Download the Complete Report Here

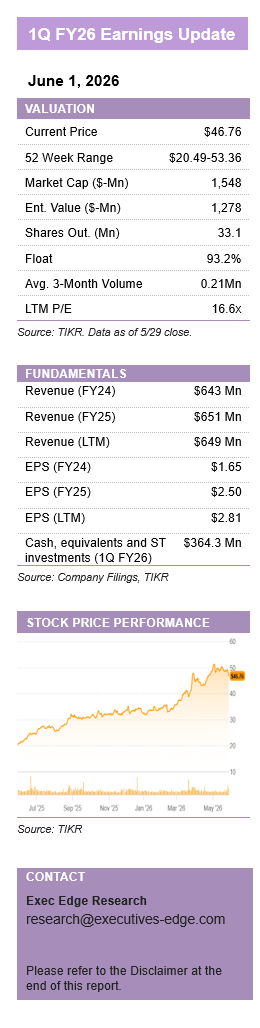

REX American Resources Corp. (REX)

REX American Resources Corp. (REX)

45Z and Lower Corn Costs Drive Record First Quarter; One Earth and CCS Projects Advance; Valuation Remains Reasonable

- Key Takeaways:

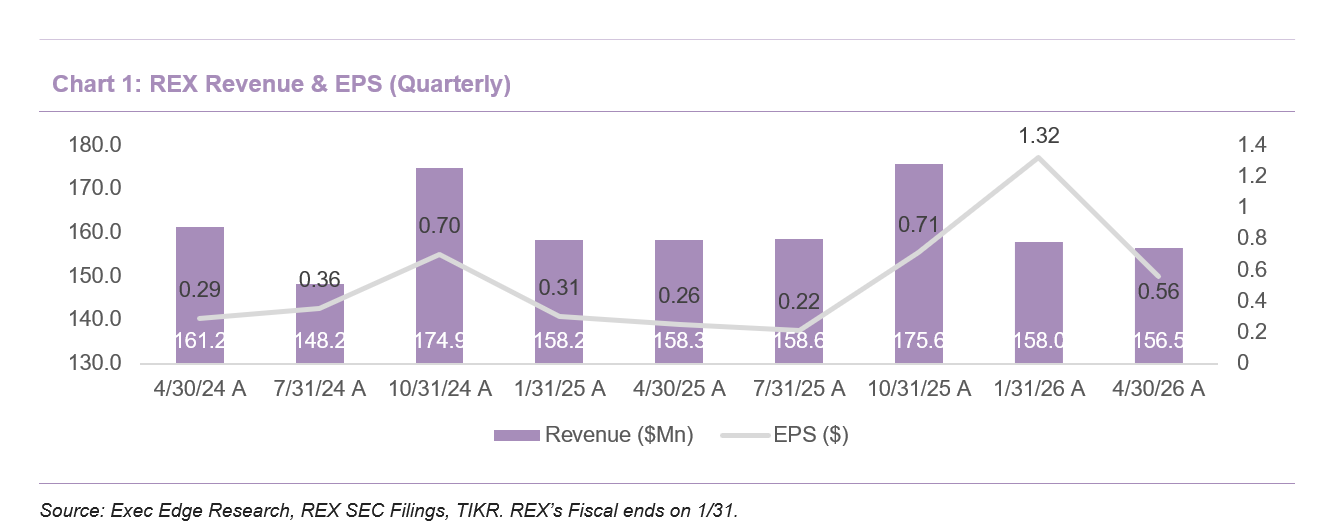

- REX delivered its best first-quarter EPS of $0.56, well ahead of consensus at $0.14 and up from $0.26 y/y.

- 45Z is becoming a structural earnings contributor, adding $7.5 million of production tax credit income at ~$0.10/gallon in 1Q FY26.

- One Earth expansion remains on track to become fully operational during FY26, with CCS / expansion spend reaching $176.3 million.

- Industry backdrop remains constructive, with stable domestic demand and ethanol exports through March up 20% y/y.

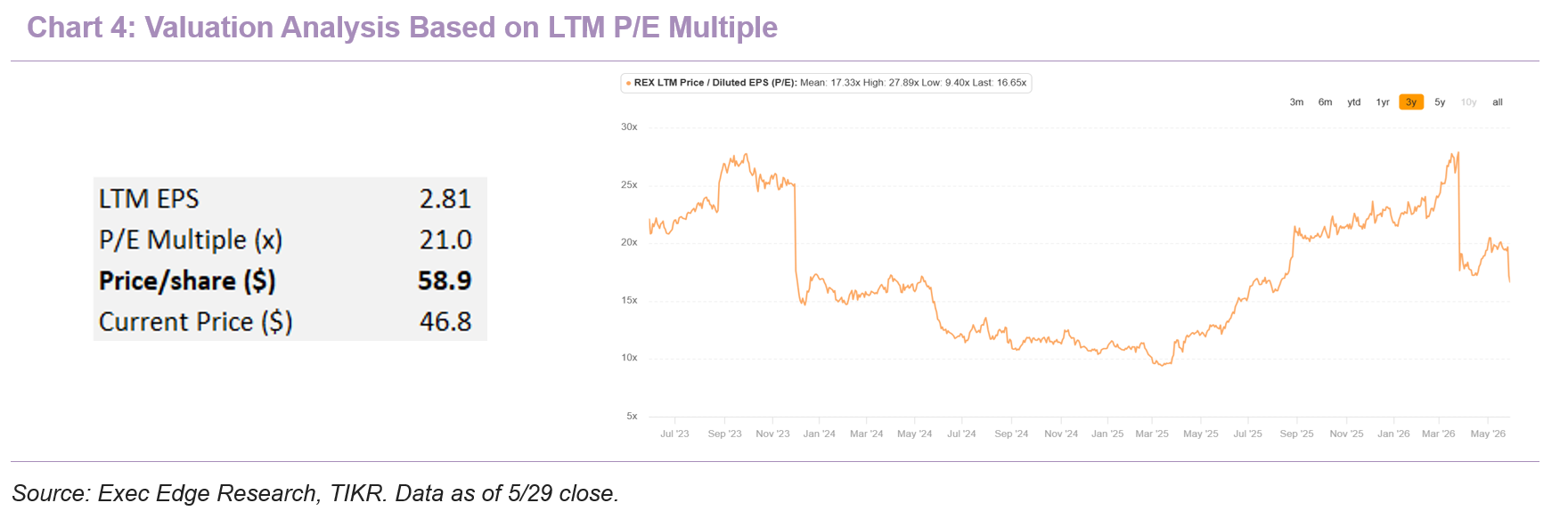

- Valuation remains reasonable at 16.6x LTM P/E, with further re-rating tied to 45Z scaling, One Earth completion, and CCS progress.

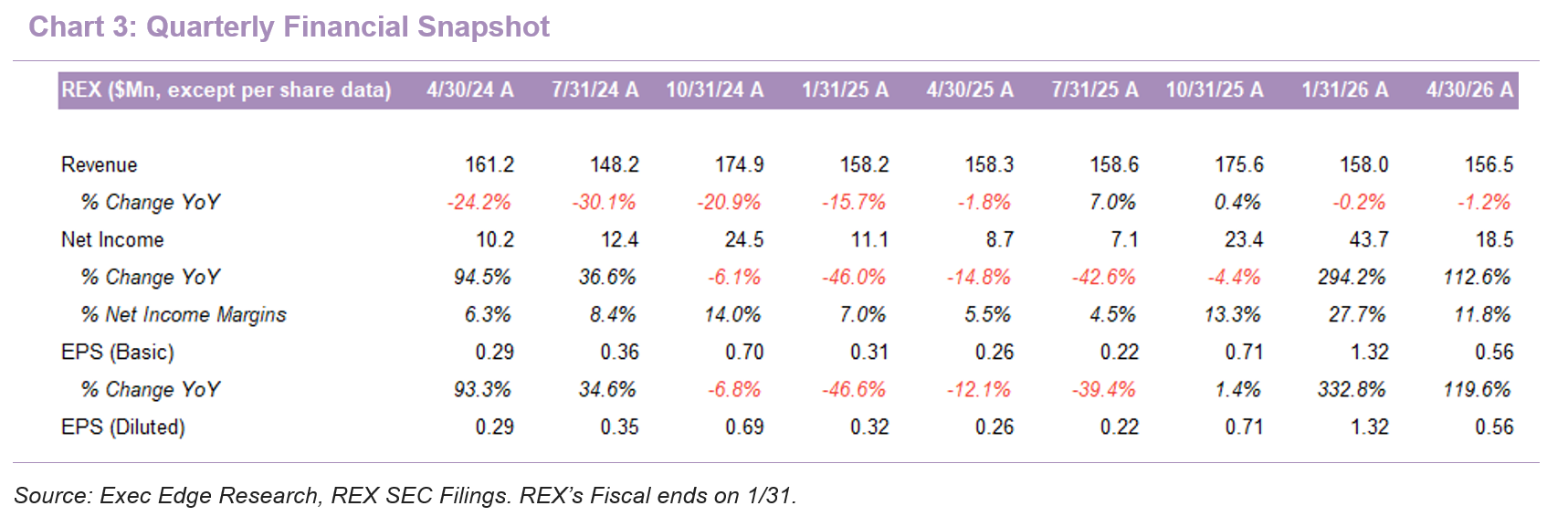

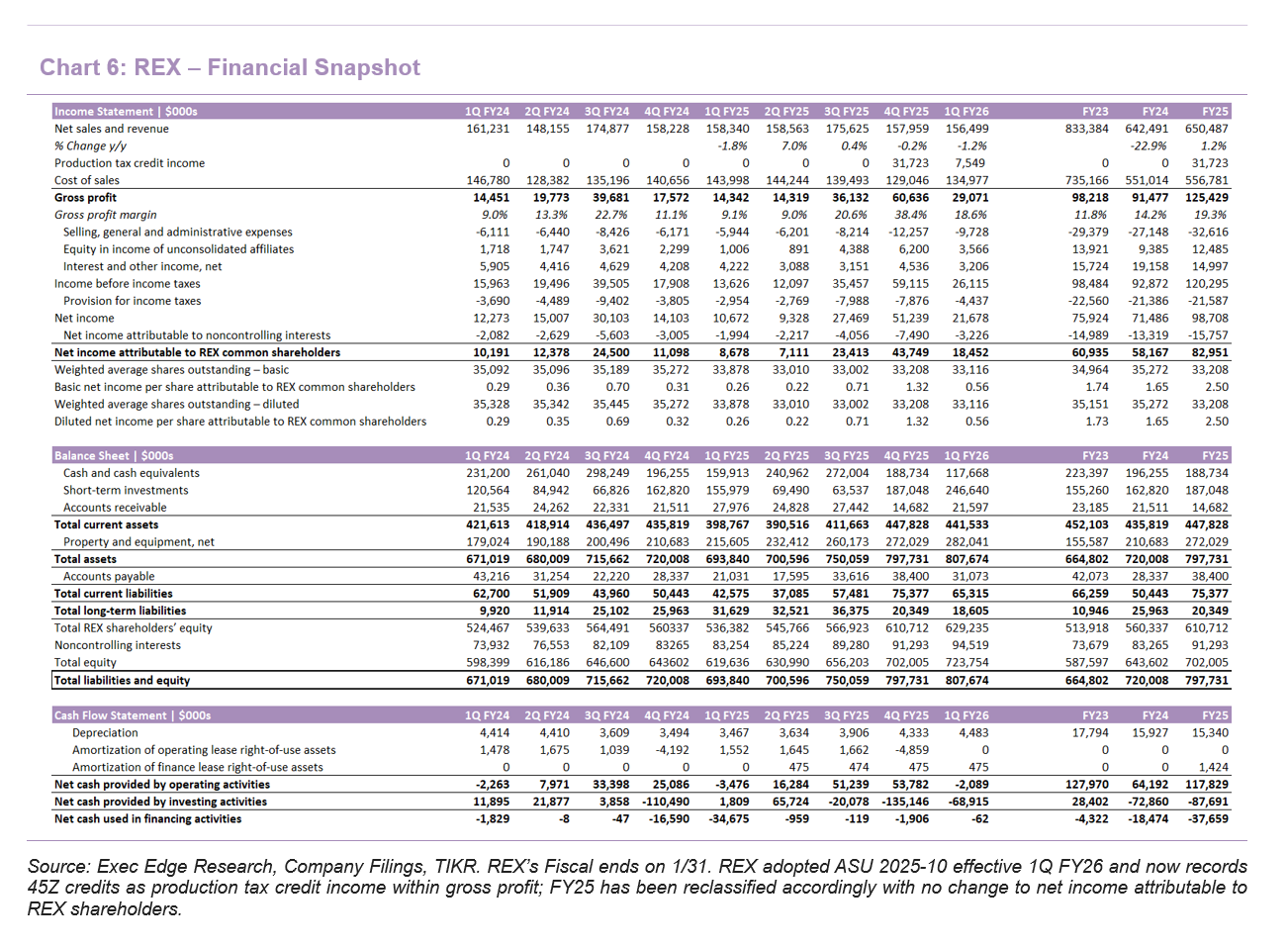

- 1Q FY26 delivered a record first quarter, with EPS materially ahead of expectations driven by 45Z credits and lower corn costs. REX reported 1Q FY26 net sales and revenue of $156.5 million, down modestly from $158.3 million in 1Q FY25, primarily reflecting lower ethanol pricing. However, earnings power improved sharply, with gross profit increasing to $29.1 million from $14.3 million y/y, primarily driven by the benefit of 45Z tax credits and lower corn pricing. Income before taxes rose to $26.1 million from $13.6 million. Net income came in at $18.5 million, or $0.56 per share, compared with $8.7 million, or $0.26 per share, in the prior-year quarter. EPS was also well above consensus of $0.14, representing a $0.42 beat, and marked the strongest first quarter (on an EPS basis) in REX’s public-company history. The quarter also extended REX’s profitability streak to 23 consecutive quarters, reinforcing the company’s ability to generate earnings through commodity cycles while layering in policy-linked earnings streams.

- Operating leverage was partly offset by SG&A rising to $9.7 million from $5.9 million y/y, primarily due to higher incentive compensation and unpaid 2025 stock bonuses recorded at fair value.

- Operating KPIs showed stable ethanol volumes, lower ethanol pricing, stronger distillers grain pricing, and continued support from corn oil. Consolidated ethanol sales volumes were 71.1 million gallons in 1Q FY26 versus 70.9 million gallons in 1Q FY25, indicating essentially flat y/y volume despite the ongoing One Earth expansion still not fully contributing. Ethanol ASP declined to $1.66/gallon from $1.76/gallon y/y, which pressured reported sales, but the earnings impact was more than offset by lower corn pricing and the new 45Z production tax credit income. Dry distillers grain volumes were approximately 155,000 tons, with ASP increasing to $155.86/ton from $145.65/ton y/y, while modified distillers grain volumes totaled 13,427 tons at an ASP of $76.94/ton. Corn oil volumes were approximately 23.9 million pounds, with ASP increasing to $0.54/lb from $0.46/lb y/y. The mix of stable ethanol volumes, stronger DDG and corn oil pricing, lower corn costs, and 45Z income drove a much stronger gross profit outcome even though headline revenue was down 1.2% y/y.

- 45Z has shifted from a potential catalyst to a visible operating earnings contributo REX recorded $7.5 million of 45Z production tax credit income in 1Q FY26, maintaining the credit at approximately $0.10/gallon across its consolidated plants while monitoring final regulatory developments. Following early adoption of ASU 2025-10, REX now records Section 45Z credits as “production tax credit income” within gross profit rather than as a tax-line item. Equity in income of unconsolidated affiliates increased to $3.6 million from $1.0 million y/y, with approximately $1.8 million of the increase attributable to 45Z tax credit income. This indicates that 45Z is contributing across both consolidated and unconsolidated plant economics, expanding the earnings base beyond the $7.5 million recognized directly in consolidated gross profit. The accounting change increased FY25 reported gross profit by $31.7 million but did not change FY25 net income attributable to REX shareholders, which remained $83.0 million.

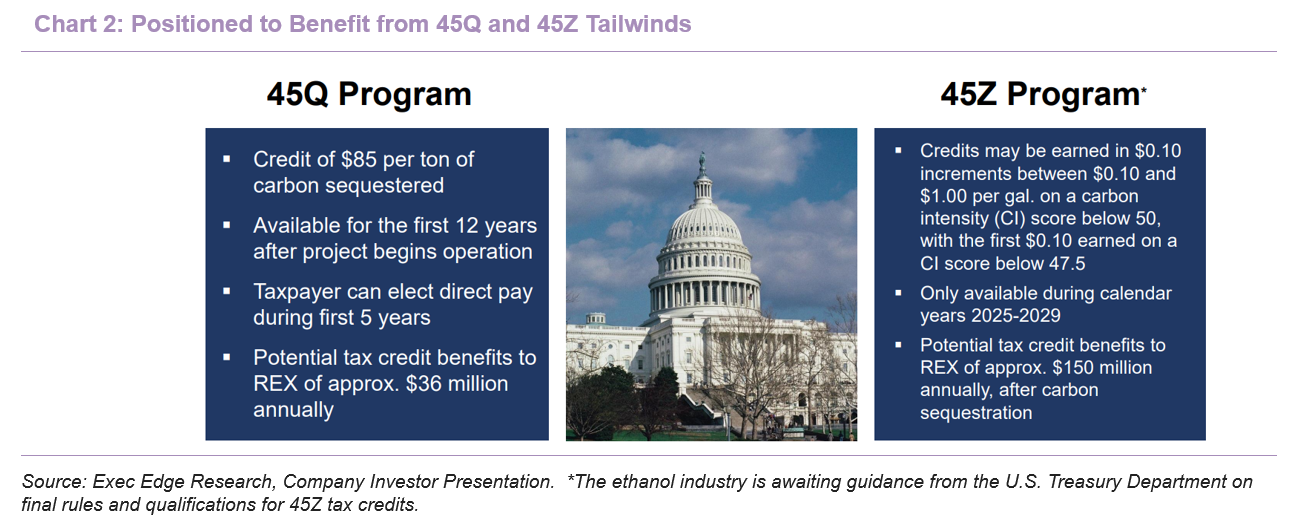

- 45Z is meaningful because it ties incremental earnings to production volumes and carbon intensity improvement, not just ethanol crush spreads. At the current ~$0.10/gallon booking rate, 45Z accounted for roughly 26% of 1Q gross profit of $29.1 million, implying that REX now has a recurring, policy-linked earnings layer tied to gallons produced and CI performance, rather than relying solely on ethanol crush spreads and co-product pricing. The company continues to monitor evolving federal discussions around Section 45Z, which still creates uncertainty around ultimate qualification and monetization levels, though current recognition supports 45Z as a meaningful earnings stream. Longer term, the carbon capture project should improve CI scores and enhance credit realization as One Earth capacity expands. As discussed in the 4Q earnings call, at full optimization, post carbon capture and with the One Earth expansion completed, credits of up to ~$1.00 per gallon could be achievable at certain facilities, implying a substantial step-up from current levels and reinforcing 45Z as a major long-term earnings driver.

- The One Earth expansion is a key volume and policy monetization catalyst, with the facility expected to become fully operational during FY26. REX’s ethanol facility expansion at Gibson City remains on schedule, with testing and commissioning expected to begin upon completion. The expansion increases REX’s production base at a time when export demand is strong and 45Z economics are now visible in reported results. While 1Q ethanol volumes were stable at 71.1 million gallons versus 70.9 million gallons y/y, incremental capacity from One Earth should support volume-led growth once fully operational. The strategic value of the expansion is enhanced by 45Z recognition, because each additional gallon potentially carries both core ethanol margin and production tax credit economics. This creates an operating leverage dynamic where higher production volumes can support revenue, gross profit, and policy-linked earnings simultaneously.

- Carbon capture remains the major medium-term value driver, with permitting the key milestone. REX continues to work with the EPA on its Class VI injection well permit application and remains engaged with the Illinois Commerce Commission on the associated carbon dioxide pipeline process. At the state level, the Illinois moratorium on carbon pipeline permitting is scheduled to expire on July 1, 2026, and REX plans to submit its application shortly after the moratorium expires. Total investment in the carbon capture and ethanol expansion projects reached approximately $176.3 million as of the end of 1Q FY26, up from approximately $166 million at FY25-end, and remains within the combined project budget range of $220 million to $230 million, subject to inflation and other market factors.

- Working capital and liquidity remain supportive, with the balance sheet absorbing capex while preserving strategic flexibility. REX ended 1Q FY26 with $364.3 million of cash, cash equivalents, and short-term investments and no bank debt, compared with $375.8 million at FY25-end, with the decline primarily reflecting ongoing capital investments in growth projects. Working capital movement was mixed, with accounts receivable increasing to $21.6 million from $14.7 million at FY25-end, while inventory declined to $26.5 million from $28.4 million and accounts payable declined to $31.1 million from $38.4 million. Net cash used in operating activities improved to $2.1 million from $3.5 million used in the prior-year quarter.

- Industry demand and forward outlook remain constructive, supported by stable domestic demand, strong exports, and continued execution on growth projects. Domestic ethanol demand remains stable, while export markets remain strong, with 2026 ethanol exports through March increasing 20% versus the same period last year, according to the Renewable Fuel Association. This export strength is important because 1Q ethanol ASP declined by $0.10/gallon y/y to $1.66, yet REX still delivered its strongest first-quarter EPS on a net income per share basis due to lower corn costs, 45Z contribution, and co-product pricing support. Operating conditions remained stable moving through 2Q FY26, and REX expressed confidence in delivering another profitable quarter. The medium-term setup remains tied to continued 45Z contribution at the current ~$0.10/gallon booking rate, One Earth volume growth, Class VI / pipeline progress, and eventual 45Q monetization.

- Reasonably valued given growth prospects and favorable industry and policy tailwinds. Our valuation incorporates multiple approaches, including historical trading ranges and peer comparisons. The analysis presented is for illustrative purposes only and does not constitute a price target or a buy/sell/hold recommendation.

- Despite strong 1Q FY26 earnings, REX remains reasonably valued relative to its improving earnings quality, policy-linked upside, and debt-free balance sheet. At the 5/29 close, REX traded at 16.6x LTM P/E, below its three-year peak of 27.9x, despite visible 45Z recognition, continued progress on the One Earth expansion and carbon capture initiatives, and favorable ethanol fundamentals. Key catalysts for further upside include continued 45Z contribution, the One Earth expansion becoming fully operational during FY26, progress on the Class VI permit and Illinois carbon pipeline process following the scheduled July 2026 moratorium expiration, and eventual 45Q monetization. Supportive industry fundamentals, including stable domestic demand, exports through March up 20% y/y, lower corn costs, and favorable ethanol economics, continue to support earnings visibility, while REX’s strong balance sheet, with no bank debt and substantial cash reserves, provides flexibility to fund growth initiatives while maintaining disciplined capital allocation.

- Time series valuation supports additional upside if earnings visibility continues to improve. REX currently trades at 16.6x LTM P/E, below its three-year peak of 27.9x, suggesting the stock remains below prior cycle highs despite a structurally improved earnings profile. Applying a 21x multiple (in line with industry average and conservative relative to REX’s historical multiple) to LTM EPS of $2.81 implies a value of approximately $59/share, indicating potential upside as 45Z contribution, One Earth volume growth, and carbon capture progress become more visible in the earnings base.

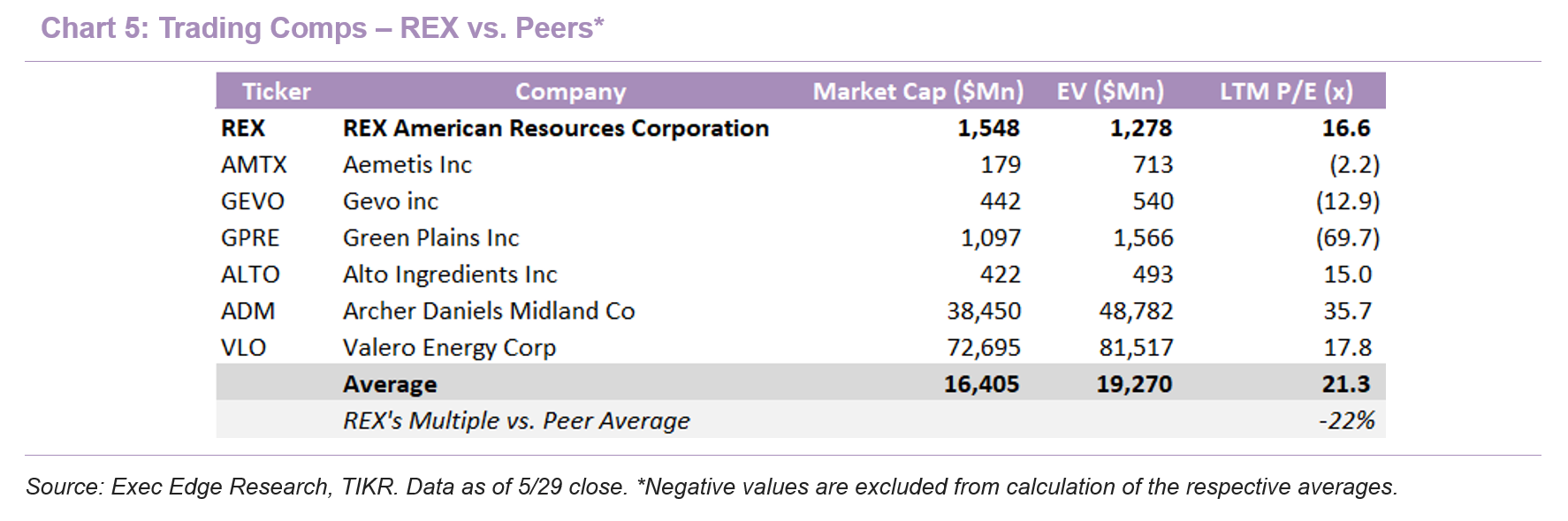

- Peer analysis also suggests room for further re-rating. REX trades below the peer average of 21.3x LTM P/E, despite its 23-quarter profitability streak, debt-free balance sheet, and increasing exposure to policy-driven earnings streams. This valuation gap suggests that the company’s improving earnings quality and structural growth drivers are not fully reflected, with further re-rating likely as execution across capacity expansion, carbon capture, and 45Z scaling continues.

Read Exec Edge’s Initiation on REX Here

Subscribe to our Weekly Newsletter to Receive All Research

Contact: