Download the Complete Report Here

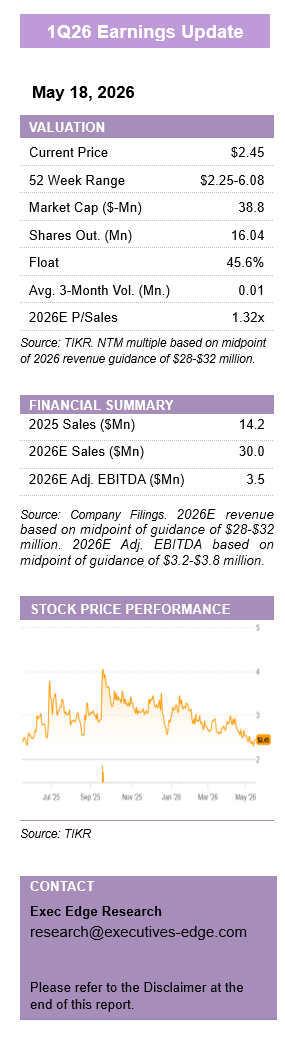

Barfresh Food Group, Inc. (BRFH)

Barfresh Food Group, Inc. (BRFH)

Revenue Beat Supports Transition-Year Setup. Manufacturing Integration and Customer Recovery Position BRFH for 2H26 Inflection.

- Key Takeaways:

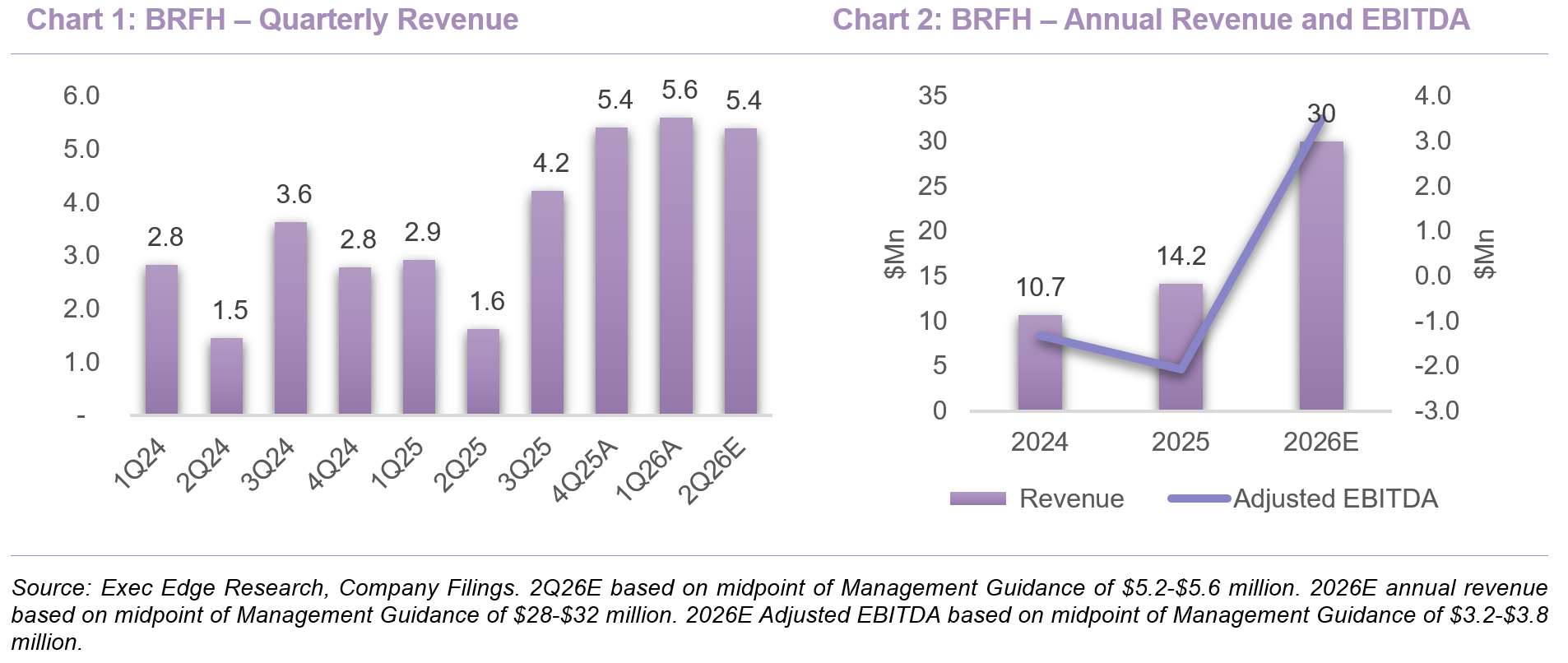

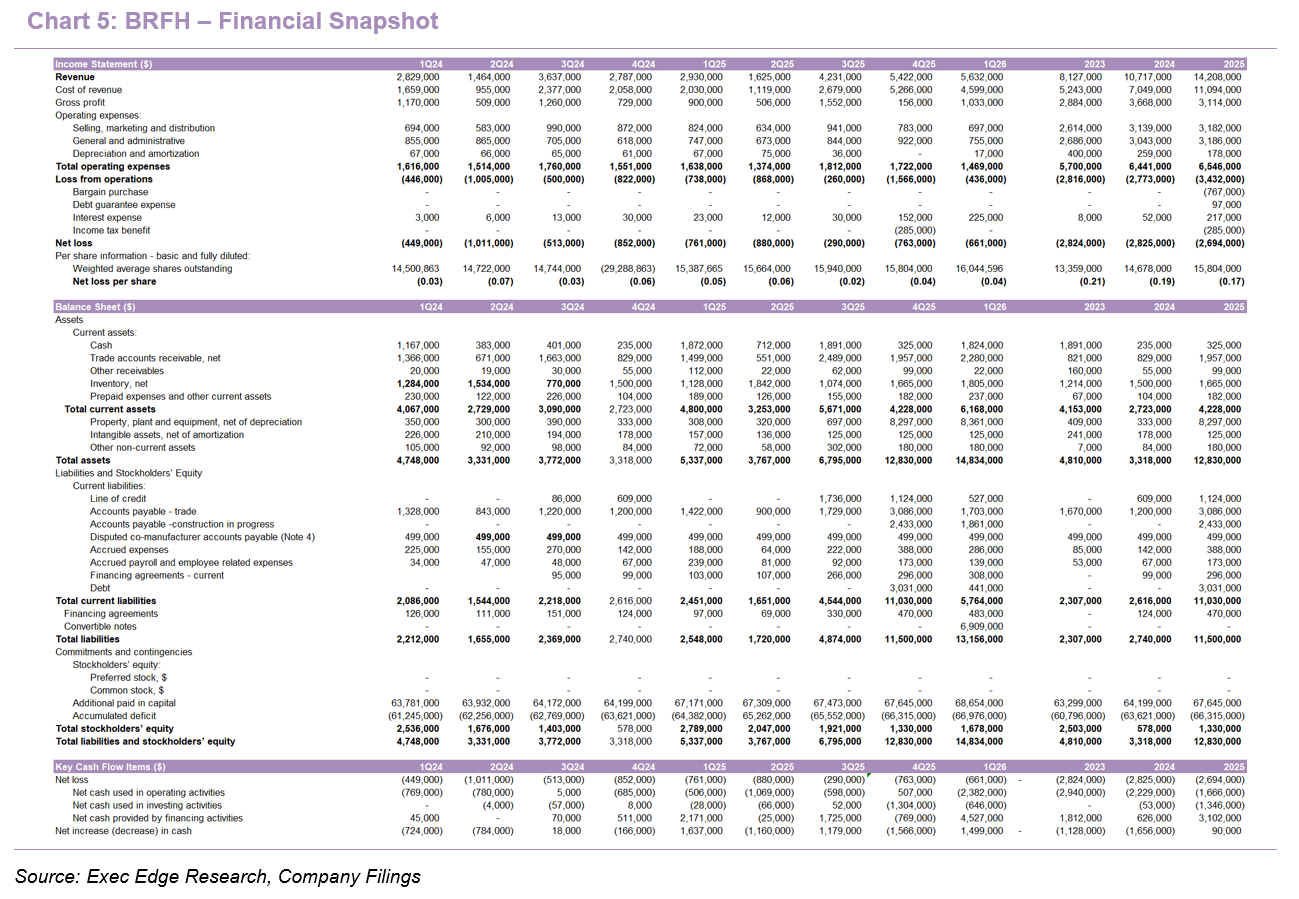

- Revenue increased 92% y/y to $5.6 million, exceeding $5.0-$5.2 million guidance, driven by stronger Arps milk contribution.

- Gross margin declined to 18% from 31% y/y as lower-margin milk mix and facility startup costs weighed on profitability.

- Education recovery is building, with active bid season, broker-led reactivation, and large-district momentum supporting a stronger 2H26 setup.

- FY26 guidance remains $28-$32 million revenue and $3.2-$3.8 million adjusted EBITDA, implying sharp 2H26 conversion.

- At ~$39 million market cap and 1.32x 2026E sales, valuation discounts capacity-led upside and EBITDA scalability.

- Top-line beat was driven by stronger-than-expected contribution from Arps Dairy’s milk processing operations, supporting continued revenue scale-up. BRFH’s 1Q26 revenue increased 92% y/y to $5.6 million from $2.9 million in 1Q25, exceeding management’s $5.0-$5.2 million guidance range. The upside was driven by stronger-than-anticipated contribution from Arps Dairy’s raw and processed milk business, which expanded the consolidated revenue base but carries a lower margin profile than BRFH’s core frozen beverage and food products.

- Profitability reflected the transitional nature of the model shift, with gross margin pressure partly offset by opex discipline and a narrower adjusted EBITDA loss. Gross margin declined to 18% in 1Q26 from 31% in 1Q25, driven by Arps Dairy’s lower-margin milk processing contribution and startup costs associated with producing in the newly acquired processing facility. Adjusted EBITDA improved to a loss of $238,000 from a loss of $506,000 y/y, but came in below prior breakeven expectations because revenue mix was more heavily weighted toward lower-margin milk processing than anticipated and production volumes through the acquired facility were lower than planned. Net loss improved to $661,000 from $761,000 y/y, indicating that revenue scale and cost discipline are beginning to narrow losses, though not yet enough to fully offset integration costs and facility ramp inefficiencies.

- Operating expenses remained controlled, reinforcing operating leverage potential once gross margin normalizes and higher-margin education volume ramps. Selling, marketing and distribution expense declined to $697,000 from $824,000 in 1Q25, reflecting lower personnel costs as BRFH increasingly leverages its broker network, reduced sampling expense following the Pop & Go freeze pop launch, and lower equipment maintenance costs as single-serve products become a greater share of the education-channel mix. G&A expense was essentially flat at $755,000 versus $747,000 y/y.

- Arps Dairy remains the central strategic initiative as it gives BRFH production control, improves customer credibility, and creates the manufacturing base needed to support a larger institutional platform. The Arps processing facility supported ~50% of BRFH’s frozen beverage and food volume in 1Q26, while the company continued to use co-manufacturers for some product during the transition. We view this as a staged internalization process rather than a completed transition, with current inefficiencies tied to equipment ramp-up, installation timing, training, and lower-than-planned production volumes through the owned facility. The strategic benefit is that owned production gives BRFH greater control over availability, timing, and execution, reducing reliance on third-party co-manufacturers while strengthening its ability to pursue larger school districts and foodservice accounts that require dependable supply at scale.

- Manufacturing transition remains the key near-term drag on margins, but the bridge to recovery is becoming clearer. Gross margin declined to 18% in 1Q26 from 31% in 1Q25, reflecting Arps Dairy’s lower-margin raw and processed milk business, commodity-price fluctuations, and startup costs tied to production transfer. The processed milk business was running at roughly 5% margin in segment reporting, compared with a normalized consolidated gross margin target in the low-40% range. As throughput improves, new equipment is installed, and school-year volume shifts mix toward core Barfresh products, consolidated gross margin should begin recovering from the 1Q26 trough.

- Revenue mix remains the critical 2H26 swing factor as growth shifts from lower-margin milk processing toward core education products. Arps’ legacy milk business is expected to remain relatively flat rather than drive substantial growth, and its stronger-than-expected 1Q26 contribution was margin-dilutive despite helping revenue exceed guidance. The more important 2H26 test is whether higher-margin core Barfresh education volume becomes a larger percentage of revenue as school-year orders ramp and lower-margin Arps milk revenue becomes less dominant in the consolidated mix. That mix shift is central to both the 2026 adjusted EBITDA guide of $3.2-$3.8 million and the longer-term operating leverage case as BRFH scales through its vertically integrated platform.

- The larger 44,000-square-foot Defiance facility remains on track for commissioning before year-end 2026 and should provide the step-change in throughput, flexibility, and unit economics needed for the next phase of growth. BRFH continues to procure and install equipment and personnel at the larger Ohio facility, supported by a $2.4 million government grant for specialized equipment and the $7.5 million senior convertible note financing completed in March 2026. The financing allowed BRFH to pay off the existing mortgage on the facility and own it free and clear, while management expects to evaluate mortgage and equipment financing against the unencumbered facility to support growth objectives and potentially repay a portion of the convertible note.

- Customer recovery and large-district momentum reinforce demand visibility in the core education channel, where supply reliability is often as important as product adoption. Education remains BRFH’s primary focus and greatest near-term opportunity, with tangible progress rebuilding customer relationships and adding new school district wins during 1Q26. The broker network and direct sales team have been communicating manufacturing progress and improved supply reliability to districts, and that message appears to be gaining traction. The 7-year award with the fifth largest school district in the U.S. remains a key validation point, demonstrating that BRFH can compete for large-scale procurement contracts where compliance, operational simplicity, and dependable fulfillment are central decision criteria. More importantly for the current quarter, bid season remains active and the company is progressing on customer reactivation as prior supply constraints ease.

- Active bid season and customer reactivation point to a potentially strongest-ever back half for core Barfresh products. BRFH is still receiving bids for the upcoming school season and is actively returning to customers that dropped off because of prior lack of supply. Management expects a step increase in revenue as the school year begins, driven by both new customers and recovered accounts, and described the upcoming back half as potentially the strongest ever for Barfresh products. This is important because 1Q26 revenue upside was Arps-led, while 2H26 should provide a cleaner read on whether improved production reliability is converting into recurring core education revenue, reinstated districts, and new school wins.

- BRFH’s 2026 priorities remain centered on completing the manufacturing transition, rebuilding education demand, and expanding the long-term revenue base. The immediate focus is commissioning the new manufacturing facility before year-end 2026, which should improve production efficiency, capacity, and supply reliability. In parallel, the company is rebuilding and expanding its education customer base following prior supply disruptions, while beginning to evaluate adjacent opportunities in foodservice, convenience, and other channels as capacity increases. Longer term, the expanded facility could also support co-manufacturing revenue once operations are stabilized, adding a potential incremental growth stream beyond BRFH’s core branded education business.

- 2026 remains a transition year, with revenue growth and EBITDA conversion weighted to the back half. Management introduced 2Q26 revenue guidance of $5.2-$5.6 million, representing more than 200% growth versus the prior-year period, and expects an adjusted EBITDA loss of $0.3-$0.2 million as the company continues progressing through manufacturing transition and facility optimization. At the midpoint, 2Q26 revenue of $5.4 million would be roughly in line with 1Q26 revenue of $5.6 million, but the y/y comparison remains strong because 2Q25 was seasonally weak for the legacy Barfresh business. The company reiterated 2026 revenue guidance of $28-$32 million, representing 97%-125% growth versus 2025, and adjusted EBITDA guidance of $3.2-$3.8 million, implying profitability should improve meaningfully in 2H26 as school-year demand, production efficiency, and product mix improve.

- The 2026 guide embeds a clear 2H26 inflection, with execution dependent on school-year volume, mix recovery, and facility optimization. At the midpoint, 2026 revenue of $30.0 million implies approximately 111% y/y growth from 2025 revenue of $14.2 million, while adjusted EBITDA of $3.5 million implies an approximately 11.7% adjusted EBITDA margin. This compares with a 1Q26 adjusted EBITDA loss of $238,000 and a 2Q26 guided adjusted EBITDA loss of $0.2-$0.3 million, meaning the full-year outlook depends on 3Q26 and 4Q26 execution. The key upcoming indicators are gross margin recovery from 18%, higher core Barfresh mix, throughput improvement in the existing facility, bid conversion for the new school year, customer reactivations, and confirmation that the larger Defiance facility remains on track before year-end.

- Illustrative 2027 outlook highlights significant operating leverage potential, driven by new customer opportunities. Based on illustrative figures presented in BRFH’s investor presentation (not to be interpreted as formal guidance), management outlined a potential pathway to ~$70 million in revenue by 2027 (vs. ~$28-32 million base in 2026), driven by $40 million+ incremental contribution from new customer opportunities under discussion. This potential is contingent on conversion of current discussions and incremental capital deployment to support capacity expansion.

- On profitability, illustrative adjusted EBITDA could scale to ~$14.5-$16.5 million in 2027, supported by ~$11 million in incremental EBITDA from these opportunities. These assumptions are underpinned by strong inbound interest from large, branded customers amid constrained U.S. dairy manufacturing capacity, as well as BRFH’s expanded production footprint, which could support up to ~$250 million of long-term revenue capacity. This highlights the magnitude of operating leverage available as facility utilization ramps and a larger share of revenue flows through the vertically integrated manufacturing platform.

- Working capital remains thesis-relevant because seasonal school demand requires inventory readiness and dependable service levels. As of March 31, 2026, BRFH had approximately $4.1 million of cash and accounts receivable and approximately $1.8 million of inventory, modestly above the ~$1.7 million level at year-end 2025. The inventory build appears constructive if it supports back-to-school readiness and customer reactivation, though cash conversion should be monitored as production transitions and demand ramps through 2H26.

- Financing and grant support provide flexibility to fund the manufacturing transition and facility expansion. The company secured a $7.5 million senior convertible note financing alongside a $2.4 million government grant for specialized equipment installation, providing capital to support facility build-out and operational growth through 2026. Management may also pursue mortgage or equipment financing backed by the unencumbered facility to support future growth initiatives and potentially repay a portion of the convertible notes, while preserving liquidity for operational needs during construction.

Attractive Valuation as Growth Accelerates and Margin Recovery Builds

- Our analysis suggests BRFH remains undervalued relative to its growth profile, manufacturing transition, and potential EBITDA inflection. The following analysis is illustrative in nature and does not constitute a price target or investment recommendation. We assess valuation using a combination of absolute, time-series, and relative peer-based approaches to frame potential re-rating as revenue growth, gross margin recovery, and profitability improve.

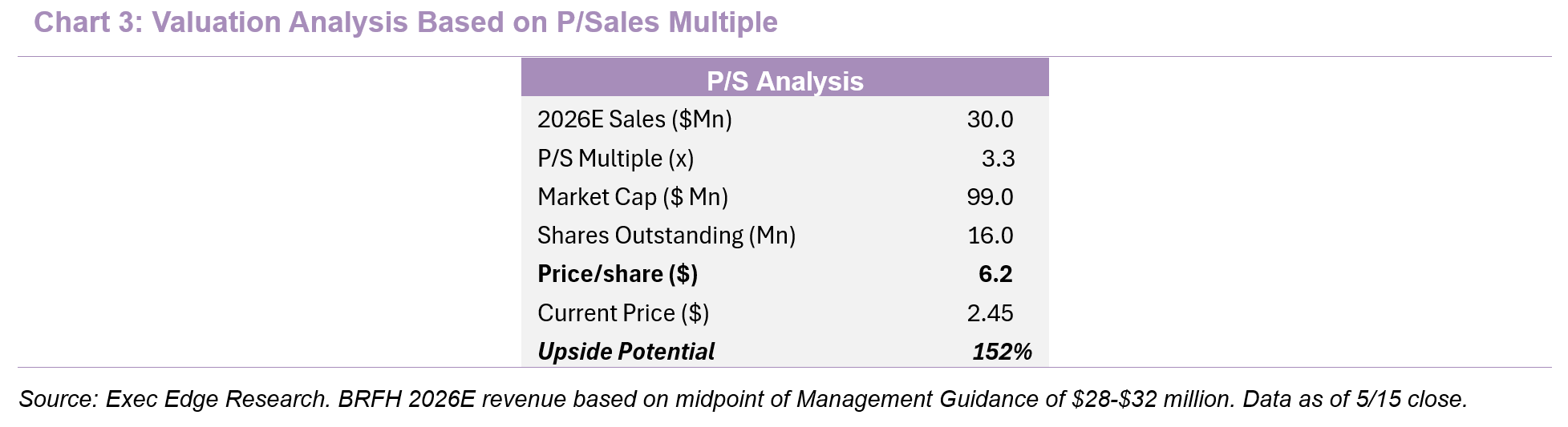

- BRFH currently trades at a discount to both its historical trading range and relevant peers, despite a step-change in revenue growth and a guided profitability inflection. Based on management guidance, BRFH is positioned to deliver approximately 111% revenue growth in 2026E at the midpoint of the guidance range, alongside adjusted EBITDA of approximately $3.5 million. This outlook is supported by improved supply reliability, reactivation of education accounts, facility optimization, and incremental daypart expansion, dynamics that do not appear fully reflected in the current multiple. At present, BRFH trades at 1.32x 2026E P/Sales, representing a meaningful discount to its one-year mean of 2.25x and well below its one-year peak multiple of 3.92x.

- Applying a 3.3x P/Sales multiple, which remains conservative relative to the one-year peak, to BRFH’s 2026E revenue estimate implies an illustrative equity value of approximately $6.2 per share versus the current share price of $2.45. Importantly, this framework does not require premium multiple expansion; it assumes only partial reversion toward prior trading levels as revenue growth accelerates, gross margin recovers, and adjusted EBITDA turns positive.

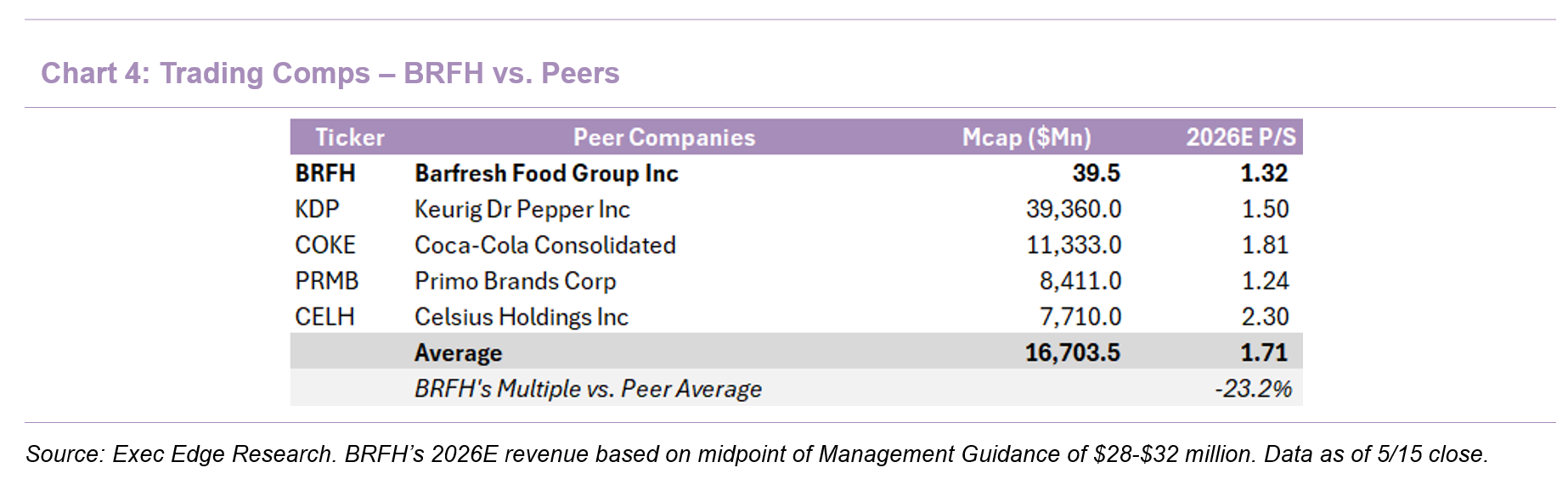

- Relative valuation also supports the rerating case. BRFH trades at 1.32x 2026E P/Sales versus a peer average of 1.71x, despite accelerating revenue growth, improving visibility into manufacturing normalization, and management’s reiterated expectation for positive adjusted EBITDA in 2026E. We believe the valuation discount could narrow as BRFH executes on its vertically integrated manufacturing strategy, improves production efficiency, regains school customers following prior supply disruptions, and demonstrates stronger operating leverage through the 2026 school-year ramp.

- We believe re-rating potential will increasingly depend on execution against measurable operational milestones, including sustained revenue growth through the school-year ramp, continued gross margin recovery from the 18% level reported in 1Q26, improved production efficiency as transition costs normalize, and achievement of positive adjusted EBITDA during 2026. Demonstrated supply reliability, successful customer re-engagement in education, commissioning of the 44,000-square-foot Defiance facility, and progress toward higher utilization of the vertically integrated manufacturing platform could support valuation convergence toward peer and historical benchmarks.

Download the Complete Report Here

Read Exec Edge’s Initiation on Barfresh Food Group Here

Subscribe to our Weekly Newsletter to Receive All Research

Contact: