Download the Complete Report Here

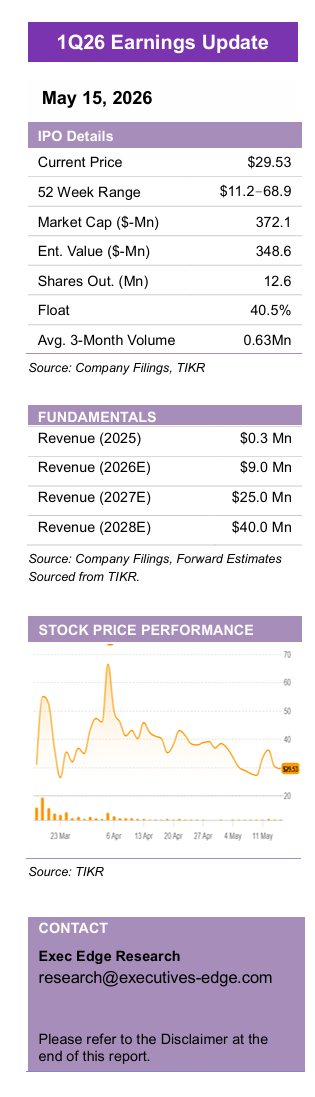

Swarmer, Inc. (SWMR)

Swarmer, Inc. (SWMR)

Combat-Validated Autonomy Platform Positioned for Accelerated Growth as License Activation Scales

- Key Takeaways:

- 1Q26 establishes the starting revenue baseline ahead of expected sequential growth.

- Meta Bureau’s $2.86 million SkyKnight award covers 16,000+ licenses, with $10.4 million of upgrade options creating software attach upside.

- Japan / Rakuten, HIMERA, and interceptor initiatives broaden SWMR’s funnel across allied markets, resilient communications, and counter-UAS applications.

- Cash increased to $23.5 million after IPO and Series A-1 proceeds, supporting engineering, product development, and integration capacity.

- Platform expansion, strategic partnerships, and autonomy adoption support a premium valuation framework.

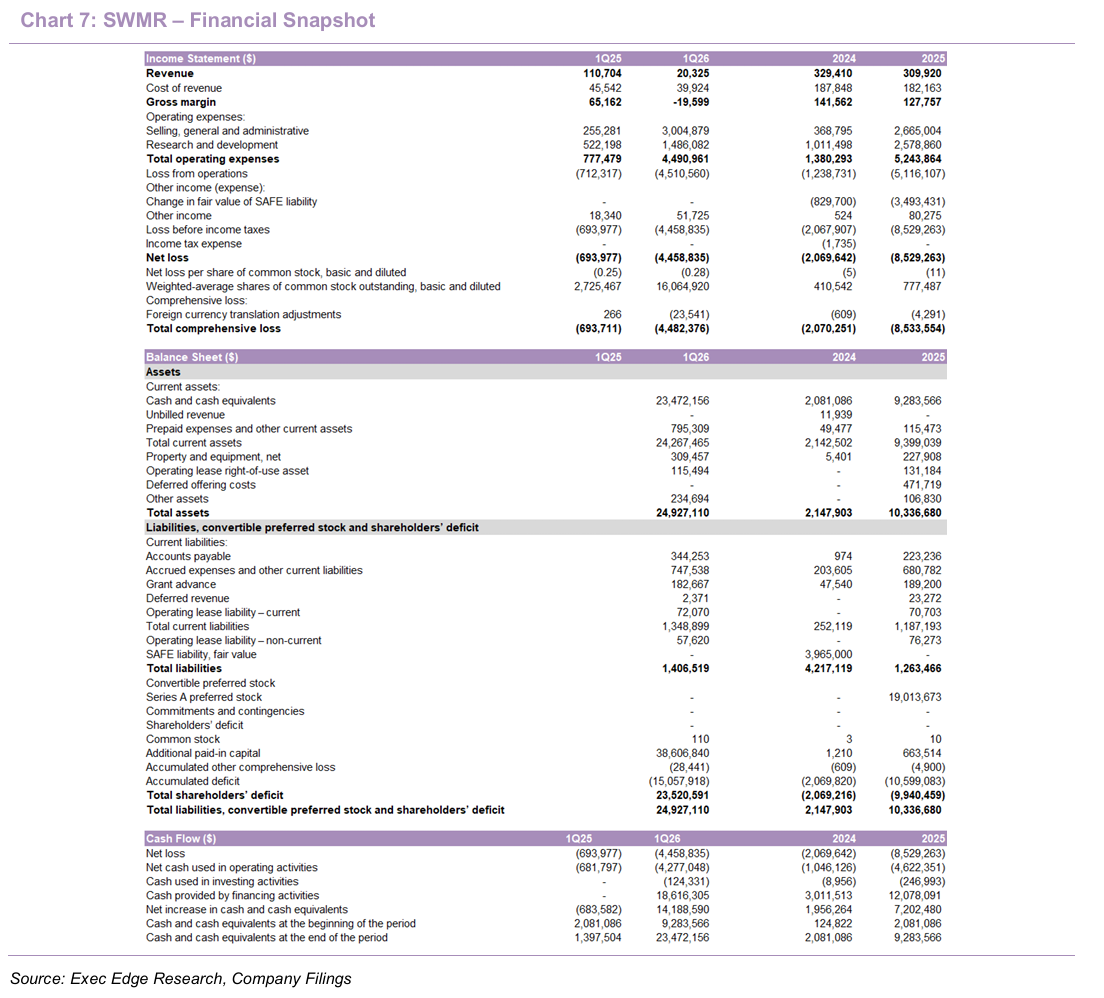

- 1Q26 establishes the starting revenue baseline ahead of expected sequential growth. SWMR’s first reported quarter as a public company showed revenue of $20,325, down 81.6% y/y from $110,704, gross profit moving to a $(19,599) loss from $65,162, and net loss widening to $(4.5) million from $(0.7) million. The revenue decline was primarily tied to the wind-down of service-related deferred revenue from the company’s historically largest Ukraine customer, from which SWMR does not expect future revenue, while the current focus has shifted toward higher-volume Ukraine and international opportunities. The quarter therefore looks more like a transition point in reported revenue than a demand signal, with the forward story tied to license activation, deployment timing, and partner production.

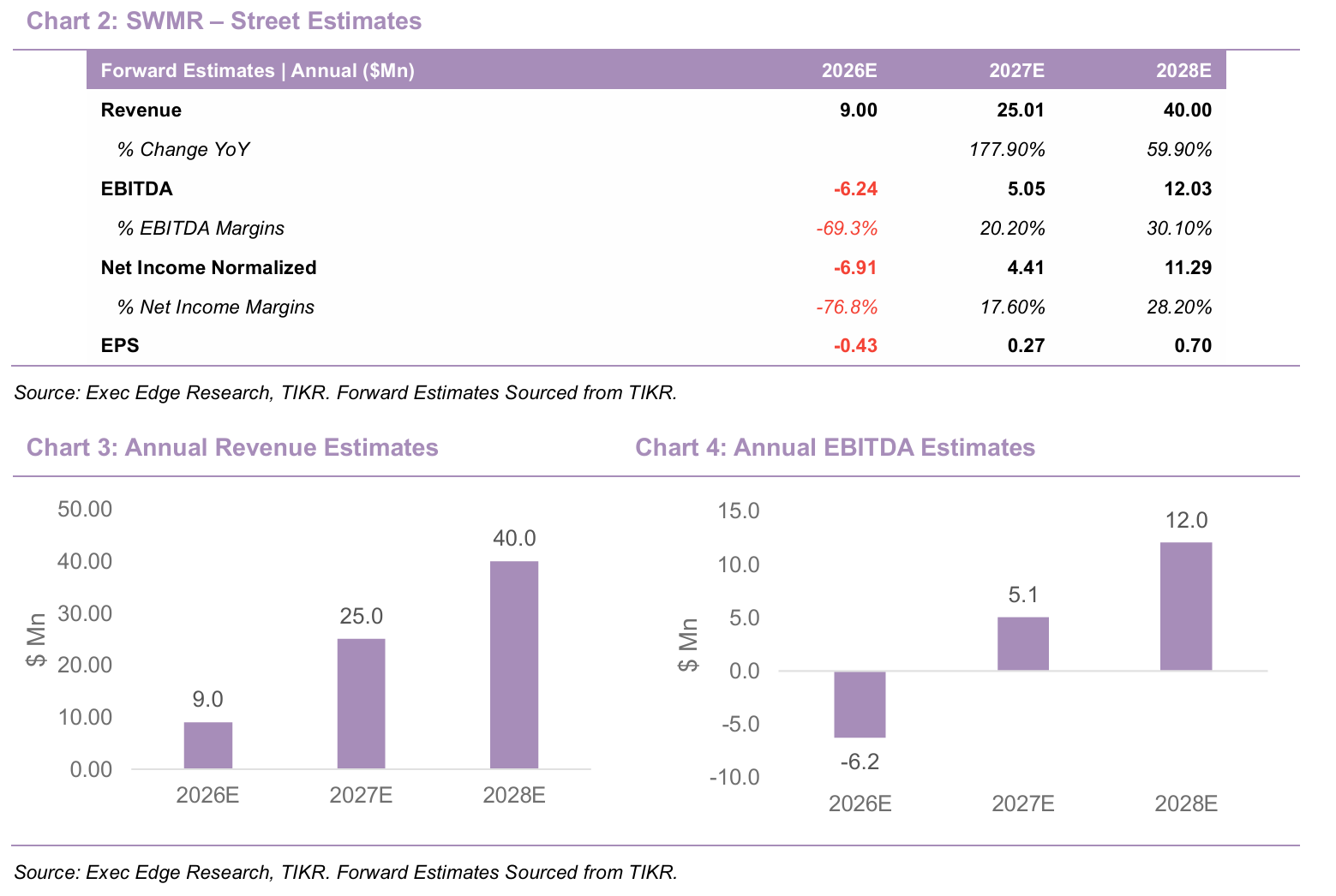

- Street estimates sourced from TIKR show that revenue is expected to increase to $1.0 million in 2Q26, $3.0 million in 3Q26, and $5.0 million in 4Q26, implying that sequential growth is expected to begin immediately as new awards and integrations start contributing to recognized revenue.

- Nasdaq listing strengthened the balance sheet and funded the next phase of product integration. During the quarter, Swarmer completed its IPO and began trading on the Nasdaq Capital Market under the ticker SWMR, raising approximately $17.3 million in gross proceeds to support continued investment in engineering, product development, and growth initiatives.

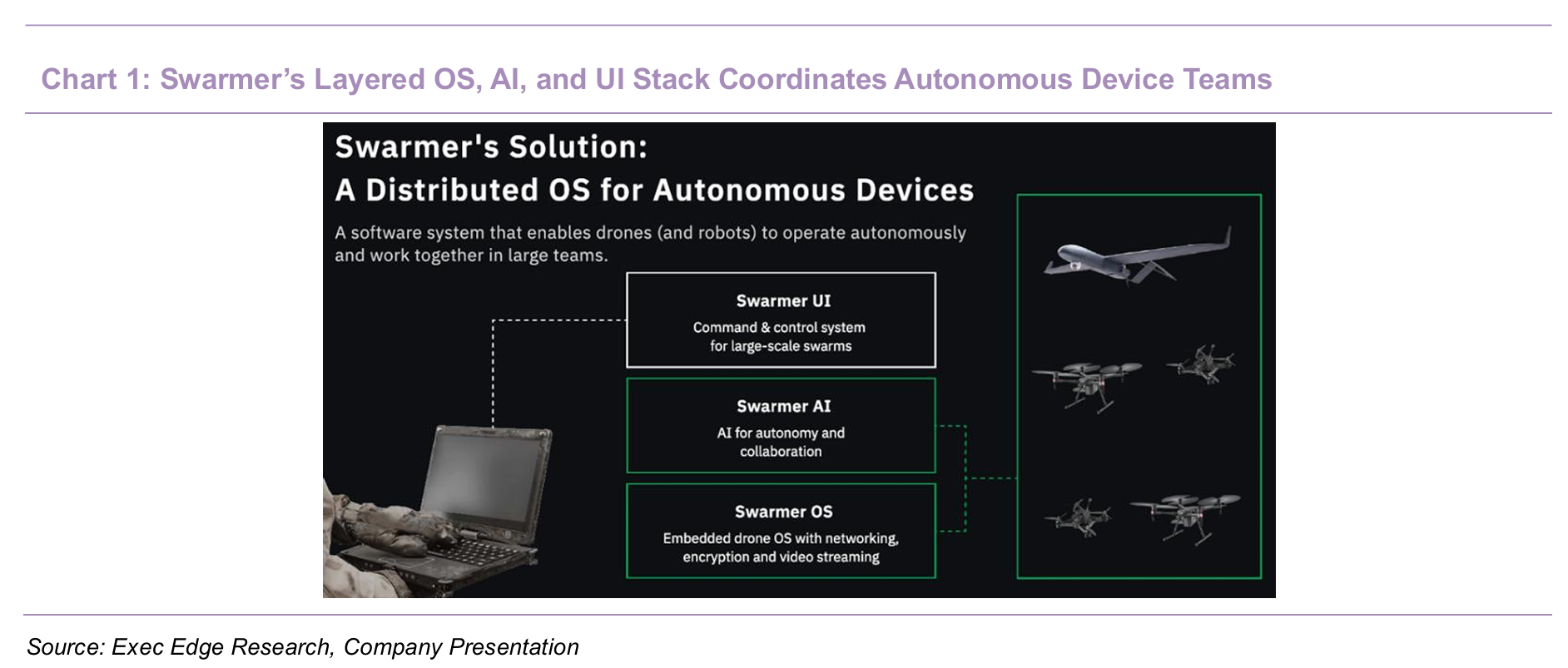

- Combat-proven intelligence layer underpins SWMR’s differentiation as drone coordination demand scales. SWMR’s platform is positioned around the core bottleneck in modern unmanned systems: coordinating, controlling, and automating large numbers of low-cost drones rather than building the hardware itself. The company’s most differentiated product input is its combat operating history, with the technology supporting more than 100,000 real-world missions in Ukraine since April 2024 across nearly 50 military units. That field exposure matters because the autonomy stack is being refined in contested environments involving jamming, operator constraints, multi-drone coordination, and rapidly changing mission requirements rather than only through lab testing or simulation.

- Meta Bureau’s ~$2.9 million contract expands deployment footprint and creates meaningful upgrade optionality. In May, Meta Bureau LLC awarded SWMR’s subsidiary, Swarmer Estonia OÜ, a contract with an initial value of $2.86 million for more than 16,000 software licenses to be deployed aboard SkyKnight quadcopter bombers and other unmanned aerial vehicles (UAVs). The agreement includes two separate license allocations for Swarmer’s full autonomy platform including Swarmer OS, AI, and UI as well as an additional allocation for Swarmer OS-only licenses, which can later be upgraded to the full autonomy stack via over-the-air software updates. If all upgrade options are exercised, the total contract value could increase by an additional $10.4 million, bringing the potential aggregate value to approximately $13.2 million. Management noted that the deployment is expected to further expand the company’s real-world operational dataset and strengthen integration with battle-proven UAV platforms operating in Ukraine.

- New initiatives broaden SWMR’s commercialization surface area beyond the initial license ramp, adding three paths to convert platform validation into larger programs: allied-market expansion, resilient communications, and counter-UAS/site-defense applications.

- Japan/Rakuten expands SWMR’s allied-market commercialization channel. SWMR’s expansion into Japan with support from Rakuten gives the company a local route into one of the world’s more advanced robotics and unmanned systems markets. The initiative broadens SWMR’s funnel beyond Ukraine-linked demand and supports potential applications across defense, emergency response, infrastructure, research, and industrial use cases. The successful demonstration of an autonomous “seek and hit” operation using eight-inch attritable drones also reinforces the company’s focus on low-cost, scalable unmanned systems. The key milestone is whether Rakuten-supported market entry converts into local integrators, signed programs, or paid deployments.

- HIMERA partnership strengthens SWMR’s autonomy stack with resilient battlefield communications. SWMR’s memorandum of understanding with HIMERA adds jam-resistant, frequency-hopping communications technology to the company’s next-generation autonomy stack. That matters because scaled autonomous operations depend on reliable connectivity in contested and degraded environments, particularly when coordinating multiple vehicles across aerial, ground, and maritime domains. The partnership could lower integration complexity for vendors by combining resilient communications with SWMR’s autonomy and coordination layer in a more deployable solution. Joint engagement with system vendors and integrators should be the next proof point for whether the partnership can move from technical integration to commercial adoption.

- Interceptor collaboration expands SWMR into counter-UAS and site-defense applications. SWMR announced MOUs with X-Drone, Norda Dynamics, and Kara Dag Technologies to develop an end-to-end drone interceptor system for Group 1-3 UAVs and unmanned surface vessels up to eight meters. The planned solution would integrate detection, targeting, terminal guidance, and autonomous coordination into SWMR’s platform, creating a lower-cost alternative to traditional missile-based defense for critical infrastructure and maritime threats. The partner base adds credibility, with X-Drone having delivered more than 70,000 unmanned systems, Norda software deployed on more than 60,000 attritable drones, and Kara Dag contributing distributed RF / acoustic detection capabilities. Strategically, the initiative extends SWMR from enabling drone operations into autonomous interception, broadening the platform’s use cases while keeping the company anchored in software-led coordination rather than hardware manufacturing. Management indicated initial deployment timelines could range from two-to-four months, making interceptor integration a tangible 2H26 milestone if testing and partner integration progress as planned.

- We note that publicly announced partnerships likely represent only a portion of the company’s broader commercial pipeline. SWMR acknowledged that several customers and programs remain undisclosed due to the sensitive nature of defense-related engagements and customer confidentiality considerations. Importantly, management noted that currently announced partnerships and reported revenue are generally trailing indicators, with most publicly disclosed projects typically reflecting business development and integration work completed approximately three to nine months earlier. As a result the underlying pipeline may be materially deeper than what is currently visible publicly, with additional updates expected as programs progress and disclosure becomes possible.

- Appointment of Mykhailo Nestor strengthens product leadership as SWMR scales its autonomy platform. SWMR appointed Nestor as Chief Product Officer to lead product strategy and development across swarm coordination, multi-domain integration, AI-powered collaborative autonomy, and distributed command-and-control systems. Nestor spent seven years as Chief Product Officer and board member at Kyivstar, part of VEON, where he helped build large-scale digital platforms used by millions of customers. His experience scaling complex software infrastructure should support SWMR’s transition from field-tested autonomy software to repeatable, partner-integrated products across allied defense and autonomous systems markets.

- SWMR’s hardware-agnostic intelligence layer addresses the core coordination problem in modern unmanned operations. SWMR is focused on solving three challenges facing autonomous systems: coordinating large numbers of unmanned platforms across multiple domains, enabling real-time decision making in contested environments, and maintaining effectiveness when communications are degraded or denied. The company operates at the software layer rather than manufacturing drones, positioning SWMR to support interoperability across aerial, ground, and maritime systems. That hardware-agnostic approach is important as defense customers increasingly prioritize scalable autonomy, resilient command-and-control, and coordination across heterogeneous unmanned fleets.

- Combat mission history shows increasing autonomy and mission complexity over time. SWMR’s combat deployments began in April 2024 with relatively simple multi-drone reconnaissance and mining operations involving approximately three drones, then expanded toward formations of roughly eight-to-10 larger unmanned systems. Early missions were semi-autonomous, with operators maintaining partial control during flight toward target areas, while more recent missions have moved toward higher levels of autonomy. Reconnaissance drones can autonomously identify and transmit battlefield data, while attack drones coordinate target engagement decisions internally based on probability-of-hit calculations rather than direct operator assignment. This progression shows that SWMR’s 100,000+ combat missions are not just validation points, but inputs into more sophisticated mission templates and broader hardware integrations.

- Per-unit licensing gives SWMR a flexible pricing framework as unmanned system volumes scale. SWMR currently prices its autonomy software primarily on a per-unit licensing basis, with pricing determined case-by-case based on integration complexity, hardware class, and expected production scale. Higher-volume platforms may carry lower per-unit pricing given broader deployment potential, while lower-volume systems such as larger fixed-wing platforms may command higher pricing because upfront integration work is spread across fewer units. The company also noted that percentage-of-system-value pricing could become relevant over time, but the market remains early and commercialization is currently focused on flexible structures that scale with customer deployment volumes.

- Margins and opex should be viewed through early-stage scale, not 1Q26 profitability. 1Q26 gross margin was (96.4)% because revenue was only $20,325 and gross profit was a $(19,599) loss, versus 58.9% gross margin on $110,704 of revenue in 1Q25. Operating expenses also stepped up to $4.5 million from $0.8 million, reflecting public-company costs, consulting and professional services, and higher engineering and product development investment. Future spending is expected to remain primarily opex-focused, including additional engineering hires and integration capacity across a broader range of hardware platforms. SWMR also suggested that long-term gross margins could exceed 70% as the business scales, reflecting the high-margin potential of a software-centric licensing model despite service and implementation obligations. As revenue begins to scale, the key test is whether new license activations and repeat integrations start to absorb the higher public-company and engineering cost base.

- Balance sheet supports engineering and integration priorities, with working capital tied to program conversion. SWMR ended 1Q26 with $23.5 million of cash and equivalents, up 152.7% from $9.3 million at year-end 2025, reflecting $17.3 million of IPO gross proceeds and $3.5 million of Series A-1 convertible preferred proceeds. Capital deployment is focused on hiring engineers, expanding integration capacity, and supporting product development rather than balance-sheet-heavy capex. As license awards and partner programs scale, the more relevant working-capital items will be deferred revenue, milestone billings, receivables, and customer advances tied to activation and service obligations.

- Street estimates frame a sharp 2Q26-2028E revenue ramp and 2027E EBITDA inflection as license activation scales. Street estimates sourced from TIKR forecast revenue of $1.0 million in 2Q26, $3.0 million in 3Q26, and $5.0 million in 4Q26, producing $9.0 million of 2026E revenue before rising to $25.0 million in 2027E and $40.0 million in 2028E. That implies growth of 178% in 2027E and 60% in 2028E, with EBITDA margin improving from (69.3)% in 2026E to 20.2% in 2027E and 30.1% in 2028E. The estimate path is consistent with a software license model moving from activation to scale, but it requires visible conversion from contract value, partner integrations, and development-stage programs into recognized revenue. We view 2Q26 as the first key checkpoint, with the $1 million estimate providing an early read on whether license activation is beginning to convert into the expected revenue ramp.

Platform Expansion, Strategic Partnerships, and Autonomy Adoption Support Premium Valuation

- The following valuation analysis is presented for illustrative purposes only and does not constitute a recommendation, investment advice, solicitation, or a price target. The analysis is based on publicly available information and company disclosures and reflects a valuation framework rather than a definitive assessment of fair value. Any implied upside or downside referenced herein is not intended as a prediction of future share price performance.

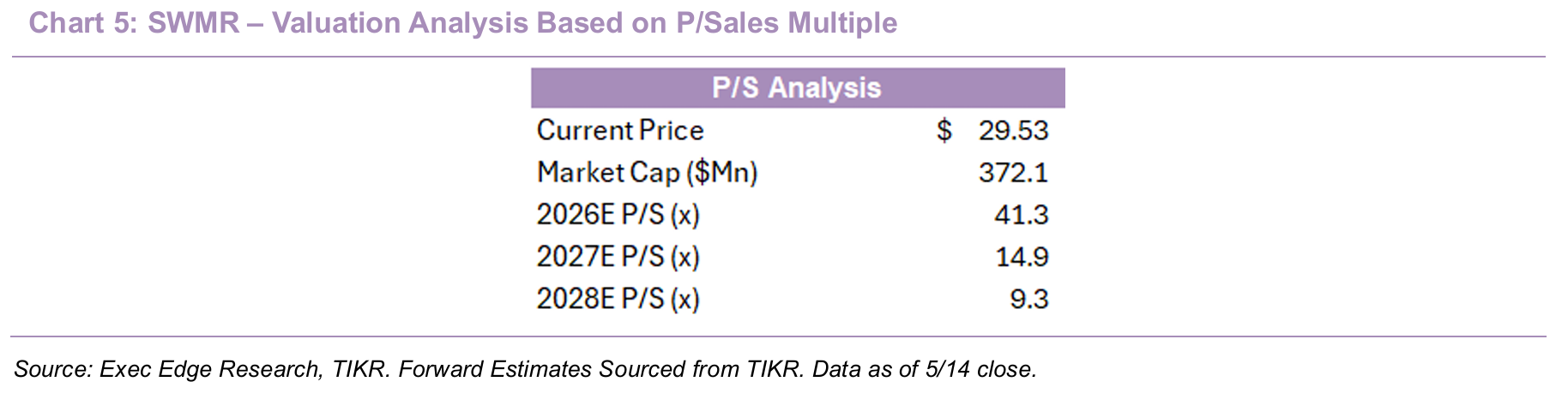

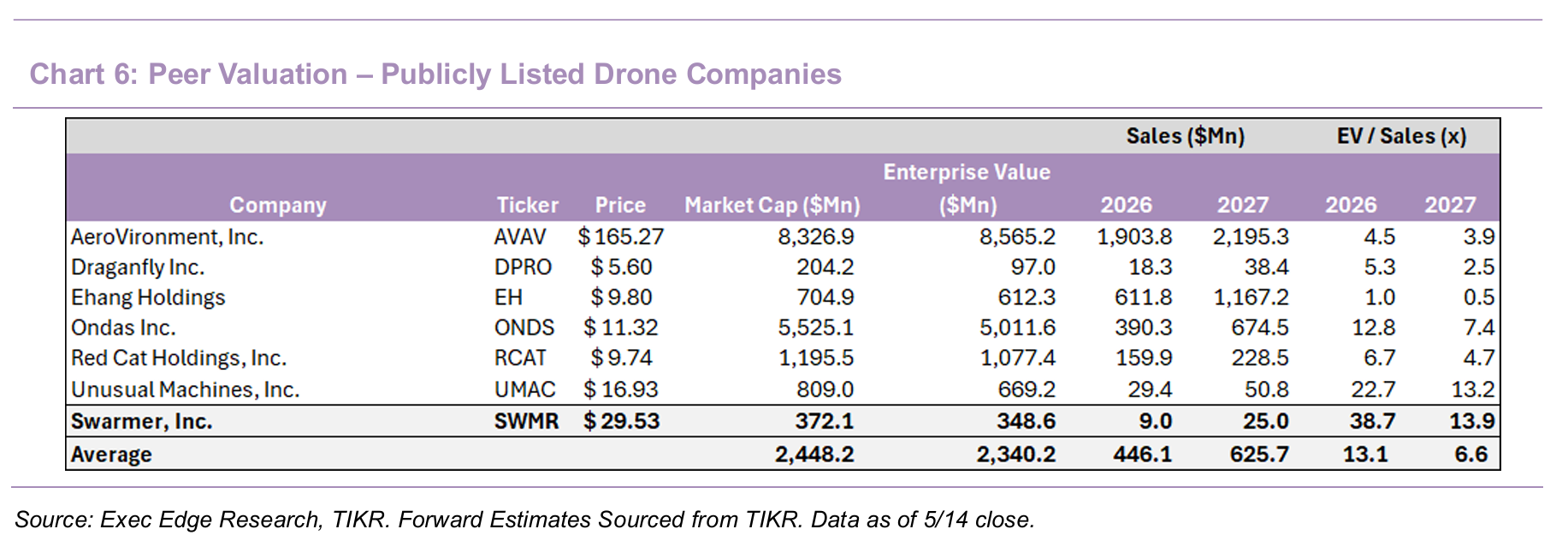

- Valuation screens elevated on near-term revenue, but the multiple compresses quickly if SWMR executes against the expected software-license ramp. SWMR currently trades at approximately 41.3x 2026E sales based on Street estimates sourced from TIKR for 2026 revenue of $9.0 million, which is demanding on near-term financial metrics and reflects the company’s early-stage commercialization profile. However, we believe the market is valuing SWMR less like a traditional defense contractor or hardware-centric drone company and more like a scarce autonomy software platform, supported by combat-validated technology, hardware-agnostic positioning, and exposure to growing unmanned systems and counter-UAS demand. The valuation moderates meaningfully as revenue scales, with the P/S multiple declining to 14.9x 2027E sales on projected revenue of $25.0 million and 9.3x 2028E sales assuming revenue reaches $40.0 million. In our view, the key to sustaining a premium multiple versus defense hardware peers will be evidence that license deployments, platform integrations, OS-to-full-stack upgrade opportunities, and international partnerships can convert into recurring software revenue and improving EBITDA visibility.

- Software-led autonomy positioning: SWMR’s hardware-agnostic autonomy platform supports a premium to hardware-centric defense and drone peers if it becomes an embedded software layer across OEMs, unmanned platforms, and mission types.

- Asset-light model: Unlike traditional defense manufacturers, SWMR does not manufacture drones or heavy hardware, allowing capital to be directed toward software development, integration capacity, and engineering talent rather than balance-sheet-heavy production infrastructure.

- Revenue scaling potential: Current revenue reflects early-stage deployments, but Street estimates sourced from TIKR call for revenue to rise from $9.0 million in 2026E to $25.0 million in 2027E and $40.0 million in 2028E as license activation scales.

- Profitability glidepath: Management highlighted the operating leverage embedded in SWMR’s model, while Street estimates sourced from TIKR show that EBITDA and EPS are likely to turn positive in 2027E as software license revenue scales.

- Defense autonomy tailwinds: Rising defense spending, accelerating unmanned systems adoption, counter-UAS demand, and battlefield lessons from Ukraine create a supportive backdrop for AI-enabled drone coordination and autonomy platforms.

- Private-market autonomy valuations support a premium framework for scaled AI-defense platforms. Shield AI, a private-market comparable within the defense autonomy ecosystem, announced a $1.5 billion Series G raise at a $12.7 billion post-money valuation in March 2026, alongside $500 million of fixed-return preferred equity financing. Media reports and private-company estimates indicate Shield AI generated approximately $300 million of revenue for the year ended March 2025 and is projected to exceed $540 million in 2026, implying roughly 42x trailing sales and 24x forward sales. The comparison is relevant despite Shield AI’s larger scale and broader platform mix because both companies are positioned around AI-enabled autonomy, collaborative unmanned operations, and software-centric defense applications. In that context, SWMR’s current 41.3x 2026E sales multiple appears more defensible if the company converts its combat-validated software stack, hardware-agnostic architecture, strategic partnerships, and license deployments into the expected revenue ramp.

Download the Complete Report Here

Read Exec Edge’s Initiation on Swarmer Inc. Here

Subscribe to our Weekly Newsletter to Receive All Research

Contact: