Download the Complete Report Here

Alico, Inc. (ALCO)

Alico, Inc. (ALCO)

Land Monetization and Corkscrew Approval Reinforce Post-Citrus Transformation; Valuation Remains Supported by Embedded Land Optionality

- Key Takeaways:

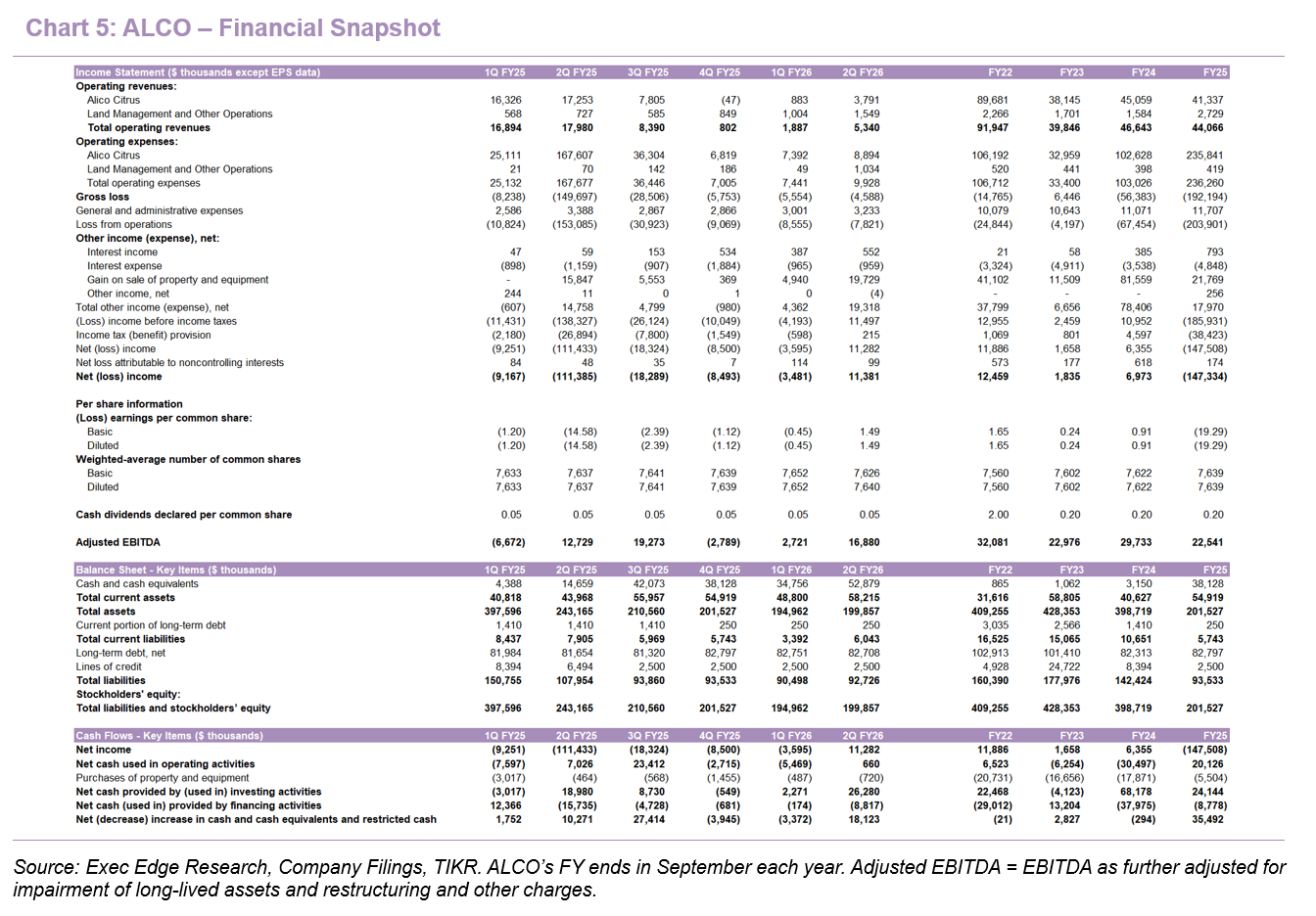

- 2Q FY26 marked another strong execution quarter, with adjusted EBITDA of $16.9 million and net income of $11.4 million.

- Land monetization accelerated, with a $26.9 million sale of non-core citrus acreage bringing YTD land sales to $34.6 million.

- Collier County approval for Corkscrew Grove East Village materially advances ALCO’s long-term development strategy in Southwest Florida.

- Liquidity strengthened despite $10.0 million of share repurchases, with $52.9 million of cash extending runway through FY28.

- Valuation remains supported by conservative land assumptions, with upside tied to monetization, entitlement progress, and long-term development optionality.

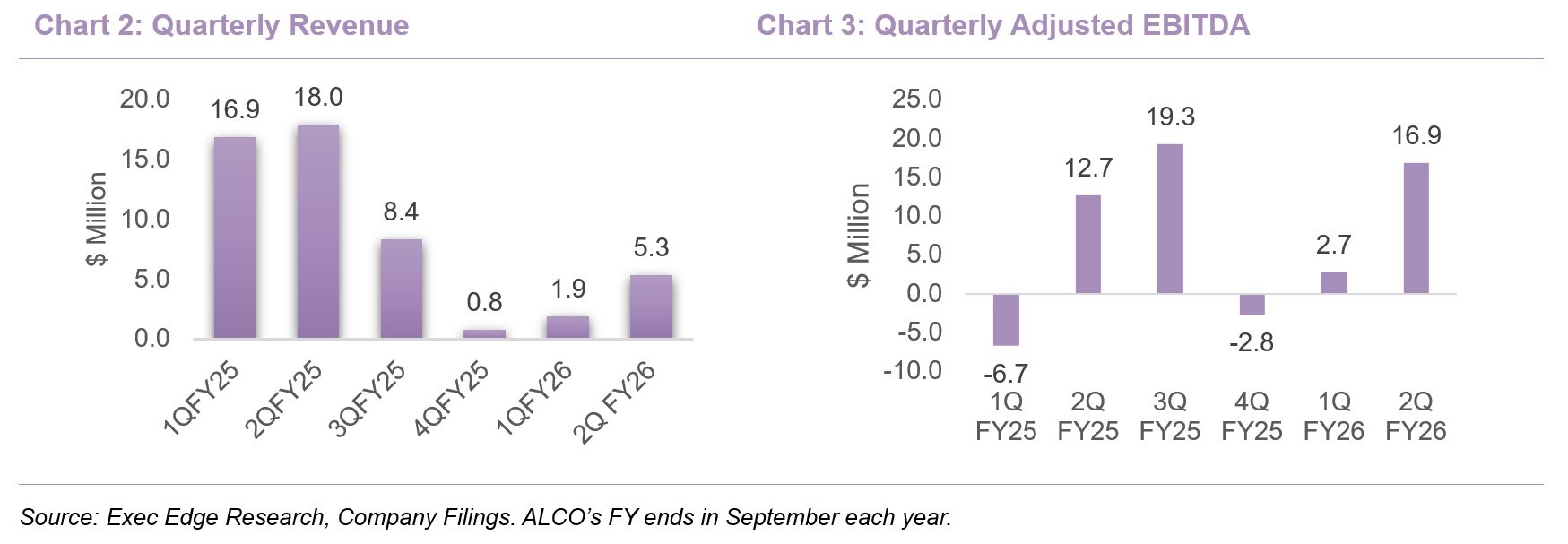

- Land monetization and lower citrus drag drove another quarter of positive adjusted EBITDA. 2Q FY26 (quarter ending March 2026) reflects continued progress in ALCO’s transition from a weather and disease-exposed citrus operator into a land-management and development platform with recurring agricultural utilization, episodic land sales, and long-duration real estate optionality. ALCO reported net income attributable to common stockholders of $11.4 million, or $1.49 per diluted share, compared with a net loss of $111.4 million, or $14.58 per diluted share, in 2Q FY25. Adjusted EBITDA increased 32.6% y/y to $16.9 million from $12.7 million, while EBITDA improved to $16.7 million from a loss of $14.7 million, reflecting the January land sale, lower citrus drag, and continued execution of the company’s land-centric operating strategy.

- Land sale proceeds funded both liquidity and shareholder returns. ALCO closed the previously announced sale of approximately 2,950 acres of citrus grove for $26.9 million during the quarter, bringing year-to-date land sales to $34.6 million. Importantly, management paired this monetization with $10.0 million of common share repurchases through April 2026, demonstrating a more active capital allocation posture while still maintaining a strong liquidity position.

- Agricultural land utilization is becoming the cash-flow bridge for ALCO’s development strategy. Approximately 97% of ALCO’s ~32,500 farmable acres are now utilized, representing ~89% of its 46,000 agricultural acres and providing a steadier lease/royalty base while land sales and development milestones remain episodic.

- Land management revenue is scaling as agricultural utilization improves. Land Management and Other Operations revenue increased 113.1% y/y to $1.5 million in 2Q FY26 from $0.7 million, driven by higher farm lease and sod revenue.

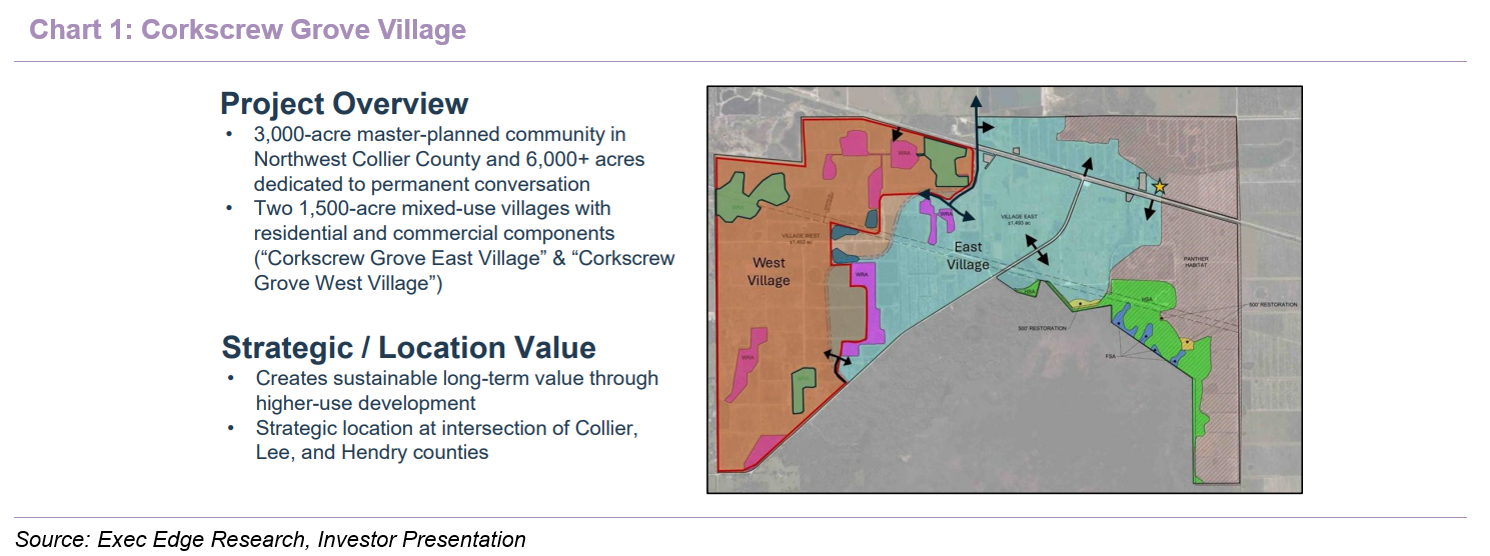

- Collier County approval materially de-risks Corkscrew Grove East Village. In April 2026, ALCO received unanimous approval from the Collier County Board of County Commissioners for the Stewardship Receiving Area and companion Stewardship Sending Area 22 for Corkscrew Grove East Village. The approval covers the creation of a 1,446.59-acre East Village Stewardship Receiving Area and a 1,295.4-acre Stewardship Sending Area, authorizing up to 4,502 dwelling units, including 362 affordable housing units for essential workers, at least 10% multi-family units, up to 238,606 gross square feet of neighborhood-scaled retail and office uses, up to 100,000 square feet of indoor self-storage, and at least 45,020 gross square feet of civic, government, and institutional uses.

- Corkscrew now moves from local entitlement to state and federal permitting. Corkscrew Grove Villages is planned as a two-village master-planned community located on approximately 4,660 acres at the northwest corner of Collier County, with more than 6,000 acres expected to be placed into permanent conservation across the overall project. With local approvals now secured for East Village, ALCO’s focus shifts to remaining federal permits from the U.S. Army Corps of Engineers and U.S. Fish and Wildlife Service, as well as state permits from the South Florida Water Management District. Management remains on its timeline of expected state approval by early 2027 and federal approval by the end of 2028, keeping the project on track for potential construction commencement in 2028 or 2029 if all required approvals are received.

- Management continues evaluating multiple monetization pathways for Corkscrew Grove, with a strategic decision potentially emerging over the next year. ALCO reiterated that the company retains flexibility to either sell entitled land outright to national or local homebuilders, pursue partnership structures where ALCO would receive upfront proceeds and participate in value creation as development progresses, or potentially build internal development capabilities. Management noted that the timing of remaining state and federal approvals, housing market conditions, and the risk-adjusted economics of each path will influence the final decision. Management also acknowledged that while ALCO has a strong in-house team, it is not a construction specialist, keeping outright land sales or builder/developer partnerships highly relevant as Corkscrew Grove advances.

- Management reiterated FY26 priorities around land monetization, entitlement progress, and capital discipline. Management reiterated that ALCO’s priorities remain focused on optimizing agricultural operations through diversified leasing programs, advancing development projects through entitlement with particular focus on Corkscrew Grove Villages, balancing required entitlement investments with shareholder returns, and maintaining operational discipline through its experienced team and local relationships. During 2Q FY26, ALCO delivered against these priorities through the $26.9 million Hendry County land sale, 97% utilization of farmable agricultural acreage, local approval for Corkscrew Grove East Village, $10.0 million of share repurchases, and quarter-end cash of $52.9 million.

- Near-term development projects continue to anchor ALCO’s embedded land value. Management reiterated that four priority projects – Corkscrew Grove Villages, Bonnet Lake, Saddlebag Grove, and Plant World – totaling approximately 5,500 acres, continue to advance as planned. These projects are estimated to carry a combined present value of $335 million to $380 million, which management expects could be realized over the next five years and represents value creation from approximately 10% of ALCO’s total land holdings.

- Recent land transaction activity continues to validate ALCO’s underlying land value. Management reiterated its estimated $650 million to $750 million portfolio value range for the remaining ~46,000 acres, despite the portfolio declining from 50,000+ acres two years ago. Importantly, recent land sales have occurred closer to ~$9,000 per acre, well above the $4,000-$5,000 per acre agricultural land assumptions embedded in the company’s more conservative NPV framework. Management cautioned that not all acreage carries comparable development potential, but the recent transaction data supports the view that ALCO’s land base remains conservatively valued.

- Diversified land management programs continue to improve portfolio resilience and reduce operational complexity. ALCO now generates revenue through fee-based or revenue-sharing agreements with citrus growers, cattle operators, mining operators, sugarcane producers, and sod farming operations. Segment operating expenses increased to $1.0 million from $0.1 million as ALCO scaled diversified land usage, but higher revenue more than offset the added cost, reinforcing the shift from direct citrus operations toward third-party land use while preserving land ownership.

- Revenue profile continues to reflect the Citrus exit, while land management streams are scaling from a smaller base. Total operating revenue was $5.3 million in 2Q FY26 versus $18.0 million in 2Q FY25, primarily reflecting the wind-down of citrus operations following the last significant harvest in April 2025. Alico Citrus revenue declined 78.0% y/y to $3.8 million. This decline reflects the intentional exit from a structurally challenged citrus business and the transition toward lower-complexity land sales, leasing, and development activities.

- Operating expenses declined sharply as the citrus wind-down reduced legacy cost intensity. Total operating expenses declined 94.1% y/y to $9.9 million, driven primarily by the reduction in Alico Citrus operating expenses to $8.9 million from $167.6 million in the prior-year quarter. G&A expense decreased by $0.16 million y/y in 2Q FY26, primarily due to lower depreciation expense following accelerated depreciation in the prior-year period, partially offset by higher contract labor costs and credit loss provisions on certain citrus receivables.

- Land sale gains drove profitability, while the comparison also reflects the removal of unusually large prior-year citrus costs. Other income improved to $19.3 million in 2Q FY26 from $14.8 million in 2Q FY25, primarily due to the $19.7 million gain on sale of property and equipment. Net income attributable to common stockholders improved to $11.4 million from a loss of $111.4 million, principally driven by the sale of ~2,950 acres for $26.9 million in gross proceeds, while citrus operating expenses declined to $8.9 million from $167.6 million as ALCO continued winding down citrus operations.

- Adjusted EBITDA was strong in 2Q FY26, though full-year guidance reflects the timing variability of the transformed model. Adjusted EBITDA increased to $16.9 million from $12.7 million in the prior-year quarter, while first-half adjusted EBITDA rose to $19.6 million from $6.1 million. Management maintained FY26 adjusted EBITDA guidance of approximately $14 million, implying a softer back half as land sales, leasing activity, and development milestones replace the historical citrus harvest cycle as the key drivers of quarterly results. ALCO also expects to end FY26 with roughly $40 million of cash, $45 million of net debt, and only the minimum required $2.5 million balance on its revolving credit facility, with guidance reflecting the approximately $10 million of share repurchases completed through April 2026.

- Robust liquidity and balance-sheet flexibility support execution of the development roadmap. ALCO ended 2Q FY26 with $52.9 million of cash and cash equivalents, up $14.8 million from $38.1 million at September 30, 2025. Total debt remained approximately $85.5 million, while net debt declined to $32.6 million from $47.4 million at fiscal year-end, reflecting land sale proceeds and disciplined balance-sheet management. ALCO also maintained approximately $92.5 million of available borrowing capacity under its line of credit and had a minimum liquidity requirement of only $5.8 million, giving it substantial flexibility to pursue entitlements, manage transition costs, and continue evaluating shareholder returns.

- Working capital remains strong as ALCO manages through the business model transition. Working capital was $52.2 million at March 31, 2026, and the current ratio was 9.63x. Total current assets increased to $58.2 million from $54.9 million, while total current liabilities increased modestly to $6.0 million from $5.7 million. Operating cash flow was positive $0.7 million in 2Q FY26, while first-half operating cash flow was $(4.8) million, reflecting timing effects as ALCO transitions away from citrus and toward land sales, leasing, and development.

- Capital allocation remains balanced between shareholder returns and development flexibility. ALCO paid a quarterly cash dividend of $0.05 per share on April 17, 2026, consistent with the prior quarterly dividend, and repurchased 245,399 shares for $10.0 million through April 2026. Management noted that any additional capital returns through increased common dividends, special dividends, tender offers, or open market repurchases would reduce year-end cash and increase net debt relative to current guidance.

- Board addition strengthens real estate and capital allocation expertise. ALCO elected Eric Speron to its Board of Directors, adding relevant experience in real estate, finance, public-company governance, and land-rich asset platforms as the company advances entitlement execution and portfolio monetization. Mr. Speron currently serves as Managing Director of Equities at First Foundation, previously worked in J.P. Morgan’s Institutional Equity division, and has board experience at Keweenaw Land Association, Tejon Ranch, Tandy Leather Factory, and Vidler Water Company.

Valuation: Sum-of-the-Parts Highlights Embedded Upside from Land Optionality

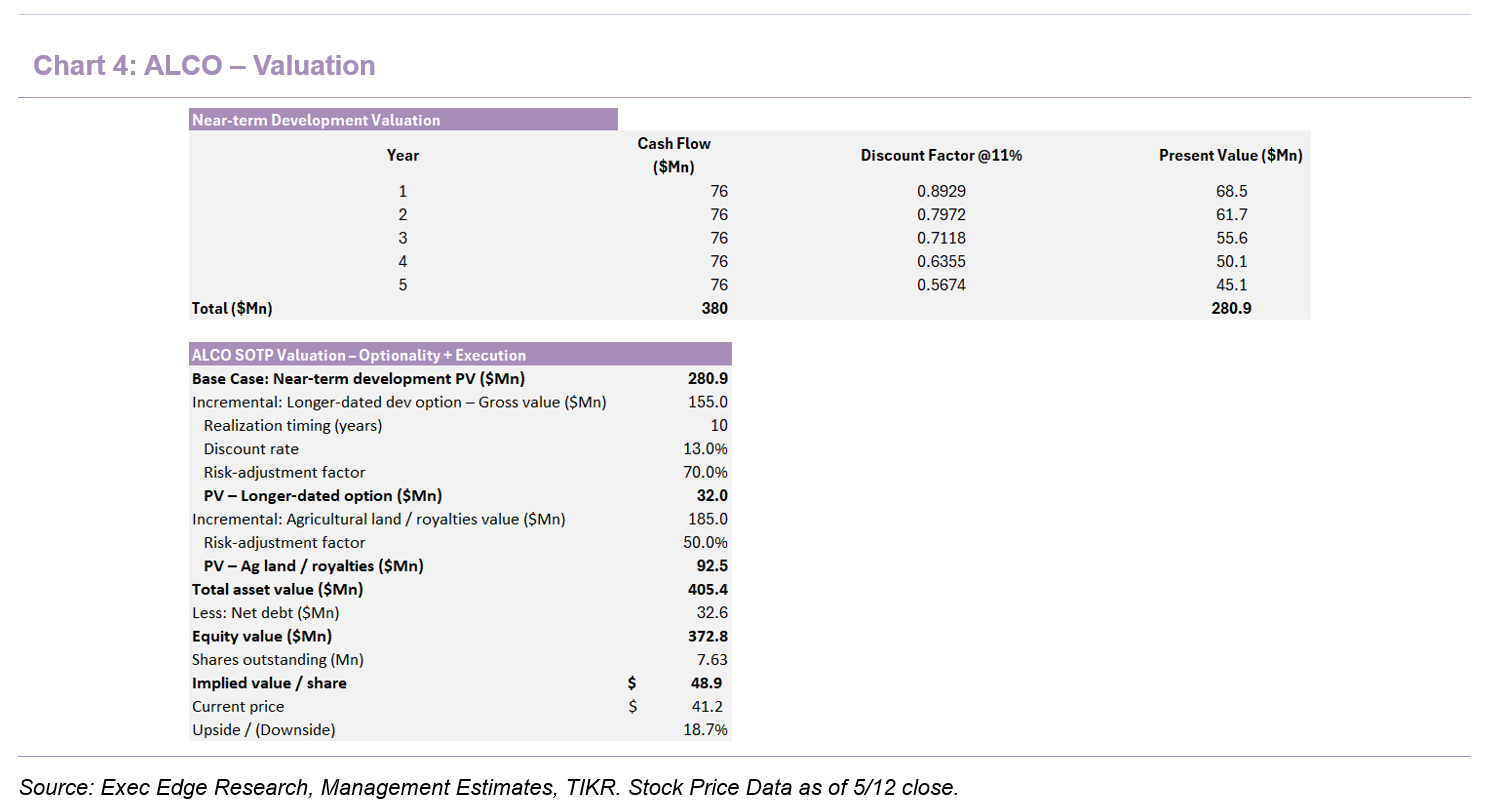

- While we do not publish a formal price target for ALCO, our analysis suggests potential upside from current levels. The valuation discussion that follows is provided for illustrative purposes only and does not constitute a stock recommendation or a buy/sell/hold opinion. In light of ALCO’s transition to a land-management-focused business model, we apply a discounted cash flow–based framework to assess expected cash flows from the company’s property portfolio over time. Any implied upside reflects the output of this framework and should not be interpreted as a formal price target.

- We value ALCO using a sum-of-the-parts (SOTP) framework that reflects the company’s evolution into a diversified land platform with distinct asset components and risk profiles. Our approach separates value across near-term development projects with defined execution visibility, longer-dated development optionality embedded in the broader land base, and the long-duration value of agricultural land and royalty streams. Near-term development is valued using a conservative discounted cash flow methodology, while longer-dated development and agricultural land value are incorporated on a risk-adjusted basis to reflect timing, liquidity, and execution uncertainty. We believe this framework more appropriately captures ALCO’s underlying asset value than a single consolidated DCF, while maintaining disciplined underwriting and a clear linkage between upside and execution.

- Base case DCF – near-term development only. Our base-case DCF values only the first tranche of ALCO’s development pipeline (approximately 10% of total land holdings), which management has identified as near-term and actively progressing through the entitlement process. We apply an 11% discount rate to reflect late-stage development risk for partially entitled land, including remaining regulatory approvals, timing uncertainty, and housing cycle sensitivity. This base case yields a value of approximately $36-$37 per share, which sits below the current share price and underscores the conservative nature of our core underwriting. Notably, this base case does not ascribe any value to additional development tranches or to the long-duration value of ALCO’s agricultural land holdings. The April 2026 unanimous Collier County approval for Corkscrew Grove East Village modestly de-risks this base case, although state and federal permits remain the key remaining approvals.

- Incremental upside from longer-dated development optionality. Beyond the initial near-term development tranche, ALCO retains additional land conversion potential over a longer time horizon. Management has outlined potential incremental development opportunities representing roughly 15% of the land base, with monetization expected well beyond the current five-year planning window. We incorporate this optionality using a conservative present-value approach and apply an explicit risk-adjustment factor to reflect extended duration, market uncertainty, and execution risk. On a risk-adjusted basis, this longer-dated development optionality contributes incremental upside to our valuation without relying on accelerated timelines or aggressive pricing assumptions.

- Agricultural land and royalties – long-duration asset value. ALCO’s remaining land base generates recurring income through agricultural leases and royalty arrangements and represents a long-duration real asset with underlying scarcity value. While this land is not assumed to be monetized through development in our base case, we incorporate partial value recognition using a conservative asset-based approach and apply a risk-adjustment factor to reflect illiquidity and the absence of near-term monetization. This treatment acknowledges embedded land value while maintaining disciplined underwriting.

- Implied Valuation. Combining our base-case DCF with risk-adjusted contributions from longer-dated development and agricultural land value, and adjusting for net debt, supports an implied equity value modestly above the current share price. We therefore arrive at an implied valuation range in the mid-to-high $40s per share, representing high-teens upside from current levels. Importantly, this upside is driven primarily by execution and entitlement progress rather than discount-rate compression or multiple expansion. As regulatory milestones are achieved and development visibility improves, we see scope for incremental value recognition over time.

- Recent land transactions continue to support potential upside to ALCO’s underlying land valuation. Management reiterated that its remaining ~46,000-acre portfolio, down from 50,000+ acres two years ago, is still estimated to be worth $650 million to $750 million. Management also noted that recent land sales have occurred above $9,000 per acre, materially higher than the $4,000-$5,000 per acre agricultural assumptions embedded in its conservative NPV framework, while cautioning that not all acreage carries comparable development potential. Management indicated that it plans to release an updated land valuation framework soon, with additional detail around acreage buckets, monetization assumptions, and entitlement progress potentially supporting further value recognition over time.

Download the Complete Report Here

Read Exec Edge’s Initiation on Alico Here

Subscribe to our Weekly Newsletter to Receive All Research

Contact: