at an entry valuation that appears to discount both execution risk and the company’s differentiated deployment model. *Valuation based on current cash in trust and after giving effect to LEGT redemptions at the Extension Meeting and related founder-share forfeiture.

- We view signed ARR as the most relevant valuation anchor for ENRD because it better captures contracted commercial demand than reported historical revenue. ENRD’s implied EV equates to 16.4x EV / signed ARR, based on $92 million of signed customer contract ARR. This screens well below the trucking autonomy peer average of 254.3x NTM EV/Sales, though those multiples are elevated by the category’s still-early revenue base. ENRD is valued at a modest premium to the broader AV / sensing peer average of 13.2x NTM EV/Sales, which appears supportable given its direct freight operations exposure, signed ARR base, live customer deployments, and integrated software-plus-operations model. As deployment scales, reported revenue, gross margin recovery, and autonomy/software mix should become the more relevant valuation markers.

- The broader valuation support comes from ENRD’s moat profile and commercialization pathway, not ARR alone. ENRD’s combination of proprietary operating data, shipper embeddedness, live freight execution, charging orchestration, cab-less hardware, and vehicle-agnostic software creates a broader operating footprint than many autonomy or sensing peers tied primarily to software, hardware, sensors, or narrower deployment models. This helps support a premium to some horizontal AV / sensing peers, while still leaving ENRD at a meaningful discount to direct trucking autonomy comparables.

- Overall, ENRD’s valuation appears best supported by a commercialization-led framework that links contracted demand, deployment scale, and software/autonomy mix to future financial inflection. The $800 million+ JBP opportunity adds upside context, with value creation tied to conversion into signed deployments and reported revenue. The key milestones are clear: convert signed ARR and JBPs into deployed revenue, improve FCaaS utilization and gross margin, scale autonomous truck deployments, and prove that Saga AI and ADS licensing can reduce capital intensity over time. Delivery across these milestones should support a stronger valuation bridge toward the broader autonomy and intelligent mobility peer set.

Risks

- Commercial scale: ENRD’s ability to commercialize its Einride Driver, Control Tower, Saga, CETs, Autonomous Trucks, connectivity, and charging infrastructure at scale remains subject to execution risk. The company must continue improving autonomous performance, complete testing and validation, expand operating domains, integrate hardware and software, maintain third-party relationships, and scale customer deployments. Delays or technical shortfalls could slow adoption, increase costs, or weaken customer confidence.

- Profitability and funding risk: ENRD has generated recurring losses and may not achieve or sustain profitability on the timeline investors expect. The company incurred net losses in 2024 and 2025 and expects continued investment in FCaaS, SaaS, autonomous trucks, charging infrastructure, product development, sales, regulatory compliance, and public-company functions. If revenue growth, fleet utilization, or SaaS adoption lags spending, ENRD may require additional capital or face pressure on margins and cash flow.

- Platform dependence: ENRD’s commercialization depends heavily on Saga’s ability to optimize electric and autonomous freight at increasing scale. If Saga cannot process additional data sources, support a larger vehicle base, or deliver reliable route, energy, charging, and operational planning, ENRD’s value proposition could weaken. Platform limitations, integration issues, software failures, or slower-than-expected feature development could impair execution and reduce the company’s ability to convert customer roadmaps into profitable deployments.

- Customer adoption: ENRD’s results depend on maintaining, expanding, and converting relationships with large enterprise customers. Sales cycles can be lengthy, customers may delay deployments, renegotiate agreements, reduce transport needs, or decline to renew and expand contracts. Because ENRD’s strategy relies on scaling from initial deployments into broader transformation programs and JBPs, slower customer adoption or weaker conversion of signed plans into operating revenue could materially affect growth and revenue visibility.

- Safety incidents: ENRD’s brand and regulatory standing could be affected by collisions, product defects, operational incidents, or perceived weaknesses in autonomous and electric freight technology. Any incident involving the Einride Driver, Autonomous Trucks, CETs, Control Tower, charging infrastructure, or related software could lead to litigation, recalls, operating suspensions, permit revocation, regulatory scrutiny, or negative publicity. Such outcomes could slow customer adoption and make future autonomous deployments harder to approve or commercialize.

- Unit economics: ENRD’s investment case depends on achieving expected FCaaS and SaaS unit economics, but actual economics may differ from management targets. Customer demand, utilization, contract terms, pricing pressure, capital expenditures, carrier costs, insurance, maintenance, supplier terms, and competitive dynamics could all affect revenue per vehicle and contribution margins. If ENRD cannot improve utilization or transition more deployments toward higher-margin software and autonomous models, long-term profitability could fall short of expectations.

- Energy constraints: ENRD’s electric freight model is exposed to battery, electricity, and grid constraints. The relative cost of electricity versus diesel, battery prices, supply shortages, raw material inflation, and local grid capacity can influence the competitiveness and deployment pace of electric trucks. Inadequate charging availability, higher energy costs, or grid bottlenecks could delay customer deployments, reduce operating efficiency, or make certain routes less attractive for electrification.

- Regulatory complexity: ENRD operates in a highly evolving regulatory environment for autonomous and electric transport. There is no unified global framework for autonomous freight, and requirements vary across U.S. federal and state agencies, European jurisdictions, and other markets. ENRD may need additional permits, exemptions, audits, safety evidence, cybersecurity controls, or operating approvals to scale. Failure to obtain or maintain approvals could restrict deployment, increase compliance costs, or limit the company’s addressable operating domains.

- Transaction and public-market risk: ENRD’s public listing remains subject to shareholder approval, regulatory approvals, closing conditions, and market conditions. Redemptions, transaction delays, lower-than-expected cash proceeds, limited trading liquidity, or post-close volatility could affect ENRD’s capital position and investor perception. As a newly public company, ENRD will also face higher reporting, governance, compliance, and investor-relations requirements, which could increase costs and place additional demands on management.

Subscribe to our Weekly Newsletter to Receive All Research

Contact: