Download the Complete Report Here

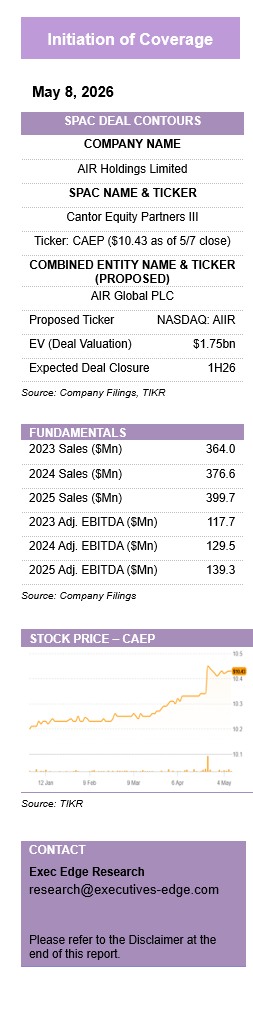

AIR Global PLC (Proposed Ticker: AIIR)

Global Flavored Shisha Leader Scaling into Higher-Value, Device-Led Inhalation Platforms

Global Flavored Shisha Leader Scaling into Higher-Value, Device-Led Inhalation Platforms

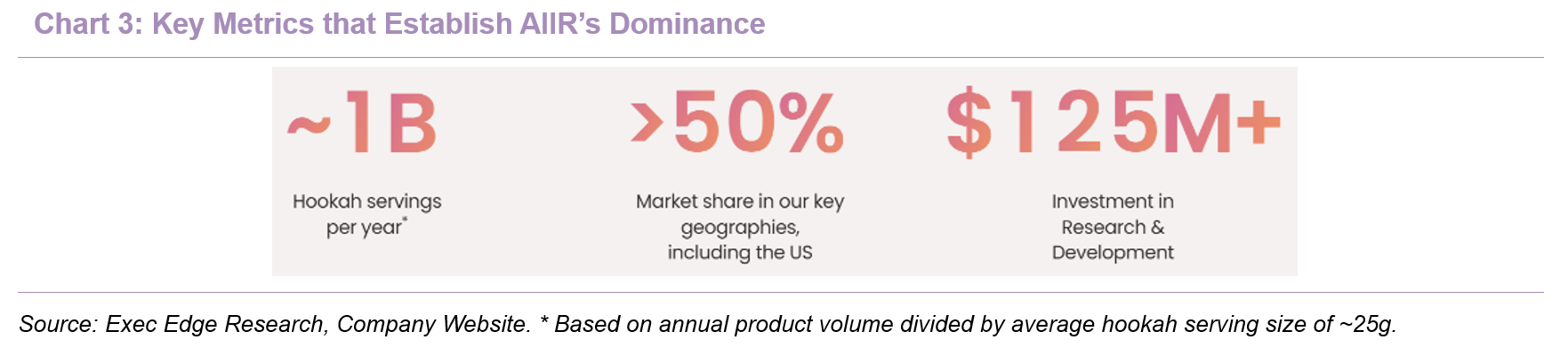

- AIIR enters public markets as a scaled, cash-generative category leader, offering differentiated exposure to a stable, value-led consumption category with embedded upside from mix evolution. The business is anchored by Al Fakher, the largest flavored shisha brand globally, serving ~14 million home consumers, supporting over 2.5 million daily sessions, and enabling ~1 billion annual servings across 90+ markets. Unlike many de-SPAC listings, AIIR combines scale, profitability, and positive cash generation at entry, positioning it as both a durable earnings base and a transition story.

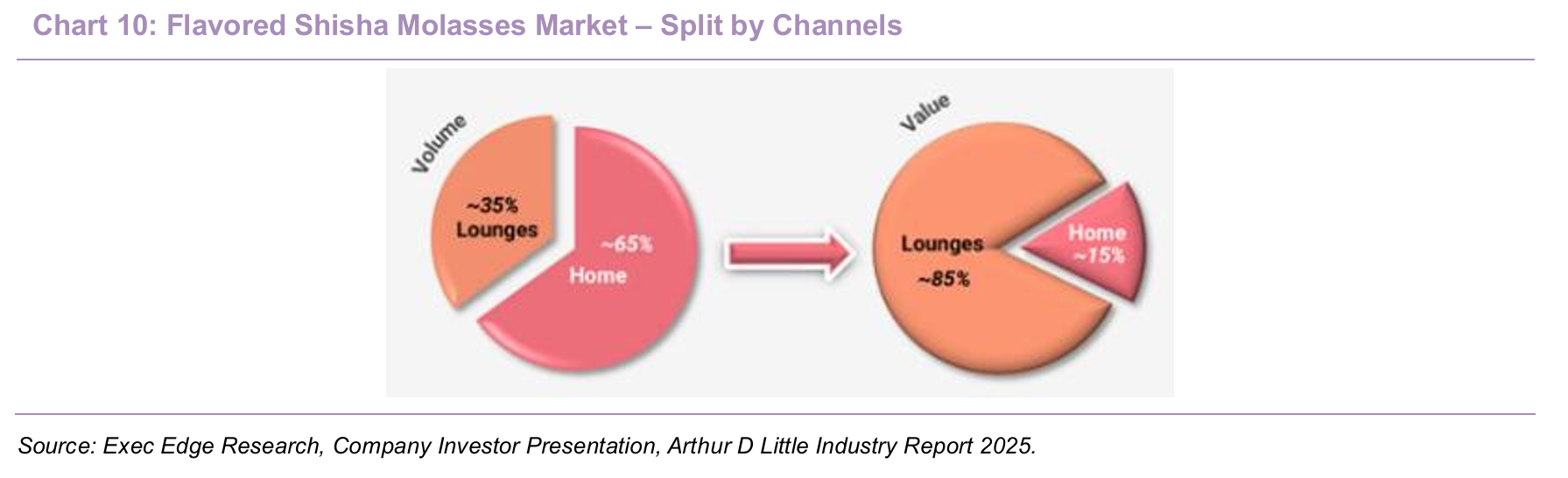

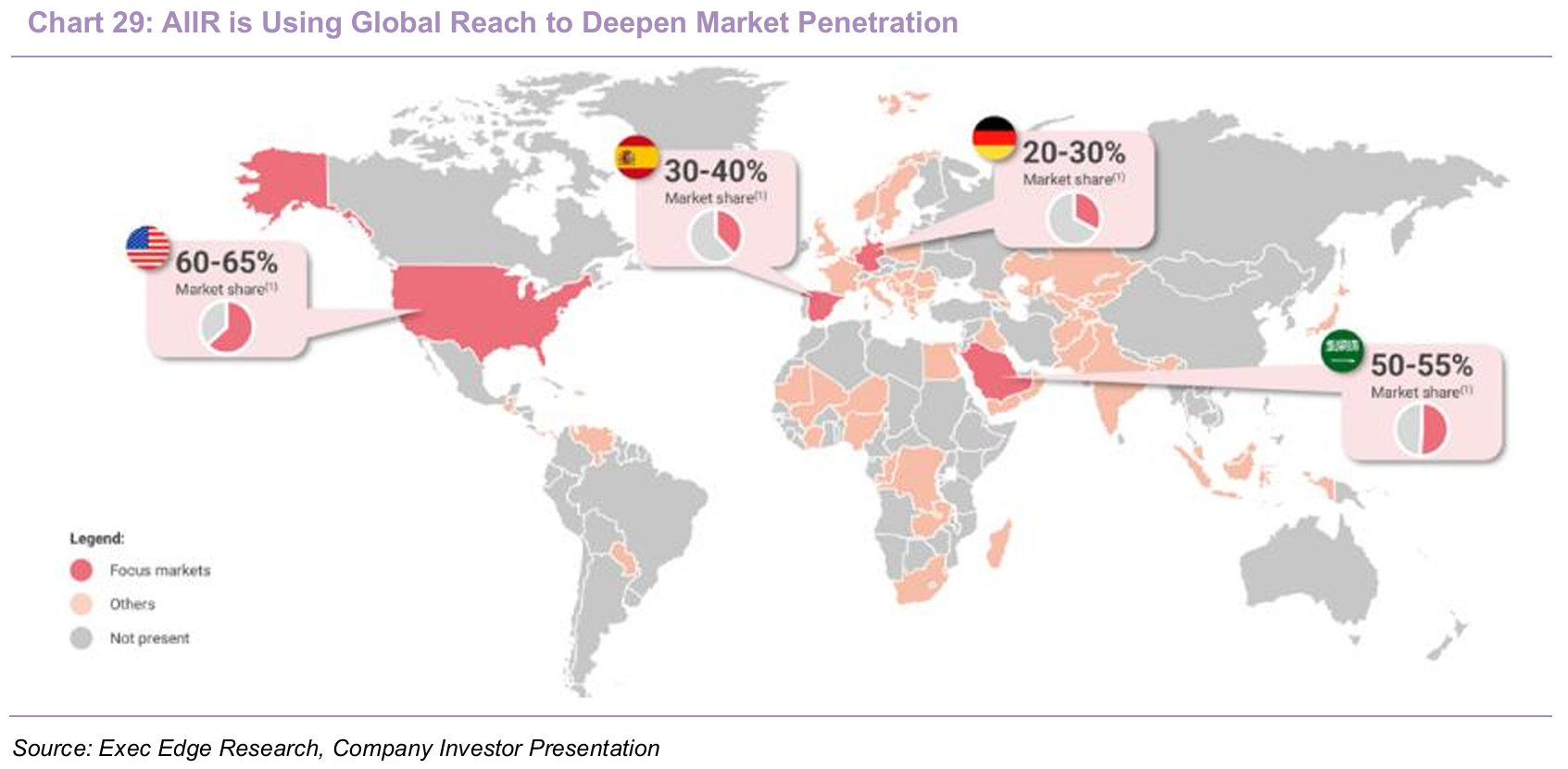

- The company’s right-to-win is underpinned by category leadership, channel dominance, and structural advantages in value capture. AIIR holds 36%-44% market share across operating markets (ex-Russia and Turkey) and >50% in key geographies including the U.S., supported by strong brand recall and presence across lounges, retail, HORECA, and digital channels. These channels are critical, with ~35% of volume generating ~85% of value, reinforcing the importance of brand trust and menu visibility. This is supported by global distribution scale, ownership of digital platforms such as Hookah.com and Shisha-World, and continued product innovation and collaborations. Together, these factors underpin pricing power, repeat consumption, and a durable competitive position.

- Industry trends support AIIR’s strategy and reinforce its positioning to capture category evolution. Shisha is emerging as a stable, value-led category, with ~3.6% retail value CAGR versus ~1.6% volume growth (2025-2030, source: Arthur D. Little), favoring branded incumbents with pricing and mix leverage. At the same time, charcoal-free systems, device-led formats, and adjacent nicotine products are expanding the addressable market, while rising regulatory complexity increases barriers to entry. AIIR is aligned with these shifts through OOKA, nicotine pouches, and functional inhalation (VANT), supported by digital platforms that enhance product rollout, consumer insight, and merchandising control.

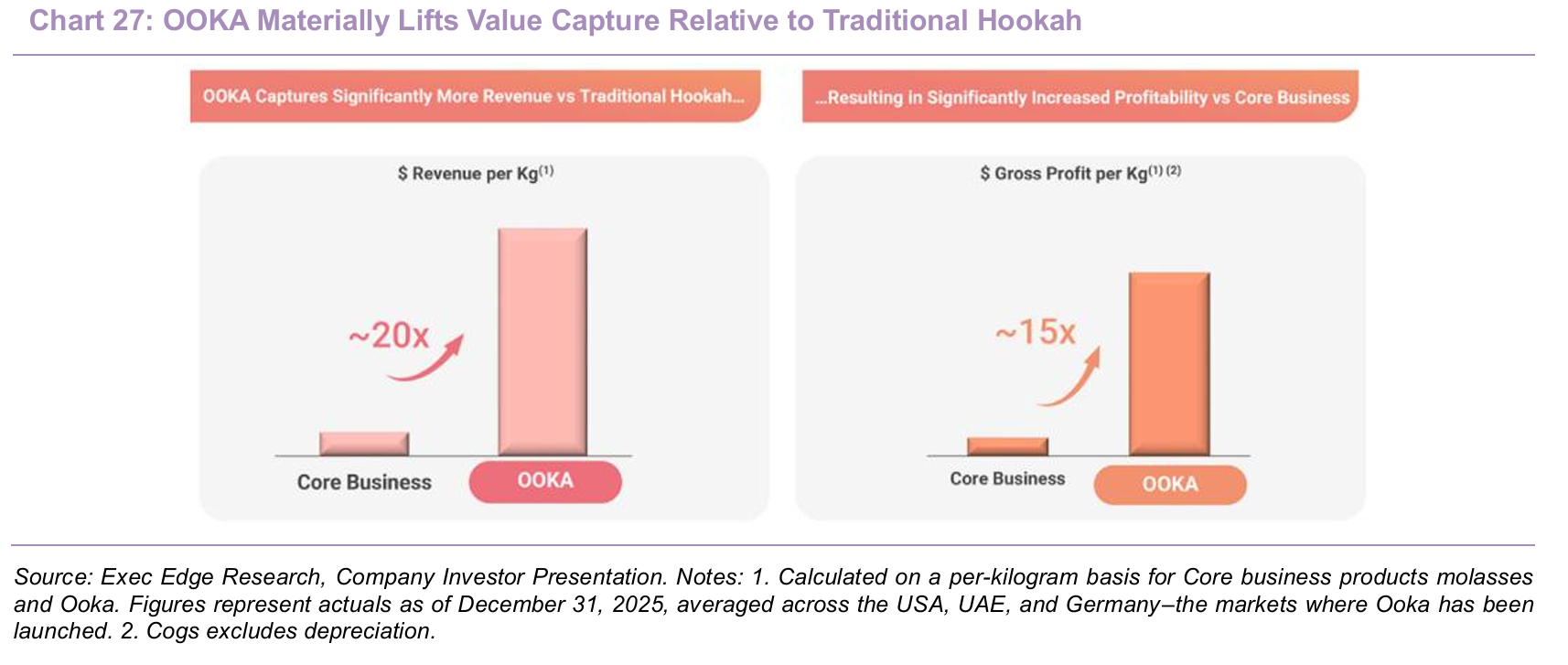

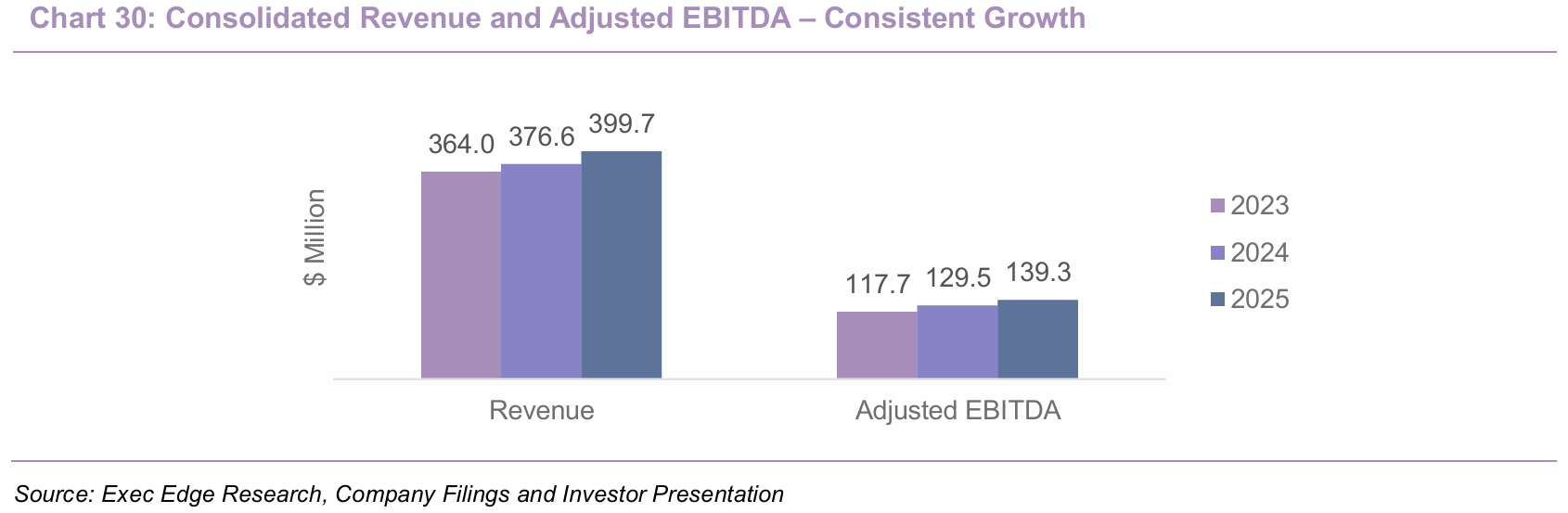

- Financial profile reflects a high-quality, self-funded growth model anchored by a strong core earnings base. The core business operates at ~40% adjusted EBITDA margins, with consolidated margins of ~34.8% in 2025 despite ongoing investment. The company generated $399.7 million of revenue, $139.3 million of adjusted EBITDA, and $115.9 million of operating cash flow in 2025, with ~83% cash conversion. Growth is expected to be driven by premiumization, pricing, and mix, with OOKA as the key catalyst. The device-and-pod system delivers ~20x revenue and ~15x gross profit per kg vs. traditional products, while adjacent categories expand the TAM.

- At an implied ~$1.75 billion EV (4.4x EV/LTM sales and 12.6x EV/LTM EBITDA), valuation is anchored in a resilient core while embedding optionality from higher-value platforms. The current multiple reflects a balance between established profitability and the need to demonstrate execution in newer segments. We believe re-rating potential will depend on successful scaling of OOKA, traction in adjacent categories, and consistent public-market delivery, positioning AIIR as a transition from a branded consumables business to a broader inhalation platform.

Company and SPAC Deal Overview

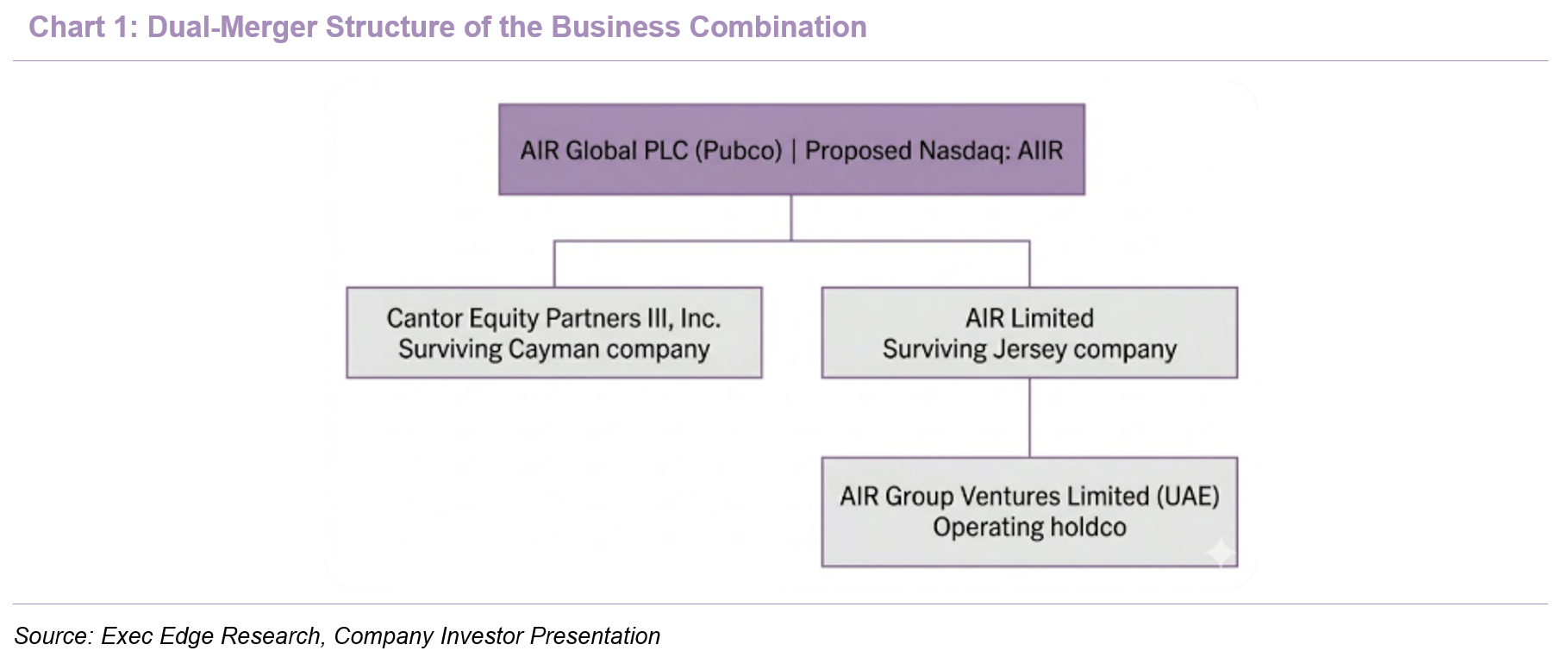

AIR Limited + Cantor Equity Partners III (CAEP) = AIR Global PLC (NASDAQ: AIIR)

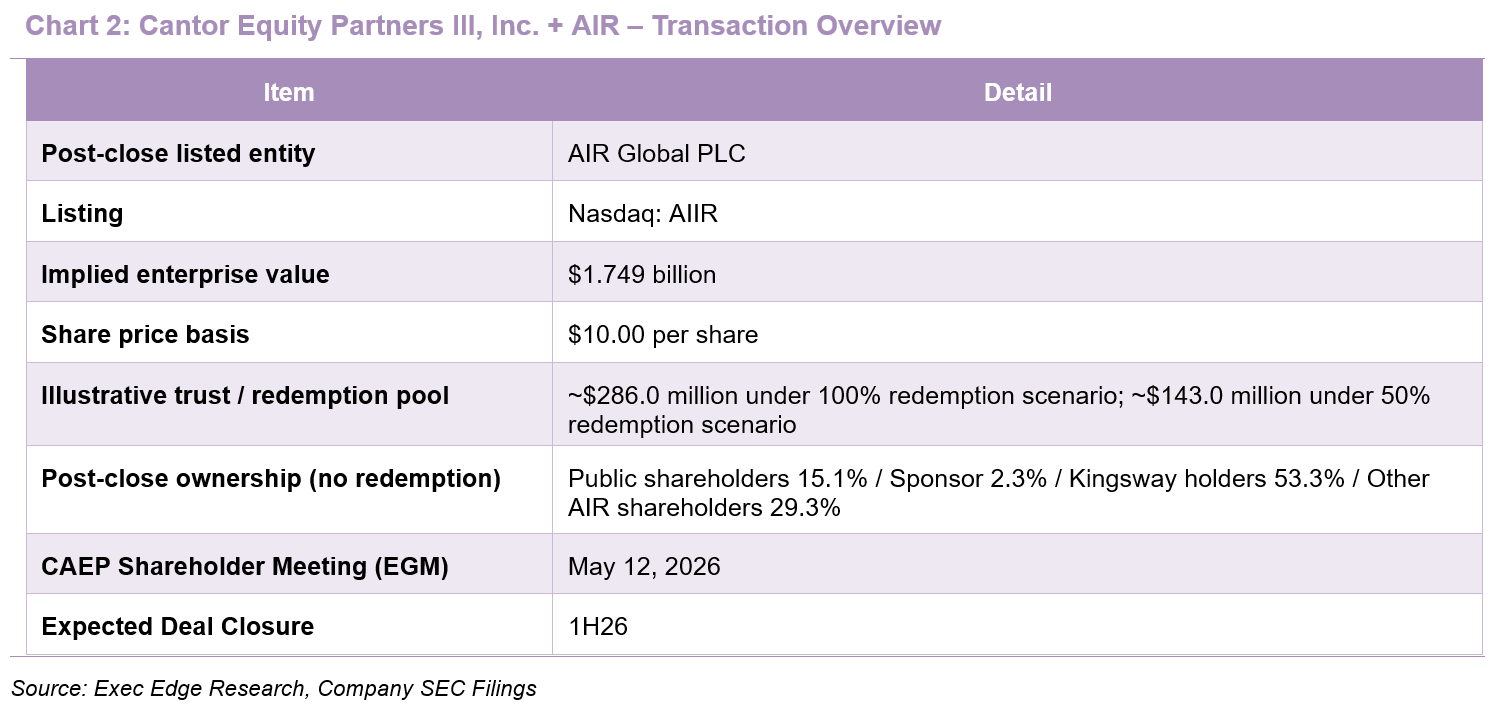

- AIR Global PLC – a global market leader in flavored molasses (commonly known as hookah, shisha or mu’assel) – is entering public markets through a business combination with Cantor Equity Partners III (CAEP), expecting to list on the Nasdaq under the ticker AIIR in 1H26 at a pro forma enterprise value of ~$1.75 billion. The company will execute its public listing through a dual-merger structure under a newly formed holding company, AIR Holdings Limited, which effectively consolidates the legacy operating business and the SPAC vehicle. The transaction involves two sequential steps: (1) Genesis Cayman Merger Sub Limited will merge with and into CAEP, with CAEP surviving as a wholly owned direct subsidiary of Pubco, and (2) Genesis Jersey Merger Sub Limited will immediately merge with and into AIR Limited, with AIR Limited surviving as a wholly owned direct subsidiary of Pubco. Following these steps, Pubco will be renamed AIR Global PLC and will list on the Nasdaq under the ticker AIIR, with the underlying business generating $399.7 million in revenue, $139.3 million in adjusted EBITDA, and $46.8 million in profit for 2025. By establishing AIIR as the ultimate parent over both the SPAC vehicle and the operating business, management is targeting a streamlined transition to public markets. On April 23, 2026, the company announced effectiveness of the F-4 registration statement ahead of the planned merger and Nasdaq listing. CAEP has scheduled its extraordinary general meeting for May 12, 2026 to approve the transaction, which is expected to close shortly thereafter, subject to customary closing conditions. We refer to AIR Global PLC as AIIR throughout this report.

- The transaction implies a pro forma enterprise value of ~$1.75 billion and results in a concentrated ownership structure, limited public float, and heightened sensitivity to redemption outcomes. Public shareholders retain the right to redeem their CAEP shares for cash, with the F-4/A presenting no-redemption, 50% redemption, and 100% redemption cases. Based on the filing, 27.6 million public shares were outstanding, and the illustrative redemption value was $10.36 per share as of December 31, 2025, inclusive of the $0.15 per redeemed share support amount funded through the Sponsor Note. Assuming no redemptions, public shareholders would own 15.1% of pro forma equity and voting power, the sponsor 2.3%, AIR shareholders excluding Kingsway 29.3%, and the Kingsway holders 53.3%, resulting in the company qualifying as a controlled company under Nasdaq rules. As a result, AIIR may rely on certain governance exemptions, and combined with concentrated ownership, minority shareholders are likely to have limited influence over corporate decisions. The sponsor has also agreed to surrender 3.4 million founder shares and subject 1.5 million post-close shares to earnout conditions. The transaction is structured primarily as a public listing event rather than a capital raise, with AIIR entering the market as an already cash-generative business and not dependent on SPAC proceeds to fund its core strategy.

- We believe the resulting company offers a relatively unusual combination of scale, cash generation, and category optionality. AIIR entered the transaction with a profitable core business anchored by Al Fakher, having generated $397 million of revenue and $158 million of adjusted EBITDA from core products in 2025, while the broader business generated $399.7 million of revenue, $139.3 million of adjusted EBITDA, and $46.8 million of profit for the year. AIIR is not approaching the market as a pre-revenue nicotine challenger or a concept-stage device platform. Instead, investors are being asked to underwrite a leading branded hookah franchise with established scale, recurring cash generation, and a strong market position, while retaining upside from OOKA, digital commerce, and adjacent inhalation categories. This combination should broaden the potential investor base, although concentrated ownership, redemption variability, and category-specific regulatory risk are likely to remain central debates around the listing.

Global Hookah Leader Expanding into Higher-Value Inhalation Platforms

- AIIR is a scaled, branded flavored molasses platform built around Al Fakher, which remains the economic and strategic center of the business. The company traces the Al Fakher brand back to 1999 and positions it as its flagship franchise, with strong recognition across core Middle Eastern markets as well as the U.S. Al Fakher is the largest flavored molasses brand globally – it owns 3 of the 5 best-selling flavors worldwide, serves ~14 million home consumers, and supports over 2.5 million daily sessions. AIIR estimates that the company enables ~1 billion hookah servings annually, holds >50% market share in key geographies including the U.S., and has invested more than invested more than $125 million in product development, engineering, and innovation across OOKA and VANT since 2019. These metrics highlight the scale of the installed consumer base, the strength of Al Fakher’s competitive position, and a sustained focus on product innovation. The category is characterized by strong flavor equity, repeat purchase behavior, and ritualized consumption, which supports the durability of leading brands. Al Fakher therefore provides AIIR with a large recurring consumption base and a premium brand platform capable of supporting line extensions, collaborations, and next-generation product formats over time.

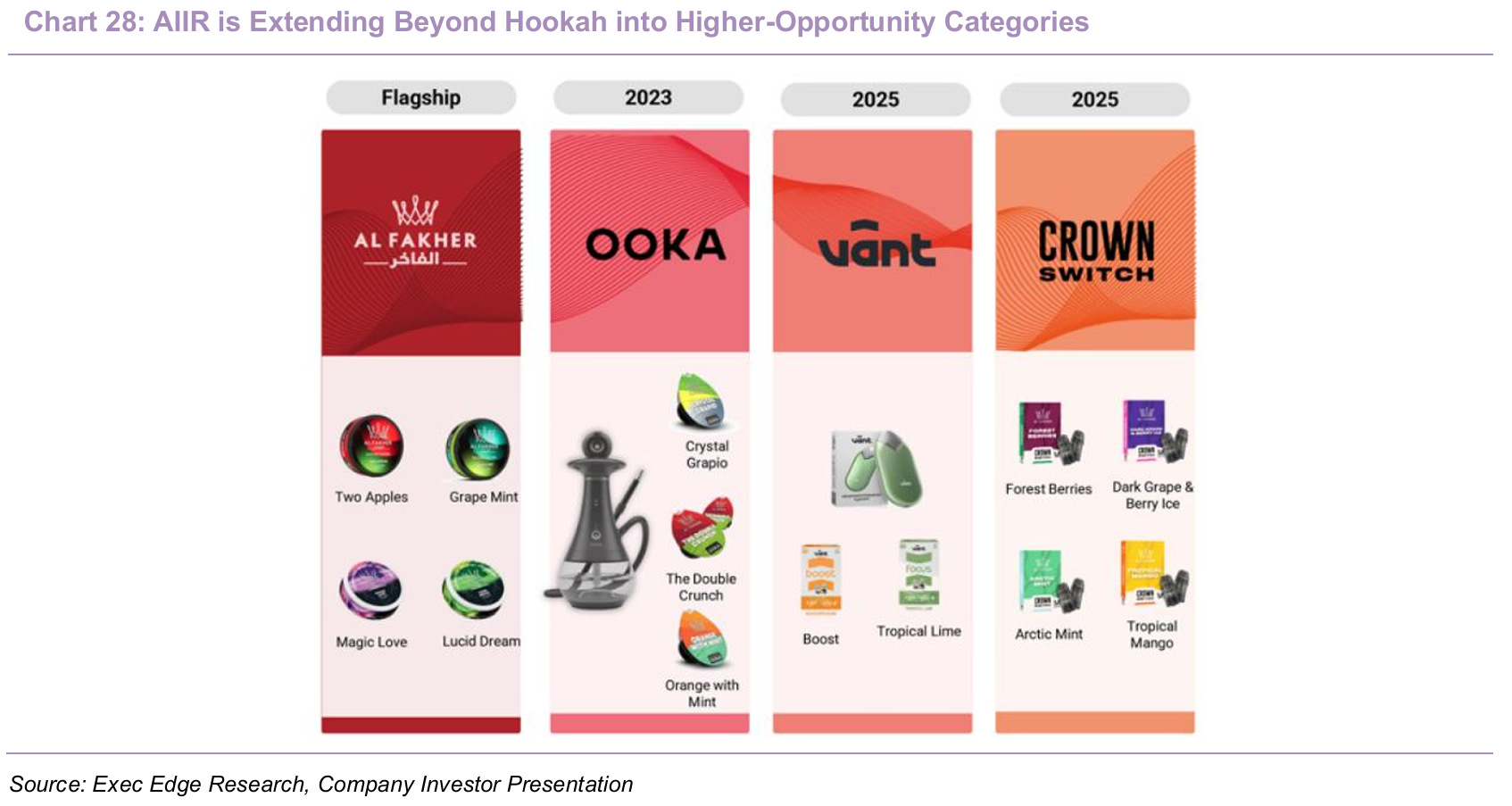

- The company’s portfolio has broadened beyond its heritage core, although flavored molasses continues to account for the large majority of group revenue. Flavored molasses remains the cornerstone of the core business, with AIIR producing multiple pack sizes and operating across a portfolio that includes Al Fakher, Shisha Kartel, Kloud King, and Zødiac. The company also highlights a widening product architecture that includes collaboration-led launches such as Snoop Dogg, tea-based tobacco-free shisha under Zødiac, and value-oriented products such as Al Aseel in Saudi Arabia. The widening mix reflects a deliberate shift beyond a single premium legacy franchise toward a broader portfolio spanning premium, value, non-tobacco, and western lifestyle segments, improving category coverage and expanding pricing and mix levers over time.

- AIIR’s collaboration strategy is a key component of its premiumization playbook, extending Al Fakher beyond its heritage shisha roots into broader, lifestyle-led consumption occasions. Partnerships with culturally relevant brands and personalities act as high-visibility entry points into new markets and consumer segments. The Snoop Dogg collaboration provides a prominent U.S. launch vehicle aligned with music, social occasions, and flavor experimentation, while the Cookies collaboration connects the brand to a well-established lifestyle platform with strong recognition among younger adult consumers. These partnerships are particularly relevant in a flavor- and occasion-led category where brand association can influence trial, menu placement, and willingness to pay for premium blends. For AIIR, collaborations extend beyond marketing into controlled product innovation, enabling portfolio renewal, stronger western-market positioning, and high-visibility limited-edition SKUs that support pricing power and consumer engagement.

- Distribution reach and channel control are emerging as important parts of AIIR’s competitive profile, particularly as the company adds digital assets to a historically wholesale-led model. The company serves 90+ markets and emphasizes the value concentration in lounges and hospitality venues, where a smaller share of category volume can represent a much larger share of consumer spend. AIIR has also assembled digital assets including Hookah.com in North America and Shisha-World in Europe, which serve as important e-commerce and consumer-insight engines. AIIR’s model is therefore extending beyond manufacturing and wholesale distribution into owned demand capture, consumer data, and more direct launch capability. That should improve visibility into consumer preferences, help management react more quickly to flavor trends, and support faster commercialization of new products across markets. Digital ownership also gives AIIR more control over merchandising, pricing architecture, and promotional activity, which is important as the portfolio broadens beyond legacy molasses into adjacent categories. Over time, this hybrid route-to-market model should strengthen AIIR’s competitive position by pairing the scale advantages of a global distribution footprint with the higher-margin and data-rich characteristics of direct digital channels. As adjacent products scale, these assets could become an increasingly important low-friction launchpad for innovation and premium offerings.

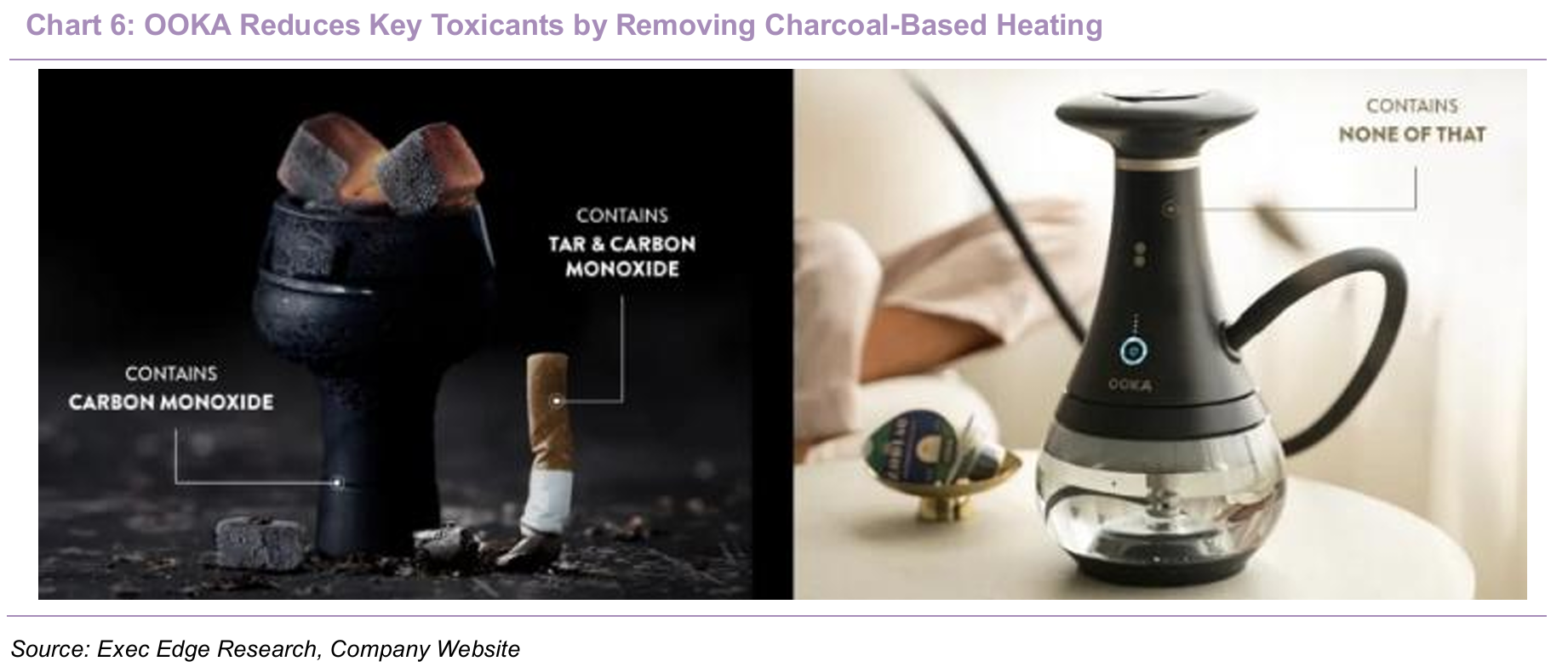

- A key strategic evolution underway is AIIR’s shift from an open consumables model toward a more proprietary, closed-system platform led by OOKA. OOKA is AIIR’s charcoal-free electronic hookah system, built around a proprietary device-and-pod architecture intended to simplify setup, reduce friction, and create more repeatable session quality. AIIR has built 18 patent families around the platform and demonstrates early economics that are materially richer than the core business, with materially higher unit economics relative to traditional hookah products, based on early launch-market data. OOKA represents the clearest pathway for AIIR to capture more value per session, deepen IP protection, and transition from branded consumables toward a device-plus-refill ecosystem. The strategic appeal is not only higher unit economics, but also stronger control over the consumer experience, more consistent product quality, and the potential for recurring refill revenues once users enter the system. This model is structurally more defensible over time and less exposed to purely price-based competition. That said, adoption will still need to prove durable at scale, making OOKA the key premiumization driver and future margin lever.

- The public listing expands AIIR’s strategic flexibility and provides a platform for adjacent category expansion. The company has consistently framed itself as cash generative and largely self-financing, while also highlighting a next phase that includes vaping, nicotine pouches, and nicotine and non-nicotine inhalation formats, including functional applications. The company conducted a controlled retail pilot for VANT in November 2025 in New York City and Madrid, and also launched Al Fakher nicotine pouches in the Middle East and the U.S. The strategy pairs the cash flows and brand equity of Al Fakher with a broader product roadmap that expands TAM and diversifies the model beyond traditional shisha. Near-term execution is likely to focus on scaling OOKA, expanding nicotine pouch distribution, validating VANT, and leveraging the public listing to support broader geographic and product expansion.

- AIIR’s operating footprint combines owned manufacturing, third-party production, and centralized IP management, which together support global scale with a relatively asset-light structure. The company operates production sites in the UAE and Poland, while also using licensed third-party manufacturing in markets including Egypt, Iraq, Lebanon, Jordan, and Malaysia, supported by leased warehouses in Poland, Germany, and the UAE. This setup provides a diversified supply base and some ability to shift production across facilities, which is important in a category where continuity of supply, regulatory compliance, and local market responsiveness all matter. As of December 31, 2025, AIIR employed 885 people globally, including 177 employees in Dubai, with the workforce concentrated across MEAA, Europe, and the Americas. Intellectual property is a key operational pillar, with 175 patent cases across 26 patent families, 71 industrial design registrations and applications, and 544 registered trademarks, which should increasingly support product differentiation, supply-chain control, and premiumization over time.

Right-to-Win

Brand, Innovation, and Execution Strength Underpin a Defensible Business Model

- AIIR’s right-to-win is rooted in a combination of category leadership, durable demand characteristics, and capabilities that are difficult to replicate at scale. The company benefits from Al Fakher’s brand strength and share leadership, participation in a stable and attractive category, and a growing innovation platform led by OOKA. These advantages are reinforced by regulatory know-how, strong cash generation, and a management team with relevant experience across tobacco, consumer brands, and device-led product development. This combination provides a credible foundation for defending the core business while extending into adjacent formats. We discuss AIIR’s moat elements in detail below.

- AIIR’s strong position and scale in the shisha tobacco category is difficult to match and sits at the core of its moat. This positioning is particularly relevant in a ritual-led, flavor-sensitive market where availability, familiarity, and repeat purchase reinforce each other over time. Al Fakher remains at the center of that advantage. The brand traces back to 1999, serves an estimated ~14 million home consumers, supports more than 2.5 million sessions per day, and underpins a system that AIIR says translates into roughly ~1 billion hookah servings per year. The brand also owns 3 of the 5 best-selling flavors globally, reflecting the importance of flavor consistency and brand trust in a category driven by ritual and repeat consumption. Scale in this setting supports stronger shelf presence, broader lounge penetration, and more efficient new product rollout, as consumers and venue operators often default to recognized, proven labels rather than experiment with regional alternatives.

- AIIR’s leadership is also evident at the share level, reinforcing its position as a scaled category leader rather than simply a large participant. The company indicates 36%-44% global market share in markets where it operates, excluding Russia and Turkey, and notes that its scale is larger than the next four competitors combined, while also pointing to >50% share in key geographies including the U.S. Leadership in a fragmented category tends to compound, as scale supports procurement, distribution, and marketing efficiency, which in turn improves visibility and availability and reinforces share. While local and regional brands will remain relevant in certain markets, AIIR has reached a threshold where brand recognition, installed consumer habits, and channel relationships create meaningful barriers to displacement. This combination provides a durable foundation for defending the core business while extending into adjacent formats and price tiers.

- AIIR operates in a structurally stable category, supporting the durability of its core profit pool while providing capacity to fund growth initiatives. The company’s target market is expected to grow at a 3.6% retail sales CAGR and 1.6% volume CAGR between 2025 and 2030, based on Arthur D. Little data cited in the company’s investor presentation. While this does not represent a hypergrowth profile, it is sufficient in a branded, flavor-led category where pricing, mix, and premiumization drive value creation more than volume expansion. This allows AIIR to compound earnings within a culturally embedded and regionally resilient market, while using cash flows from the core flavored molasses business to fund newer categories and device-led innovation.

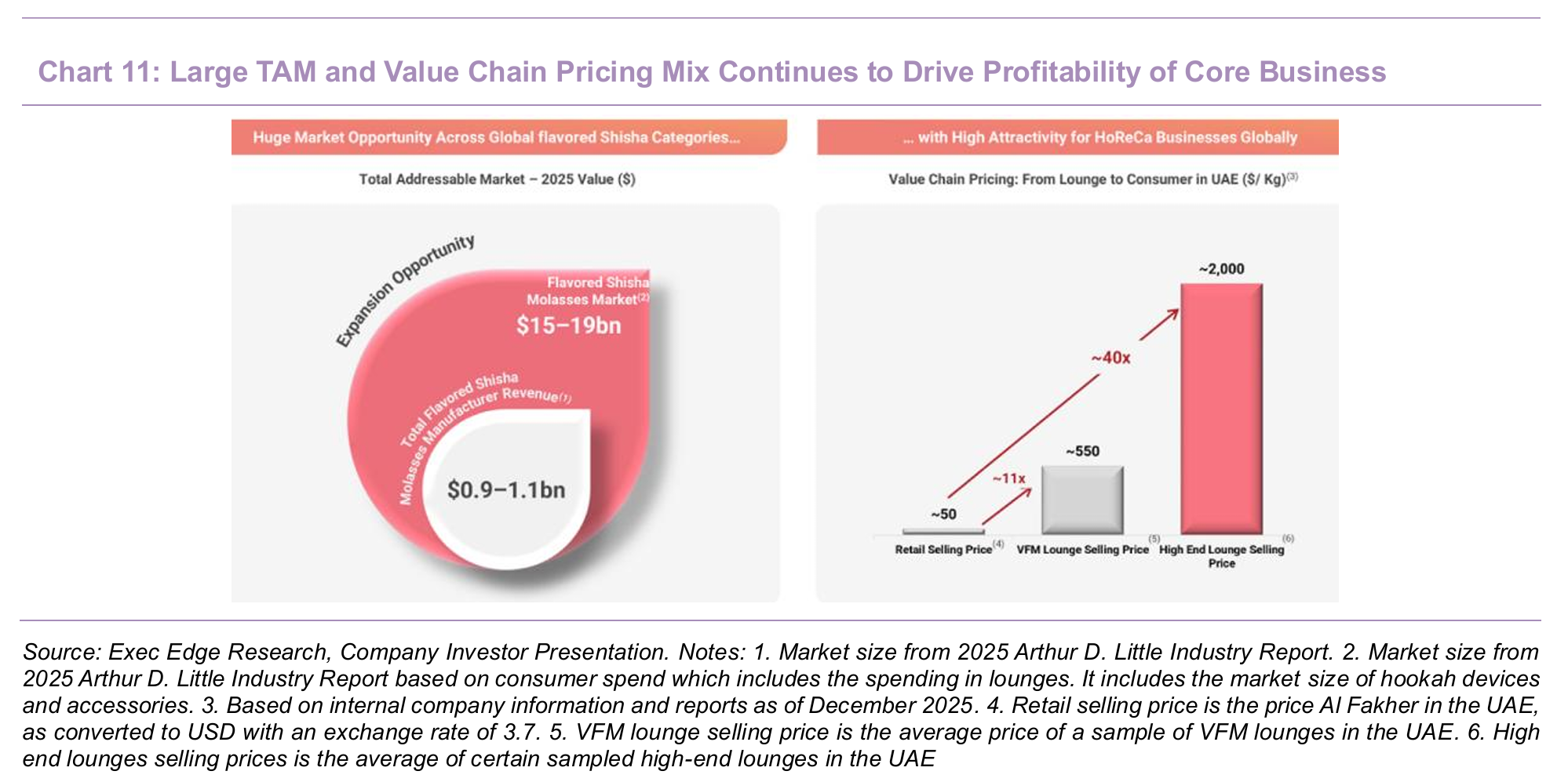

- The shisha value pool is heavily skewed toward downstream consumption, creating a large monetization gap relative to manufacturer revenues. Arthur D. Little estimates a $15-$19 billion global flavored hookah molasses consumer-spend opportunity in 2025, compared with only $0.9-$1.1 billion at the manufacturer level. This reflects significant value capture within lounges and hospitality settings. A UAE value-chain example illustrates this dynamic: flavored molasses priced at ~$50 per kg at retail can translate to ~$550 per kg in value for-money lounges and ~$2,000 per kg in high-end lounges, implying ~11x and ~40x value uplift, respectively. This gap highlights the importance of brand strength, channel access, and premium positioning in capturing a greater share of the downstream value pool over time.

- AIIR’s scale and channel presence position it to benefit disproportionately from this value concentration in premium consumption environments. While only ~35% of volume is consumed in lounges, these venues account for roughly ~85% of category value, underscoring the importance of on-premise visibility and brand preference. In contrast to fragmented or declining categories that drive price competition, shisha demand remains anchored in social, venue-led consumption, supporting more rational pricing and stronger returns on brand investment. AIIR’s leadership and distribution footprint enhance its ability to secure placement in these high-value channels, reinforcing both pricing power and the durability of its core business. In this context, steady category growth becomes a structural advantage, reducing execution risk while enabling the company to fund innovation from internally generated cash flows.

- Strong product innovation gives the company a more credible path to premiumization than a traditional molasses supplier and raises the barrier for smaller competitors attempting to follow. The clearest expression of that lead is OOKA, a charcoal-free electronic hookah system built around a device-and-pod architecture designed to simplify setup, improve consistency, and reduce the friction historically associated with traditional hookah use. The economics are materially richer than the legacy business, with launch-market data showing ~20x revenue per kilogram and ~15x gross profit per kilogram relative to traditional hookah products in the U.S., UAE, and Germany. AIIR has invested more than $125 million in research and development, and its innovation pipeline already extends beyond OOKA into vaping, nicotine pouches, and VANT, indicating a broader innovation platform rather than a single product extension.

- AIIR’s innovation advantage is supported by a meaningful IP portfolio and a science-led commercialization model, making the moat more durable than simple first-mover status. The company discloses 175 patent cases across 26 patent families, including a concentration around OOKA, alongside 71 industrial design registrations and applications and 544 registered trademarks. Device-led premiumization is more defensible when reinforced by patents, design registrations, and proprietary formulations rather than marketing alone. The broader strategic implication is that AIIR can monetize more than flavor and brand, including convenience, repeatability, and controlled-system economics, thereby shifting the business mix toward higher-value formats over time. While execution risk remains around consumer adoption and scale-up, AIIR has already assembled a more developed technical, scientific, and IP infrastructure than most category peers, which should support the conversion of innovation into a repeatable source of moat expansion.

- Regulatory expertise is a core moat element for AIIR, protecting both its legacy business and its innovation agenda across a broad product portfolio. The company’s management team has deep experience operating in highly regulated tobacco and consumer categories, and it has built a science program to support product development, toxicology, and regulatory engagement. In traditional hookah, the category’s social and occasional use profile is relevant, with hookah historically treated differently from cigarettes in some jurisdictions. In the U.S., there are state and local settings where flavored shisha benefits from carve-outs from broader flavored tobacco restrictions. AIIR also highlights that youth experimentation with hookah has tended to screen lower than more accessible inhalation formats, supporting a more differentiated regulatory framework than a generic “tobacco” label might imply. On the core side, regulatory know-how supports distribution continuity, licensing, and compliance across 90+ markets. On the innovation side, it enhances the company’s ability to commercialize OOKA, nicotine pouches, and adjacent formats, with a clearer understanding of how claims, ingredients, and device design affect regulatory treatment. While smaller brands may compete on price or local relevance, they are less likely to match AIIR’s combination of scientific infrastructure, regulatory engagement, and multinational compliance capabilities. Although regulatory outcomes remain market-specific and uncertain, AIIR’s expertise lowers execution risk and supports the durability of both the core franchise and the next-generation product roadmap.

- Financial self-sufficiency, supported by strong cash generation, provides AIIR with greater strategic flexibility than many earlier-stage nicotine or device peers that remain dependent on external funding. In 2025, AIIR generated $399.7 million in revenue, $139.3 million of adjusted EBITDA, $46.8 million in profit, and $115.9 million of net cash generated from operating activities. The company has a history of strong cash conversion, with multi-year operating cash generation averaging more than $110 million annually, and net debt/adjusted EBITDA of 2.1x. This profile supports sustained investment in OOKA, adjacent categories, marketing, and selective M&A, with a meaningful portion funded internally.

- Financial strength enhances both resilience and execution capacity. A strong cash profile can support product launches, inventory investment, scientific work, regulatory processes, and partnership development without requiring dilutive financing or a short-term operating posture. It also provides flexibility to manage category volatility, working capital, and pursue tuck-in opportunities such as NameLess from a position of control. The balance sheet therefore functions not only as a defensive attribute, but as an enabler of innovation and expansion, particularly relative to peers with weaker cash generation. While leverage and capital allocation will require ongoing monitoring as the company scales, the current financial profile strengthens AIIR’s ability to fund growth while maintaining discipline.

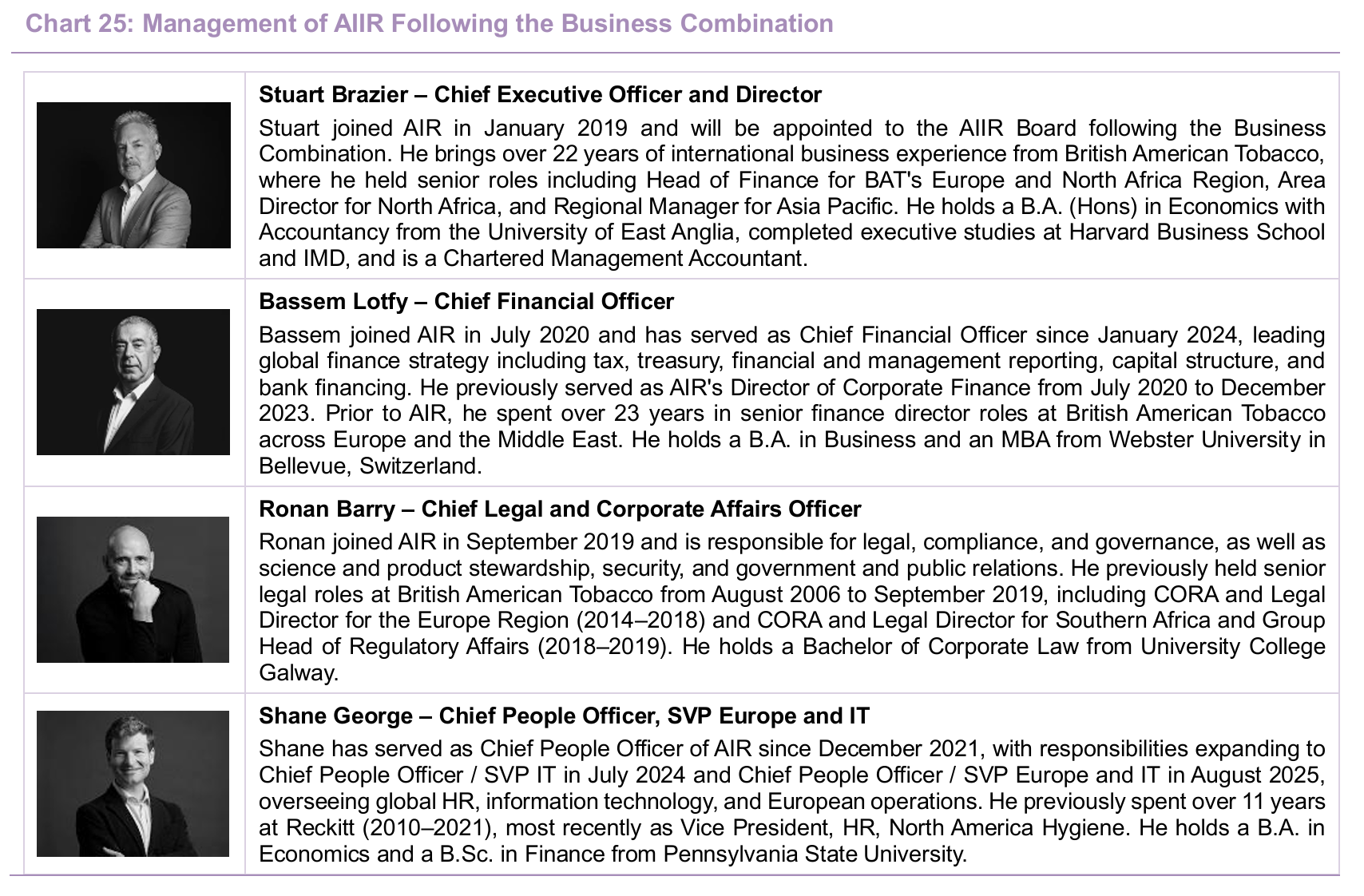

- AIIR’s management team combines tobacco regulatory depth, consumer-brand execution, device engineering, and public-market readiness in a way that aligns closely with its multi-category strategy. CEO Stuart Brazier’s two decades at BAT support the transition to a disciplined, multinational platform, while CFO Bassem Lotfy’s background in large-scale tobacco finance underpins capital allocation, financial controls, and cash conversion as AIIR balances core profitability with investment in OOKA and new categories. Ronan Barry’s legal and corporate affairs experience is relevant given AIIR’s presence across 90+ markets and expansion into more regulated adjacent formats. On the innovation side, leadership with Dyson backgrounds across engineering and new growth supports device design, user experience, and commercialization of inhalation platforms, while consumer brand and supply-chain expertise from companies such as Reckitt, Kellogg’s, Philips, and GE strengthens portfolio expansion and operational scale. Overall, the leadership team is aligned with the key execution priorities: defending the core franchise, navigating regulation, scaling OOKA, and expanding into adjacent categories.

- AIIR’s governance is supported by Kingsway-aligned board leadership, with Chairman Tamir Saeed providing capital allocation oversight alongside Kingsway’s position as the company’s largest shareholder. This alignment is particularly important as AIIR enters public markets with a concentrated ownership structure, placing greater emphasis on capital discipline and long-term value creation. Taken together, management and governance are structured to support execution across regulated consumables, branded FMCG, and device-led innovation.

- See the Management Team section for brief biographies of the leadership team.

Industry Trends and Company Positioning

Shisha is Evolving into a Stable, Value-Led Global Lifestyle Category

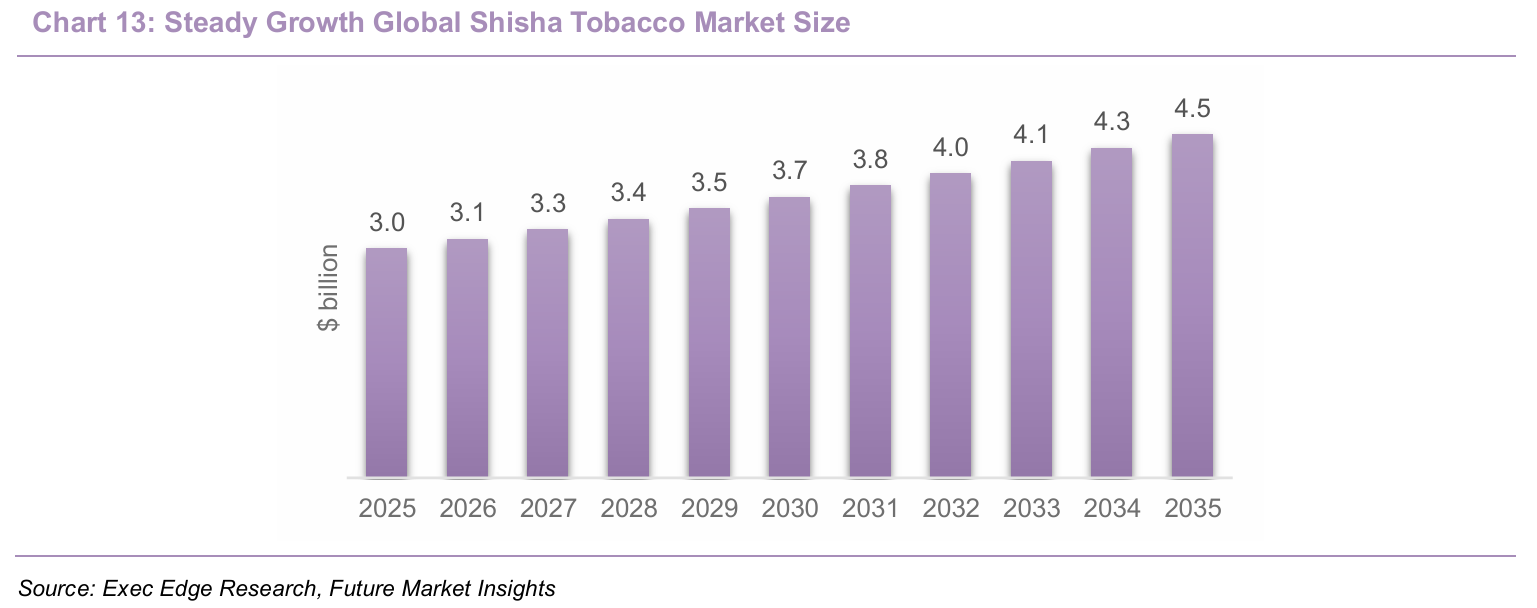

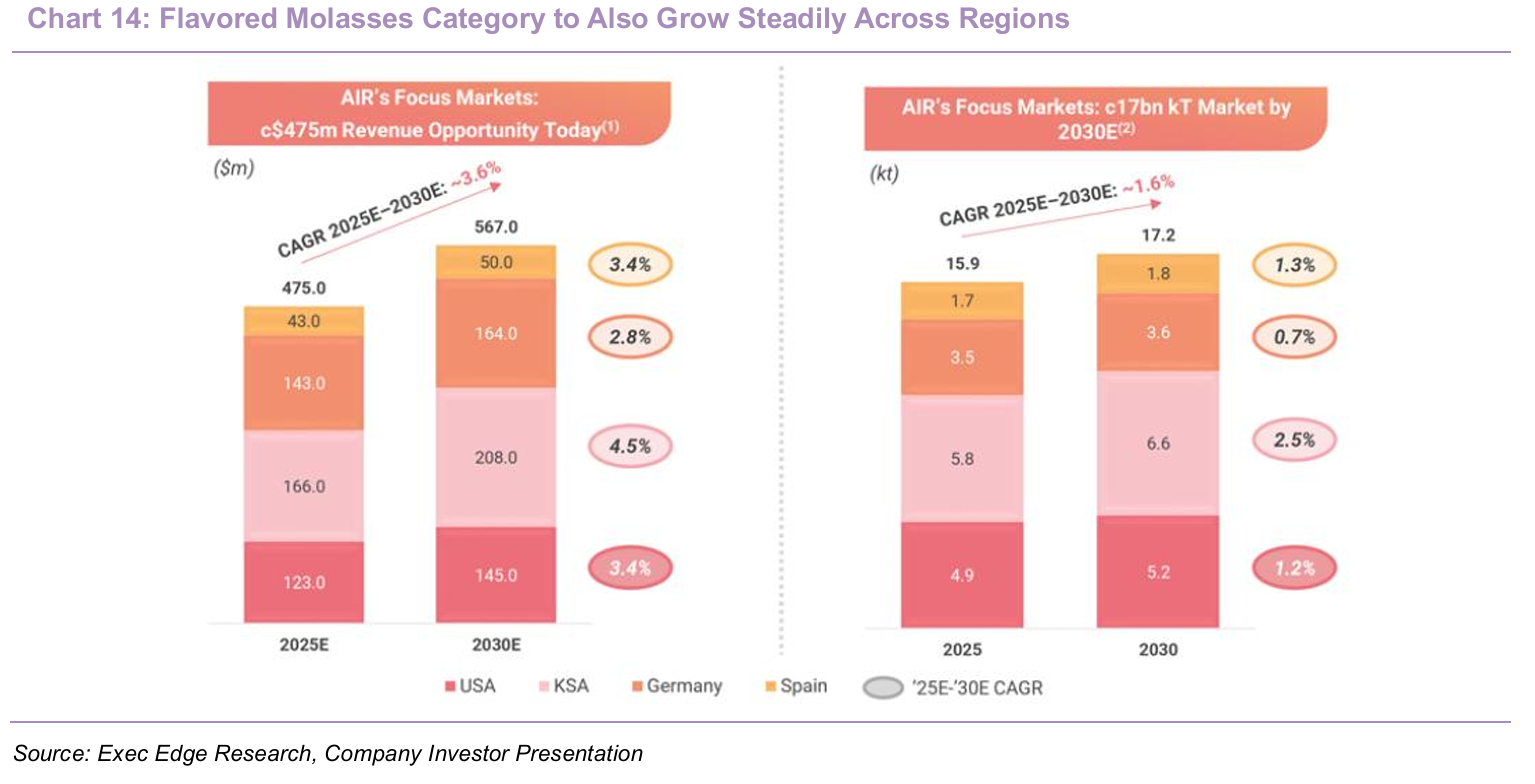

- Shisha is emerging as a steady, value-led global category, where growth is driven more by pricing, premiumization, and mix than by consumption frequency. Arthur D. Little data cited in AIIR’s investor presentation points to 3.6% retail sales CAGR between 2025-2030 for flavored molasses category within the broader global shisha tobacco market. This market is expected to grow from $475 million in 2025 to $567 million by 2030. Over the same period, volume is projected to increase at 1.6% CAGR, from 15.6 kT to 17.2 kT, implying value growth outpacing volume. This supports a favorable backdrop for branded players to compound through pricing and mix. Future Market Insights, which tracks the growth of the larger global shisha tobacco market, expects it grow from $3.0 billion in 2025 to $4.5 billion by 2035, implying a 4.1% CAGR. Taken together, these estimates point to a structurally stable category where scale, brand strength, and channel access matter more than volume acceleration.

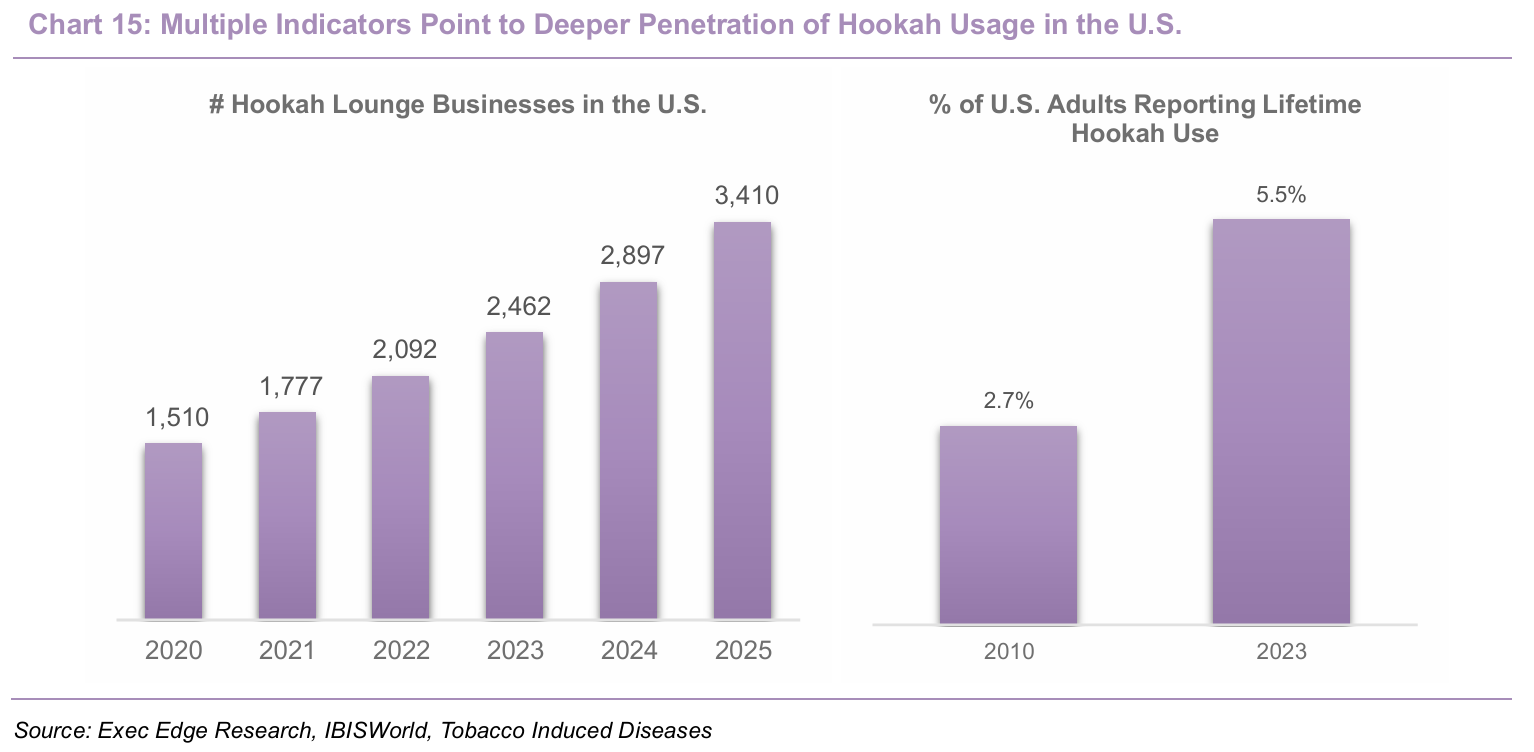

- Lounge and café expansion is increasing category visibility and reinforcing shisha as a social, experience led consumption occasion. The growth story is not limited to market-sizing forecasts, as lounge and café infrastructure also points to expanding category visibility in western markets. IBISWorld estimates 3,410 hookah lounge businesses in the U.S. in 2025, with the number of businesses growing at a 17.7% CAGR between 2020 and 2025 and the industry’s market size growing at a 17.9% CAGR over the same period. Hookah use has grown in the U.S. in recent years as lounges and cafés offering flavored smoking have become more common and are frequented by younger urban consumers. This matters because shisha demand is shaped as much by venue experience as by product availability. Unlike cigarettes or personal vaping, hookah is often consumed in a shared setting where service, atmosphere, and brand familiarity influence repeat behavior. We view lounge growth as a key indicator of category health, as venues both normalize the ritual for new consumers and reinforce brand preference in premium settings where consistency and reliability matter.

- Consumer data reinforces that shisha remains an occasional, experience-led format, with expanding familiarity but stable usage intensity. The investment case is not predicated on rising consumption frequency, but on expanding familiarity and lifetime trial within an inherently occasional-use category. A 2025 study in Tobacco Induced Diseases found that the weighted percentage of U.S. adults reporting lifetime hookah use increased from 2.7% in 2010 to 5.5% in 2023, while current use remained relatively stable at 0.3%–0.6% across the period. This is consistent with AIIR’s positioning of shisha as a social ritual rather than a daily-consumption format. CDC data also shows nuance: among U.S. young adults aged 19–30, past-12-month hookah use declined from 20.6% in 2014 to 8.0% in 2022, which suggests market growth should not be framed as broad-based usage acceleration. Instead, the opportunity lies in higher-value monetization of a known, occasional-use category through premium venues, flavors, and branded formats. This dynamic supports value growth driven by mix, pricing, and premiumization within an inherently occasional-use category.

- This industry structure directly reinforces AIIR’s positioning as a scaled, brand-led operator in a value driven category. The trend should benefit AIIR because Al Fakher provides a strong brand platform in a category where flavor trust, lounge visibility, and repeat ritual drive demand. A market growing at a mid-single-digit value CAGR does not require an aggressive volume inflection for AIIR to create value; instead, the company can compound through pricing, premiumization, geographic deepening, and channel penetration. AIIR’s 90+ market footprint, leading flavor portfolio, and OOKA roadmap position it to monetize steady category growth while using the core business to fund innovation.

Charcoal-Free Systems and Nicotine Alternatives Broaden AIIR’s Addressable Market

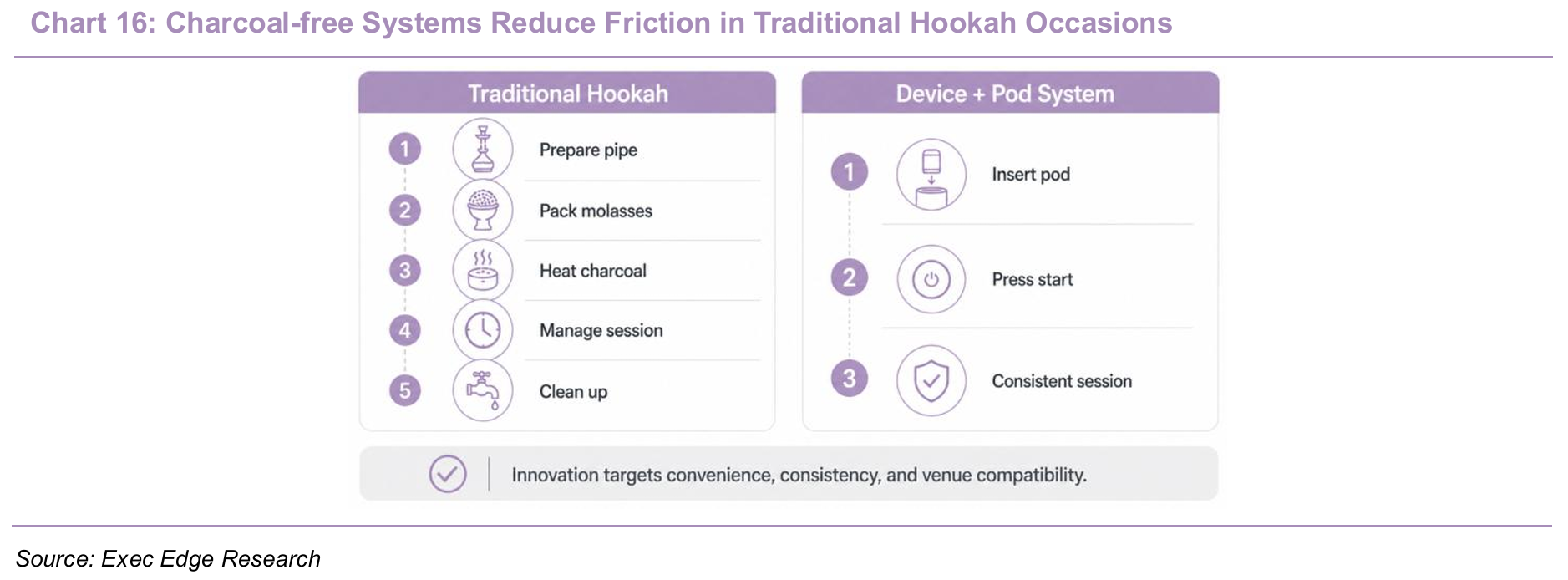

- Charcoal-free systems are lowering structural barriers to adoption by reducing friction, improving consistency, and expanding venue compatibility. Traditional hookah remains a social and ritual-led category, but its preparation model introduces constraints that can limit adoption outside specialist settings. Consumers typically require multiple components, heating time, cleanup, and user skill to produce a consistent session, while charcoal adds operational challenges including heat, ash, odor, ventilation needs, and handling risk. Device-led systems address these limitations without fundamentally altering the ritual, making consumption more accessible, repeatable, and compatible with indoor and premium hospitality environments. Scientific literature also supports this design direction: studies cited by the American Chemical Society indicate that charcoal contributes materially to harmful by products such as polycyclic aromatic hydrocarbons and carbon monoxide, while also noting that electric systems require product-specific evaluation. The focus is not on health claims, but on a shift toward more standardized, controlled, and lower-friction consumption formats.

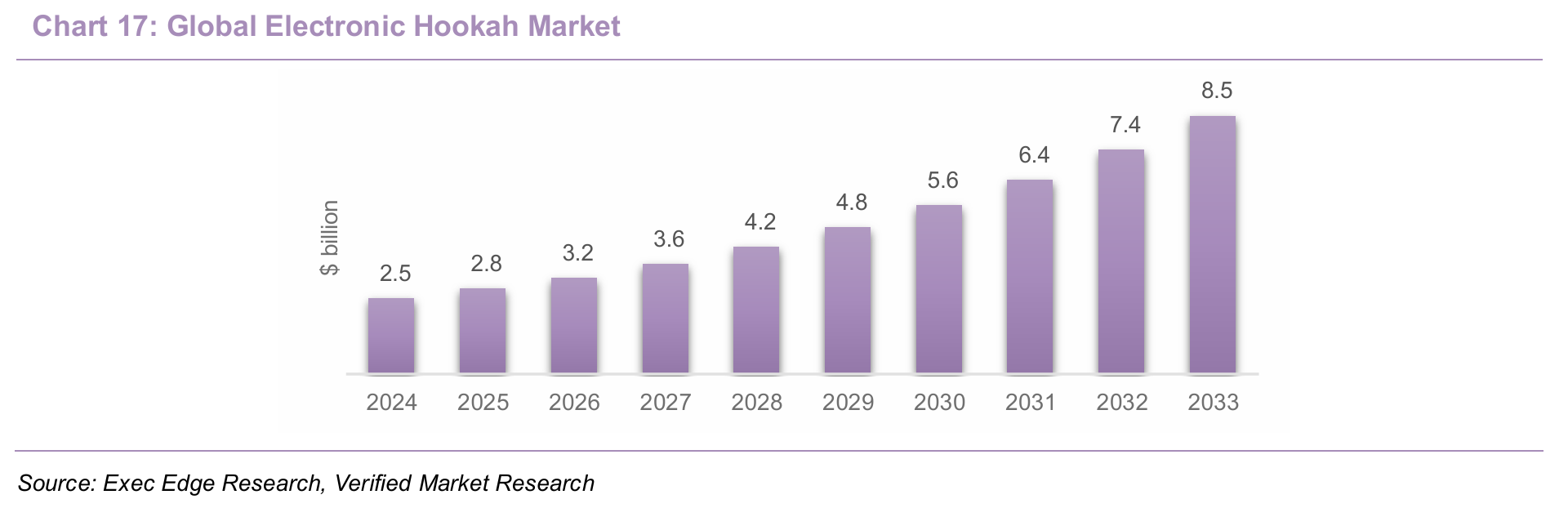

- Electronic hookah formats are scaling as consumers shift toward convenience, customization, and device led consumption. Verified Market Reports estimates the global e-hookah market at $2.5 billion in 2024, growing to $8.5 billion by 2033, implying a 15.2% CAGR. The market is segmented across product types, flavors, distribution channels, and usage occasions, reinforcing that e-hookah represents a broader consumption format rather than a simple replacement device. Key drivers include improved flavor delivery, customizable experiences, digital marketing, and appeal among younger consumers. While definitions can overlap with vaping and other electronic inhalation formats, these segments should be viewed as adjacent and partially overlapping rather than directly comparable, with the directional signal remaining clear: demand is shifting toward products that reduce preparation burden, expand flavor and design flexibility, and integrate more naturally into digital and specialty-retail ecosystems. This directly supports the strategic positioning of OOKA as a controlled device and-pod system designed to capture these evolving consumption preferences.

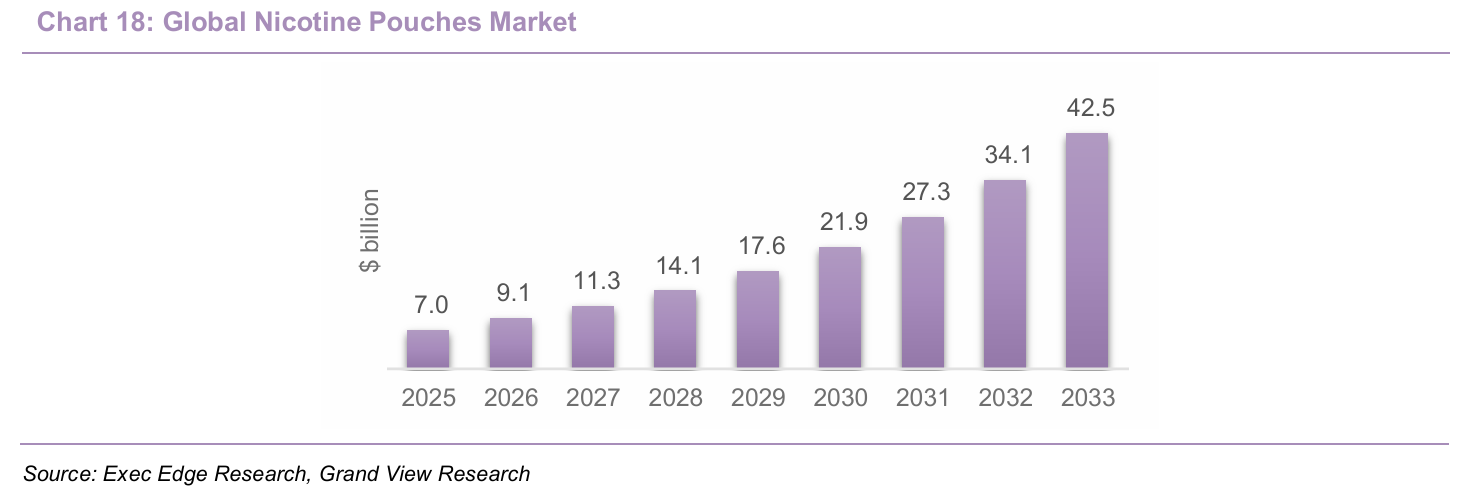

- The rise of nicotine alternatives is expanding the industry beyond traditional combustible formats, creating a larger and faster-growing innovation landscape. Grand View Research estimates the global nicotine pouch market at $7.0 billion in 2025, growing to $42.5 billion by 2033, implying a 24.7% CAGR, with similarly strong growth projected in the U.S. This shift is already visible at scale among incumbents such as Philip Morris International, where smoke-free products accounted for 43% of total net revenues in 1Q26 and continue to grow at a materially faster pace than the legacy combustible portfolio. PMI’s international smoke-free segment delivered net revenue and gross profit growth of 24.7% and 28.6% y/y, respectively, underscoring the acceleration toward multi-format nicotine platforms. The implication is a structural transition toward integrated nicotine ecosystems spanning consumables, devices, oral products, flavors, and controlled distribution. For AIIR, this supports the strategic expansion beyond legacy shisha into nicotine pouches and functional inhalation, while reinforcing the importance of compliance and disciplined, adult-focused commercialization.

- AIIR’s diversification strategy is aligned with these industry shifts, positioning the company to expand both its addressable market and value capture. The company is reducing hookah friction through OOKA, extending Al Fakher into nicotine pouches, piloting VANT in functional inhalation, and leveraging digital platforms such as Hookah.com and Shisha-World to strengthen channel control. OOKA is particularly important, with launch-market data indicating roughly 20x revenue per kilogram and 15x gross profit per kilogram versus traditional hookah products, highlighting the potential for device-led premiumization to materially shift mix and profitability. The opportunity extends beyond TAM expansion to include recurring consumable economics, improved consumer data capture, and a more defensible product architecture. Industry trends are increasingly supportive of AIIR’s transition from a legacy molasses supplier to a broader inhalation platform.

Digital Channels are Emerging as Key Enablers in a Fragmented, Flavor-Led Category

- Digital channels are becoming increasingly important in hookah, given the category’s fragmented structure, SKU complexity, and reliance on flavor discovery. Traditional hookah commerce has relied on lounges, specialty retailers, local distributors, and regional brands, which can limit assortment visibility and real-time insight into consumer preferences. Online portals address these constraints by aggregating flavors, devices, accessories, reviews, and replenishment into a single consumer-facing destination. Industry sources including Research and Markets and The Insight Partners highlight online retail as a growing distribution channel across hookah products and flavors. This matters because hookah is a flavor-led, accessory-heavy ecosystem where consumers typically browse across multiple blends, devices, and components prior to purchase. The breadth of offerings across platforms such as Hookah.com and TheHookah.com illustrates how digital aggregation improves discovery and purchasing efficiency. Hookah.com’s B2B portal lists bulk shisha tobacco, master cases, bowls, hoses, accessories, nicotine pouches, and multiple brands, while TheHookah.com markets itself around a broad selection of hookahs, shisha flavors, accessories, and charcoals. AIIR’s own data further reinforces this positioning, with SEMrush-based traffic share for Hookah.com in the U.S. and Shisha-World in Germany, alongside Google Search Console data from December 2024 to December 2025, indicating that owned portals can function as both demand capture and consumer insight engines in this fragmented category.

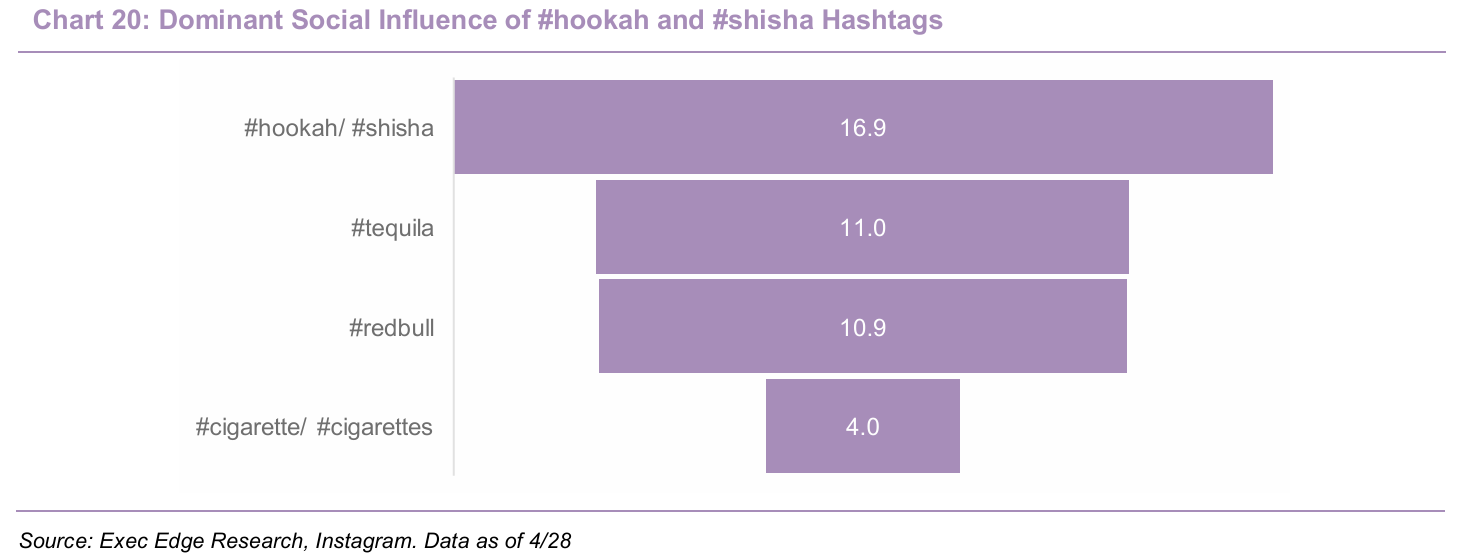

- Social media is reinforcing hookah’s positioning as a lifestyle-led category, expanding discovery and engagement beyond traditional retail channels. Instagram data as of April 28, 2026 shows ~17 million hashtag uses for #shisha / #hookah, exceeding comparison categories such as #tequila and #redbull (~11 million) and #cigarettes (~4 million). Academic research also supports this dynamic: a 2026 Nicotine & Tobacco Research study analyzing 299,544 U.S. Twitter/X posts from 2021–2023 found that 57% of posts carried positive sentiment, with themes centered on lounges, flavors, and social use. This positions digital platforms as both a discovery layer and a commercialization channel for new flavors, collaborations, and device-led formats.

- AIIR is structurally positioned to capture this shift through ownership of scaled, category-specific digital assets. Hookah.com in North America and Shisha-World in Europe provide direct visibility into consumer preferences, traffic trends, and assortment performance, enabling faster feedback loops on product launches and collaborations. These platforms should support commercialization of OOKA consumables, Al Fakher nicotine pouches, VANT, and acquired brands such as NameLess. The strategic value extends beyond online sales to include faster learning cycles, improved merchandising control, and more effective monetization of digitally driven demand.

Regulatory Differentiation is Driving Competitive Advantage in Social Inhalation

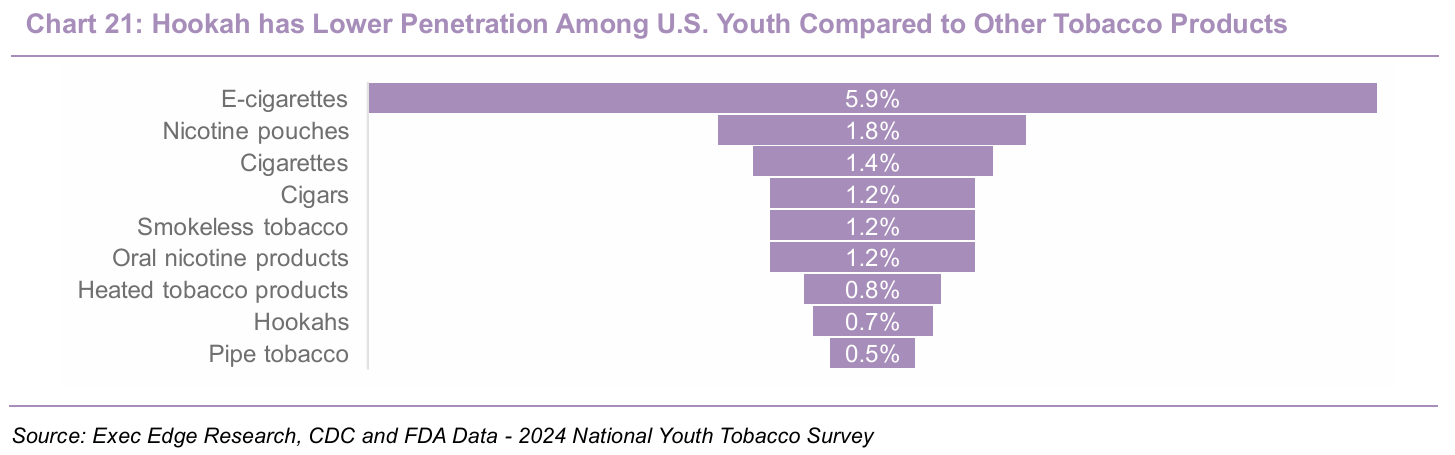

- Regulation is tightening across tobacco and inhalation formats, but shisha is increasingly being treated through category-specific rules rather than a single blanket framework. In the U.S., the FDA brought hookah tobacco under federal oversight through the 2016 “deeming” rule, meaning manufacturers are regulated across manufacturing, importing, packaging, labeling, advertising, sale, and distribution. The FDA also applies nicotine warning requirements to covered tobacco products, with compliance dates beginning in 2018, making packaging and claims discipline a core operating requirement for the category. At the same time, usage data supports a differentiated regulatory profile relative to more accessible formats. CDC’s 2024 National Youth Tobacco Survey showed current hookah use at 0.7% of middle and high school students, below e-cigarettes at 5.9%, nicotine pouches at 1.8%, cigarettes at 1.4%, and cigars at 1.2%. This creates a nuanced regulatory backdrop: hookah is regulated within the tobacco framework, but its lower youth-use prevalence and more social, occasion-based consumption profile support differentiated policy treatment relative to higher-frequency or youth-skewing products.

- Across major AIIR markets, regulation is increasingly product-specific, creating both compliance burdens and structurally protected lanes for scaled operators. California provides a clear example: while the state restricts most flavored tobacco products, the California Department of Public Health allows flavored shisha or hookah tobacco to be sold in licensed stores that restrict entry to individuals aged 21+ at all times. This distinction is important given that flavors remain central to hookah’s consumer proposition. In the EU, the Tobacco Products Directive requires cigarettes, roll-your-own tobacco, and waterpipe tobacco to carry combined health warnings covering 65% of the front and back of packages, with Germany applying waterpipe-specific packaging and warning rules within this broader framework. Germany also illustrates regulatory evolution: a 2022 rule limiting shisha tobacco packs to 25g was lifted from July 1, 2024, after criticism that it encouraged illicit-market activity. Tobacco Reporter noted that the government had expected €155 million of additional tax revenue but instead saw tax income decline as the black market expanded. This suggests that regulation in some markets is moving toward more pragmatic, product-specific calibration rather than a uniform tightening trajectory.

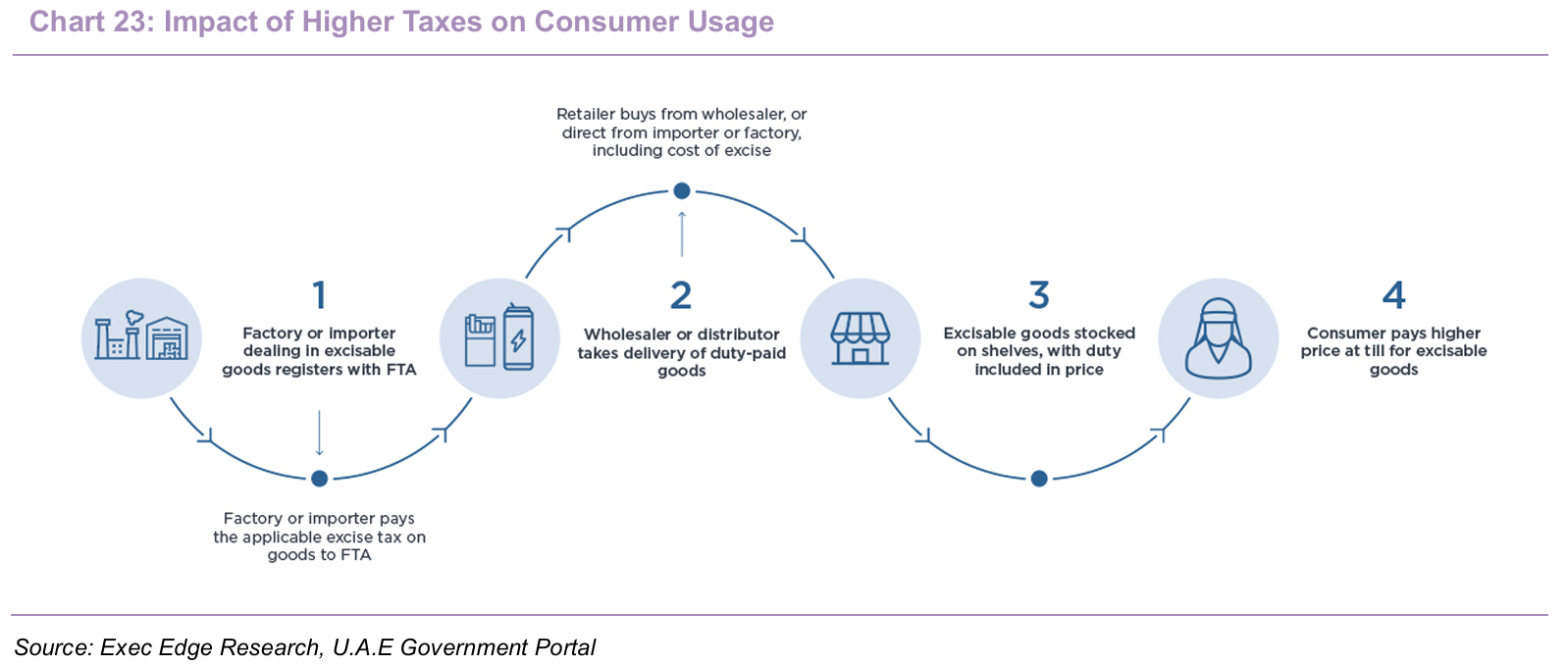

- Gulf markets highlight the dual role of regulation as both a cost burden and a structural barrier to entry. The UAE applies a 100% excise tax to tobacco products, electronic smoking devices, and related liquids, while Cabinet Resolution No. 55 of 2019 establishes a minimum excise price mechanism that includes AED 0.1 per gram for waterpipe tobacco and similar ready-to-use products. Saudi Arabia similarly applies a 100% excise tax to tobacco products, with PwC noting the Excise Tax Law became effective on June 11, 2017, and WHO FCTC materials also describing the kingdom’s 100% tax implementation. Saudi regulation has continued to tighten at the retail level, including restrictions on proximity to schools and mosques reported in 2025. The implication is that regulatory intensity is becoming a structural feature of the category, making scale, compliance systems, tax discipline, and market-by-market regulatory expertise increasingly important. This dynamic favors operators that can absorb compliance costs, manage excise complexity, and maintain consistent product stewardship across jurisdictions.

- Regulatory complexity is increasingly emerging as a competitive moat, reinforcing the advantages of scale, compliance capability, and operating experience of leaders like AIIR. The company operates across 90+ markets, is supported by a management team with tobacco regulatory expertise, and is building a portfolio of science-led products including OOKA and VANT, making regulatory execution central to its strategy. Category specific rules, flavor exemptions, and adult-only retail channels can preserve commercial access for compliant operators, while higher warning, tax, and authorization requirements raise barriers for smaller competitors. In this context, regulation functions not only as a risk factor, but as a structural enabler of durable market share and long term competitive positioning.

- Taken together, industry structure, format evolution, digital channel development, and regulatory dynamics are reinforcing a category where scale, brand strength, and execution capability increasingly define long – term winners – positioning AIIR to benefit from both structural stability and evolving growth vectors.

Middle East Developments Introduce Near-Term Energy and Supply-Chain Volatility

- The 2026 escalation of the Iran–Israel–U.S. conflict has shifted regional risk from a background overhang to an active disruption. As of April 30, the Strait of Hormuz had been effectively constrained for ~60 days following Iran’s declaration to close the strait, shutting in ~20% of global oil and LNG shipments and reducing transit to a fraction of the 130+ daily crossings seen pre-conflict. Conditions have not normalized despite intermittent peace headlines. Reuters noted that U.S.–Iran peace hopes were offset by continued shipping constraints, while Middle Eastern crude and condensate supply losses reached 496 million barrels by mid-April. As of April 30, oil prices were still rising, with the brent crude oil reaching $114/ Bbl, as Hormuz disruption outweighed other supply developments. The World Bank baseline assumes the most acute disruption ends in May, with shipping gradually returning toward pre-war levels by October.

- The Strait of Hormuz remains the core transmission channel, linking the conflict to global energy, freight, and inflation dynamics. The IMF estimates 25%–30% of global oil and ~20% of LNG flows through Hormuz, making this a global energy shock rather than a regional issue. The World Bank forecasts energy prices to rise 24% in 2026, with Brent averaging $86/bbl under its baseline and potentially reaching $115/bbl if disruption persists and recovery slows. The same update projects a 16% increase in overall commodity prices and a 31% rise in fertilizer prices, reflecting spillover from higher natural gas and urea costs. The IMF highlights energy prices, supply chains, and financial markets as key transmission channels, with large energy importers in Asia and Europe most exposed. For Middle Eastern economies, the impact is mixed: exporters benefit from price strength, while logistics disruption, airspace constraints, freight inflation, and weaker travel or trade activity can pressure non-oil sectors, including consumer, hospitality, and distribution.

- AIIR’s exposure is manageable but real, primarily through supply continuity, freight costs, and working capital. The company is headquartered in Dubai, operates production in the UAE and Poland, uses licensed third party manufacturing across several markets, and sells into the UAE and Saudi Arabia, making regional logistics stability relevant to both supply and demand. Disruption may require alternative land routes, increasing transport costs, extending lead times, and delaying shipments, particularly if Gulf sea routes or nearby air corridors become less reliable. Margin impact would likely come through higher freight, fuel, warehousing, and working-capital costs rather than an immediate demand shock, although premium lounge traffic in the Gulf could soften if tourism and hospitality activity weaken. Mitigation comes from AIIR’s scale and diversified footprint: UAE and Poland production, licensed manufacturing across markets, and distribution in 90+ countries provide greater flexibility than smaller, single-market operators. Even so, Middle East geopolitics remains a key variable for route availability, freight inflation, inventory planning, and near-term margin resilience.

Management Team

Experienced Consumer-Goods Leadership with Kingsway-Backed Governance

- AIIR will be led by CEO Stuart Brazier, whose 22-plus years at British American Tobacco across Europe, North Africa, and Asia Pacific bring deep experience in large-scale consumer and regulated-category execution. CFO Bassem Lotfy brings more than two decades of BAT finance leadership across Europe and the Middle East, supporting capital allocation, financial discipline, and public-market readiness. Chief Legal and Corporate Affairs Officer Ronan Barry oversees legal, compliance, governance, regulatory, and public affairs, drawing on 13 years of senior legal roles at BAT. Chief People Officer Shane George, formerly of Reckitt, leads global HR and IT and also oversees European operations. At the board level, Chairman Tamir Saeed (Managing Partner at Kingsway) provides strategic and capital allocation oversight alongside Kingsway founder-CEO Manuel Stotz, while independent directors Faisal Bari, Ian Fearon, Andrew Gundlach, Husam Manna, and former AIR CEO Reinhard Mieck contribute experience across consumer finance, regulatory science, capital markets, governance, and consumer-brand leadership. The eight-director Board will include six independent directors and serve staggered three-year terms.

Growth Strategy

Premiumization, Adjacencies, and Expansion to Drive Next Phase of Growth

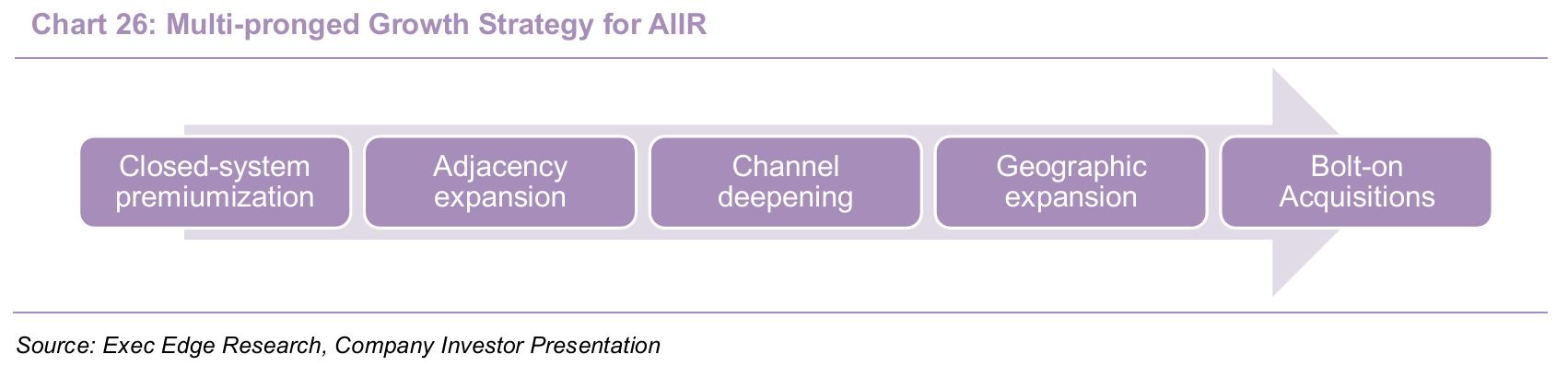

- AIIR’s growth strategy focuses on expanding the profit pool it can address while leveraging the strength of Al Fakher and its global footprint to support execution. Management is pursuing a multi-pronged plan centered on premiumization through OOKA, expansion into adjacent inhalation categories, deeper channel control, broader geographic monetization, and selective bolt-on acquisitions. The strategy is designed to improve mix, expand TAM, and reinforce AIIR’s leadership in social inhalation, while preserving the cash-generative foundation of the core business.

- Expansion of OOKA provides AIIR with a credible pathway to premiumize the hookah category and capture meaningfully higher value per session than the legacy molasses model. OOKA is a charcoal-free electronic hookah system built around a proprietary device-and-pod architecture that simplifies setup, improves consistency, and lowers the friction historically associated with traditional hookah preparation. The economics are materially stronger than the core business, with launch-market data indicating materially higher revenue and gross profit per unit relative to traditional hookah products in the U.S., UAE, and Germany. AIIR has invested more than $125 million in OOKA and VANT product innovation since 2019, with OOKA representing the company’s most visible innovation platform and a central element of its premiumization strategy. The model shifts AIIR from open consumables toward a device-plus-refill ecosystem that supports higher gross profit density, stronger control over the consumer experience, and recurring pod revenue once users enter the system. This enables monetization beyond brand equity, extending to convenience, consistency, and proprietary technology. Successful scaling of OOKA could improve mix, expand margins, and shift investor perception of AIIR from a traditional flavored molasses supplier toward a more differentiated inhalation platform with stronger unit economics and greater pricing power.

- Expansion into adjacent inhalation categories broadens the addressable market beyond traditional shisha while leveraging the company’s existing strengths in flavor development, brand-building, and route-to market. The current roadmap extends into nicotine pouches, vaping, and functional inhalation, with management framing these categories as a natural extension of AIIR’s core capabilities rather than a sharp strategic departure. The portfolio already includes Al Fakher nicotine pouches launched in the Middle East and the U.S., a controlled retail pilot for VANT launched in November 2025 in New York City and Madrid, and the broader commercialization of inhalation platforms designed to deliver nicotine and non-nicotine formulations, including functional applications. This expands AIIR’s exposure to segments that are structurally larger and, in some cases, faster growing than traditional hookah molasses, while creating additional avenues to monetize the Al Fakher brand beyond its heritage base. AIIR can leverage its installed consumer base, flavor equity, and existing commercial infrastructure to enter adjacent categories with lower customer acquisition costs than new entrants. The strategy also diversifies the revenue base, reducing dependence on a single category and expanding the set of product and geographic opportunities. Over time, adjacent-category expansion could become a meaningful contributor to both growth and valuation.

- AIIR is focused on widening and deepening its distribution network, particularly in the highest-value consumption channels where brand visibility and repeat purchase can compound more quickly. The company serves 90+ markets through a combination of wholesale, retail, hospitality, and digital channels, with lounges and HORECA venues representing especially important points of consumption and brand-building. In flavored shisha molasses, only around 35% of category volume is consumed in lounges, yet those venues account for roughly 85% of value, underscoring the importance of on premise presence and premium consumer touchpoints. At the same time, the company has assembled digital assets including Hookah.com in North America and Shisha World in Europe, creating owned e-commerce infrastructure that supports consumer acquisition and product rollout. Collaboration-led launches such as those with Snoop Dogg and Cookies further enhance channel effectiveness, as limited-edition, lifestyle-led releases are inherently well suited to digital merchandising, lounge activation, and social media-driven discovery. This hybrid channel strategy allows AIIR to combine the scale of traditional distribution with improved visibility into consumer preferences, pricing behavior, and launch effectiveness. Digital ownership also supports faster product testing, lower-friction launches, and more data-driven merchandising. As channel control improves, AIIR should see faster adoption of premium products, improved mix, and higher-margin revenue, particularly as the portfolio expands into devices, nicotine pouches, and adjacent inhalation formats.

- Geographic expansion is a key element of AIIR’s growth strategy, focused on deeper penetration of existing strongholds and selective entry into underdeveloped markets where the brand can still gain share. The business already spans 90+ markets, with meaningful positions across the Middle East, Europe, Africa, and the U.S., while western markets, particularly the U.S. and parts of Europe, remain important avenues for continued growth. The underlying opportunity remains sizable, with the flavored molasses category across focus markets expected to approach $475 million by 2030, while AIIR already holds leading positions in several core geographies. The strategy centers on combining pricing, premiumization, broader distribution, and new format expansion to deepen monetization in markets where the category is gaining cultural relevance. Geographic growth is also supported by the company’s manufacturing and distribution footprint, which includes production in the UAE and Poland and licensed third-party manufacturing across additional markets. This structure provides supply flexibility and local market responsiveness, supporting expansion without requiring a fully greenfield approach in each geography. As market penetration deepens, AIIR should benefit from a broader consumer base, stronger scale advantages, and a more diversified geographic revenue mix.

- AIIR is also using selective bolt-on acquisitions to deepen category leadership, strengthen local market positions, and broaden the portfolio in ways that can be scaled across its wider platform. The clearest example is the acquisition of NameLess, a premium German hookah brand announced in December 2025, which adds a recognized local brand and provides another asset to commercialize through AIIR’s distribution network spanning 90+ markets. Management has also highlighted additional bolt-on M&A opportunities in the core business, reflecting the fragmented nature of the category across geography, brand heritage, and route-to-market. Acquisitions can add local relevance, complementary flavors, and new customer relationships more quickly than greenfield brand building, while also creating cross-sell potential through AIIR’s broader commercial infrastructure. This approach reinforces multiple priorities simultaneously, including market expansion, premiumization, and channel density. Disciplined tuck-in acquisitions should support share consolidation in flavored hookah while adding capabilities across newer categories, digital commerce, and product innovation.

Fundamentals and Valuation

High-Quality Core Earnings Support AIIR’s Evolution to a Higher-Value Business Mix

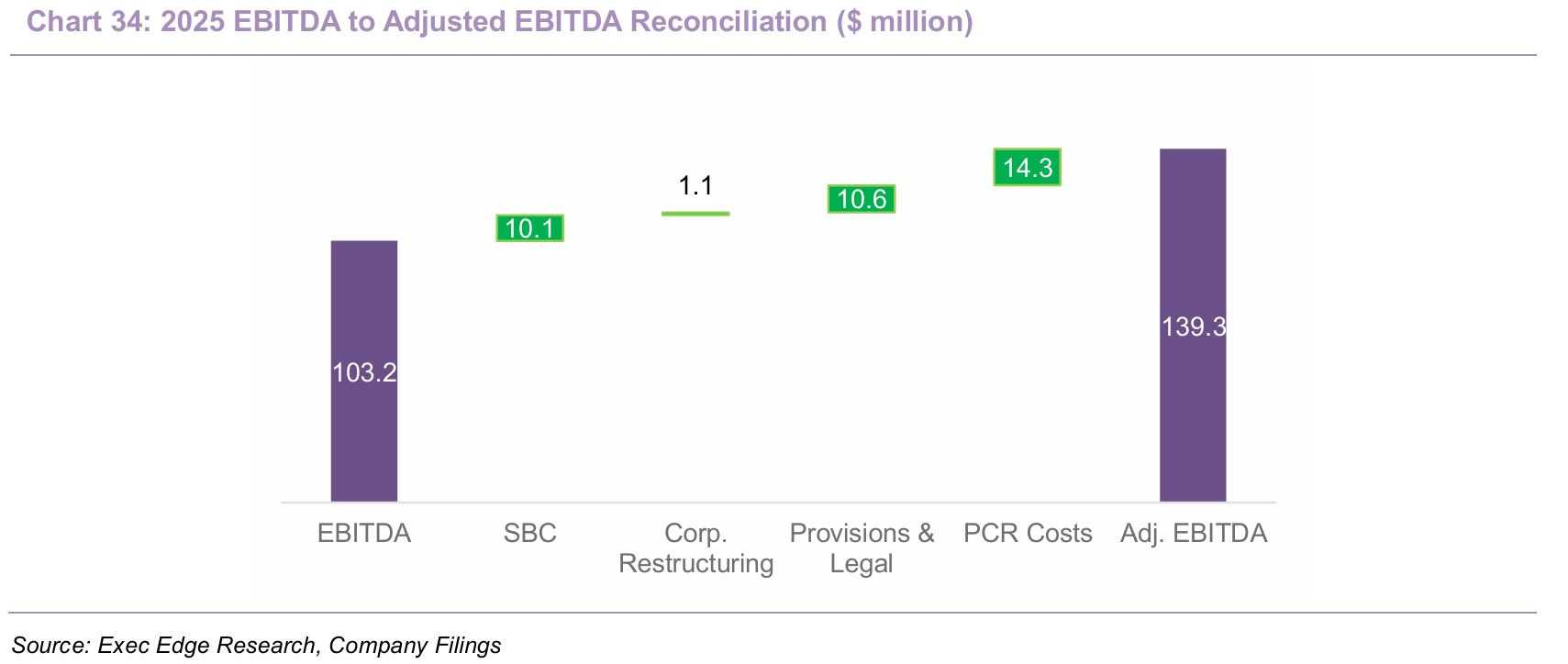

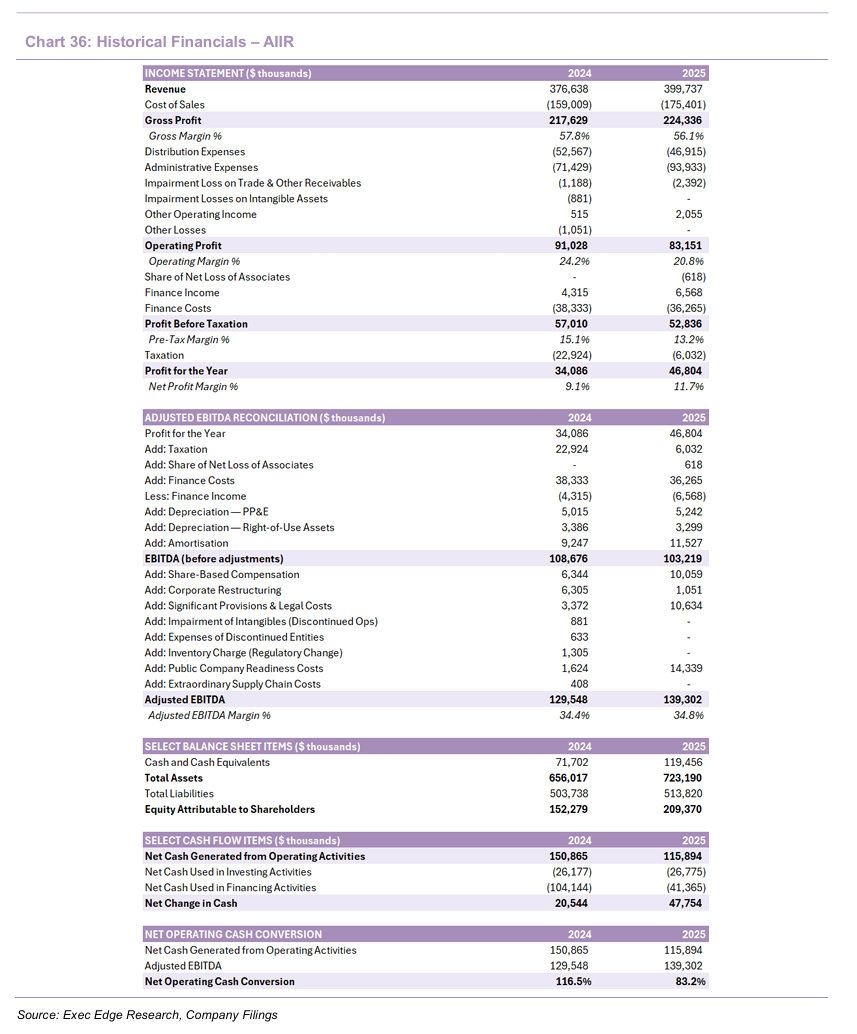

- AIIR enters public markets with a stable, high-margin, and cash-generative core business that provides a strong foundation for its next phase of growth. The company exited 2025 with steady top-line expansion and modest margin improvement, reinforcing the resilience of its earnings base despite continued investment in newer categories and public company readiness. Consolidated revenue increased to $399.7 million in 2025 from $376.6 million in 2024 (+6.1% y/y), while adjusted EBITDA grew to $139.3 million from $129.5 million (+7.5% y/y). Adjusted EBITDA margin expanded to 34.8% from 34.4%, indicating maintained operating discipline through the investment cycle. Profit for the year increased to $46.8 million from $34.1 million, highlighting underlying earnings resilience even as the company absorbed strategic and transaction-related costs. On a three-year basis, adjusted EBITDA has compounded from ~$118 million in 2023 to ~$139 million in 2025, indicating a pattern of steady progression rather than a one-off uplift. Overall, AIIR is entering public markets with a credible earnings base, where future value creation is likely to be driven more by mix shift and premiumization than by volume alone.

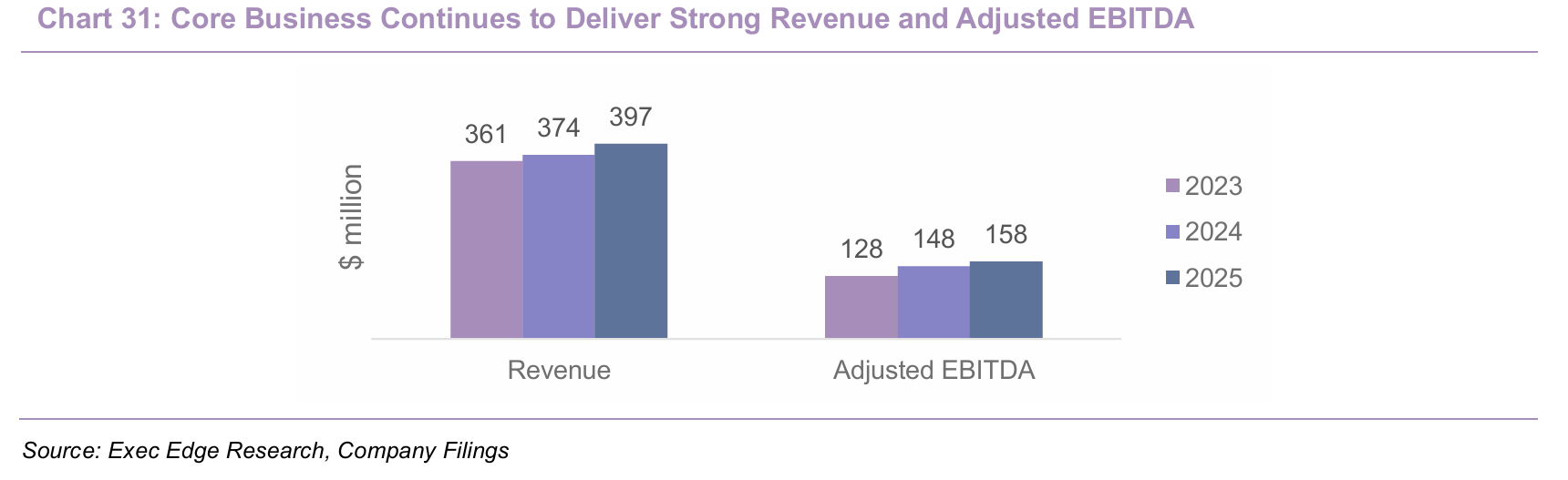

- The core molasses business remains the primary earnings engine, funding investment in newer categories that are still in build-out mode but structurally higher value. In 2025, core revenue was $397 million versus $375 million in 2024, while core adjusted EBITDA increased to $158 million from $150 million, implying a stable ~40% margin profile across both years. This compares to consolidated adjusted EBITDA of $139.3 million, reflecting the impact of continued investment in the New Growth Markets segment, including OOKA, nicotine pouches, VANT, and Crown Switch. The resulting profile is one where the core franchise continues to drive earnings and cash generation, while newer categories dilute near-term margins but represent the primary driver of future mix and margin expansion. The strategic importance of these newer segments therefore lies less in current contribution and more in their potential to expand the addressable market and evolve the earnings profile over time. The investment case hinges on scaling the emerging portfolio into a meaningful second profit pool, rather than the current segment mix.

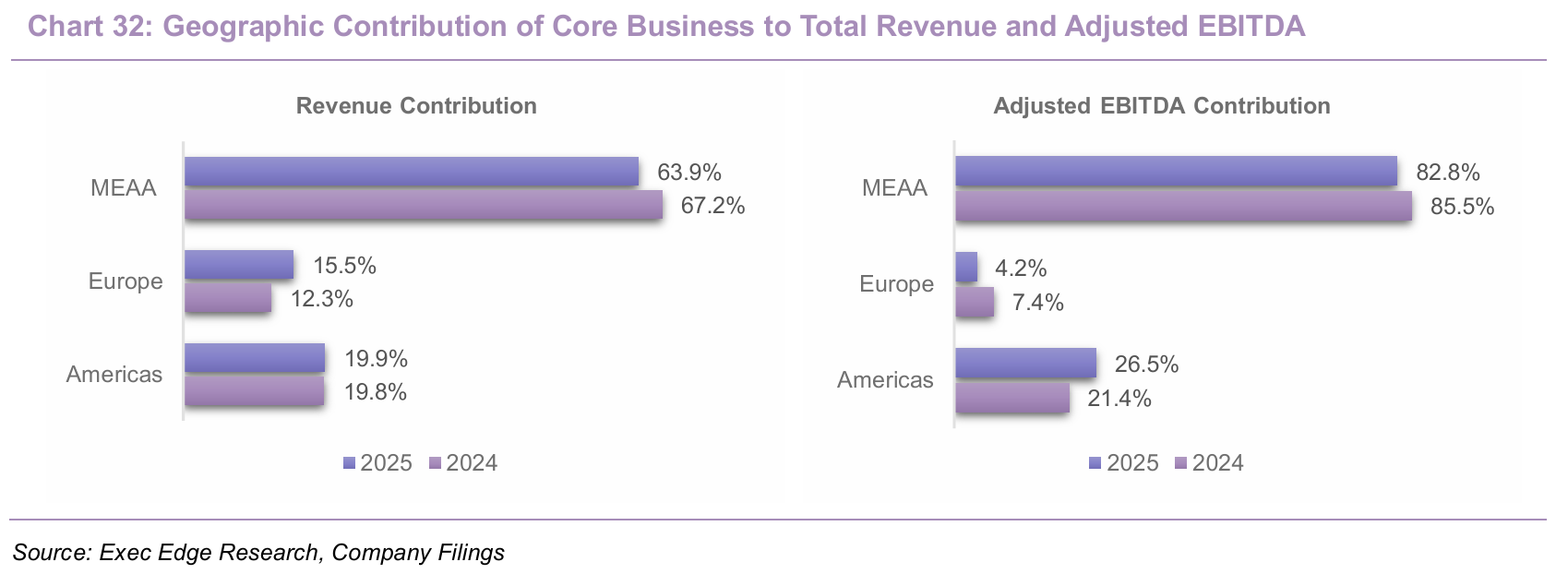

- AIIR’s geographic mix reflects a balance between a high-margin, heritage-led core and emerging growth markets shaping the next phase of the business. While the Americas, Europe, and MEAA (Middle East, Africa and Asia) remain central to the footprint, these regions serve distinct roles. The Middle East anchors the core business through strong brand heritage, lounge penetration, and premium consumption occasions that support margin stability. In contrast, western markets, particularly the U.S. and parts of Europe, represent key growth vectors driven by product innovation, collaboration led launches, and the rollout of newer formats such as OOKA and adjacent inhalation categories.

- Geographic mix is therefore a key driver of both margin trajectory and execution quality. Market-level profitability varies based on channel structure, pricing power, distributor economics, regulatory intensity, and franchise maturity. As a result, future margin progression will depend not only on product mix, but also on regional mix, particularly as higher-value western channels scale. At the same time, operating across multiple regions mitigates exposure to regulation, excise, FX, and geopolitical risks. We view geographic revenue and adjusted EBITDA contribution as a key indicator of whether AIIR can scale newer markets while preserving the profitability of its core business.

- Cost structure supports gross margin resilience, as value is concentrated in higher-value inputs rather than bulk commodity volumes. On a per-kilogram basis, glycerin accounts for 42% of volume and fructose for 39%, while tobacco represents only 14% and flavors 5%. By value, however, the mix shifts materially, with tobacco rising to 33% of COGS, miscellaneous costs contributing 25%, flavors 16%, and packaging 14%, while glycerin and fructose fall to just 7% and 4%, respectively. The cost base is therefore driven less by low-value commodity inputs and more by higher-value components such as tobacco, flavors, packaging, and production-related costs. As a result, gross margin performance is more closely linked to procurement discipline, pricing power, and product mix than to movements in bulk input volumes, reinforcing the durability of margins in the core business.

- Margin profile reflects a high-quality core earnings engine, with near-term dilution driven by investment in newer categories and public-company readiness. On a consolidated basis, adjusted EBITDA margin expanded by ~40 bps to 34.8% in 2025, while the core business sustained a margin of roughly 40%, highlighting the strength of the underlying franchise. The gap between core and consolidated margins underscores the current model dynamic: a highly profitable, cash-generative core funding newer categories that remain in build-out mode and constrain near-term margin progression.

- Adjustment items were also meaningfully higher in 2025, including $14.3 million of public-company readiness costs versus $1.6 million in 2024, alongside higher share-based compensation and legal / provision-related expenses. This results in a gap between reported and adjusted profitability that is expected to normalize as the business transitions to a steady-state public-company cost structure, and explains why reported operating profit declined year-on-year despite growth in adjusted EBITDA.

- Current margin dilution is primarily a function of investment in newer categories and public-company readiness, rather than a structural limitation to profitability. The underlying earnings profile reflects a strong core business that is funding expansion, while the path to cleaner reported operating leverage is expected to improve as newer categories scale and non-recurring costs normalize. Near-term margins are therefore likely to remain stable to modestly improving, with more meaningful upside driven by mix shift into OOKA and improved absorption of corporate and launch-related expenses.

- The company’s next phase of growth is expected to be driven more by mix shift and premiumization than by acceleration in the legacy shisha franchise. The core molasses category remains positioned for mid-single digit growth, supported by a market that continues to expand in value terms and by AIIR’s brand strength across lounges, hospitality, and retail. The primary growth lever is OOKA, where economics are materially superior to the core business, with roughly 20x revenue per kilogram and 15x gross profit per kilogram in launch markets. As adoption scales, OOKA has the potential to disproportionately influence mix and profitability, given its higher-value, device-led model and recurring refill economics.

- Adjacent categories such as nicotine pouches and functional inhalation provide additional avenues for growth, although they remain in early stages of monetization rather than near-term earnings drivers. Growth over the next 2-3 years is therefore expected to be shaped by a combination of resilient core demand, pricing and premium mix, OOKA scaling, and gradual contribution from newer categories and acquisitions such as NameLess. Margin expansion is likely to follow rather than lead this growth, as near-term dilution from investment and launch costs gives way to improved mix and operating leverage as higher-value segments scale.

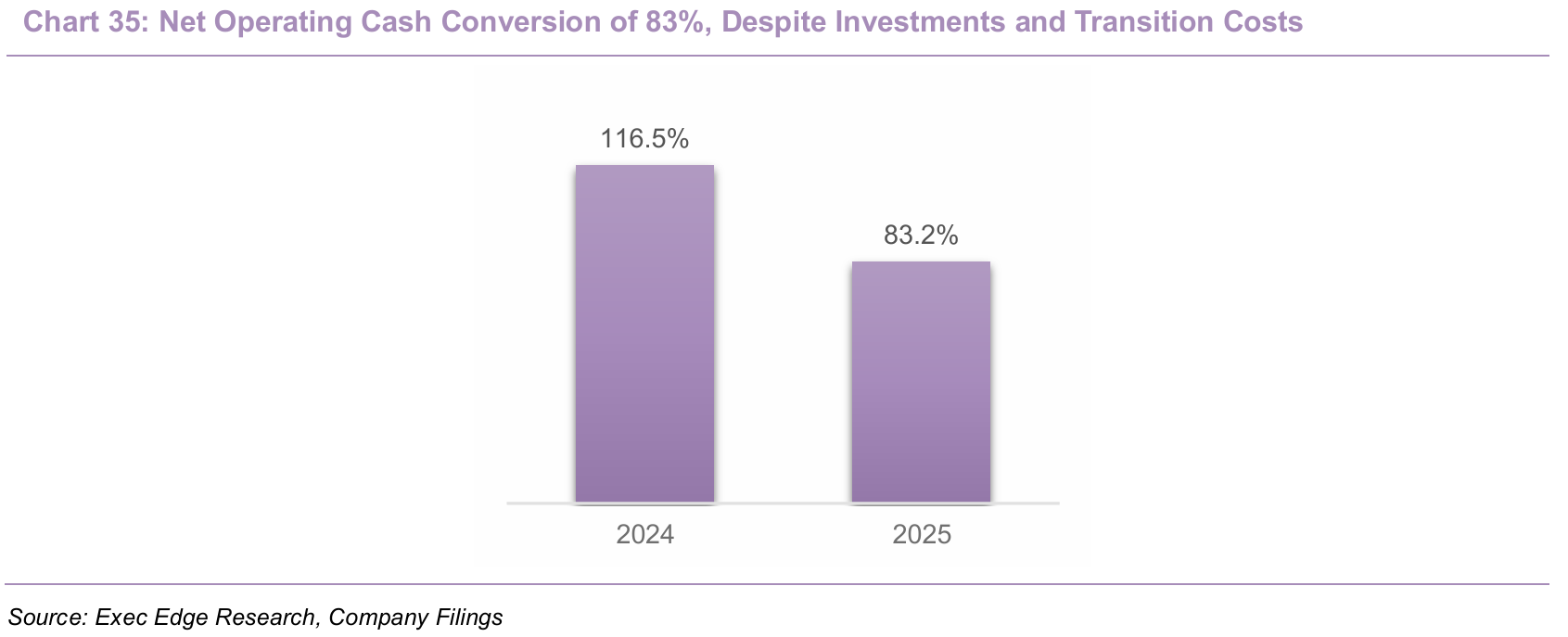

- We believe AIIR’s earnings quality is best reflected in its cash generation, reinforcing a self-funded growth model rather than reliance on external capital. Net cash generated from operating activities was $115.9 million in 2025, equal to roughly 83.2% of adjusted EBITDA, which remains strong by consumer-product standards despite ongoing investment in newer categories and transaction-related costs. This level of cash conversion supports continued investment in product development, geographic expansion, and selective M&A without requiring a trade off between growth and balance-sheet preservation. The more relevant signal is the business’s ability to consistently convert operating earnings into cash through the investment phase, rather than the near-term gap between reported and adjusted profitability. This positions AIIR to fund expansion internally while scaling higher-value growth drivers.

- AIIR’s balance sheet complements this cash-generative profile, with leverage at levels that provide flexibility without constraining execution. Net debt/adjusted EBITDA was 2.1x in 2025 on a pre-transaction basis, with management targeting a leverage range of roughly 2.5x, indicating capacity to invest while maintaining balance sheet discipline. Leverage is supported by a stable core earnings base and recurring operating cash flow, rather than reliance on external capital, which is particularly relevant in the context of the pending listing and redemption variability. This positions the company to fund expansion without dependence on SPAC proceeds for day-to-day execution, while maintaining flexibility to invest in innovation and acquisitions. While leverage will require ongoing monitoring as the business scales, the current profile is consistent with controlled expansion, with the balance sheet acting as a support rather than a constraint to the growth strategy. We believe this combination of a strong core earnings base and mix-driven growth opportunity forms the foundation for valuation, where upside is likely to be driven by successful scaling of higher-value segments.

Valuation Anchored by Core Earnings, with Upside from Emerging Growth Platforms

- Valuation appears broadly in line with tobacco and nicotine peers on current financials, while offering

embedded upside if AIIR can scale higher-value categories such as OOKA, nicotine pouches, and VANT.

The following analysis is illustrative in nature and does not constitute a price target or a buy/sell/hold

recommendation. Any implied upside should be interpreted as an output of the analytical framework rather than a

definitive valuation outcome. - At the transaction valuation, AIIR offers incoming public-market investors exposure to a profitable, cash

generative category leader with growth optionality that is not yet fully reflected in the current peer

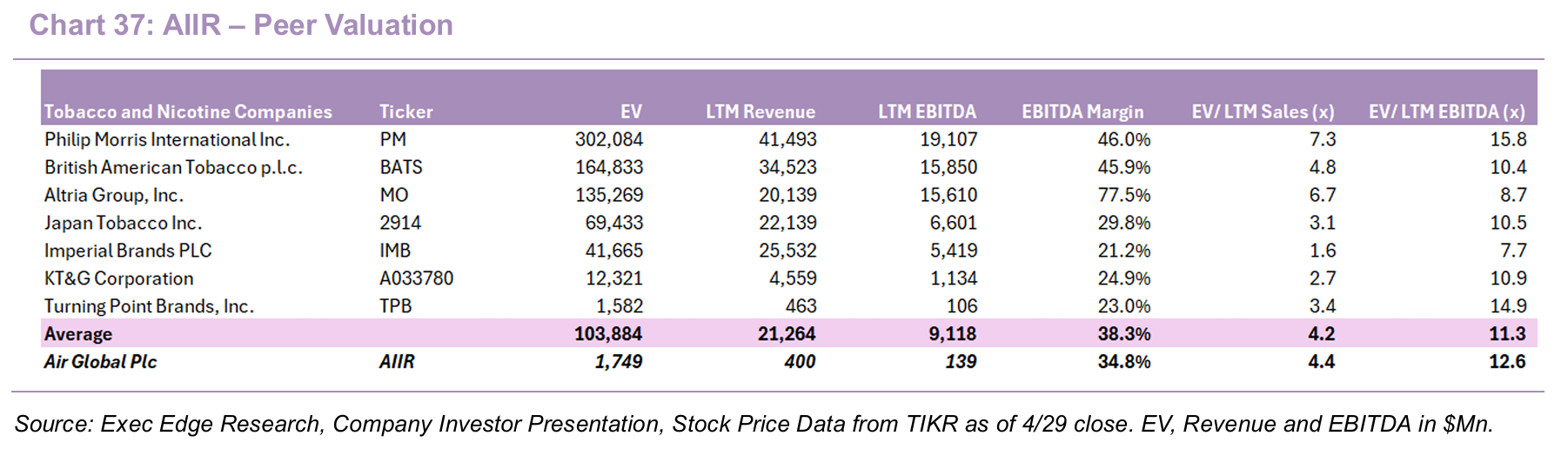

framework. The SPAC deal values AIIR at $1.749 billion EV, implying 4.4x EV/LTM sales and 12.6x EV/LTM EBITDA

versus peer averages of 4.2x and 11.3x, respectively. On sales, AIIR screens broadly in line with the peer group,

trading below premium global names such as Philip Morris International and Altria Group, while remaining above

lower-multiple tobacco peers. On EBITDA, AIIR trades at a modest premium to most traditional tobacco names,

though still below higher-growth nicotine and inhalation platforms. Importantly, this positioning comes despite AIIR

operating at a margin below large-cap peer averages, suggesting the current valuation is supported by the strength

of the core franchise and future mix potential rather than margin leadership alone. - The deal valuation is therefore attractive in the context of both existing shareholder monetization and

incoming investor exposure. Existing shareholders retain meaningful participation in a scaled, cash-generative

business entering public markets, while incoming investors gain exposure to a leading flavored shisha franchise with

a self-funded path into higher-value inhalation formats, including platforms such as OOKA and emerging adjacent

categories. This reflects a valuation that sits between a legacy molasses business and a fully scaled next-generation

inhalation platform, anchored by the profitable core while leaving room for upside as these newer segments scale

into the mix. - We believe multiple expansion is likely to depend on a combination of continued core stability and evidence

that AIIR can convert strategic optionality into a more diversified earnings profile. The core business remains

central to this framework, providing the cash generation, margin base, and execution track record that underpin

valuation support and fund investment in newer categories.- OOKA remains the clearest re-rating driver, given disclosed launch-market economics of roughly 20x revenue

per kilogram and 15x gross profit per kilogram versus traditional hookah. As adoption scales, even moderate

penetration could meaningfully influence mix and investor perception, particularly if recurring pod demand proves

durable. At the same time, the durability of the core franchise is equally important, as it reduces execution risk

and provides the financial capacity to scale these higher-value segments without reliance on external capital. - Additional upside would come from traction across adjacent categories such as nicotine pouches and

functional inhalation, particularly if growth is delivered without material margin dilution or disproportionate

capital intensity. The market will also likely look for a period of consistent public-company execution, including

sustained cash generation, disciplined leverage, and clear capital allocation. If AIIR can demonstrate both

resilience in the core business and credible scaling of newer categories into a meaningful second profit pool, the

stock could justify a wider premium to traditional tobacco peers and move closer to the valuation range of higher

growth nicotine and inhalation platforms.

- OOKA remains the clearest re-rating driver, given disclosed launch-market economics of roughly 20x revenue

Risks

- Regulatory exposure: AIIR’s products fall under tobacco, nicotine, and hemp-derived regulatory regimes that

continue to evolve across its markets. U.S. activities are subject to FDA oversight, certain products lack premarket

authorization, and rules governing flavors, marketing, packaging, and CBD remain in flux. Changes in laws, excise

tax regimes, smoking and advertising restrictions, or enforcement priorities could limit product availability, restrict

promotional activity, raise compliance costs, or require changes to portions of the portfolio. - Health liability: AIIR’s products contain nicotine and, in certain cases, by-products of combustion that have been

associated with health effects, and the long-term effects of shisha and heat-not-burn formats remain incompletely

studied. The company may face product liability, consumer fraud, or failure-to-warn claims similar to those historically

brought against tobacco manufacturers. - Illicit competition: Counterfeit, smuggled, and duty-not-paid shisha products represent a significant share of the

global market and compete directly with AIIR’s legitimate offerings. As a leading branded producer, the company is

a frequent target of counterfeiting activity, particularly in jurisdictions with higher excise taxes. Illicit trade can

compress pricing, divert sales, dilute brand equity, and require ongoing investment in enforcement. - Demand evolution: AIIR’s growth depends on continued consumer demand for shisha and the adoption of newer

formats such as OOKA, VANT, and nicotine pouches. Consumer preferences are shaped by health awareness,

cultural trends, pricing, and the availability of substitutes, and may shift faster than the company can adjust product

mix or production. Novel inhalation devices are at an early stage of commercialization, and demand patterns may

prove less predictable than those of the established flavored molasses business. - Supply concentration: AIIR relies on sole or effectively exclusive distributors in several core markets and on a

limited set of third-party manufacturers for proprietary flavoring ingredients and device components, including OOKA

and VANT. Tobacco leaf and other raw materials are sourced from a narrow set of geographies. Termination of a key

relationship, supplier capacity constraints, or commodity price volatility could disrupt supply, raise costs, or limit

AIIR’s ability to meet demand on commercially reasonable terms. - Leverage and liquidity: AIIR carries substantial indebtedness, including secured senior credit facilities that pledge

certain assets and contain restrictive covenants limiting financing, investment, and dividend flexibility. A portion of

borrowings carries floating interest rates, and the company operates as a holding company dependent on subsidiary

cash flows for debt service. Future capital needs may require additional debt or equity issuance, which could be

dilutive, costlier than expected, or unavailable on acceptable terms during periods of market stress. - Governance and shareholder profile: Following the Business Combination, AIR shareholders will beneficially own

approximately 82.7% of AIIR, and the Sponsor and AIR shareholders together will hold at least 84.9% at closing.

AIIR expects to qualify as a controlled company, foreign private issuer, and emerging growth company under Nasdaq

and SEC rules, allowing reliance on reduced disclosure and governance exemptions. Public shareholders will face

limited float, concentrated voting power, and potential PFIC considerations that may affect liquidity and minority

influence. - Transaction execution: Completion of the Business Combination is subject to shareholder approvals, regulatory

clearances, minimum cash conditions, and Nasdaq listing requirements, and may not occur on the expected timeline

or at all. Significant redemptions by SPAC public shareholders could reduce available cash, alter the post-closing

capital structure, and affect AIIR’s ability to fund growth initiatives. Following closing, AIIR will also incur incremental

costs and management attention associated with operating as a U.S.-listed public company. - Geopolitical risk: AIIR has meaningful exposure to the Middle East through its Dubai headquarters, UAE production

footprint, and key regional markets including the UAE and Saudi Arabia. Escalation of regional tensions could disrupt

Gulf shipping routes, increase freight and energy costs, delay inventory flows, and pressure working capital. While

AIIR’s diversified manufacturing base and 90+ market footprint provide some mitigation, a sustained disruption could

impact margins, supply-chain efficiency, and demand in core markets. Foreign exchange volatility and trade barriers

could further pressure reported results and margins.

Download the Complete Report Here

Subscribe to our Weekly Newsletter to Receive All Research

Contact: