Download the Complete Report Here

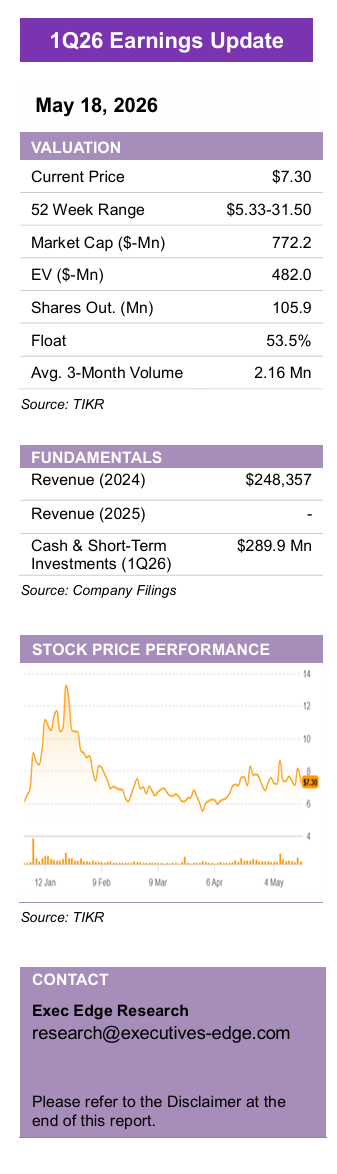

Terrestrial Energy Inc. (IMSR)

NRC Progress, Riot Data-Center Channel, and DOE Programs Strengthen Commercialization Path; Valuation Offers Milestone-Driven Re-Rating Potential

- Key Takeaways:

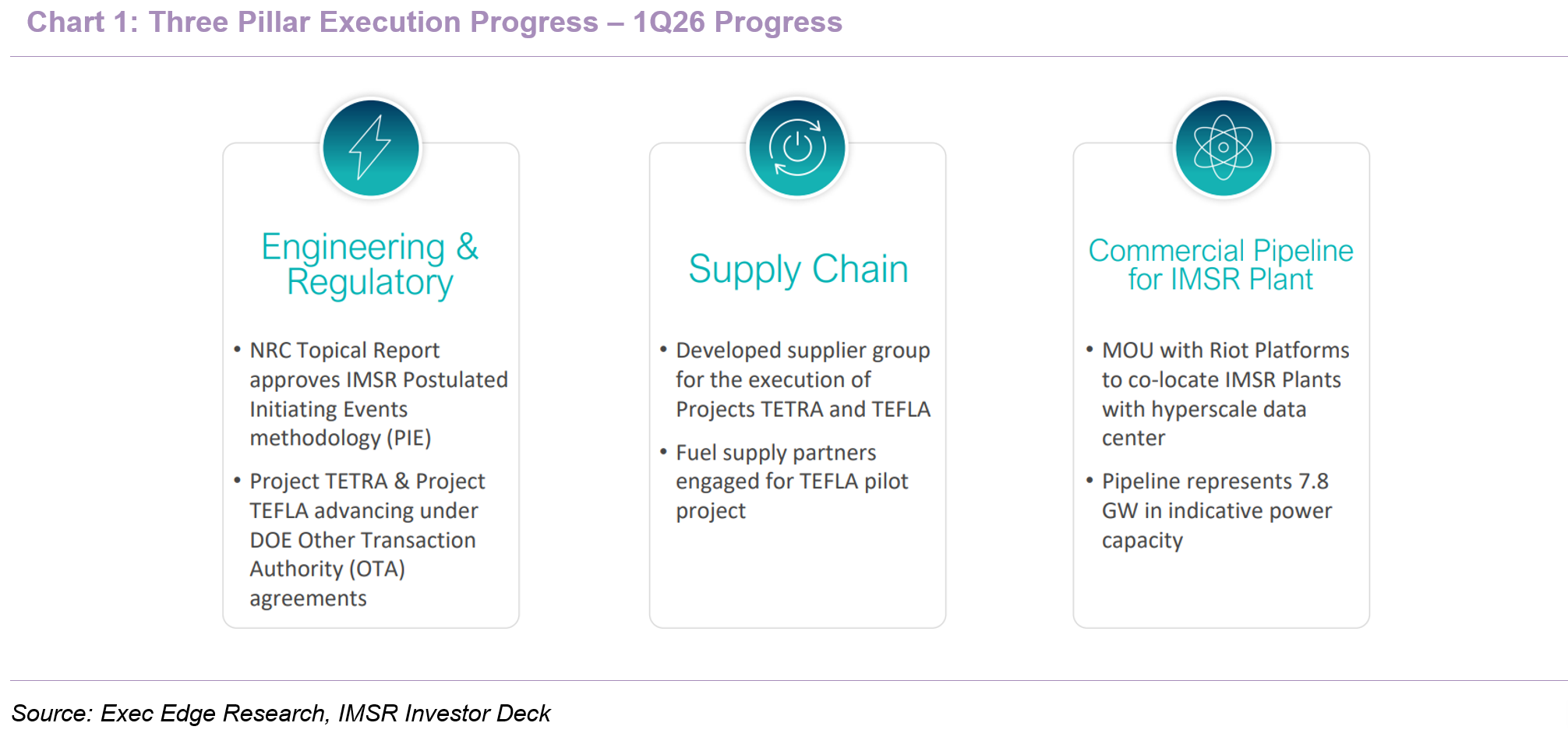

- 1Q26 reinforced IMSR’s three-pillar execution roadmap, with progress across NRC licensing, DOE pilots, supply chain, and project origination.

- NRC approval of the PIE Topical Report adds a second foundational safety framework, improving regulatory visibility for repeat IMSR deployments.

- Riot collaboration creates a scalable data-center channel, expanding the commercial pipeline to ~10 projects and 7.8GW of indicative capacity.

- Cash burn remained controlled at $7.9 million, with $289.9 million of cash and investments supporting multi-year execution runway.

- Valuation remains compelling at ~$482 million EV, with upside tied to NRC progress, Riot conversion, fuel readiness, and project financing.

- 1Q26 showed progress across IMSR’s key commercialization vectors, with regulatory, DOE program, supply-chain, commercial pipeline, and liquidity milestones collectively advancing the de-risking narrative. IMSR continues to execute against a milestone-driven roadmap that is more appropriately measured by regulatory progress, project pipeline development, fuel readiness, supply-chain qualification, and cash runway than by near-term revenue. The quarter advanced all three of management’s stated pillars: IMSR engineering and regulatory programs, including DOE-backed TETRA and TEFLA projects; supply-chain development, including materials testing and supplier execution; and commercial pipeline expansion, led by the Riot Platforms collaboration. The company reported a 1Q26 net loss of $10.5 million, ended the quarter with $289.9 million of cash and investments, and reported quarterly cash burn of $7.9 million, while expanding its commercial pipeline to ~10 IMSR Plant projects representing 7.8GW of indicative power capacity.

- NRC approval of the PIE Topical Report adds another foundational element to IMSR’s licensing basis. In May, the NRC issued its Safety Evaluation Report approving IMSR’s Postulated Initiating Events methodology, following acceptance of the company’s final submission in April 2026. The approval validates IMSR’s framework for identifying and evaluating events that could challenge safe plant operation, making it a core safety-analysis milestone rather than a process update. Importantly, approved Topical Reports can be referenced in future operating license applications without repetitive re-evaluation, reducing review scope and supporting standardized outcomes across multiple IMSR deployments. The PIE approval builds on the NRC’s September 2025 approval of IMSR’s Principal Design Criteria, which addressed foundational safety and design requirements, including inherent safety, reactor power control, and load-following capability.

- The regulatory pathway is increasingly defined around operating-license readiness and repeat deployment. Construction permits enable large-scale plant construction and address major environmental requirements, while operating-license preparedness determines whether the nuclear systems satisfy safety standards for commercial operation. IMSR’s Topical Reports are most relevant to the latter because they resolve foundational safety analyses that can be reused in future applications. The company remains primarily focused on NRC Part 53 as the more practical pathway for initial IMSR deployment and fleet-scale licensing, while Part 57 appears more relevant to microreactors, with only limited potential applicability around waste-related provisions.

- DOE-backed TETRA and TEFLA advance two critical workstreams: reactor validation and fuel readiness. During the quarter, IMSR completed OTA contracts with the U.S. Department of Energy for Project TETRA, its reactor pilot project, and Project TEFLA, its fuel line pilot project. TETRA supports engineering and regulatory work for future IMSR Plant commercial operation, while TEFLA supports the infrastructure needed for IMSR fuel supply. Together, the programs address two gating items for advanced nuclear commercialization: licensing-quality reactor data and scalable fuel production capability. While traction is still programmatic rather than revenue-generating, successful execution should reduce schedule risk, strengthen NRC engagement, improve customer confidence, and support future fleet economics.

- Supply-chain work continued through graphite testing, materials qualification, and supplier development. IMSR’s materials testing and qualification programs remained active during the quarter, including graphite irradiation at NRG Petten, one of the world’s most powerful test reactors. This work is essential for reactor materials qualification, supplier selection, and licensing readiness, particularly because graphite performance is central to the IMSR Core-unit architecture. Supplier relationships also remained in active execution, supporting reactor component fabrication and fuel infrastructure development, while the company built out its supplier group for TETRA and TEFLA. These activities do not yet generate revenue, but they reduce first-of-a-kind execution risk by moving IMSR from design assumptions toward qualified materials, selected suppliers, and manufacturable components.

- Riot partnership creates a scalable data-center channel and expands IMSR’s commercial pipeline. In May, Terrestrial Energy and Riot Platforms announced a collaboration to develop co-located IMSR nuclear plants and hyperscale data centers for AI and high-performance compute applications. The partnership contemplates multiple 390MW IMSR Plants representing up to 4GW of nuclear capacity across U.S. candidate sites, including existing Riot facilities in Texas and Kentucky. The structure combines Riot’s hyperscale data-center development, operations, marketing, and leasing expertise with IMSR’s reactor design and licensing capabilities, creating a repeatable nuclear-plus-data-center template rather than a single-site project. IMSR’s physically separated non-nuclear energy conversion systems also enable hybrid configurations, including natural gas as a bridge fuel, which could accelerate commercial power availability and improve resiliency during project development.

- Collectively, 1Q26 strengthened the case that IMSR is moving from technology validation toward commercial deployment. The quarter connected regulatory progress, DOE-backed reactor and fuel programs, supply-chain qualification, and commercial origination into a clearer execution path. This matters because demand for clean, firm power continues to rise from AI infrastructure, reshoring, manufacturing electrification, and energy security needs. IMSR’s differentiated design directly addresses those use cases: the plant is roughly one-sixth the size of a conventional nuclear plant, uses turbines operating at nearly 50% greater efficiency than light-water-reactor-driven turbines, operates at low pressure, and relies on standard-assay uranium enriched to less than 5% U-235 rather than HALEU. These attributes support the core customer and financing proposition: lower deployment complexity, stronger fuel availability, improved affordability, and a more scalable path to repeat deployment.

- Additional IMSR project announcements remain an important 2026 commercialization catalyst. IMSR reaffirmed its expectation to announce 1-3 additional IMSR projects during 2026, with the Riot MOU representing progress against that target. Further site or strategic partner disclosures would help validate demand beyond a single data-center channel, increase visibility into pipeline quality, and provide investors with clearer evidence that IMSR’s commercial origination efforts are moving from broad market interest toward specific deployment opportunities.

- Fuel strategy remains a core IMSR differentiator, with TEFLA converting standard-fuel availability into a practical commercial supply pathway. IMSR uses standard-assay LEU enriched to less than 5% U-235, avoiding the HALEU enrichment levels of 15–20% required by many Generation IV peers and reducing exposure to commercial-scale HALEU supply constraints. TEFLA is therefore strategically important because enrichment is only the first step in IMSR’s fuel chain; the final reactor feed is IMSR fuel salt, requiring deconversion into uranium tetrafluoride and additional chemical production steps to meet licensed purity requirements. By developing this fuel-line process at pilot scale, TEFLA supports first-plant readiness, reduces fuel-supply execution risk, and strengthens the long-term recurring revenue opportunity tied to fuel supply and Core-unit services.

- Management also emphasized fuel flexibility but kept the commercial focus on affordability and deployment practicality. IMSR’s liquid-fuel design provides broader optionality than conventional solid-fuel reactors, and the company has evaluated LEU+ as a potential future input if it becomes widely available and commercially attractive. However, management continues to prioritize standard-assay LEU because the near-term nuclear market challenge is not maximizing fuel complexity, but delivering lower-cost, financeable, and scalable clean power. This keeps IMSR’s fuel strategy aligned with the broader commercialization thesis: reduce supply-chain risk, simplify deployment, and support repeatable fleet economics.

Investment Ramp Supports Commercialization Roadmap; Plant-Level Economics Remain Compelling

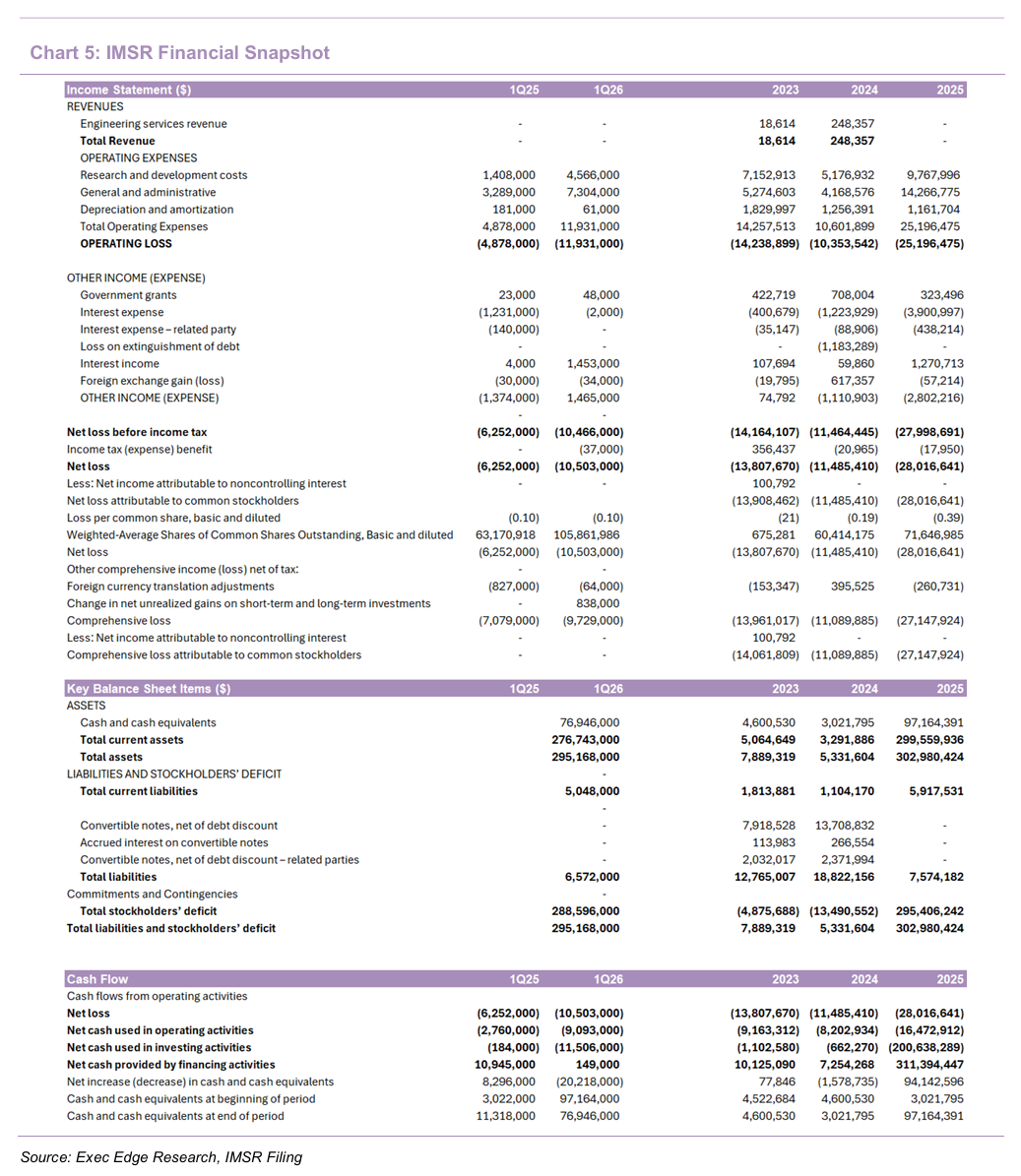

- Financial performance reflected planned execution spending, with sequential comparisons more useful given IMSR’s 2025 business transformation. IMSR reported a 1Q26 net loss of $10.5 million, compared with a $6.2 million net loss in 4Q25, as the company continued scaling fuel development, graphite testing, public-company infrastructure, and commercialization resources. On a sequential basis, R&D increased by $1.0 million, driven by fuel development and graphite testing programs, while G&A increased by $4.6 million, primarily reflecting headcount and stock-based compensation as IMSR builds out its public-company team. On a y/y basis, R&D increased by $3.2 million and G&A increased by $4.0 million, while other income and expense improved by $2.8 million due to lower interest expense and higher interest and dividend income. The spending ramp appears intentional and milestone-linked rather than reflective of operating inefficiency, with incremental investment directed toward the workstreams that matter most for commercialization: NRC engagement, fuel development, graphite testing, supplier qualification, and project origination.

- Cash burn remained controlled, and the balance sheet provides runway for milestone execution. IMSR ended 1Q26 with $289.9 million of cash and short-term investments, compared with $297.8 million at year-end, implying quarterly cash burn of $7.9 million. Burn increased $1.8 million sequentially after adjusting for one-time merger-related transaction costs, driven by a $0.6 million discretionary bonus payment, a $1.0 million accounts payable paydown to vendors offering extended credit terms, and $0.2 million of higher R&D payments. Share count increased by only ~100,000 shares from stock option exercises, leaving dilution minimal, while the balance sheet remains clean with limited liabilities, modest lease obligations, and no debt.

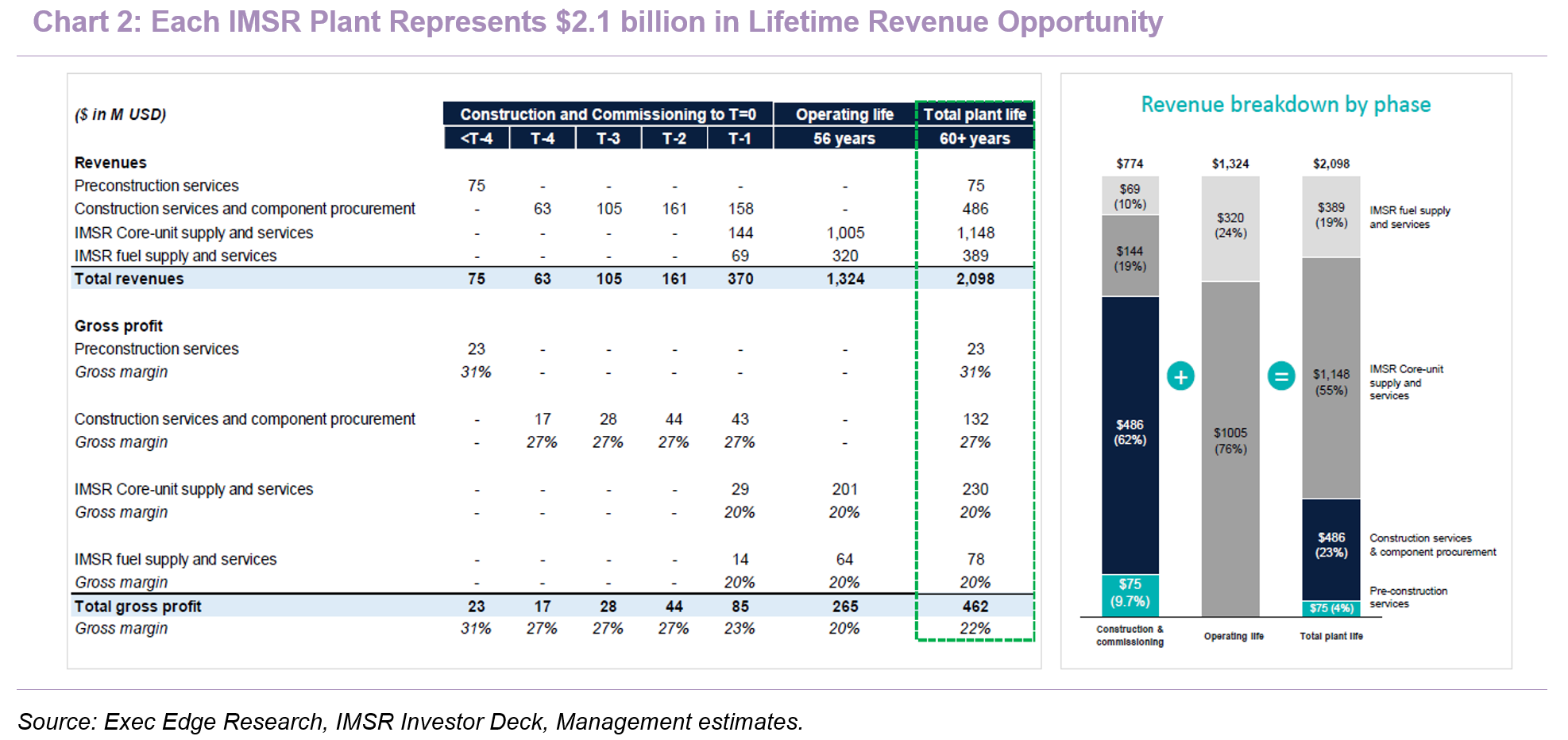

- Long-term unit economics remain compelling despite IMSR’s current pre-revenue stage. Management estimates that each IMSR Plant represents approximately $2.1 billion of cumulative revenue opportunity over a 60+ year plant life, including pre-construction services ($75 million), construction services and component procurement ($486 million), IMSR Core-unit supply and services ($1.148 billion), and IMSR fuel supply and services ($389 million). The model generates $774 million during the approximately four-year construction and commissioning phase, followed by $1.324 billion during the 56-year operating life, creating both upfront project revenue and long-duration recurring revenue after commercial operation begins.

- Revenue mix supports an annuity-like model anchored in Core-unit and fuel services. Management estimates a blended gross margin of approximately 22%, with pre-construction engineering services at 31%, construction services and component procurement at 27%, and Core-unit supply and fuel services each at 20%. Core-unit and fuel services together represent 74% of total plant-life revenue, or approximately $1.537 billion, with $1.324 billion generated over the operating life. This shifts IMSR’s model from episodic construction revenue toward recurring, multi-decade cash flows tied to fuel supply and Core-unit replacement cycles.

Long-Duration Nuclear Platform; Valuation Hinges on Commercialization Execution

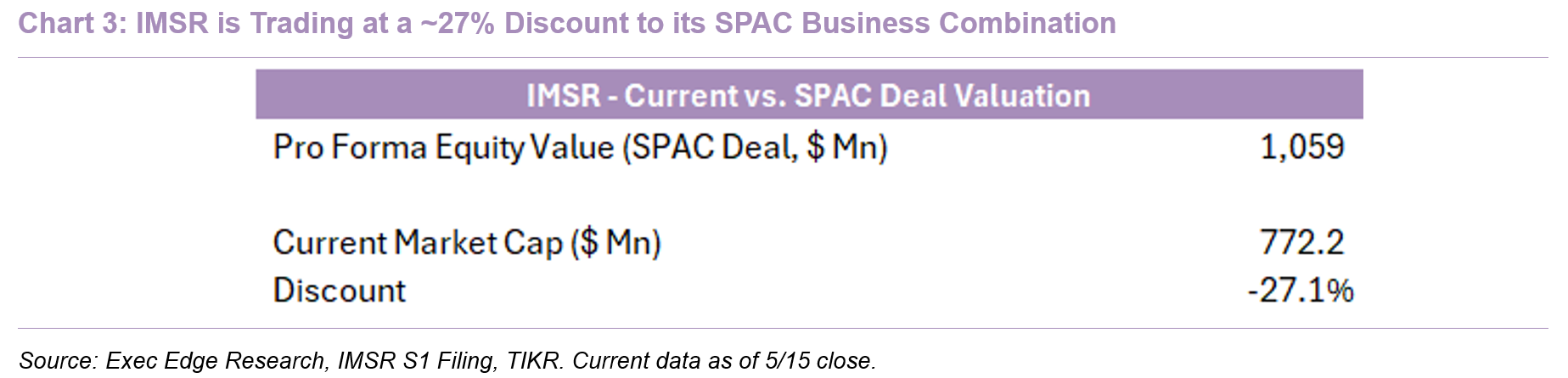

- IMSR’s current valuation reflects limited pricing of long-term commercialization potential relative to its business combination with HCM II Acquisition Corp. The following analysis is illustrative and not intended as a price target or investment recommendation but highlights the disconnect between current valuation and potential value creation as key milestones are achieved.

- IMSR currently trades at a material discount to the valuation implied at the time of its October 2025 business combination. At closing, the transaction implied a pro forma equity value of approximately $1.06 billion, based on ~105.8 million shares outstanding at $10.00 per share. As of May 15, 2026, IMSR’s equity market capitalization stands at approximately $772 million, representing a ~27% discount from the transaction reference value.

- Enterprise value provides a more appropriate basis for valuation at this stage of development. Adjusting for ~$290 million of cash and short-term investments, IMSR’s current enterprise value is approximately $482 million. In effect, the market is attributing less than $500 million of value to IMSR’s operating platform, intellectual property, regulatory progress, fuel strategy, and project pipeline, despite more than a decade of development and recent progress across NRC approval of the PIE Topical Report, completed DOE OTA contracts for TETRA and TEFLA, and the Riot data-center collaboration.

- Current valuation reflects execution and timeline risk despite a capital-light model supporting more efficient long-term value creation. This valuation primarily reflects a discount for time-to-commercialization and execution risk rather than a reassessment of the long-term addressable opportunity. IMSR’s capital-light model, focused on design, component supply, and fuel provision rather than plant ownership, should enable more efficient capital deployment than traditional nuclear developers. IMSR remains pre-revenue, with first commercial plant operations targeted for 2034, and near-term financials are expected to reflect elevated R&D and public company costs. However, the company has differentiated itself within the Generation IV nuclear landscape through commercially available SALEU fuel, completion of the Canadian Nuclear Safety Commission’s Vendor Design Review, advancing NRC engagement, and DOE-supported programs addressing licensing, reactor validation, and fuel readiness.

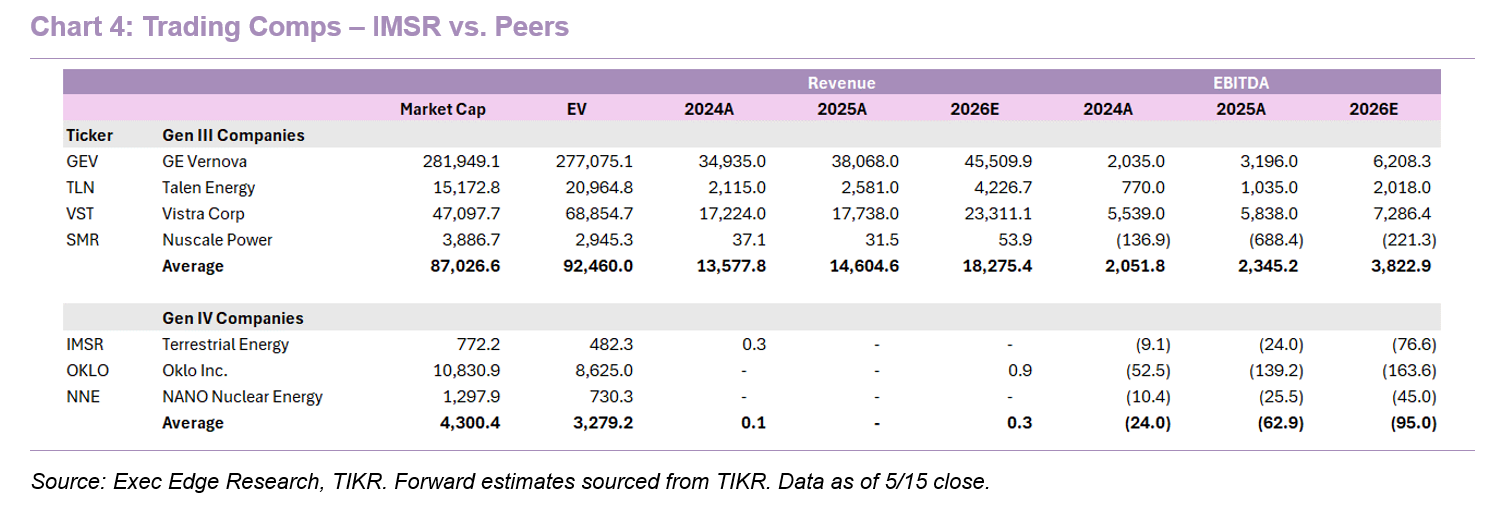

- Relative valuation comparisons underscore this dynamic. Established Generation III nuclear operators trade at significantly higher enterprise values supported by operating fleets and stable cash flows, while Generation IV developers trade at materially lower valuations reflecting pre-revenue status and development risk. As advanced nuclear technologies progress toward commercialization, valuation outcomes are likely to increasingly differentiate based on regulatory readiness, fuel availability, and execution credibility. In this context, IMSR’s valuation can be viewed as a long-duration option on regulatory and project execution, supported by a substantial cash balance providing multi-year runway.

- Bottomline: At $482 million of enterprise value, IMSR reflects significant execution and timeline risk while offering asymmetric upside to regulatory and commercialization milestones, supported by a multi-year cash runway. 2026 remains milestone-driven, with progress across NRC licensing, TETRA, TEFLA, fuel readiness, Riot/data-center origination, and flagship project development as key drivers of potential re-rating.

Download the Complete Report Here

Read Exec Edge’s Initiation on Terrestrial Energy Here

Subscribe to our Weekly Newsletter to Receive All Research

Contact: