Download the Complete Report Here

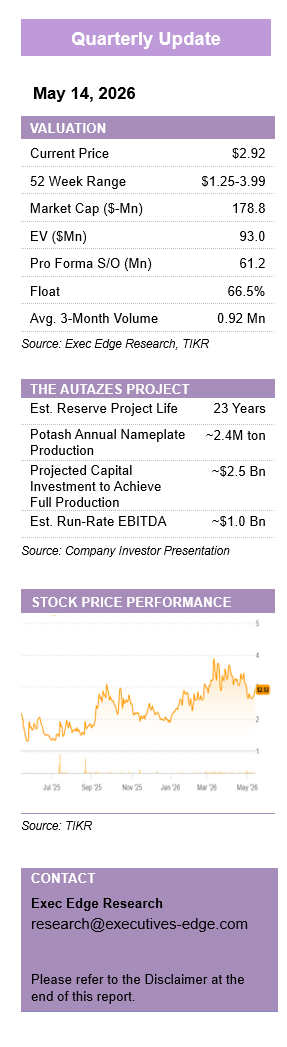

Brazil Potash Corp. (GRO)

Brazil Potash Corp. (GRO)

FEED Award and Equity Raise Improve Autazes Financing Visibility; 1Q26 Execution Supports Continued Project De-Risking. Valuation Remains Attractive.

- Key Takeaways:

- FEED award moves Autazes toward lender-ready execution planning, with Wood and Promon strengthening technical credibility and Brazilian delivery capability.

- The $63.3 million equity raise materially improves liquidity, supporting FEED, engineering, and development work while project financing discussions continue.

- 1Q26 progress across water rights, Mura engagement, and BOOT proposals further de-risked key regulatory, community, and infrastructure workstreams.

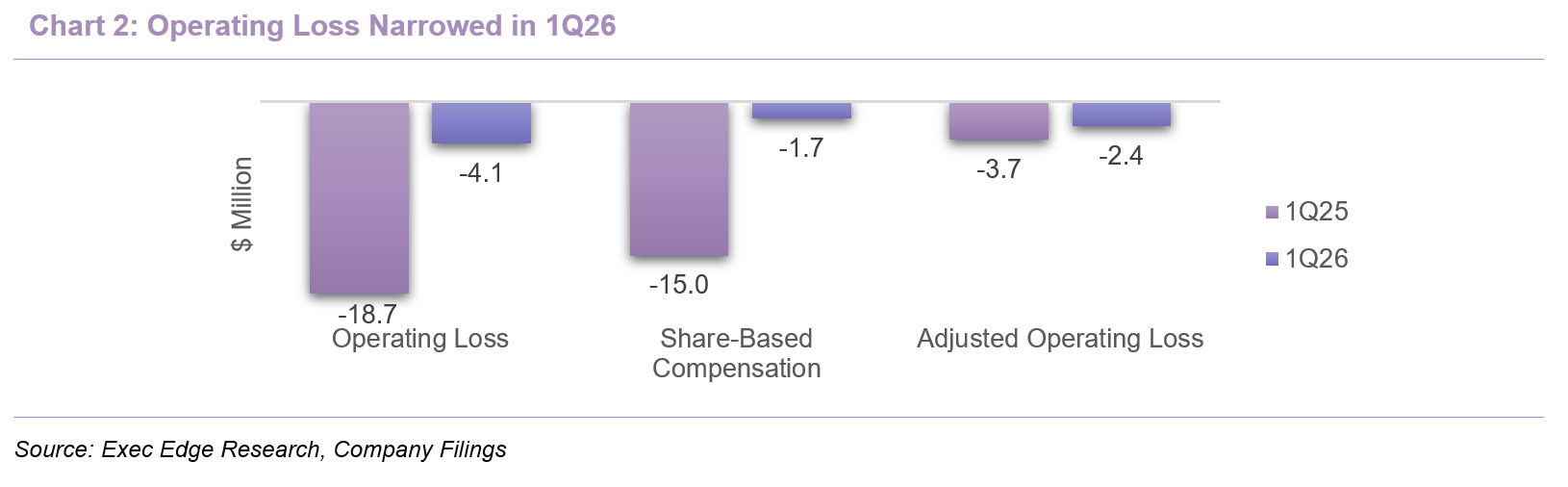

- Development-stage financials improved y/y, with operating loss narrowing to $4.1 million from $18.7 million on lower non-cash compensation.

- Valuation remains compelling at $93 million pro forma EV, with rerating tied to FEED completion and construction financing milestones.

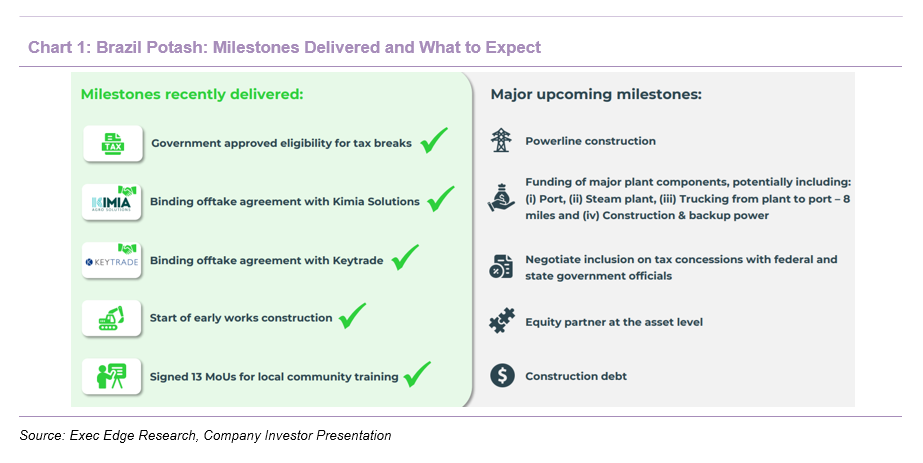

- Surface FEED contract award materially improves Autazes’ bankability and advances the project from permitting-led de-risking toward lender-facing execution readiness. In May 2026, GRO awarded the FEED contract for key surface infrastructure to a Wood plc and Promon Engenharia consortium, covering the processing plant, tailings facility, river barge port, and approximately 13 km of road upgrades linking the plant to the port. This scope is central to the project’s execution case as it ties together processing throughput, tailings handling, water balance, power requirements, port logistics, and construction sequencing into a single engineering framework. The FEED work should make the financing process more actionable by replacing broad project assumptions with diligence-ready engineering detail. That should improve lender confidence in the construction plan, sharpen the basis for cost and schedule discussions, and give DFIs, ECAs, infrastructure partners, and strategic equity investors a more concrete framework for evaluating risk, returns, and required capital commitments.

- The Wood-Promon consortium is important because it combines global potash engineering credibility with local Brazilian execution capability. Wood brings direct potash and fertilizer infrastructure experience, including K+S’s Bethune potash mine in Canada and multiple international potash expansions exceeding 8 million annual tons of production, which should support lender confidence in the FEED package. Promon adds more than 60 years of Brazilian EPCM and project management experience, including complex industrial, mining, and fertilizer projects, which is relevant given Autazes’ local engineering, licensing, logistics, and Amazonas State execution requirements. In our view, this combination strengthens GRO’s ability to deliver a financeable engineering package and advance discussions around construction debt, infrastructure funding, and anchor equity participation.

- Recently closed $63.3 million equity offering materially strengthens liquidity and improves GRO’s ability to advance Autazes while larger project financing discussions continue. GRO closed an underwritten public offering generating $63.3 million of gross proceeds, including full exercise of the underwriters’ option to purchase an additional 3.3 million shares. The financing included 7.0 million common shares issued at $2.50 per share and pre-funded warrants to purchase up to 18.3 million common shares at $2.499 per warrant, with proceeds intended for working capital and general corporate purposes. While not a substitute for the larger construction financing required to build Autazes, the raise is important because it extends corporate runway, supports ongoing engineering and development work, and gives GRO greater flexibility as it advances FEED, infrastructure funding discussions, and potential DFI/ECA-led construction financing.

- 1Q26 execution further de-risked Autazes and showed steady progress across the water, community, and infrastructure funding workstreams needed to move the project closer to construction readiness.

- Water rights approval improved project design and reduced execution complexity. ANA granted GRO a 10-year authorization to extract up to 2,400 m³/hour for 12 hours per day, or 10.5 million m³ annually, from the Rio Madeira. The approval allows the company to replace the original plan for 16 groundwater wells at 250 meters depth with surface water sourcing, reducing construction complexity and potentially lowering capital requirements. The water strategy also incorporates recycling, surface runoff capture, and water purification, which should help align the project design with environmental requirements while supporting processing needs. Together with 21 Installation Licenses already secured across the mine shafts, processing plant, eight-mile road upgrade, and river barge port, the water approval represents another tangible step in converting Autazes from a permitted development asset into a more execution-ready construction project.

- Stakeholder alignment progressed through a more formal community partnership framework with the Mura Indigenous Council. Through Potássio do Brasil, GRO signed a Term of Commitment and Cooperation with the Mura Indigenous Council, creating a framework for sustainable territorial development across 37 Mura villages in Autazes. The agreement supports the Bem Viver Mura Program across four pillars – social development, cultural appreciation, income generation, and institutional strengthening – with governance and monitoring mechanisms to track implementation. Indigenous engagement is central to Autazes’ project durability, permitting resilience, and community acceptance, and the agreement complements WSP Global’s ongoing work with Mura communities on demographic analysis, needs assessment, and development priorities.

- BOOT proposals add a potential capital-efficiency lever as GRO evaluates third-party funding for core infrastructure. GRO received third-party Build, Own, Operate and Transfer proposals covering several core infrastructure components, including the river barge port, steam plant, and a 20MW construction power system that is designed to convert into backup power during operations. These proposals remain under evaluation, but they are strategically important because third-party infrastructure ownership could shift a portion of project capital requirements away from GRO while preserving access to critical logistics and utility assets. For a development-stage company advancing a capital-intensive potash project, this type of structure could improve financing flexibility, reduce equity funding pressure, and help align specialized infrastructure operators with project execution.

- GRO’s 2026 execution agenda is now more clearly defined following the FEED award, equity raise, and 1Q26 permitting/community progress. The near-term roadmap is now centered on converting Autazes into a financeable construction package by completing FEED for surface facilities, continuing engineering work across mine shafts and processing infrastructure, and using the recently completed $63.3 million equity raise to support corporate runway and ongoing project advancement while larger funding discussions progress. The next major milestones remain securing construction debt, potentially through DFI/ECA participation, advancing third-party infrastructure funding for components such as the port, steam plant, and power systems, and identifying a strategic anchor equity partner at the project level to reduce reliance on corporate-level dilution. In parallel, the ANA water rights approval, 21 Installation Licenses, and formal Mura cooperation agreement provide a stronger regulatory and stakeholder foundation for moving toward long-lead equipment procurement, initial civil works, and eventual full-scale construction. With high offtake coverage, a clearer engineering path, improved liquidity, and continued alignment around Indigenous engagement, Autazes is increasingly positioned as a strategic domestic potash supply asset for Brazil’s import-dependent fertilizer market.

Development-Stage Financials Improve While Autazes’ Project Economics Remain Intact

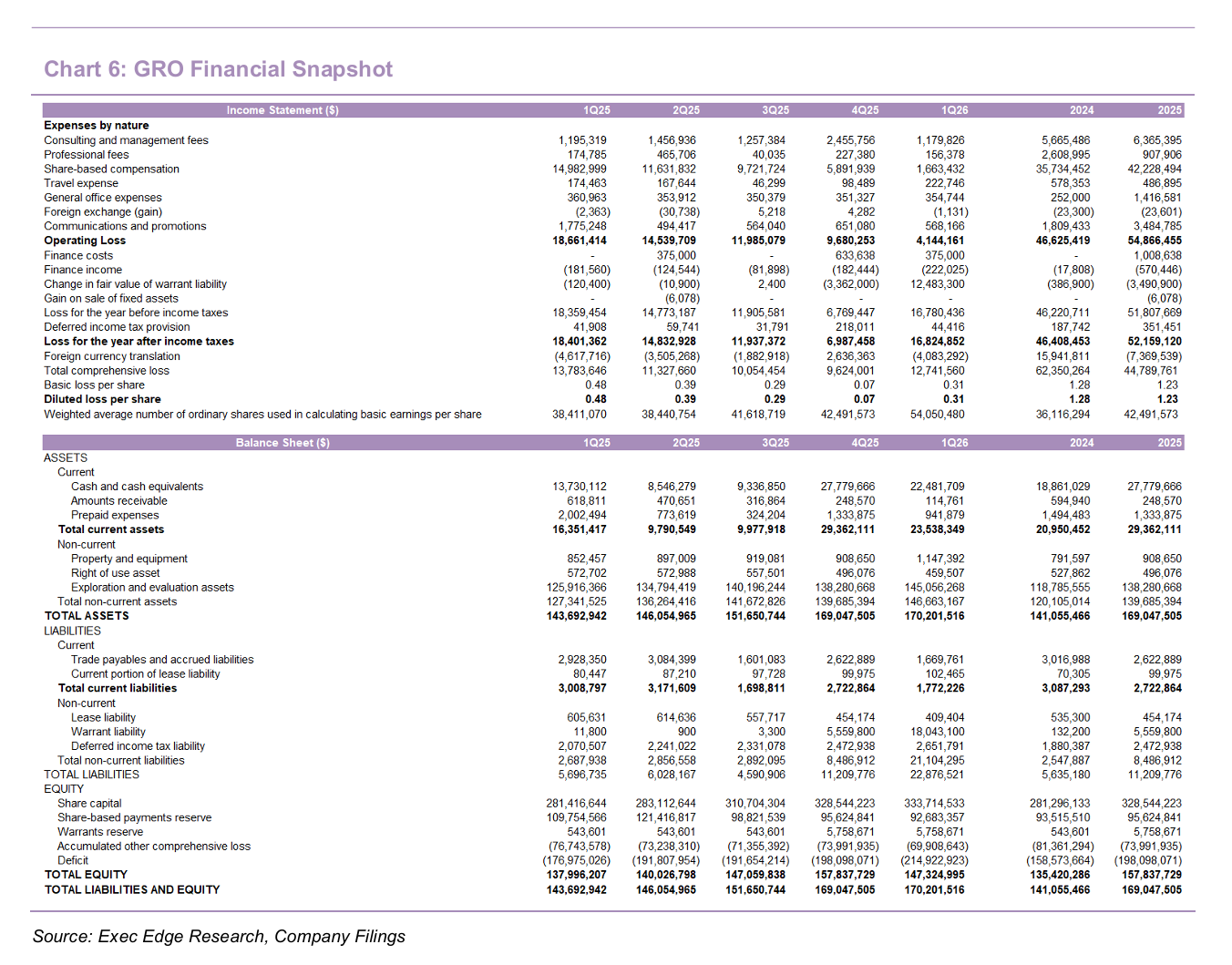

- 1Q26 financials remained consistent with GRO’s development-stage profile, with reported losses driven more by funding structure and non-cash items than operating deterioration. GRO has not yet commenced mining operations or potash production, so the income statement continues to reflect corporate costs, project advancement activity, and financing-related items rather than commercial operating performance. This profile should persist until Autazes reaches commercial production, which management has indicated could occur approximately four years after construction begins. The going concern language in the 1Q26 financial statements remains important, as the company is still dependent on external financing to fund construction; however, the recently completed $63.3 million equity raise improves near-term liquidity and partially mitigates corporate runway risk while larger project-level financing discussions continue.

- Operating loss narrowed sharply, reflecting normalization of non-cash compensation and lower promotional spending rather than a change in revenue trajectory. Operating loss improved to $4.1 million in 1Q26 from $18.7 million in 1Q25, primarily due to a material decline in share-based compensation, which fell to $1.7 million from $15.0 million in the prior-year period following elevated RSU amortization in 1Q25. Reduced communications and promotion expense also supported the y/y improvement, and no RSUs were granted during 1Q26. Excluding share-based compensation, adjusted operating loss was closer to $2.4 million in 1Q26 versus $3.7 million in 1Q25, suggesting a lower underlying corporate cost base while the company continues to advance permitting, engineering, financing, and stakeholder workstreams.

-

- Net loss improved only modestly because financing-related costs and warrant fair value movements offset most of the operating expense improvement. Net loss declined to $16.8 million in 1Q26 from $18.4 million in 1Q25, despite the $14.6 million improvement in operating loss, as the quarter included higher finance costs tied to shares issued under the equity line of credit and a $12.5 million non-cash loss from changes in the fair value of warrant liabilities. The key point is that reported net loss was shaped more by capital structure and mark-to-market items than operating spend, which improved y/y as GRO continued advancing Autazes.

- Operating cash burn improved y/y, while investing outflows increased as Autazes development activity continued. Net cash used in operating activities declined to $2.9 million in 1Q26 from $4.3 million in 1Q25, reflecting lower underlying corporate cash costs despite GAAP net loss volatility. Net cash used in investing activities increased to $2.3 million from $0.9 million y/y, primarily reflecting higher exploration and evaluation expenditures as the company continued advancing Autazes.

- Financing cash flow was minimal during 1Q26, with the more meaningful liquidity event occurring after quarter-end through the $63.3 million equity raise. Net cash used in financing activities was ~$50,000 in 1Q26, primarily lease payments, compared with ~$14,000 of net cash provided in 1Q25 from stock option exercises net of lease payments.

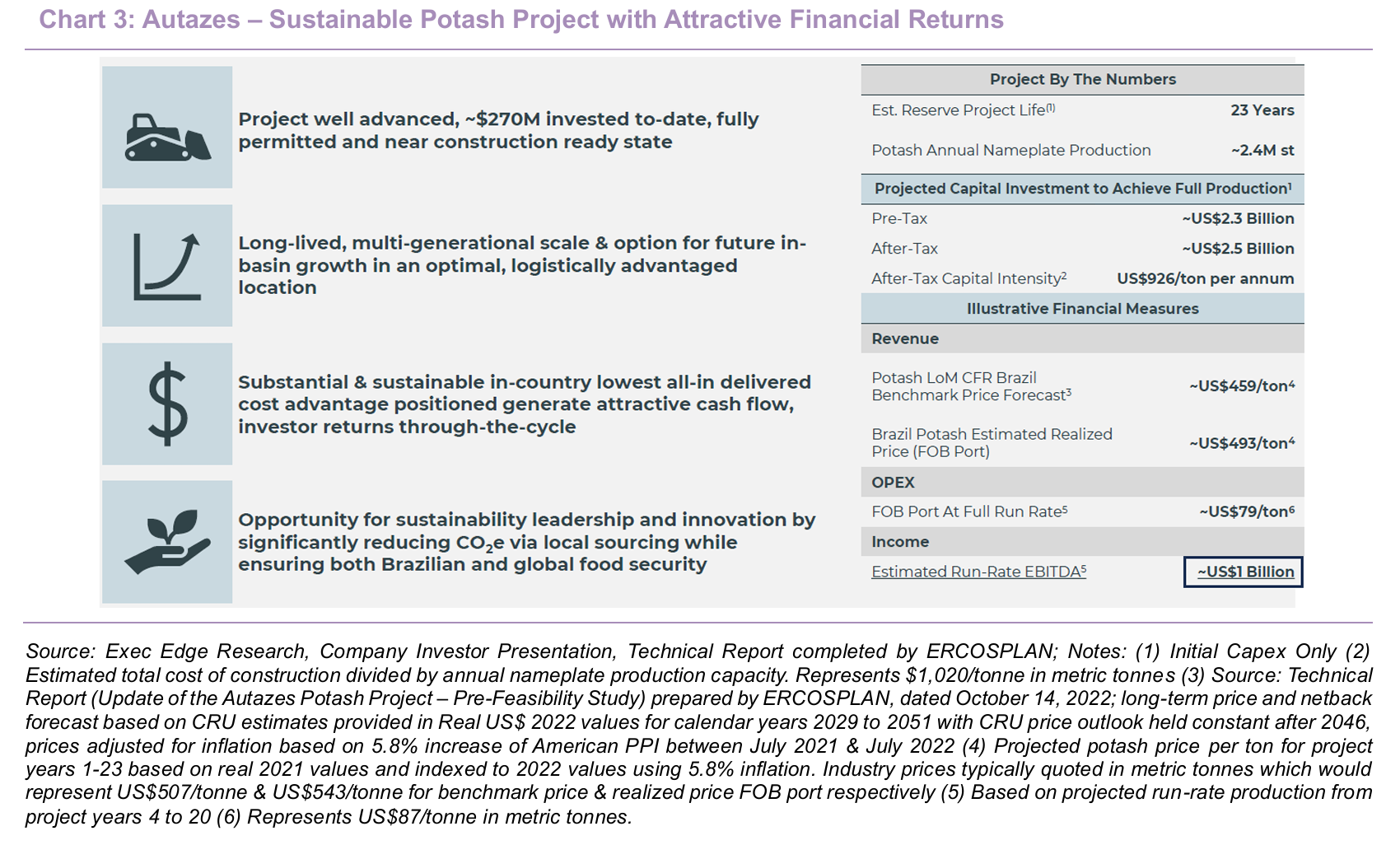

- Autazes’ long-term financial profile remains intact. Based on ERCOSPLAN technical report assumptions, management illustrates potential run-rate EBITDA of ~$1.0 billion at commercial scale, supported by an estimated realized price of ~$493/ton FOB Port and operating costs of ~$79/ton at full run-rate. This implies mine-gate gross margins above 80% and an EBITDA margin approaching ~75% after transportation, G&A, and financing costs, reflecting the project’s structural delivered-cost advantage in Brazil’s import-dependent potash market.

- The opportunity remains significant, though still execution dependent. Autazes is planned for ~2.4 million tons of annual production over a ~23-year reserve life, with projected capital investment of ~$2.5 billion, or ~$926 per ton of annual nameplate capacity. While the October 2022 pre-feasibility assumptions remain exposed to cost inflation, funding terms, potash pricing, and timing risk, they illustrate why FEED, construction financing, infrastructure funding, and stakeholder alignment are critical valuation catalysts.

- Cash declined sequentially during 1Q26, but post-quarter financing materially improved pro forma liquidity. Cash and equivalents totaled $22.5 million as of March 31, 2026, down from $27.8 million at year-end 2025, primarily reflecting $2.9 million of operating cash use and $2.3 million of investing outflows tied to exploration and evaluation expenditures at Autazes. Subsequent to quarter-end, GRO completed the $63.3 million equity offering, lifting pro forma cash to roughly $85.8 million before offering expenses and strengthening near-term liquidity as FEED, engineering, and construction financing workstreams continue.

Attractive Valuation Relative to Long-Term EBITDA Potential

- GRO’s current enterprise value implies a meaningful discount to Autazes’ potential steady-state economics, even after allowing for meaningful development-stage risk. The following analysis is illustrative only and does not constitute a price target or investment recommendation. Traditional earnings-based valuation is not directly applicable because GRO remains pre-revenue and construction financing has not yet been secured. However, peer multiple benchmarking provides a useful framework for understanding the gap between current market value and the potential production-stage value of Autazes.

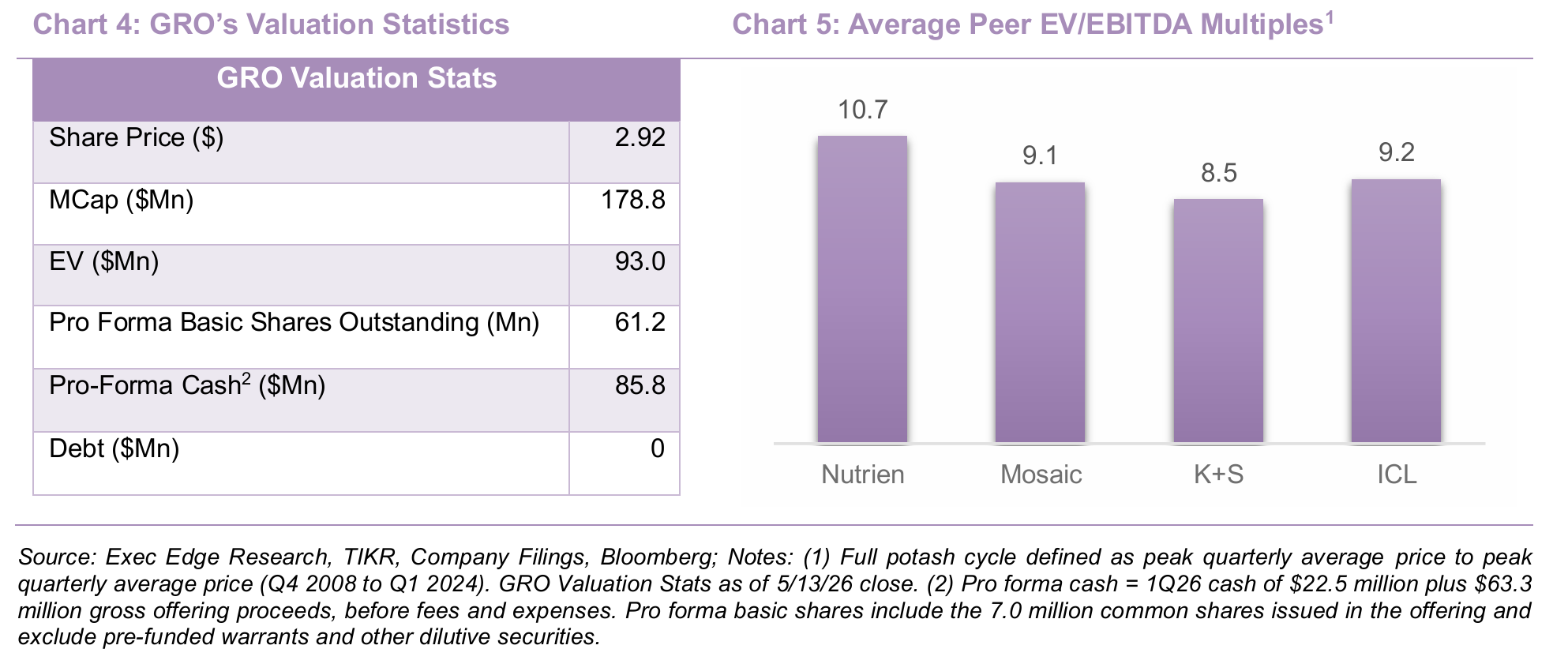

- Established global potash producers trade at EV/EBITDA multiples of 8.5x-10.7x across the cycle, with Nutrien at 10.7x, ICL at 9.2x, Mosaic at 9.1x, and K+S at 8.5x, implying a peer average of 9.4x. Applying that average multiple to Autazes’ targeted steady-state EBITDA potential of $1.0 billion would imply a notional production-stage enterprise value of $9.4 billion. This is not a near-term valuation target and should be discounted materially for construction financing, dilution, execution timing, commodity price volatility, and project ramp risk. Still, the comparison highlights the magnitude of the value gap if GRO can continue converting Autazes from a permitted development asset into a financed construction project.

- The current valuation suggests the market is assigning only a modest probability-weighted value to that long-term cash flow opportunity. As of the May 13, 2026 close, GRO had a market capitalization of ~$179 million. The company remained debt-free, held $22.5 million of cash at March 31, 2026, and subsequently completed a $63.3 million equity raise, implying pro forma cash of $85.8 million before fees and an estimated enterprise value of $93 million. That EV represents less than 0.1x the project’s illustrative $1.0 billion steady-state EBITDA potential, underscoring both the embedded optionality and the market’s continued discount for financing and execution risk.

- Valuation should evolve with de-risking milestones. Key catalysts include FEED completion, construction financing, BOOT/infrastructure funding, anchor equity participation, and initial construction activity. Support also comes from Autazes’ delivered-cost advantage, contracted offtake, Franco-Nevada’s involvement, Brazil food-security relevance, and GRO’s U.S. listing, though realization still depends on reducing financing and execution risk.

Download the Complete Report Here

Read Exec Edge’s Initiation on Brazil Potash Corp. Here

Subscribe to our Weekly Newsletter to Receive All Research

Contact: