Download the Complete Report Here

GrabAGun Digital Holdings Inc. (PEW)

GrabAGun Digital Holdings Inc. (PEW)

Revenue Beat and Market Share Gains Reinforce Digital Platform Thesis; PEW Logistics Adds Higher-Margin Optionality. Attractively Valued.

- Key Takeaways

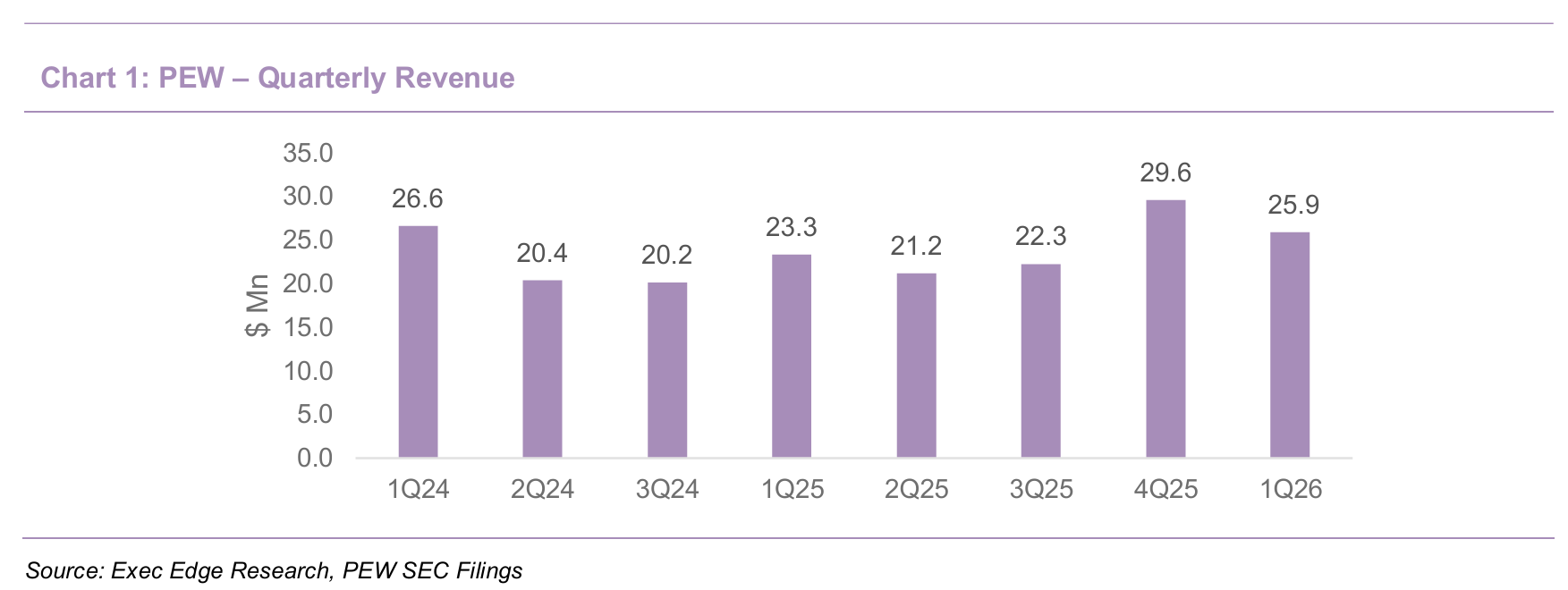

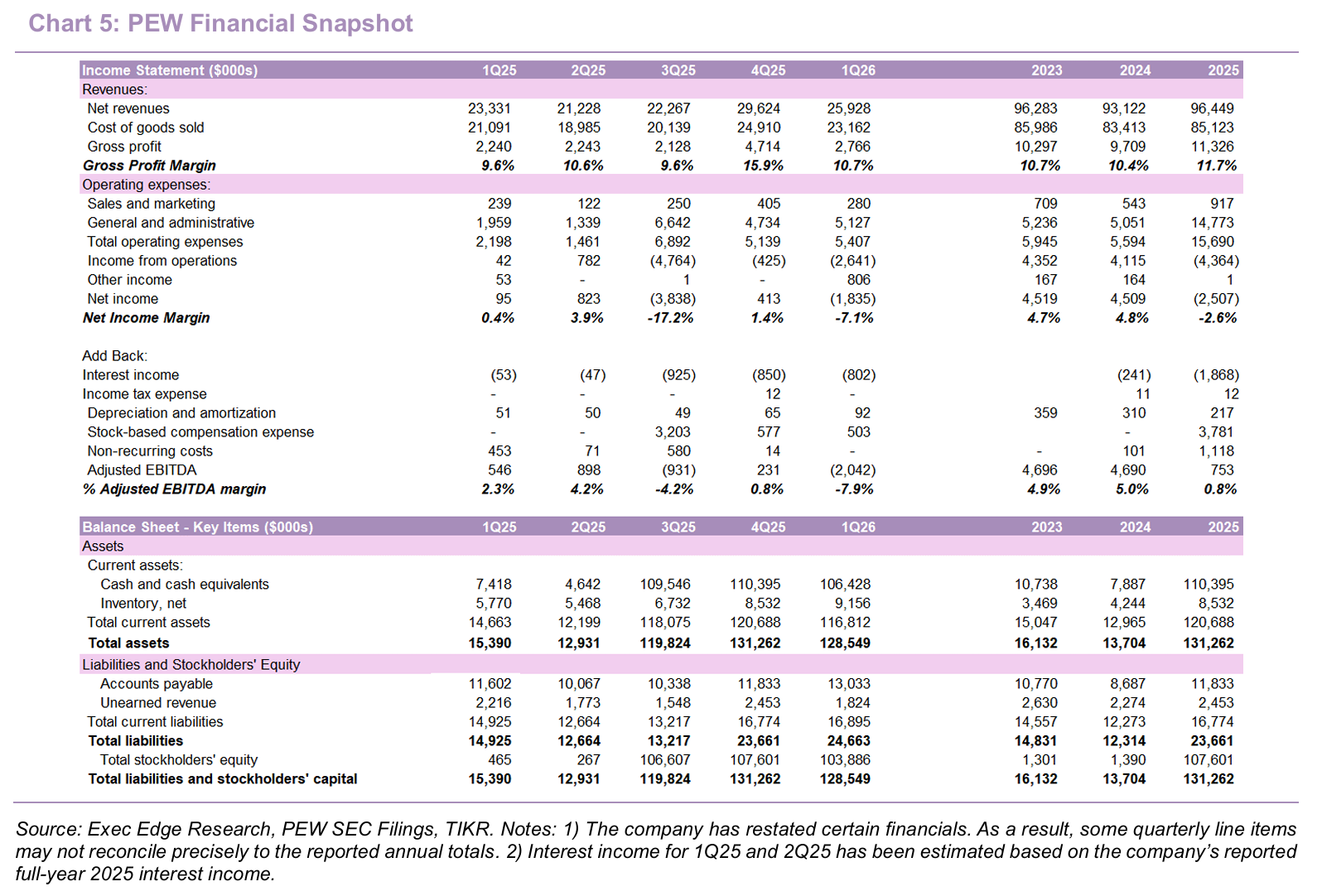

- PEW delivered $25.9 million of 1Q26 revenue, up 11.1% y/y and ahead of Street estimates of $24.5 million.

- Continues outperforming the broader firearms market, with firearm sales growth materially ahead of Adjusted NICS trends as digital execution and AI-driven pricing supported ongoing market share gains.

- Expanded PEW Logistics during 1Q26 with the addition of Derya Arms, further validating early manufacturer adoption.

- Shoot & Subscribe now contributes 15% of ammo revenue, adding an early recurring revenue layer to PEW’s platform.

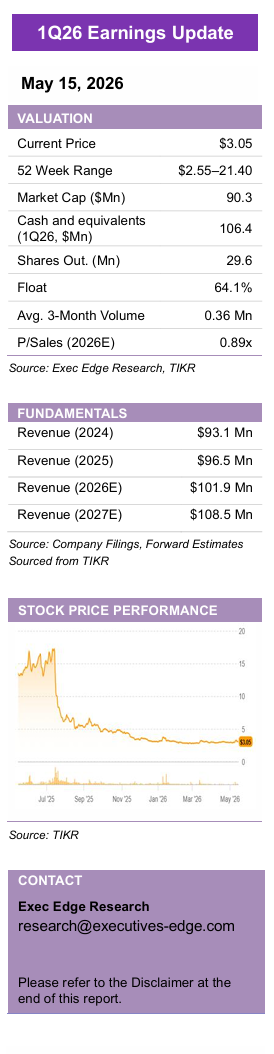

- Valuation remains compelling, with ~$90 million market cap below $106.4 million cash and a negative enterprise value.

- 1Q26 revenue beat reinforces PEW’s share-gain story as platform execution outpaced broader industry demand. PEW reported 1Q26 revenue of $25.9 million, up 11.1% y/y from $23.3 million, and ahead of Street estimate of $24.5 million by $1.4 million, or 5.8%. This was another quarter of meaningful outperformance, as firearms sales increased 10.5% y/y while adjusted NICS background checks increased only 1.6% over the same period. Management noted that demand remained stable month by month during the quarter and did not show major spikes from geopolitical events, suggesting that topline growth was primarily driven by execution rather than one-time demand pull-forward.

- Firearms remain the primary growth driver, while non-firearms returned to growth despite broader ammunition softness. Firearms product sales increased 10.5% y/y to $21.7 million, supported by market share gains, favorable product mix, and pricing optimization. Non-firearms product sales increased 10.4% y/y to $4.1 million despite continued softness in ammunition demand across the broader 2A industry. Service sales contributed $0.1 million as PEW Logistics began generating revenue during the quarter. The return to growth in non-firearms is notable because it broadens the revenue base beyond firearms and suggests that accessories, ammunition, and service-related categories can contribute to growth even in a softer category environment.

- Customer KPIs continue to validate PEW’s platform model and mobile-first strategy. Customer lifetime value increased 4.2% y/y to $906, while total site traffic increased 12.6% y/y. Mobile remained the dominant channel, accounting for approximately 67% of site traffic, 70% of transactions, and 64% of net revenue in 1Q26. Mobile’s transaction share exceeding its traffic share reinforces management’s commentary that mobile drives higher conversion rates and a structurally lower cost per transaction than traditional retail.

- KelTec and Derya validate early PEW Logistics adoption, strengthening the higher-margin platform opportunity. PEW Logistics is a white-label direct-to-consumer fulfillment solution for firearms manufacturers, enabling branded storefronts, ATF-compliant FFL workflows, end-to-end fulfillment, and first-party customer data without manufacturers needing to build compliance, IT, customer service, or logistics infrastructure. PEW launched the platform in January with KelTec Weapons, a 35-year American firearms manufacturer with a loyal customer base that validated the platform’s value proposition from day one and added Derya Arms in March as its second manufacturer partner. Derya is a global manufacturer with more than 200,000 firearms produced and products used across 50+ countries, further validating the platform’s appeal across both domestic and international manufacturer profiles. Since launch, PEW Logistics has processed $1.3 million of GMV, while leveraging PEW’s FFL network that places a licensed dealer within 15 miles of 97% of the U.S. population and supports average checkout-to-delivery time of just under three business days.

- PEW Logistics expected to operate at materially higher margin profile than the core e-commerce business. PEW Logistics carries a significantly higher gross margin profile relative to the company’s traditional hard goods e-commerce business, reflecting the platform’s revenue-share structure and incremental pick-pack-ship service fees. Management noted that gross margins for PEW Logistics can reach upwards of 70%, supported by the platform’s more asset-light and service-oriented operating model.

- Management expects manufacturer onboarding to accelerate as existing PEW Logistics partners demonstrate revenue traction. Additional manufacturer adoption could accelerate as existing partners begin generating visible revenue and operating metrics, while also emphasizing the platform’s ability to help manufacturers improve gross margins and regain access to valuable first-party customer relationships and purchasing data.

- Shoot & Subscribe reaches 15% of ammo revenue, adding early proof of recurring purchase behavior. The ammunition subscription service, launched in 4Q25, now contributes 15% of PEW’s ammo revenue line. This is an important early proof point because ammunition is naturally repeat-purchase oriented, and converting frequent shooters from one-time transactions into contracted recurring relationships should improve retention, purchase frequency, and customer lifetime value. The subscription architecture can also extend across additional product categories over time, creating a broader recurring revenue opportunity. Early traction gives the initiative more tangible commercial relevance and supports the thesis that PEW can layer predictable revenue streams onto its existing digital commerce platform.

- Marketing scale and customer acquisition are becoming more visible contributors to outperformance. Growth was supported by improved product selection, right-item at right-price purchasing, reduced platform friction, and expanded marketing capabilities across social media and other channels. The company continues to drive traffic and consumer demand through a broader customer acquisition funnel, while supplier relationships and product partnerships support availability of in-demand inventory. The first-quarter traffic growth of 12.6%, revenue growth of 11.1%, and LTV growth of 4.2% indicate that acquisition efforts are translating into monetizable platform engagement rather than low-quality traffic. Repeat purchase momentum remains strong, with repeat rate holding steady, supporting revenue durability as PEW scales both D2C commerce and platform-based services.

- Infrastructure investment is being made ahead of anticipated platform scaling. PEW remains on track to bring its new headquarters and fulfillment facility online by 4Q26, after acquiring the facility in 4Q25. The new facility is approximately 2.5x the company’s current operational footprint and is intended to support growth in both PEW’s core D2C business and PEW Logistics well beyond 2026.

- Potential ATF rule changes could create a meaningful long-term distribution catalyst. Proposed ATF amendments could allow certain firearm transfers to occur remotely with secure identity verification and direct-to-home delivery under an approved framework. If finalized, such a regime would require secure remote identity verification, NICS integration, advanced compliance systems, secure record keeping, and operational execution at scale. PEW’s 15 years of investment in digital infrastructure, compliance workflows, FFL integration, and regulated online firearm transactions position the company well if the industry shifts toward remote compliance and direct-to-home delivery. Timing and final rule structure remain uncertain, but regulatory complexity could increase the strategic value of PEW’s infrastructure.

- Higher public company costs and growth investments drove quarterly net loss. PEW reported a net loss of $1.8 million in 1Q26 compared to net income of $0.1 million in the prior-year period. The loss was due to increase in SG&A expense which was primarily driven by approximately $1.5 million of incremental headcount supporting growth initiatives, roughly $0.5 million of stock-based compensation, and nearly $0.8 million of insurance and professional fees associated with operating as a public company.

- Gross margin expanded on favorable product mix and pricing optimization. Gross profit increased to $2.8 million in 1Q26, representing a gross margin of 10.7%, compared to $2.2 million or 9.6% of net sales in the prior-year period. The 107 bps y/y gross margin improvement was primarily driven by a more favorable mix toward higher-margin firearm categories as well as continued benefits from the company’s pricing optimization initiatives. PEW continues to focus on sustainable margin improvement while maintaining competitive pricing.

- Adjusted EBITDA impacted by elevated growth and public company expenses. Adjusted EBITDA for 1Q26 was a loss of $2.0 million compared to positive adjusted EBITDA of approximately $0.5 million in the prior-year period, primarily reflecting higher operating expenses related to growth investments and public company costs. The decline was partially offset by stronger gross profit generation driven by revenue growth and gross margin expansion during the quarter.

- Operating expenses increased following public listing and growth investments. Total operating expenses increased to $5.4 million in 1Q26 from $2.2 million in the prior-year period, primarily reflecting planned investments associated with operating as a public company, the launch and scaling of PEW Logistics, and incremental hiring to support ongoing growth initiatives.

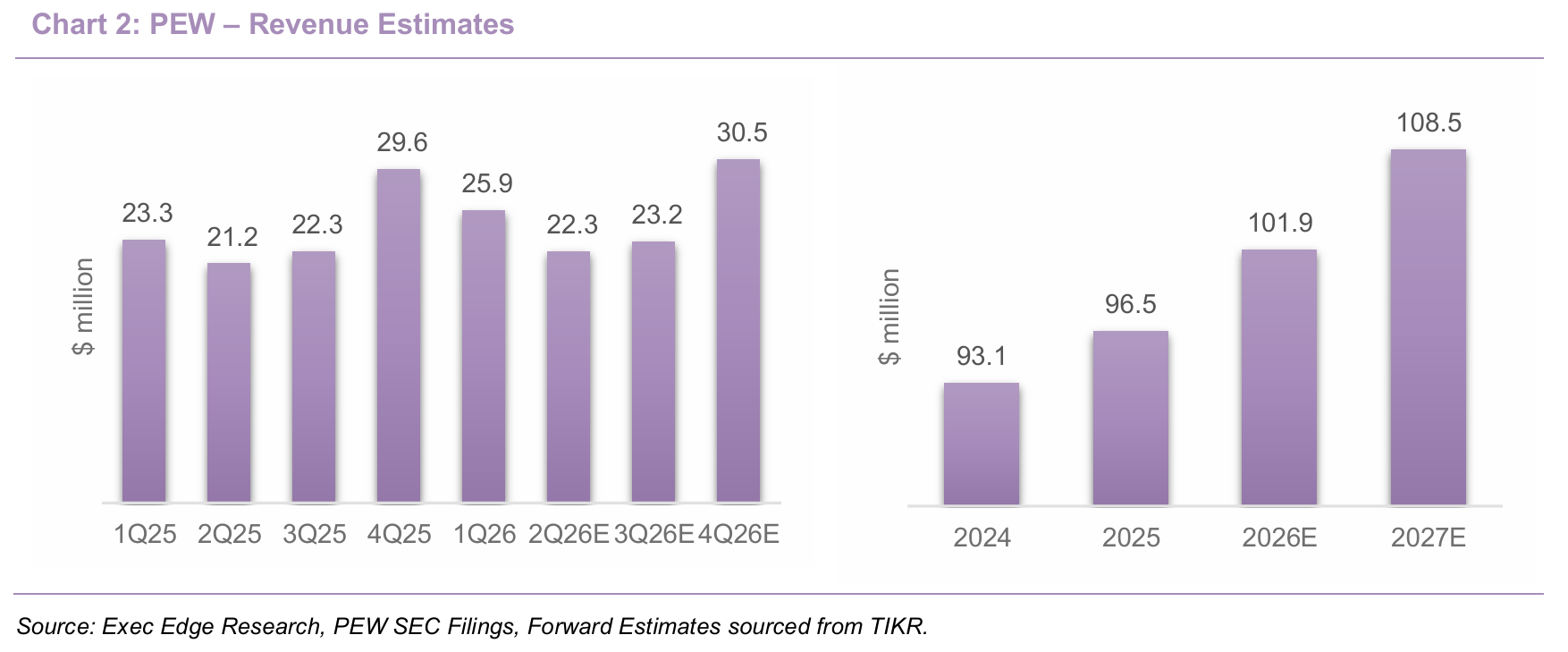

- 1Q26 revenue beat supports the path toward more than $100 million in 2026 revenue. According to Street estimates sourced from TIKR, PEW is likely to generate a topline of $22.3 million in 2Q26. Annual estimates suggest that growth is set to continue as revenue is likely to exceed $100 million in 2026 and reach $108.5 million in 2027.

- Favorable working capital dynamics and supplier-funded growth support balance sheet flexibility. PEW ended 1Q26 with $106.4 million of cash and minimal debt, compared with $110.4 million of cash at year-end 2025. Inventory increased to $9.2 million from $8.5 million sequentially, while accounts payable increased to $13.0 million from $11.8 million. The company collects from customers before paying suppliers, effectively allowing suppliers to co-fund growth. The $4.0 million sequential decline in cash reflected $1.7 million of net cash used in operating activities, $1.3 million of investing cash outflow, and $1.1 million of financing cash outflow, including share repurchases. This working capital structure supports inventory availability, D2C growth, and PEW Logistics scaling while preserving liquidity. It also allows PEW to fund platform investments and buybacks while maintaining cash above its current market capitalization.

- PEW continued opportunistic share repurchases during 1Q26 while preserving growth capital. During 1Q26, PEW repurchased approximately $2.4 million of common stock under its previously authorized $20.0 million share repurchase program, with roughly $8.7 million remaining available for future repurchases. Management noted that the company will continue to evaluate opportunistic buybacks while maintaining a disciplined capital allocation framework and preserving balance sheet flexibility to support long-term growth initiatives.

- Disciplined M&A remains a priority alongside organic platform investment. PEW’s capital allocation framework remains centered on disciplined, accretive M&A opportunities that enhance platform capabilities and meet internal return thresholds, while avoiding acquisitions pursued solely for headline growth. Although the company continues investing organically in its new fulfillment facility and expanded inventory capacity to support both D2C and PEW Logistics growth, management emphasized patience and flexibility, with M&A focused on the right assets at the right price rather than arbitrary growth targets.

Attractive Valuation Supported by Cash-Backed Asymmetry and Peer Discount

- Our analysis suggests that PEW stock remains attractively valued. The following analysis is presented for illustrative purposes only and does not constitute a stock recommendation, price target, or buy/sell/hold rating. We apply multiple valuation approaches, including market cap versus cash and enterprise value, comparison with the SPAC deal valuation, and peer valuation.

- PEW’s current market cap remains below its cash balance, implying little value for the core business. At the 5/14 close, PEW’s market cap was approximately $90 million, compared with $106.4 million of cash and equivalents, or $3.62 per share, and roughly $7.8 million of long-term debt. This implies a negative enterprise value of approximately $8 million, suggesting that the market is assigning little value to PEW’s digital platform, continued share gains, PEW Logistics, and other growth initiatives.

- PEW also trades at a substantial discount to its SPAC deal valuation. PEW was valued at $312.5 million of equity value in its SPAC deal with Colombier Acquisition Corp. II, which closed in July 2025. Against the current market cap of approximately $90 million, the stock trades at roughly a 71% discount to the SPAC deal valuation, despite 11.1% y/y revenue growth in 1Q26, market share gains versus Adjusted NICS, and early PEW Logistics traction.

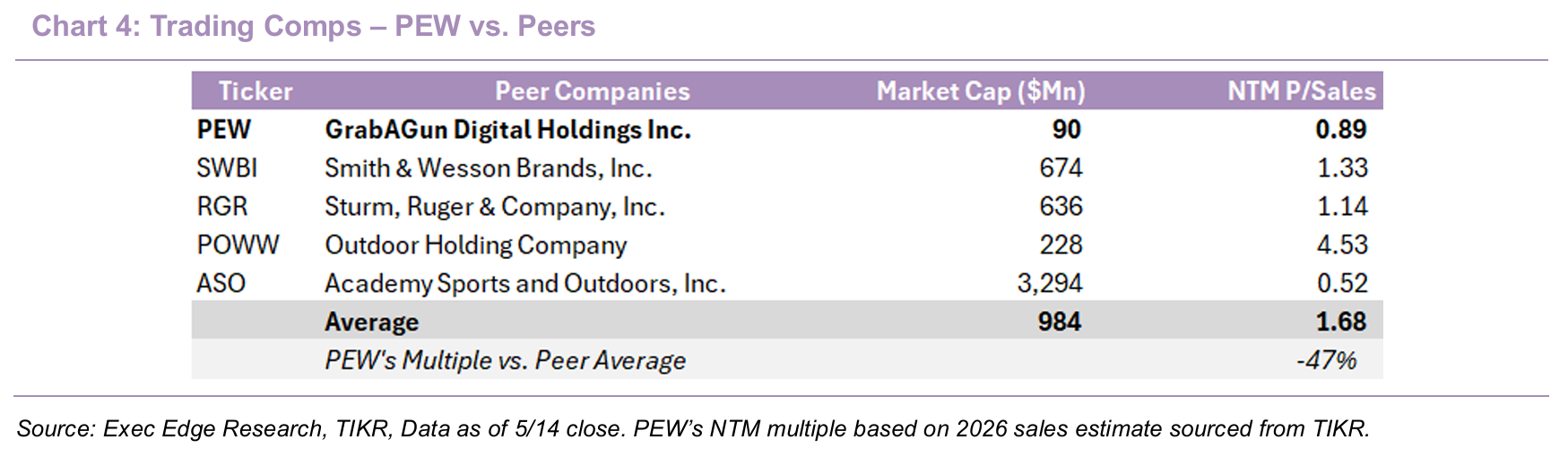

- Peer valuation also supports the discount argument. PEW trades at 0.89x 2026E P/Sales, below the peer group average, despite a cash-rich balance sheet, more than $100 million of expected 2026 revenue, and a developing higher-margin platform revenue stream through PEW Logistics. We believe the discount can narrow as PEW continues to gain share, scales PEW Logistics beyond KelTec and Derya, improves service revenue mix, and uses its balance sheet for buybacks and disciplined M&A.

- Rerating potential is tied to execution across both the core D2C platform and higher-margin growth initiatives. Key drivers include sustained revenue outgrowth versus Adjusted NICS, continued non-firearms growth, stable or improving gross margin, narrowing adjusted EBITDA losses as public company costs normalize, and further PEW Logistics traction beyond KelTec and Derya. Additional upside could come from Shoot & Subscribe scaling beyond 15% of ammo revenue, opportunistic buybacks while market cap remains below cash, disciplined M&A, and potential ATF rule changes that increase the value of PEW’s compliance-native digital infrastructure.

Download the Complete Report Here

Read Exec Edge’s Initiation on PEW Here

Subscribe to our Weekly Newsletter to Receive All Research

Contact: