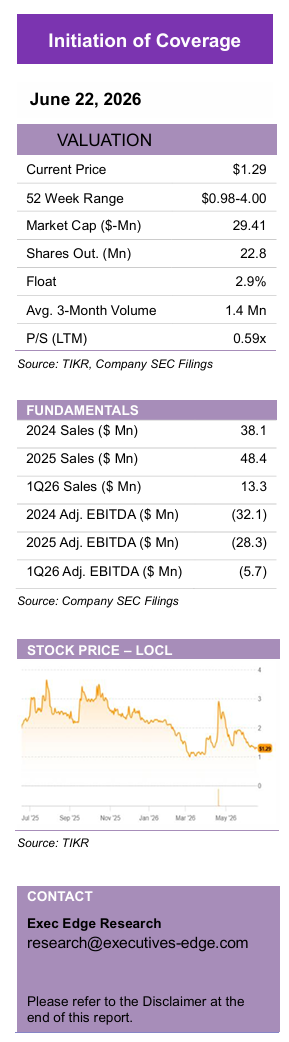

Download the Complete Report Here

Local Bounti Corporation (LOCL)

Local Bounti Corporation (LOCL)

From Capacity Ramp to Yield-Led Growth: Stack & Flow, Retail Demand, and SKU Breadth Support LOCL’s Next Phase

- LOCL is a branded CEA fresh-produce platform built around patented Stack & Flow Technology. LOCL produces lettuces, leafy greens, arugula, cress, baby leaf, and salad kits through a hybrid vertical nursery and greenhouse grow-out model designed to improve crop turns, yield density, and facility efficiency. The company operates across Georgia, Texas, Washington, California, and Montana, with GA, TX, and WA as the current Stack & Flow-enabled production base. With these facilities at full harvestable capacity and run-rate capacity committed to customers, the story is shifting from capacity build-out to asset productivity and retail-volume conversion.

- Stack & Flow, AI-enabled optimization, and retail demand create a higher-yield, lower-cost business model. Stack & Flow has delivered measurable facility-level gains, including Georgia doubling run-rate production, Texas automated harvesting doubling facility output, and tower upgrades adding 10% run-rate yield capacity. The 2026 AI and computer-vision patent adds a data-driven optimization layer to support consistency, yield, and operating transferability. Retail relationships across 13,000 doors convert production into demand visibility, while 25+ retail products broaden LOCL’s shelf relevance.

- Large produce TAM and CEA trends favor LOCL’s model, with the market now rewarding execution over capacity. The U.S. fruit and vegetable market remains large and growing, while consumers and retailers increasingly favor fresh, local, convenient, and value-added produce. Retailers are also prioritizing regional supply chains to reduce volatility, shrink, and freight exposure, while the CEA reset has shifted investor focus toward unit economics, energy efficiency, labor productivity, and capital discipline. LOCL is aligned with these trends, but its re-rating case depends on proving facility-level productivity and demand-backed utilization.

- Operating leverage is improving, supporting management’s path to positive adjusted EBITDA. 2025 and 1Q26 results show the operating leverage story beginning to emerge. Revenue growth is translating into higher gross profit, stable adjusted gross margin, and an improving EBITDA profile, with 1Q26 adjusted EBITDA loss improving 35% y/y to $(5.7) million. The $15 million convertible note and warrant investment from U.S. Bounti, LLC, an entity managed by Charles R. Schwab, also signals continued strategic investor support and adds flexibility as LOCL pursues yield initiatives, retail launches, and EBITDA improvement.

- Valuation recovery depends on sustained execution, not just sector re-rating. We do not provide a price target or stock recommendation. However, we note that LOCL trades at 0.59x LTM sales, below its prior high multiple, leaving room for recovery if recent operating progress proves durable. Within the CEA-linked peer set, LOCL remains differentiated by its patented Stack & Flow platform, retail footprint, full-capacity utilization, and improving adjusted EBITDA trajectory. Any re-rating will depend on sustained revenue growth, stable adjusted gross margin, balance sheet discipline, and investor confidence that LOCL can convert its asset base into repeatable, higher-quality retail volume.

Company Overview

Innovation-Led Platform Scaling from CEA Production to Retail Distribution

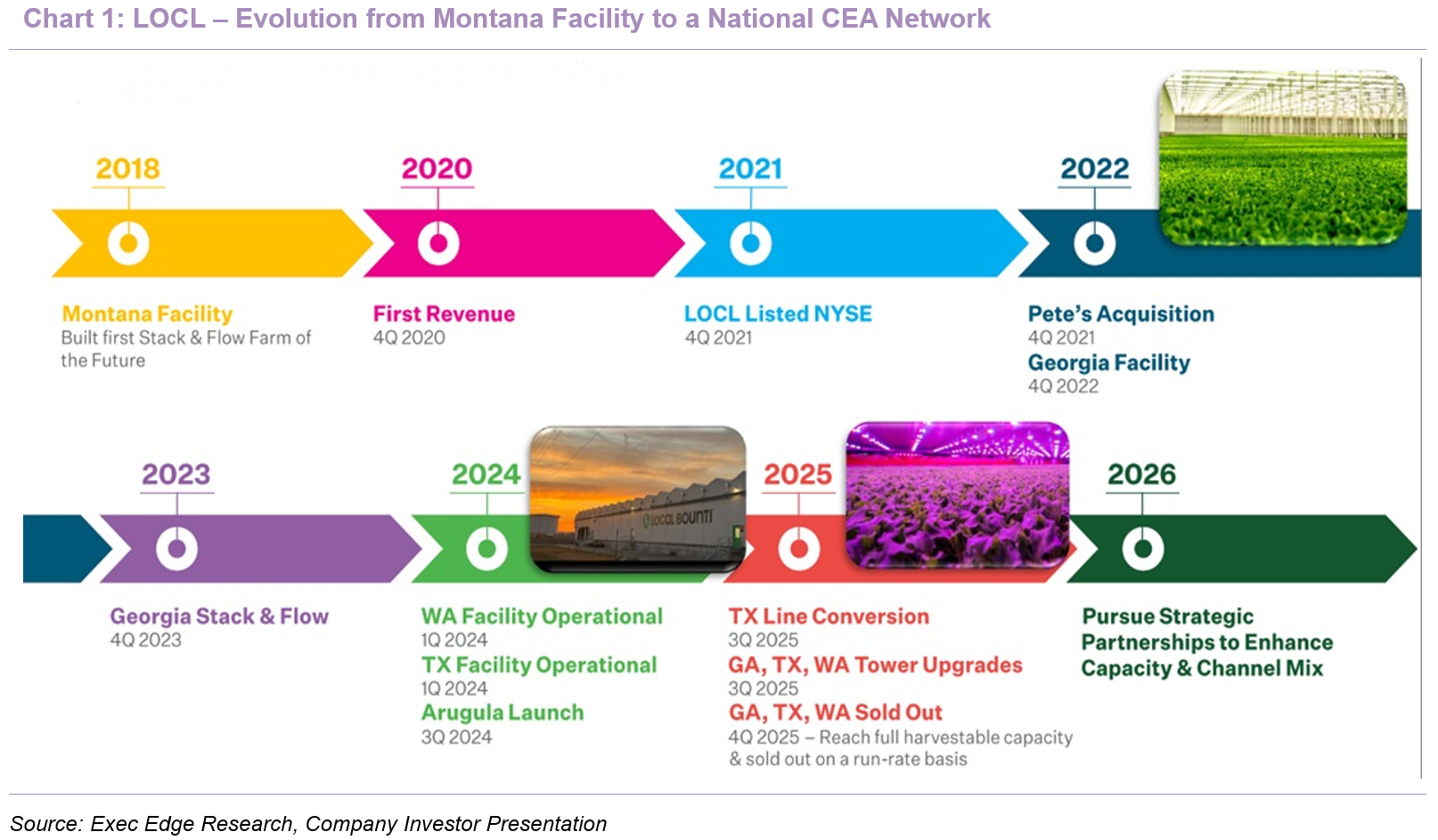

- Local Bounti Corporation (LOCL) is a controlled environment agriculture company focused on branded fresh produce through the commercialization of its patented Stack & Flow Technology. LOCL was founded in August 2018 and is headquartered in Hamilton, Montana. The company produces sustainably grown produce, focused primarily on living lettuce, leafy greens, loose leaf lettuce, and salad kits, and operates as a CEA platform that uses a hybrid of vertical nursery production and controlled-environment greenhouse grow-out to grow food in a more controlled environment. LOCL’s public listing followed the November 19, 2021 business combination between Local Bounti and Leo Holdings III Corp., and its common stock is listed on the NYSE under the ticker LOCL. The company’s operating history has moved through several distinct phases: the first Montana facility reached commercial operations in 2H20, LOCL listed on the NYSE in 4Q21, the Pete’s acquisition expanded the company into California and Georgia, and the company added purpose-built Washington and Texas facilities in 2024. By 2025-26, the company’s profile had shifted from early capacity build-out toward a broader network model built around facility utilization, retailer commitments, product expansion, and technology-enabled yield improvement.

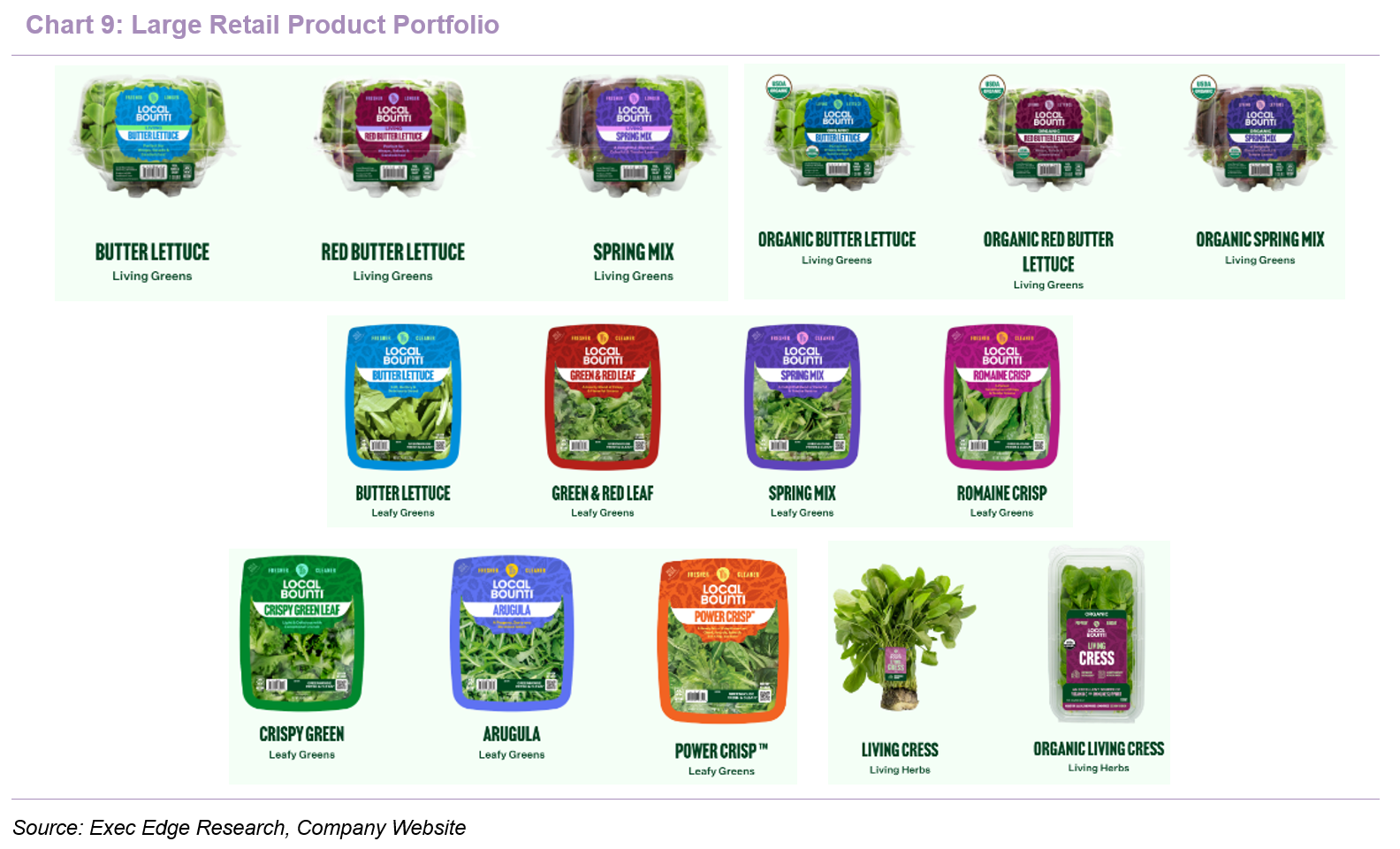

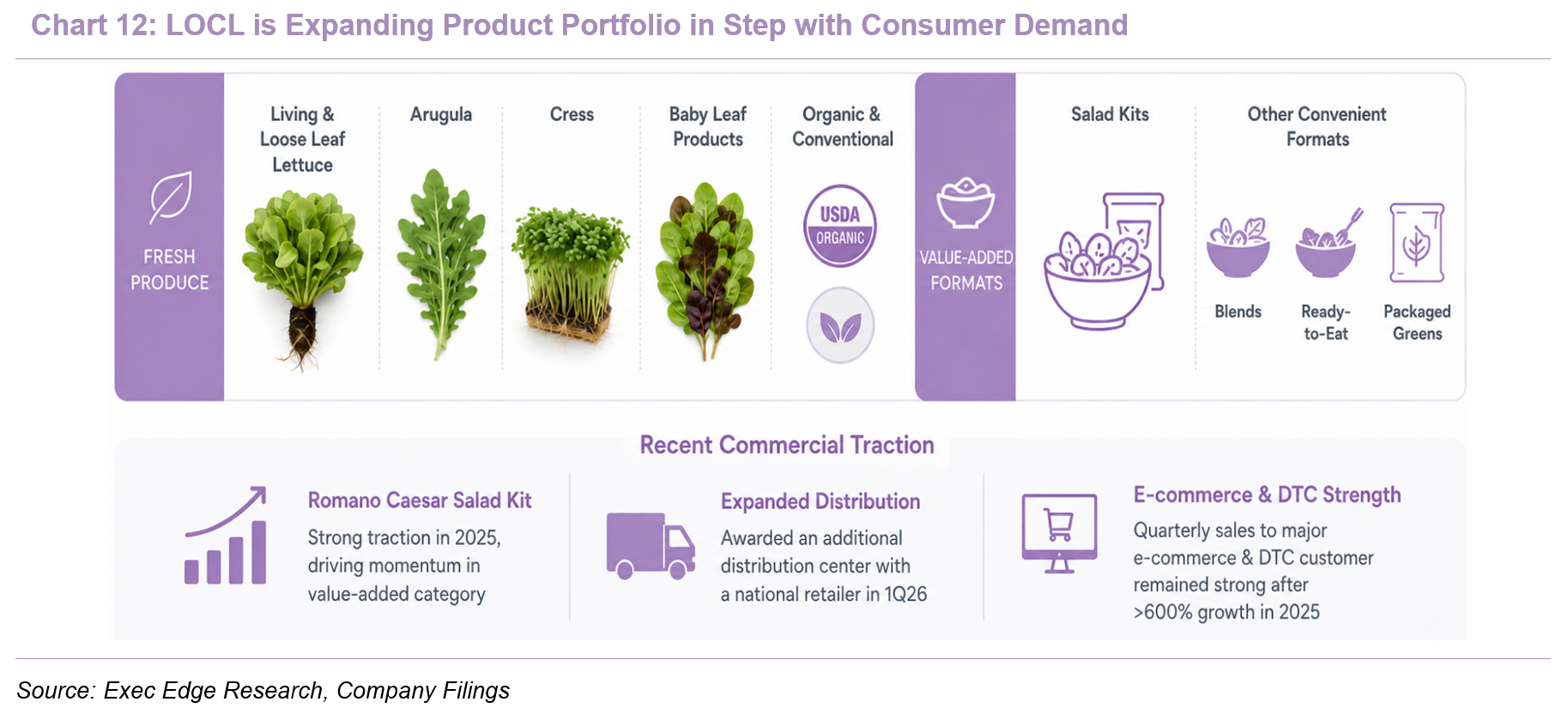

- LOCL’s product portfolio is centered on lettuce and leafy greens, with a growing mix of value-added retail products designed for broader shelf presence. The company’s core offerings include living butter lettuce, loose leaf lettuce, packaged leafy greens, cress, arugula, baby leaf products, organic and conventional varieties, and salad kits. LOCL’s product portfolio has broadened beyond core living lettuce into 25+ retail products across packaged leafy greens, cress, arugula, ready-to-eat blends, salad kits, and organic / conventional offerings, giving the company a broader shelf-space opportunity across fresh and value-added produce formats. The company’s branded proposition emphasizes non-GMO, Greenhouse Fresh & Clean™ produce, sustainably grown with sunlight, and designed to offer weeks of freshness. Recent product development has broadened the offering beyond core living lettuce. LOCL continued to expand arugula after successful launches at its Pasco, WA and Mount Pleasant, TX facilities in 2025. The company’s website presents the consumer-facing portfolio as living greens, leafy greens, salad kits, and herbs, reinforcing a retail brand architecture that extends beyond a single lettuce SKU.

- The company operates a distributed production network across legacy greenhouse assets and newer Stack & Flow-enabled facilities, with Georgia, Texas, and Washington representing the current state-of-the-art operating base. LOCL’s first Hamilton, Montana facility was built in 2019, reached commercial operations in 2H20, and now acts as corporate headquarters without active commercial operations while management evaluates future commercial use. The 2022 Pete’s acquisition added two California greenhouse facilities, Carpinteria and Oxnard, and one Georgia facility that was then under construction. Georgia became operational in July 2022, was expanded in 2023, and later received Stack & Flow Technology, while Washington and Texas began operations in 2024 as purpose-built facilities. The company’s property footprint includes Montana headquarters and vacant land in Hamilton, California production facilities in Carpinteria and Oxnard, the Georgia production facility in Byron, the Texas production facility in Mount Pleasant, and the Washington production facility in Pasco. The latest investor presentation shows GA, TX, and WA as Stack & Flow-enabled facilities and MT and CA as legacy facilities. GA, TX, and WA are operating at full harvestable capacity, with the entire run-rate capacity committed to customers. LOCL is also reviewing additional capacity expansion, including Midwest plans, pending retailer discussions and product-specific commitments.

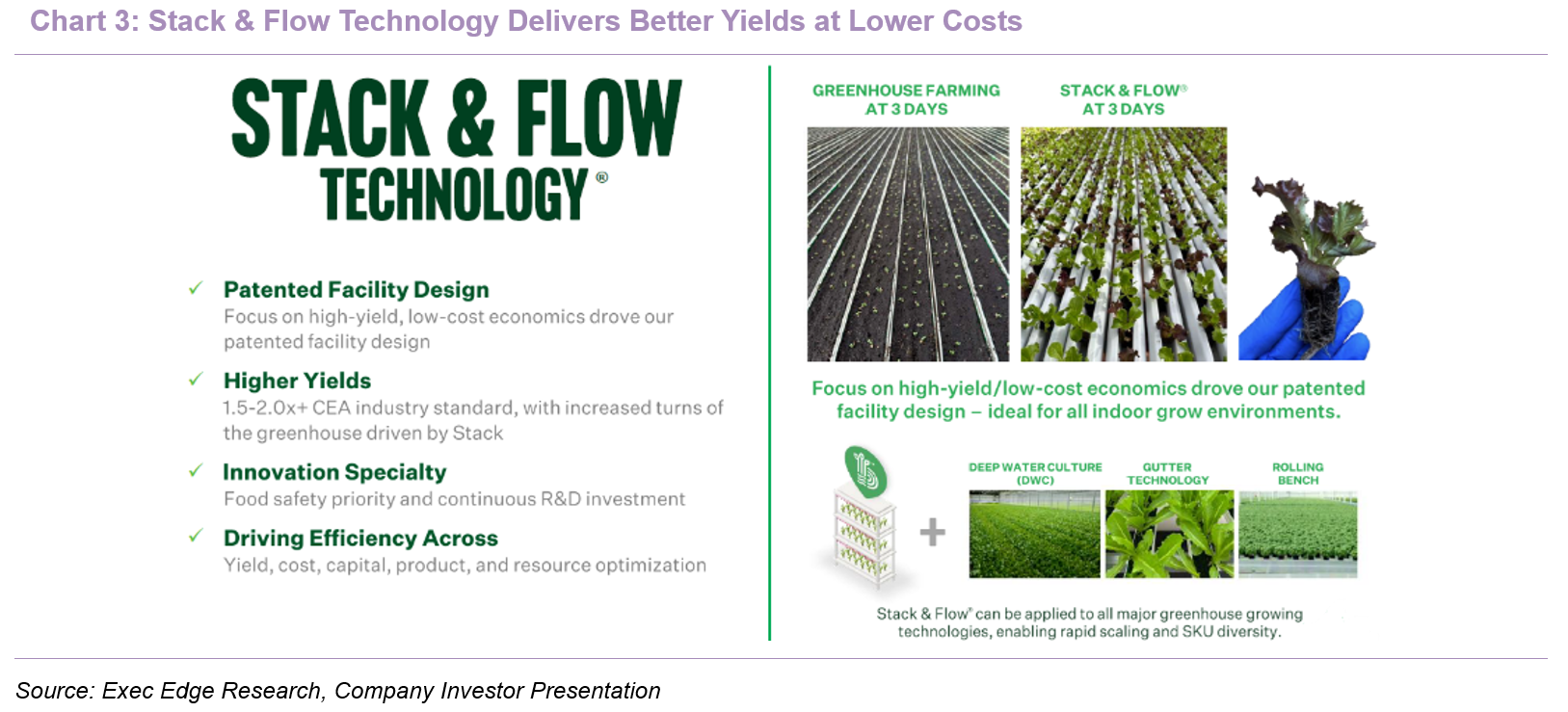

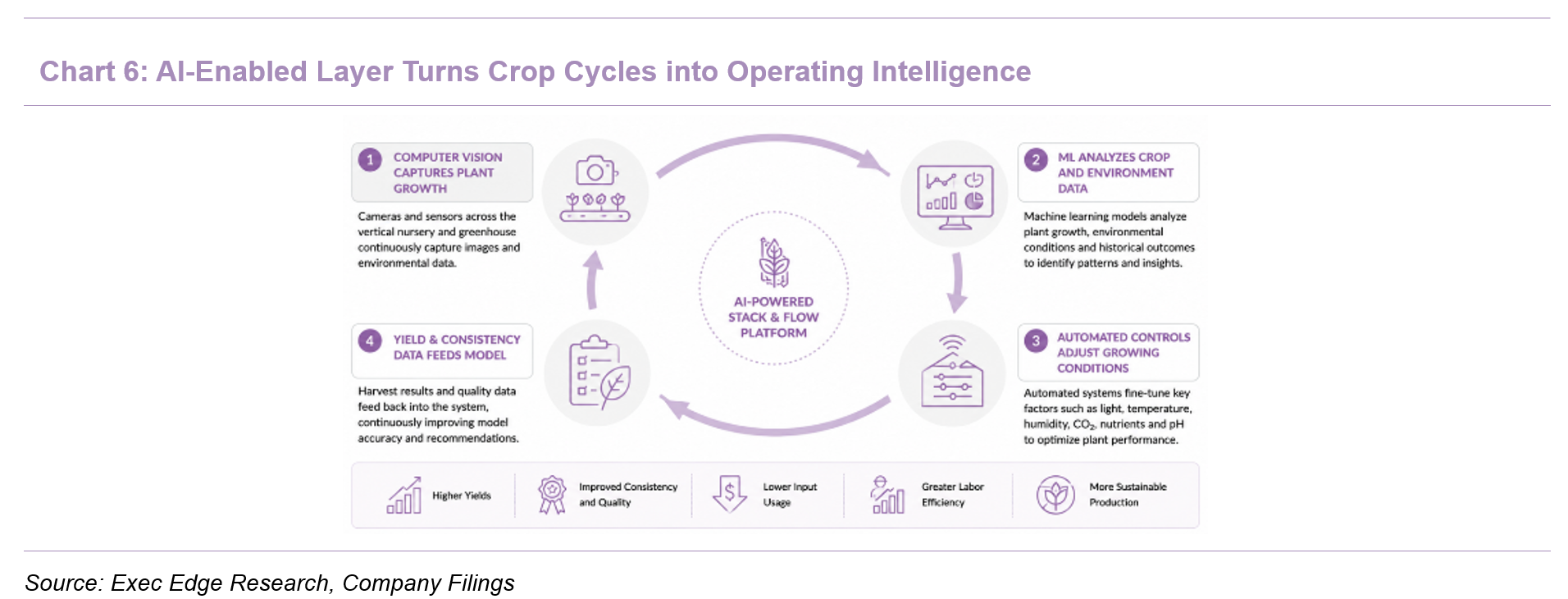

- LOCL’s Stack & Flow Technology is the company’s core production architecture, designed to combine the crop-turn benefits of vertical farming with the scale and natural-light advantages of greenhouse production. The system starts with a stacked vertical nursery, where young plants are grown in a controlled, space-efficient environment during the early growth phase. Plants are then transferred into greenhouse grow-out for final production, where natural sunlight and controlled variables such as temperature, humidity, carbon dioxide, nutrients, pH balance, and irrigation support maturation. The chart above illustrates the operating logic clearly: at three days, Stack & Flow shows visibly denser early-stage plant development versus conventional greenhouse farming, highlighting why the company frames the model around higher yield and lower-cost unit economics. The architecture also appears adaptable across major greenhouse growing systems, including deep water culture, gutter technology, and rolling bench formats, which supports SKU diversity and potential retrofit flexibility. The newer AI and computer vision layer extends this architecture by analyzing plant-growth and environmental data, then using machine learning and automated controls to improve consistency, yield, and production precision across crop cycles.

- The company’s technology stack extends beyond the Stack & Flow layout to include facility design, crop-science know-how, environmental controls, production automation, computer vision, machine learning, and proprietary operating data. Its IP portfolio includes patents, trademarks, and proprietary rights around its growing approach, with “Local Bounti” and “Stack & Flow Technology” serving as principal trademarks. The IP base was strengthened in February 2026 with U.S. Patent No. 12,557,741, titled “Optimizing Growing Process in a Hybrid Growing Environment Using Computer Vision and Artificial Intelligence.” This patent covers methods that use computer vision, machine learning, and automated environmental controls to optimize plant growth across the vertical nursery and greenhouse grow-out phases. Strategically, this matters because LOCL’s technology advantage is not limited to facility hardware. As more facilities operate at commercial scale, each crop cycle can generate data that helps refine growing recipes, standardize operating practices, identify plant-health issues earlier, and improve consistency across geographies. LOCL’s IP portfolio therefore protects more than the physical grow-system design; it also supports the data-driven optimization layer that can improve consistency, yield, and operating transferability as the network scales.

- LOCL’s commercial model is built around direct retailer relationships, broad retail-door access, and a strategy of matching regional production capacity with committed demand. The company distributes products to ~13,000 retail doors across 35 U.S. states, primarily through direct relationships with blue-chip retail customers, including Albertsons, Sam’s Club, Kroger, Target, Walmart, Whole Foods, Brookshire’s, and H-E-B. Retail remains the primary channel, complemented by club and foodservice, while co-location with nationally recognized distributors could help leverage existing distribution networks and reduce duplicative freight. This retail-focused strategy is also helping improve the company’s channel mix, which generally carries more favorable pricing and margin profiles.

- ESG footprint is anchored in its controlled-environment agriculture model, which is designed to reduce the resource intensity and supply-chain exposure of fresh produce. The company states that its growing method uses 90% less land and 90% less water than conventional agriculture, while also reducing pesticide and herbicide use and supporting fresher, longer-lasting products closer to end markets. Its ESG messaging maps the business to 12 of the 17 UN Sustainable Development Goals, including clean water, sustainable infrastructure, responsible consumption, climate action, life below water, life on land, and partnerships. The sustainability proposition is commercially relevant because retailers and consumers increasingly value produce that combines freshness, traceability, lower resource use, and reduced food miles. For LOCL, sustainability is therefore part of the business model itself, tied directly to how the company grows, distributes, and positions its products within the CEA market.

Right-to-Win

Superior Yield, Retail Access, and SKU Breadth Define LOCL’s Right-to-Win

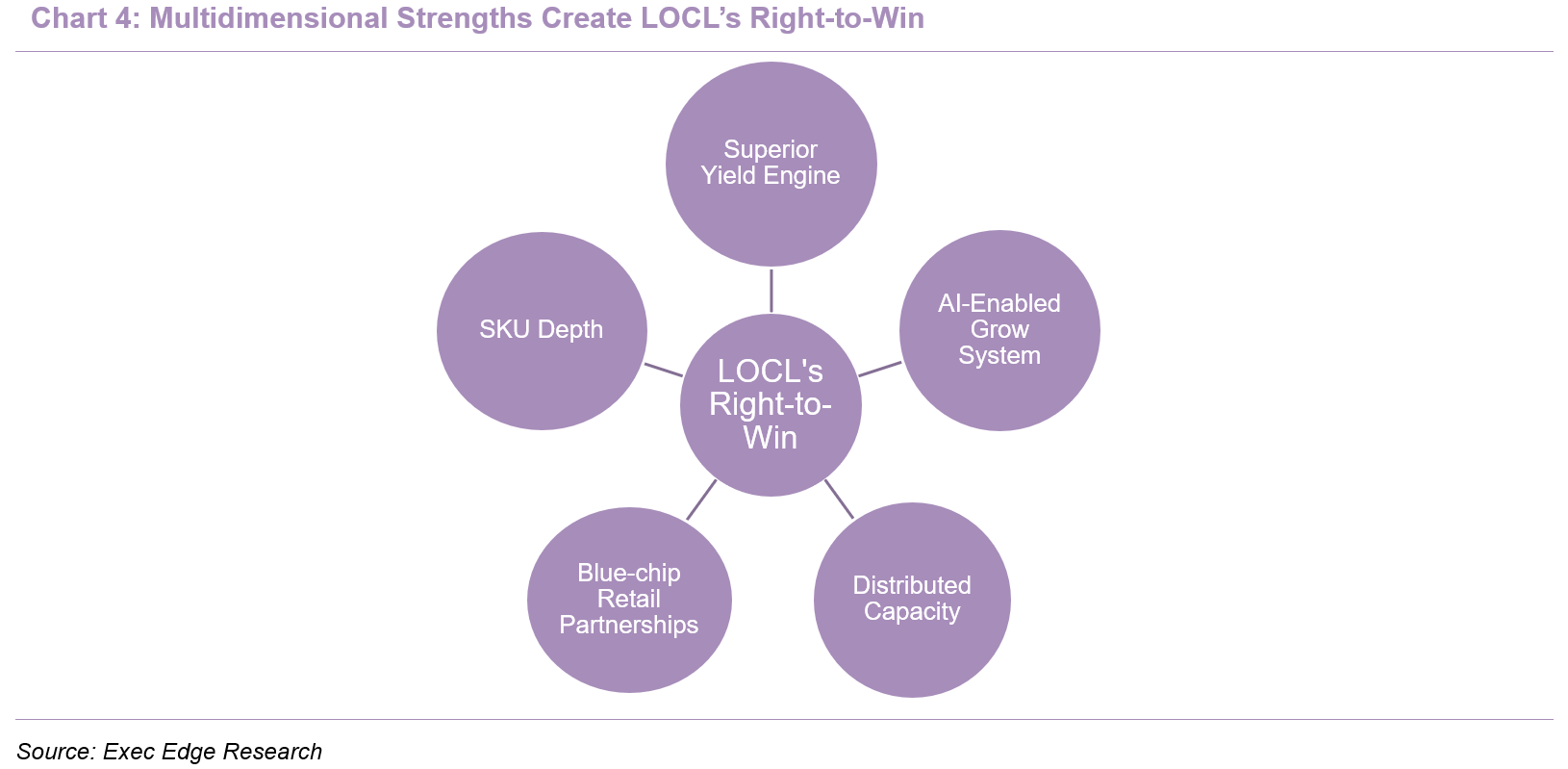

- We believe LOCL’s right-to-win rests on the combination of its proprietary growing technology, distributed capacity, and established retail demand. Stack & Flow provides the production foundation, with demonstrated yield gains across Georgia, Texas, and Washington, while AI-enabled optimization adds an IP-backed data layer that can improve consistency over time. The company’s regional farm network and direct relationships with blue-chip retailers convert this operating platform into demand visibility across ~13,000 retail doors. SKU breadth further extends LOCL beyond core lettuce into adjacent categories such as arugula, baby leaf, organic butter lettuce, and salad kits, supporting broader shelf presence and deeper account penetration. We discuss these elements in detail below.

- Stack & Flow creates a yield and unit-economics moat in CEA. LOCL’s strength starts with the fact that its core growing system is not a conventional greenhouse model, but a hybrid approach that uses a vertical stack nursery for early plant development and then transfers young plants into greenhouse grow-out for final production. This design reduces the square footage required for early-stage growth, increases annual farm turns, and allows the company to use controlled variables such as natural light, temperature, humidity, carbon dioxide, nutrients, and pH balance during the final phase of production. The system is intended to support lower capital expenditure, lower operating expenses, higher labor efficiency, higher yield, and retrofit potential versus other greenhouse and CEA operations.

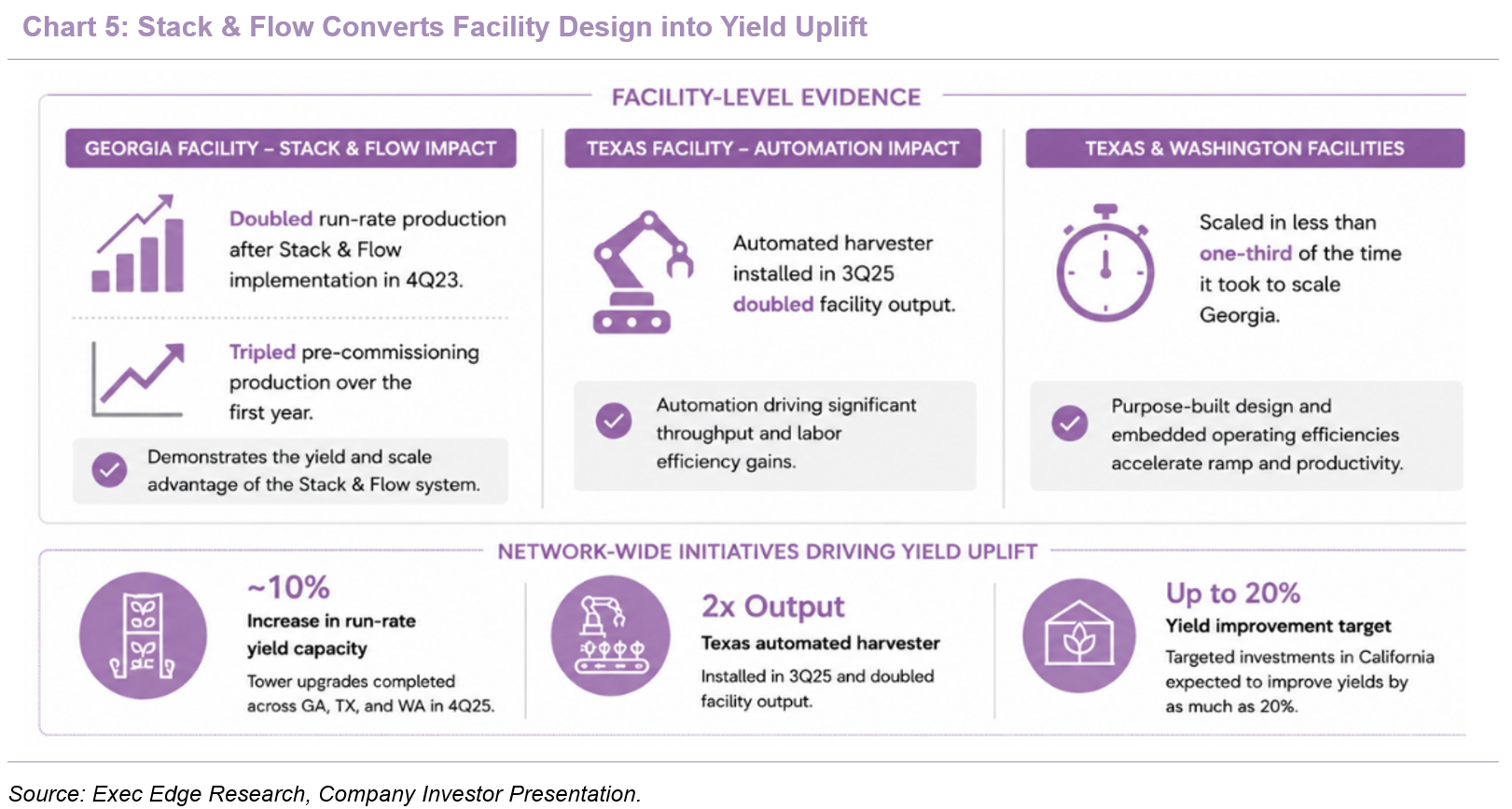

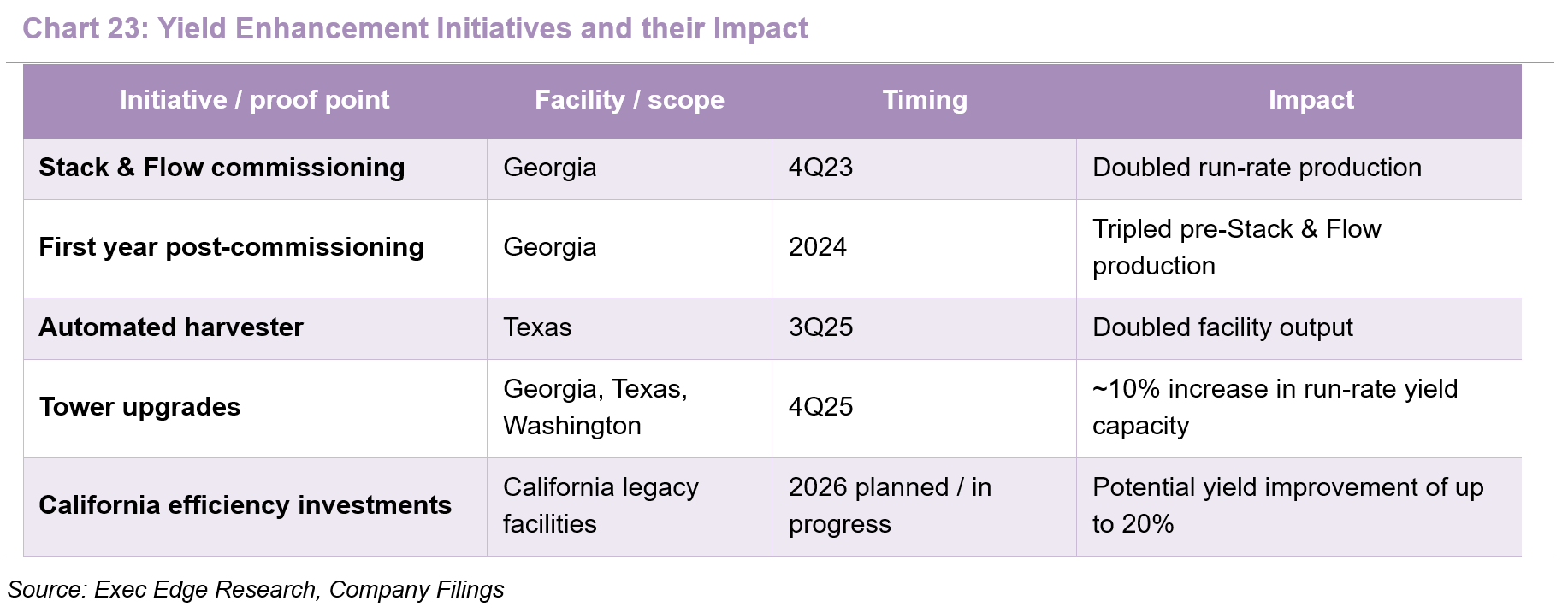

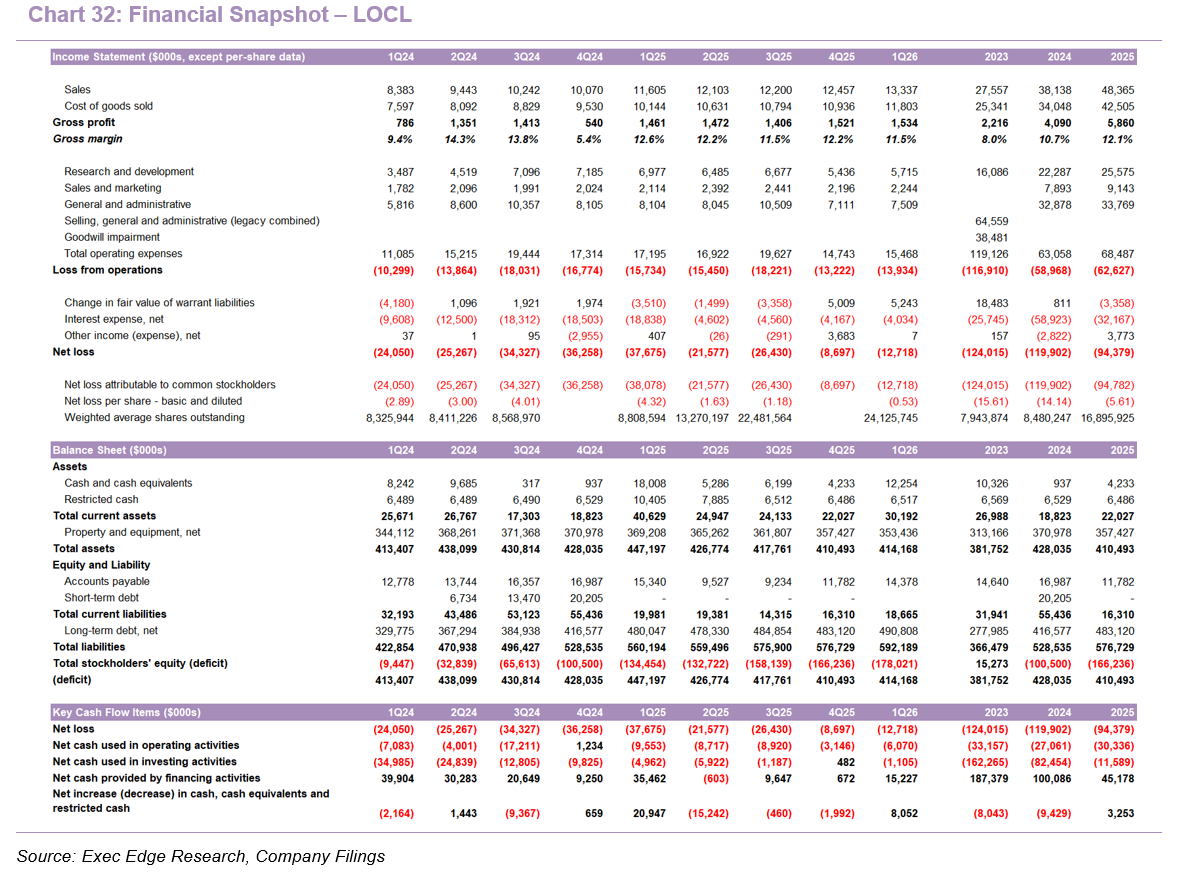

- LOCL has already shown facility-level evidence that the architecture can translate into measurable output gains. Georgia doubled run-rate production after Stack & Flow was implemented in 4Q23 and tripled pre-commissioning production over the first year, while Texas and Washington scaled in less than one-third of the time it took to scale Georgia, supported by purpose-built design and embedded operating efficiencies. Recent operational initiatives further reinforce the yield-led thesis: tower upgrades completed across Georgia, Texas, and Washington in 4Q25 drove an ~10% increase in run-rate yield capacity, the Texas automated harvester installed in 3Q25 doubled facility output, and management is making targeted California investments that it believes can improve yields by as much as 20%. This matters because LOCL’s thesis increasingly depends on extracting more output from its existing asset base rather than simply adding capacity. Stack & Flow gives the company a repeatable production template that can support higher throughput, better cost absorption, and selective retrofit opportunities across the network. The financial read-through is beginning to show in the reported numbers: 2025 sales increased 27% y/y to $48.4 million, while gross profit increased 43% y/y to $5.9 million and company-reported adjusted gross margin remained 29%, suggesting that higher output and facility learning are supporting scale while preserving the underlying production margin.

- LOCL’s AI-enabled growing optimization adds a proprietary data layer to Stack & Flow, strengthening the moat beyond physical greenhouse design. The advantage is that Stack & Flow gives LOCL a repeatable production architecture across the vertical nursery and greenhouse grow-out phases. The company is now layering computer vision, machine learning, and automated environmental controls onto that hybrid system, giving it a way to observe plant growth, analyze environmental variables, and adjust production conditions with greater consistency across facilities. This matters because Stack & Flow can become more valuable as it is operated, not just when it is built. As LOCL captures more crop, facility, climate, and operating-cycle data, the platform should become better at standardizing yield, improving consistency, and transferring best practices across the network.

- The moat was reinforced in February 2026, when LOCL was issued U.S. Patent No. 12,557,741 for “Optimizing Growing Process in a Hybrid Growing Environment Using Computer Vision and Artificial Intelligence.” The patent covers proprietary methods that use computer vision, machine learning, and automated environmental controls to optimize growth across the vertical and greenhouse phases of production. Management highlighted this patent as a formal protection of the proprietary technology underpinning the Stack & Flow platform. LOCL has also been deploying these AI-driven capabilities across its Stack & Flow-enabled facilities, using plant-growth and environmental data to support yield, consistency, and operating precision.

- LOCL’s technology stack can evolve from facility know-how into a learning system. As GA, TX, and WA operate at full harvestable capacity, each crop cycle should add more operational data, helping LOCL refine growing protocols, identify issues earlier, and standardize best practices across the network. In a CEA model where profitability depends on reliable throughput, labor efficiency, energy discipline, and product quality, an IP-backed data layer makes the operating model harder to replicate through capital spending alone.

- The operating leverage signal is also becoming more visible. R&D declined 18% y/y to $5.7 million in 1Q26, with the company attributing the reduction to the maturation of production, harvesting, and post-harvest packaging initiatives tied to commercial-scale Stack & Flow deployment. This supports the view that LOCL’s technology investment is beginning to shift from development intensity toward repeatable operating execution.

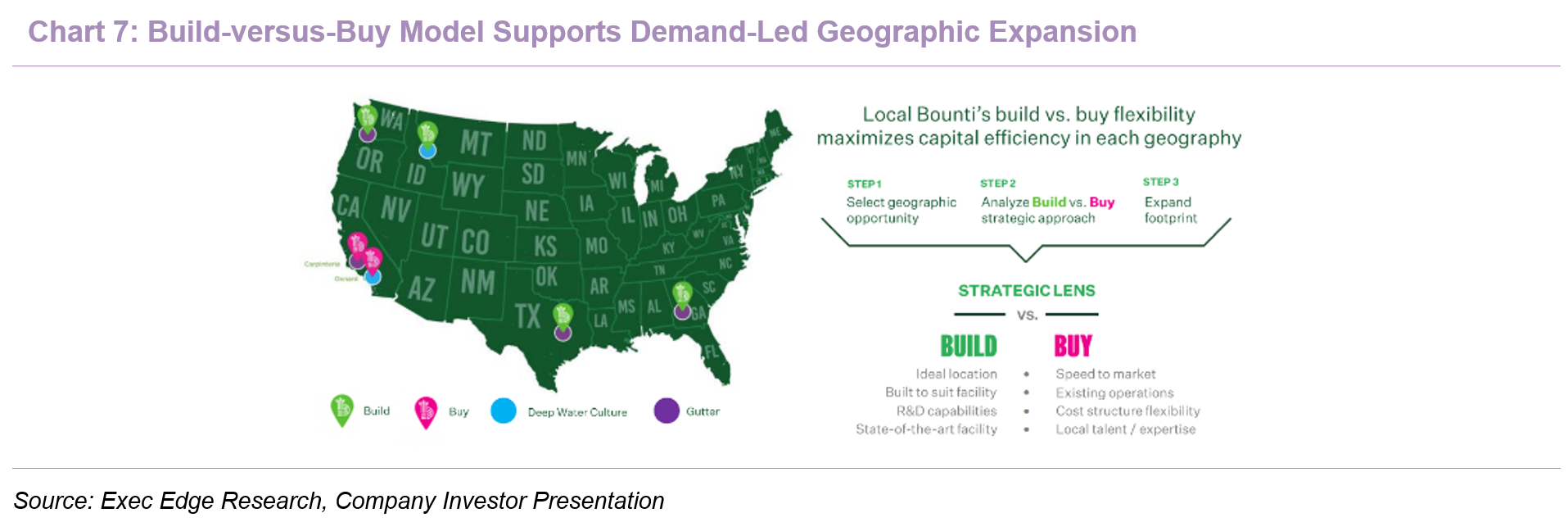

- LOCL’s distributed farm network aligns production capacity with retailer demand, regional freshness, and more efficient service economics. The company’s flexible operating model allows it to build new purpose-designed facilities, expand existing assets, or acquire and retrofit greenhouse facilities with Stack & Flow Technology. This gives LOCL more than one path to enter a geography, which matters in fresh produce because proximity, reliability, and channel commitment are as important as production technology. LOCL regularly assesses future farm locations based on known demand from key existing customers and freight-route optimization, with the objective of limiting transportation cost while improving customer service through consistent delivery schedules. The company also plans to use pre-engineered, pre-fabricated, and standardized components to reduce execution risk when building modular facilities.

- The moat element is the combination of regional production, demand-led expansion, and replicable operating design. LOCL currently serves ~13,000 retail doors across 35 U.S. states and operates a network that includes Stack & Flow-enabled facilities in Georgia, Texas, and Washington, with California legacy greenhouse assets and the Montana headquarters facility. The company’s newer Washington and Texas facilities began shipping product in 2Q24 and scaled in less than one-third of the time it took to scale Georgia, reflecting the benefits of purpose-built design and integrated operating efficiencies. LOCL’s Washington facility also expands distribution capabilities in the Pacific Northwest, while Georgia and Texas give the company a broader South and Southeast platform.

- LOCL is applying the same demand-led framework to future expansion. Additional capacity projects remain under review, including potential Midwest expansion, with timing and scope tied to retailer discussions and product-specific commitments. This reduces the risk of speculative capacity build-out, as new capacity is intended to follow clearer demand signals from blue-chip retailers and distributors. In our view, that creates a practical competitive advantage: while new greenhouse capacity can be built, replicating a multi-region network integrated with retailer planning, committed demand, and facility-level ramp experience should be materially harder.

- Blue-chip retail relationships create a competitive advantage by converting CEA capacity into committed, repeatable demand. LOCL has an established retail footprint, with products sold through ~13,000 retail doors across 35 U.S. states and direct relationships with Albertsons, Sam’s Club, Kroger, Target, Walmart, Whole Foods, Brookshire’s, and H-E-B. The company also reports a differentiated position in living butter lettuce, including an ~80% share of the CEA market in the Western U.S. For a CEA operator, retail access is not just a sales channel; it is what turns installed capacity into predictable volume, better utilization, and a clearer basis for SKU and facility planning. Retail access can therefore become a moat when it supports volume visibility, SKU expansion, freight planning, and facility utilization.

- Recent execution supports this thesis. The company’s three state-of-the-art facilities are operating at full harvestable capacity, with entire run-rate capacity committed to customers. In 1Q26, LOCL secured and launched programs with two additional accounts, including a large premier retail customer covering more than 250 stores with a six-SKU rollout, and a large regional retailer. The company also expanded its retail presence in select southern markets with a new national retailer in 4Q25 and was awarded bids in 1Q26 and early 2Q26 that extend supply programs with multiple national retail accounts through 1Q27, spanning baby leaf lettuce and organic butter lettuce.

- These relationships also improve the quality of LOCL’s growth. Future capacity projects, including potential Midwest expansion, remain tied to retailer discussions and product-specific commitments, which should reduce the risk of building capacity ahead of demand. The existing retail base also gives LOCL a platform to deepen account penetration as new SKUs and incremental facility output become available.

- The financial relevance of this retail base is visible in the improving loss rate. Adjusted EBITDA loss improved 35% y/y to $(5.7) million in 1Q26, while adjusted EBITDA margin improved to (42.7%) from (75.7%) in 1Q25. We would not isolate the improvement to retail wins alone, but it reinforces the broader operating leverage thesis: higher-quality volume, cost discipline, and better facility utilization are starting to translate into a narrower adjusted EBITDA loss rate.

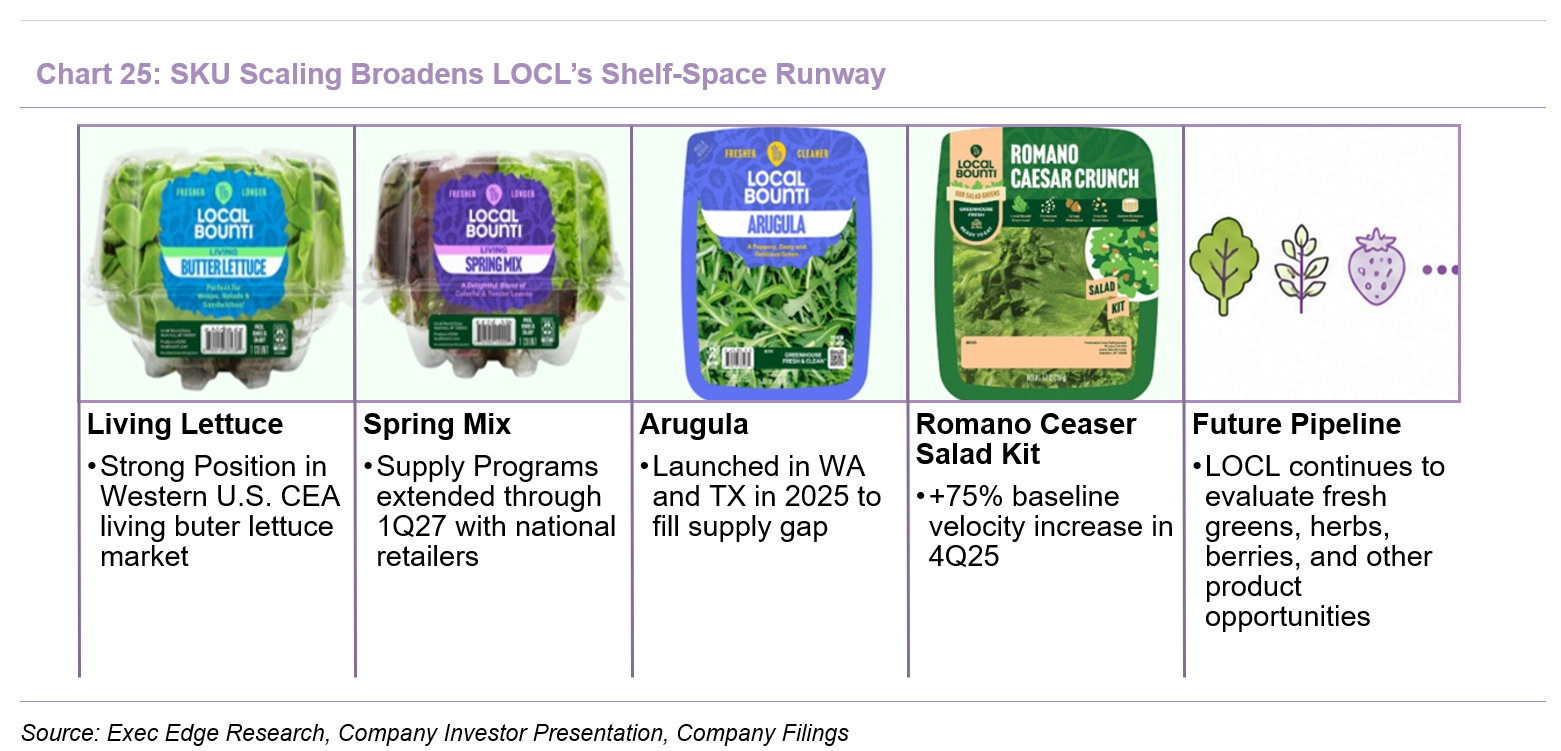

- Broad SKU diversity gives LOCL a shelf-space advantage by moving the business beyond single-product lettuce exposure toward a broader branded fresh-produce platform. LOCL’s portfolio spans living and loose leaf lettuce, arugula, organic and conventional products, cress, and value-added product lines. LOCL’s product breadth has expanded into 25+ retail products across living and loose leaf lettuce, arugula, cress, organic and conventional offerings, baby leaf products, and value-added formats, giving the company more ways to capture shelf space and deepen retailer relevance. The company’s modular distributed model and Stack & Flow Technology are central to this product breadth, as they support SKU diversity and can be expanded to meet customer demand. SKU diversity can help capture more in-store real estate, deepen retailer relationships, and improve consumer relevance across regional markets.

- The company has already shown evidence that product innovation can translate into retail traction. LOCL’s family-sized 10-ounce Romano Caesar Salad Kit in the Pacific Northwest delivered a 75% increase in baseline velocity, measured as units sold per store per week, during 4Q25, and the company was awarded an additional distribution center with a national retailer in 1Q26. LOCL is also pursuing arugula growth after launches at Pasco, WA and Mount Pleasant, TX in 2025, using baby leaf capabilities to address what management describes as unreliable and insufficient conventional arugula supply. In addition, quarterly sales to a major e-commerce and DTC customer continued to perform strongly after growth of more than 600% during 2025.

- This SKU breadth increases LOCL’s relevance to retailers and consumers at the same time. Retailers gain more ways to use LOCL as a dependable supply partner across salads, baby leaf, butter lettuce, arugula, and value-added items, while consumers see a brand associated with greenhouse fresh, non-GMO, sustainably grown, longer-lasting produce. The company also cites meaningful product-quality differentiation, including 10–1,000x less bacteria versus field-grown loose leaf lettuce, which supports its longer shelf-life and reduced-waste positioning. We view that combination of product breadth, freshness, and value-added formats as a practical advantage in a category where shelf availability, shrink reduction, and repeat purchase are critical.

- The SKU expansion strategy is also showing early leverage in reported results. Sales and marketing expense increased only $0.1 million y/y in 1Q26, while sales increased $1.7 million y/y, suggesting that incremental revenue growth is not currently requiring a disproportionate increase in selling expense. This supports the view that value-added SKUs can deepen retail relevance while leveraging the existing go-to-market infrastructure.

Industry Trends and Company Positioning

Large Produce TAM Supports LOCL’s SKU Expansion Runway

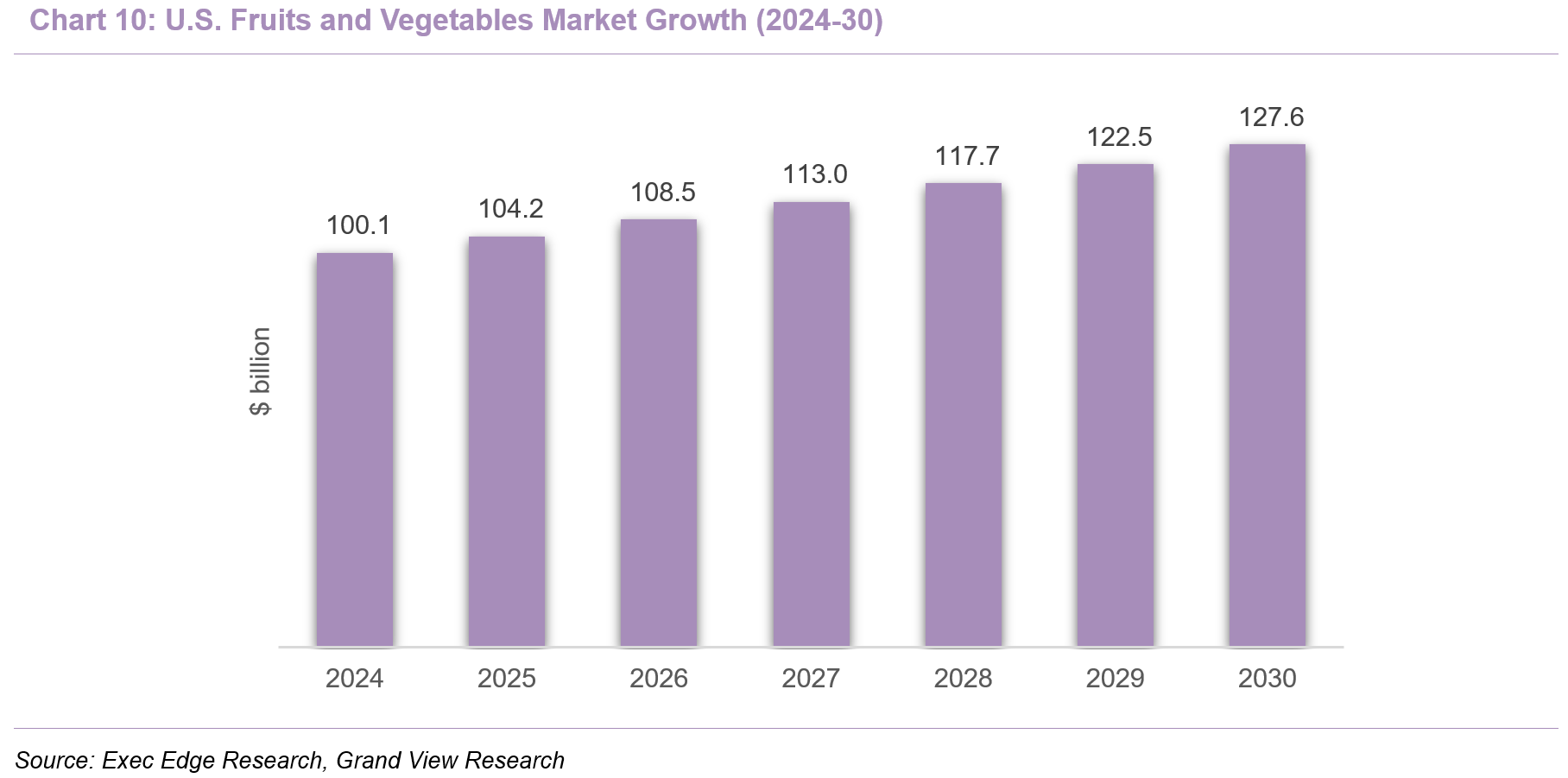

- The U.S. fruit and vegetable market represents a large and expanding addressable base, with leafy greens providing a focused entry point within the broader fresh-produce category. LOCL’s opportunity sits within a U.S. produce market that continues to expand as consumers prioritize health, fresh foods, convenience, and locally sourced products. Grand View Research estimates the U.S. fruits and vegetables market at $100.1 billion in 2024, with the market expected to reach $127.6 billion by 2030, implying a 4.1% CAGR from 2024-30. Fresh fruits and vegetables dominate the category, accounting for 80.8% of the market in 2023, which is particularly relevant for LOCL’s positioning in fresh leafy greens and salad-oriented products. Key growth drivers include rising health awareness, increasing demand for fresh and locally sourced produce, growing adoption of online grocery and delivery, and higher consumer interest in plant-based diets and healthier snacking. Supermarkets and hypermarkets remain the largest distribution channel, with more than 58% share in 2023, while online is expected to be the fastest-growing channel at a 5.2% CAGR over the forecast period. This backdrop supports LOCL’s SKU expansion strategy, as the company’s CEA model targets fresh, local, sustainable, and retail-distributed produce within a broader category benefiting from favorable consumer and channel trends.

- Produce growth is increasingly becoming a frequency and occasion-expansion story, not just a category-growth story. FMI’s 2026 produce research notes that shoppers continue to value fresh fruits and vegetables, but only 31% eat them daily, creating what FMI describes as a frequency gap. Cost remains a constraint, with 44% of consumers eating fresh produce three days per week or less, but nearly half of shoppers still cite health as a primary motivation for produce consumption. The category implication is that growth depends on making produce more affordable, convenient, and routine, with retailers using snacking, smaller pack sizes, prepared formats, and meal-building solutions to increase usage occasions beyond the traditional weekly stock-up trip.

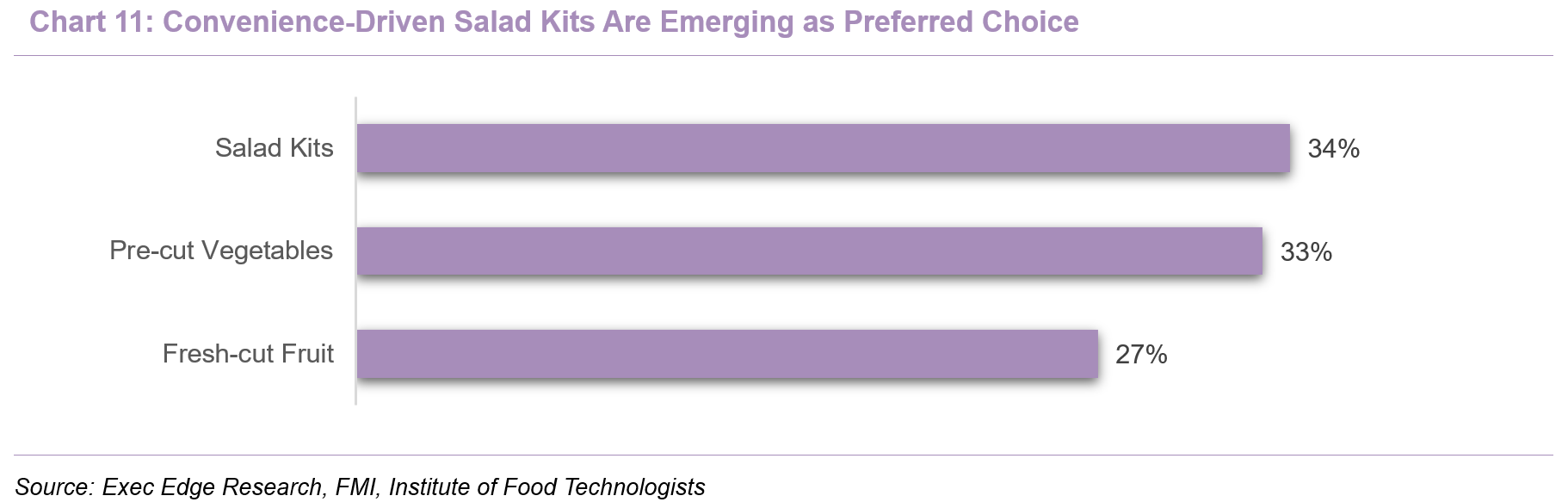

- Generational change and convenience-led formats are reshaping how produce is discovered, purchased, and consumed. FMI notes that fruit now accounts for nearly 56% of total produce volume, supported by Millennials and Gen Z, who over-index on fruit purchases and use produce more frequently in breakfast and snacking occasions. Vegetables remain more dinner-dependent, making convenience and ready-to-use formats important tools for expanding consumption across dayparts. Salad kits are one of the clearest examples: FMI data cited by Food Technology shows that 34% of consumers frequently purchase packaged salad kits, ahead of 33% for precut vegetables and 27% for fresh-cut fruit. This supports the retailer opportunity to reposition vegetables through ready-to-assemble meals, recipe content, and value-added formats, which aligns with LOCL’s move beyond core lettuce into salad kits, arugula, baby leaf, and other higher-utility produce SKUs.

- We believe LOCL is well positioned to benefit from this trend because its product roadmap is expanding in the same direction as consumer demand, from core lettuce toward broader fresh, convenient, and value-added produce formats. The company’s portfolio now includes living and loose leaf lettuce, arugula, organic and conventional offerings, cress, baby leaf products, and salad kits, giving LOCL more ways to participate in the broader U.S. produce TAM rather than remaining dependent on a single lettuce SKU. LOCL’s value-added SKU activity, including salad kits, has shown early retail traction, while quarterly sales to a major e-commerce and DTC customer continued to perform strongly after growth of more than 600% during 2025. The company is also pursuing arugula growth following launches at Pasco, WA and Mount Pleasant, TX. In our view, SKU expansion increases LOCL’s retail relevance, supports shelf-space gains, and helps monetize fixed facility capacity through higher-utility product formats.

CEA Reset Rewards Operators with Input-Cost Resilience and Unit Discipline

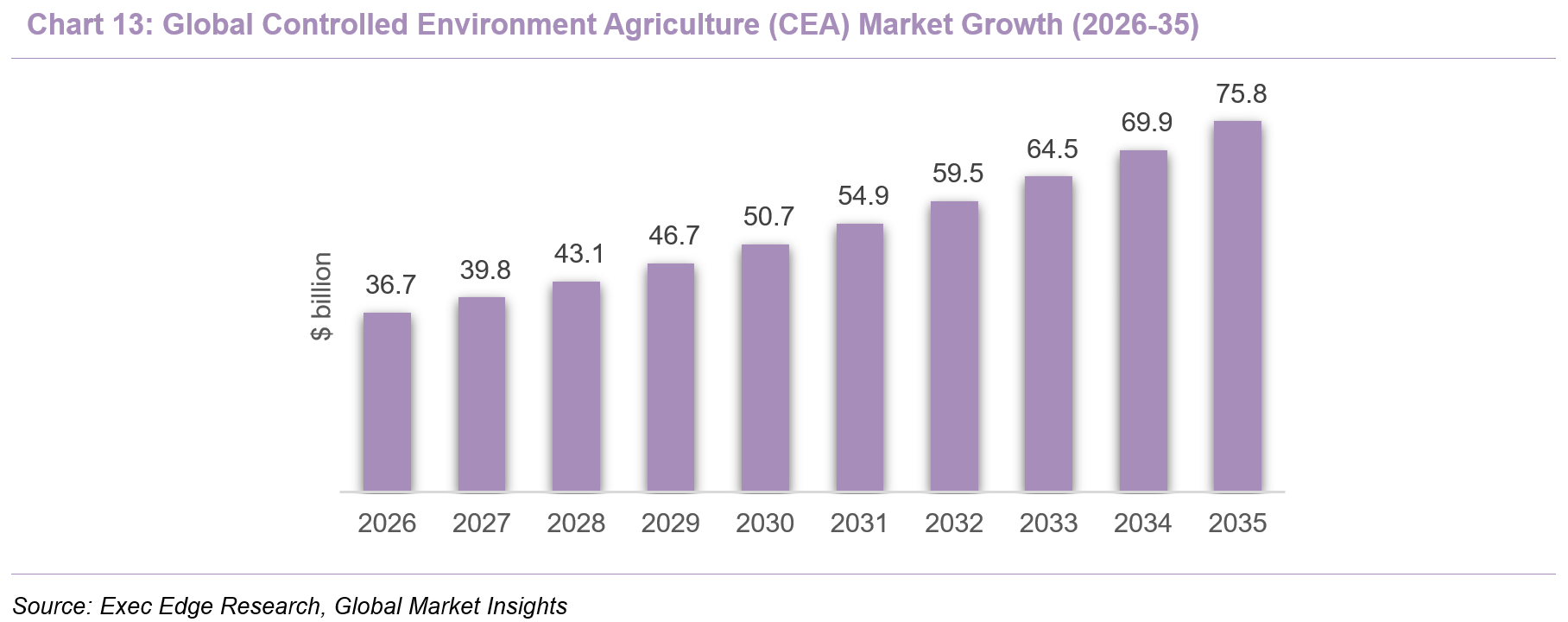

- CEA remains a structurally attractive category, but the sector’s focus has shifted from capacity growth to execution, unit economics, and capital discipline. Global Market Insights estimates the controlled environment agriculture market at $33.7 billion in 2025, with the market expected to reach $75.8 billion by 2035, implying an 8.4% CAGR from 2026-35, driven by sustainable food production, climate resilience, and automation adoption. However, the funding environment remains selective, with capital increasingly favoring operators that can demonstrate throughput, customer demand, and cost control over those dependent on repeated external funding. AgFunder’s Global AgriFoodTech Investment Report 2026 shows that global AgriFoodTech funding was $16.2 billion in 2025, down only 3% y/y, while deal count fell 12%, implying that fewer companies are receiving funding even as overall capital levels stabilize. The pressure is more acute in indoor and novel farming systems: AgFunderNews reported that Novel Farming Systems funding fell from $336 million in H1 2024 to $144 million in H1 2025, while Agriculture Dive, citing PitchBook, reported that at least 28 indoor farming companies had declared bankruptcy or ceased operations. High-profile failures have reset investor expectations, including Bowery’s shutdown after raising more than $700 million, AppHarvest’s Chapter 11 filing in 2023, and AeroFarms’ restructuring through bankruptcy before emerging with a narrower operating focus. The key takeaway is that CEA remains a structural growth story, but capital markets are no longer underwriting growth without proof of throughput, customer demand, cost absorption, and facility-level profitability. As a result, future winners are more likely to be operators that can demonstrate repeatable yield, retailer-backed capacity planning, and a realistic route to cash generation.

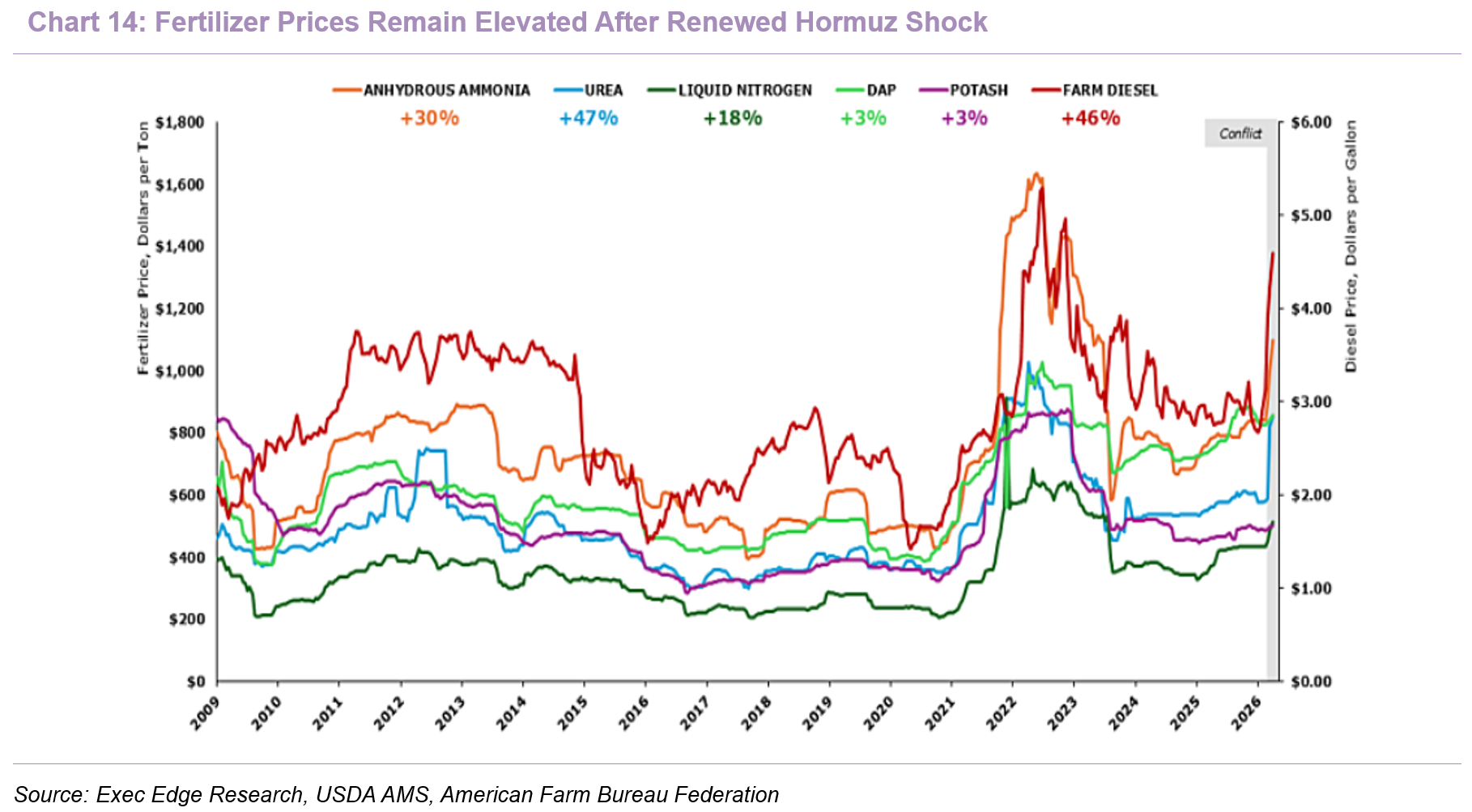

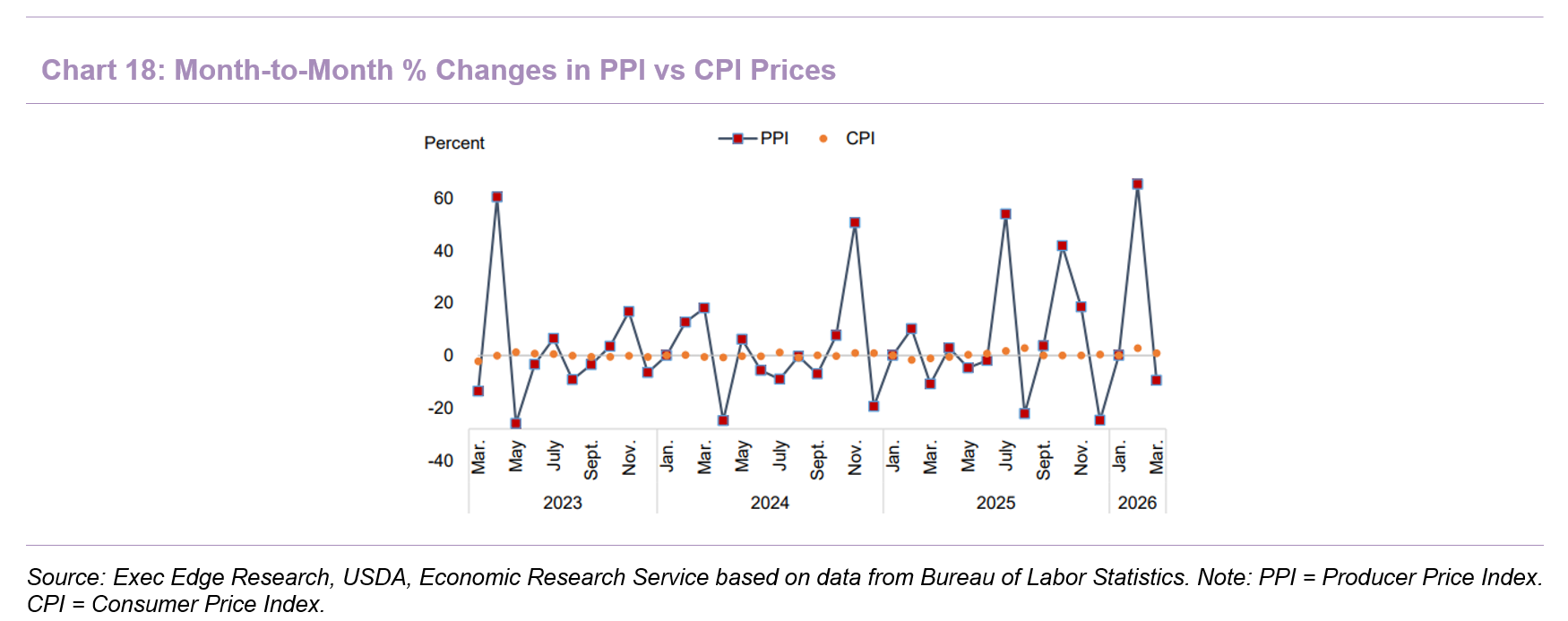

- Outdoor-ag inflation is reinforcing the strategic value of CEA operators that can reduce exposure to fertilizer and long-haul freight shocks while potentially participating in stronger retail produce pricing. BLS data for May 2026 show lettuce prices rose 15.9% m/m and 24.9% y/y, with fresh fruits and vegetables up 6.7% y/y, even as food-at-home CPI increased 2.7% y/y compared with 2.9% y/y in April 2026.

- Fertilizer has become a key outdoor-ag pressure point as Hormuz disruption exposes concentrated global supply chains. NDSU’s March 2026 Agricultural Trade Monitor identified the Strait of Hormuz as a fertilizer chokepoint, with Persian Gulf countries accounting for ~43% of seaborne urea exports, ~44% of seaborne sulfur trade, 27% of global ammonia exports, and 16% of phosphate exports. The American Farm Bureau Federation reported that nitrogen fertilizer prices rose more than 30% after Middle East tensions escalated, urea prices increased 47% since the end of February, and combined fuel and fertilizer costs increased ~20%-40%, nearing 2021-22 levels. Farmdoc also noted that urea prices rose 28.2% within three weeks of the Hormuz closure, while its scenario work shows DAP could rise from a February 2026 pre-crisis benchmark of $622/st to $866-$945/st under contested-transit or extended-conflict scenarios.

- Diesel and refrigerated freight remain another pressure point for field-grown produce. Fresh produce is particularly exposed because it often moves in refrigerated trucks that require fuel for both transport and cooling. In May 2026, the PPI for No. 2 diesel fuel increased 106% y/y, while the PPI for truck transportation of freight increased 17.3% y/y, reinforcing how fuel and freight inflation can move through field-grown produce supply chains.

- Tariffs can amplify fertilizer cost pass-through when supply chains are already disrupted. NDSU’s January 2026 Agricultural Trade Monitor found that fertilizer tariff pass-through exceeded 100% during peak tariff months, as market uncertainty and supply-chain disruption amplified costs beyond the direct tariff rate. AgWeb’s summary of the same NDSU work quantified the effect for DAP, showing a 342% spot-price pass-through rate and a 156% retail pass-through rate, while noting that MAP and urea showed similar U.S.-Canada price divergence.

- CEA models can strengthen retailer supply resilience by reducing exposure to some of the cost vectors pressuring outdoor production. While CEA does not eliminate inflation risk, it can reduce direct dependence on broad-acre fertilizer application, weather-sensitive field yields, and long-haul refrigerated freight lanes. For LOCL, this supports the retail thesis: closer-to-market production and committed capacity can help retailers protect availability, freshness, and replenishment consistency during periods of outdoor-ag cost volatility.

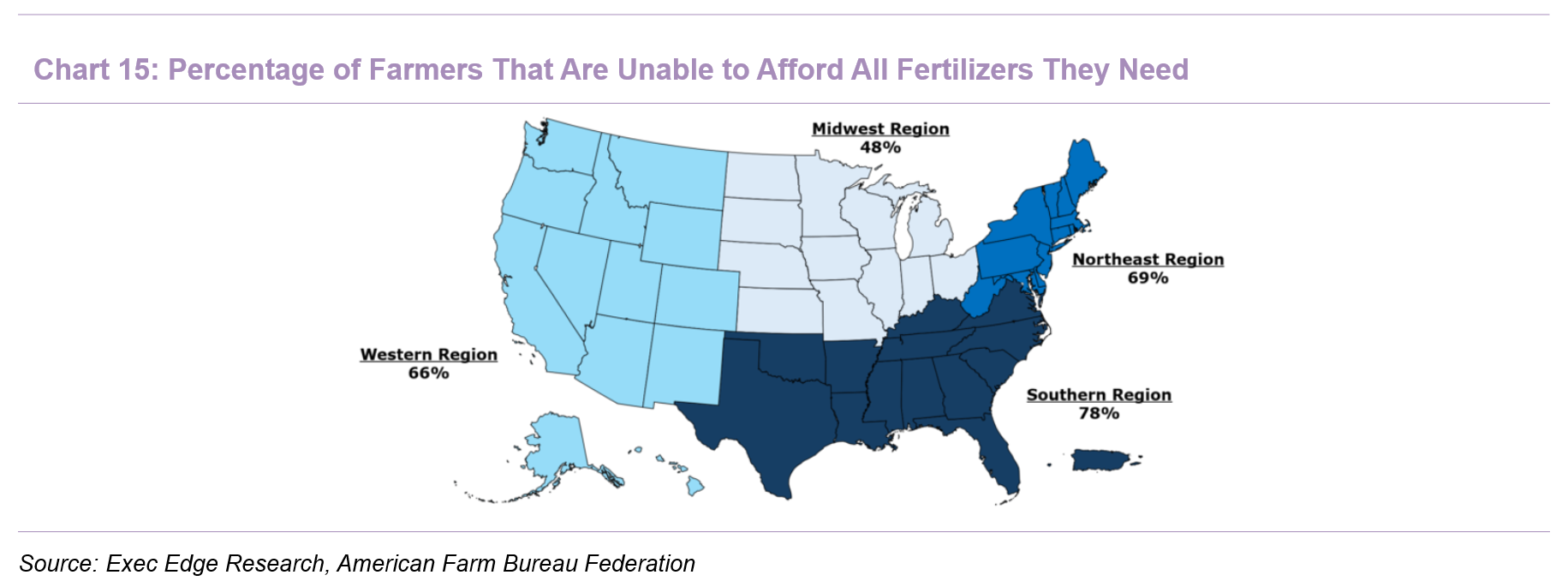

- Fertilizer affordability is becoming a direct outdoor-ag production constraint, not just a commodity-price issue. The American Farm Bureau Federation’s April 2026 Fertilizer Availability Survey, based on responses from more than 5,700 farmers, found that ~70% of respondents could not afford all the fertilizer they needed. The constraint was most acute in the South, where 78% reported affordability pressure and only 19% had pre-booked fertilizer ahead of the season. This matters because fertilizer affordability can become a supply and margin risk for outdoor growers, forcing lower application rates, acreage adjustments, or higher cost absorption. Regional CEA models can reduce direct dependence on broad-acre fertilizer application and some long-haul field-ag cost pass-through, even though they do not eliminate input-cost exposure.

- Energy, labor, and automation discipline are now central to CEA unit economics, making productivity per dollar invested in facility capacity more important than headline capacity growth. The CEAg World x Agritecture 2025 Global CEA Census shows that 47.13% of respondents cited high energy costs as a key challenge, followed by labor costs at 45.98%, difficulty accessing funding at 29.89%, and financing at 20.69%. At the same time, agriculture remains labor-constrained, with USDA ARS citing demographic shifts, rising labor costs, and limited skilled-worker availability, while the American Farm Bureau Federation notes that fruit and vegetable producers can spend up to 40% of production expenses on labor. For CEA operators, this creates both a cost challenge and an automation opportunity, as controlled facilities can standardize repetitive workflows across seeding, harvesting, packaging, and food safety. We believe the next phase of CEA competition is likely to reward operators that can lower cost per pound through energy discipline, automation, climate control, and crop-cycle optimization, rather than simply adding square footage.

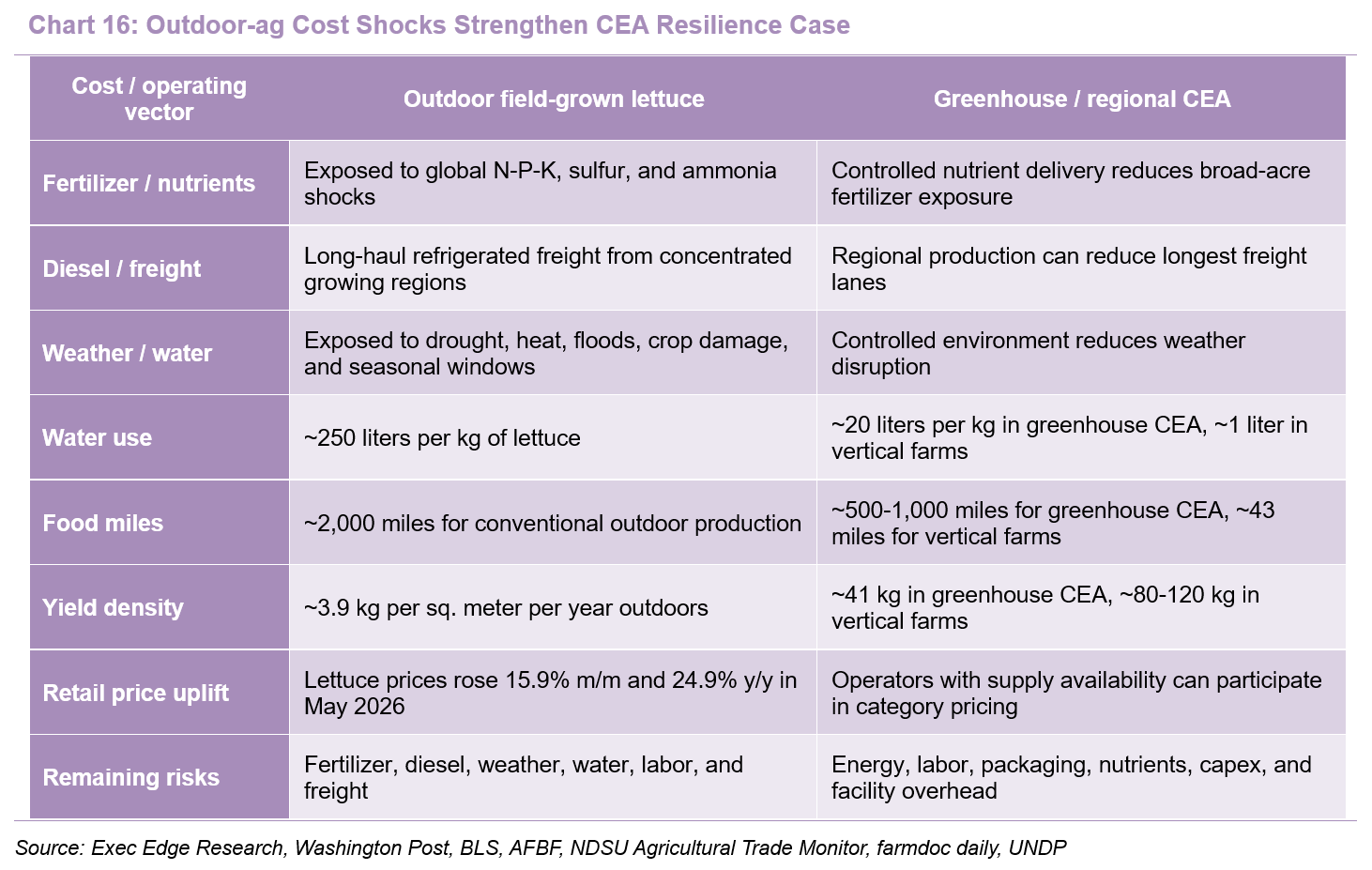

- Water scarcity, land constraints, and sustainability keep CEA strategically relevant, but operators will increasingly need to pair environmental benefits with viable economics. CEA’s long-term value proposition remains strongest in resource-constrained produce categories where consumers and retailers need reliable year-round supply, lower pesticide exposure, and reduced dependence on weather-sensitive field production. UNDP’s 2025 controlled environment agriculture paper states that CEA can reduce agricultural water usage by 53-98%, reduce chemical usage by as much as 100%, and use less land to produce the same amount of food as conventional farming.

- The sustainability case is especially visible in lettuce. UNDP’s Controlled Environment Agriculture for Sustainable Development compared conventional outdoor farming, greenhouses, and vertical farms, showing that conventional outdoor lettuce production uses 250 liters of water per kg, versus 20 liters for greenhouse production and 1 liter for vertical farming. It also compares typical food miles at 2,000 miles for conventional outdoor farming, 500-1,000 miles for greenhouse production, and 43 miles for vertical farms. Yield intensity is also materially higher, with lettuce output of 3.9 kg per square meter per year outdoors, 41 kg in greenhouses, and 80-120 kg in vertical farms.

- Productivity vs. Sustainability. The same UNDP paper also notes that current CEA systems are often energy-intensive and costly to establish. USDA ERS similarly states that CEA systems help producers control factors such as temperature, wind, lighting, and precipitation, enabling production while limiting adverse weather and pest pressure. This duality is important: sustainability is a demand enabler, but not a standalone moat. Retailers and consumers may value local, sustainable, pesticide-light produce, but the product must still compete on price, quality, availability, and freshness. The conclusion is that CEA has a durable role in food systems, particularly for high-value produce, but the winners will be the operators that translate sustainability claims into cost, consistency, and supply-chain reliability.

- LOCL is positioned to benefit from this industry reset because its model combines CEA input-cost resilience with demand-backed utilization and yield-led operating discipline. Its regional Stack & Flow-enabled network can reduce direct exposure to broad-acre fertilizer application, weather-driven yield volatility, and long-haul refrigerated freight relative to outdoor field production, while still recognizing that CEA operators face their own cost pressures across energy, labor, packaging, and facility overhead. That matters more in a market where lettuce prices are rising sharply at retail, as operators with available, local, contracted supply can potentially participate in stronger category pricing while reducing exposure to some of the outdoor-ag cost pressures behind that inflation. LOCL’s three Stack & Flow-enabled facilities in Georgia, Texas, and Washington are operating at full harvestable capacity with run-rate capacity committed to customers, while tower upgrades, automated harvesting, and AI-enabled crop optimization – including a 2026 patent – support the company’s effort to convert category pricing strength into higher throughput, better utilization, and progress toward positive adjusted EBITDA.

Retailers Shift Toward Resilient, Local Produce Supply Chains

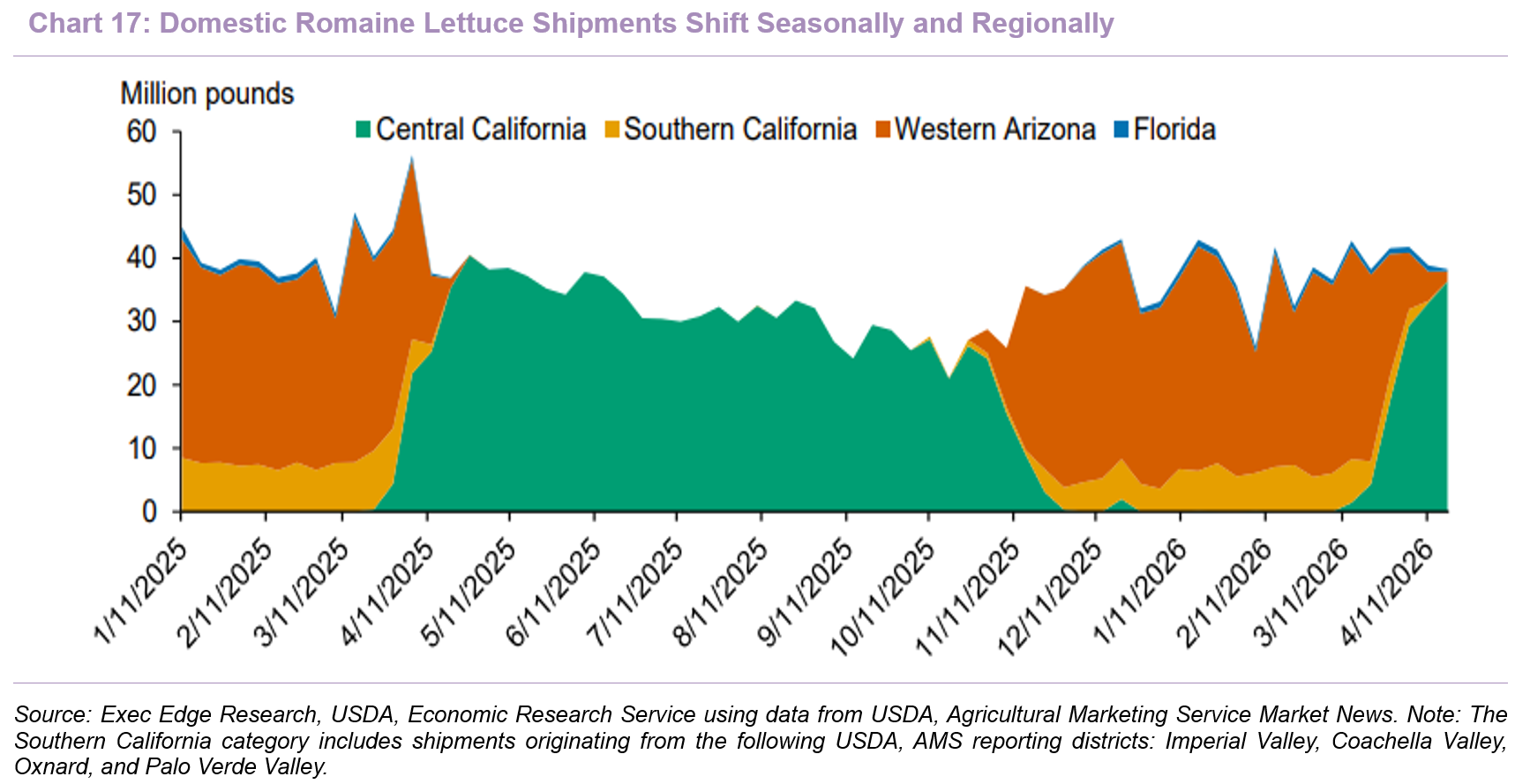

- Retailers are increasingly treating local and regional sourcing as a supply-chain resilience tool, not just a consumer-marketing attribute. Fresh lettuce supply remains concentrated and seasonal, creating exposure to weather, water, acreage shifts, transportation lanes, and regional crop windows. USDA ERS’ Vegetables and Pulses Outlook: April 2026 shows that domestic romaine lettuce shipments transition sharply from Western Arizona in the winter to Central California in the spring and summer, with Southern California and Florida contributing smaller seasonal volumes. The same report estimates 10.11 billion pounds of fresh domestic lettuce availability in 2025, up 4% y/y, with U.S. production accounting for 93% of availability. Within that market, romaine / leaf lettuce represented a record 62% of total fresh lettuce availability in 2025, versus a 25% average in 1999-2001, confirming the long-term mix shift toward leafy formats most relevant to salad and fresh-meal occasions. However, 1Q26 domestic shipments were lower y/y for iceberg, romaine, and leaf lettuce, down 11%, 5%, and 13%, respectively, after rain and high heat in the Arizona / California desert region reduced yields and quality. We believe this supports the case for regional CEA supply as a resilience layer in leafy greens.

- Producer-level volatility in fresh vegetables reinforces why retailers value supply models that can deliver more predictable availability and pricing. Retailers need reliable shelf availability without disrupting price perception, but fresh vegetable procurement costs can move sharply before those pressures can be passed through, creating margin and merchandising risk. USDA ERS’ Vegetables and Pulses Outlook: April 2026 shows that fresh vegetable producer prices were far more volatile than retail prices from 2023 through early 2026, with repeated month-to-month PPI swings while CPI moved more gradually. In early 2026, fresh vegetable PPI rose 88% y/y in February and remained ~90% above March 2025 in March, while fresh vegetable CPI increased 5% y/y in February and 8% y/y in March. USDA ERS attributes this pattern to supply shifts across key growing regions, weather disruptions, and winter production transitions. For retailers, localized and controlled supply can help reduce exposure to upstream volatility, supporting more stable procurement, fewer stockouts, and better category planning – all of which align with LOCL’s regional CEA network model.

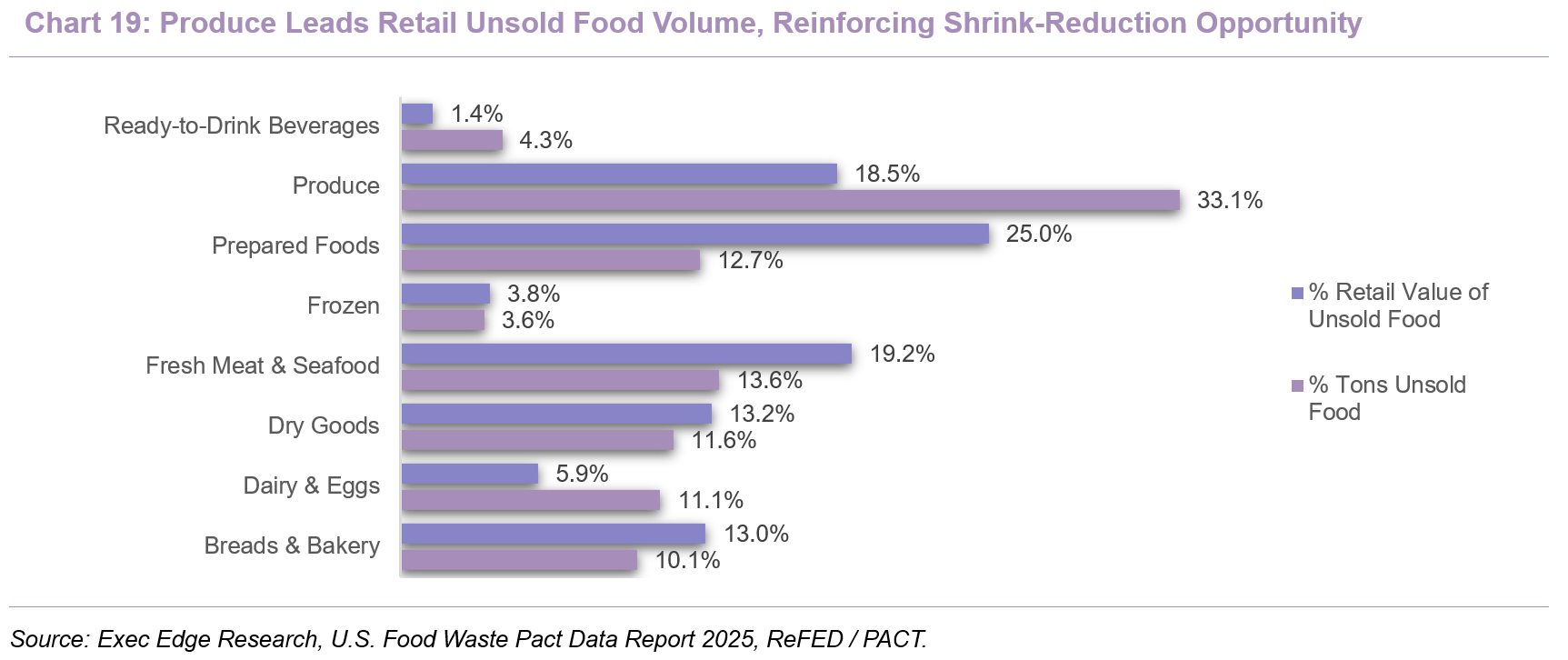

- Local sourcing can improve produce economics by reducing freshness risk, shrink, and service variability across retail supply chains. Produce is the most exposed department for shrink because it is perishable, quality-sensitive, and subject to demand volatility. ReFED estimates that U.S. retailers generated 3.98 million tons of surplus food in 2024, with 33.1% coming from produce, the largest category contribution. A separate ReFED / PACT 2025 data report states that produce led retail unsold food volume with 1.3 million tons, about 2x any other department. These data points strengthen the commercial case for shorter, more responsive produce supply chains: reducing travel time can help preserve shelf life, reduce quality degradation, and give retailers more flexibility to match deliveries with demand. For retailers, the value of local sourcing is increasingly economic as much as promotional: shorter supply chains can support fresher product, lower shrink, more reliable replenishment, and fewer miles between production and consumption, all of which reinforce the strategic logic of LOCL’s distributed farm network.

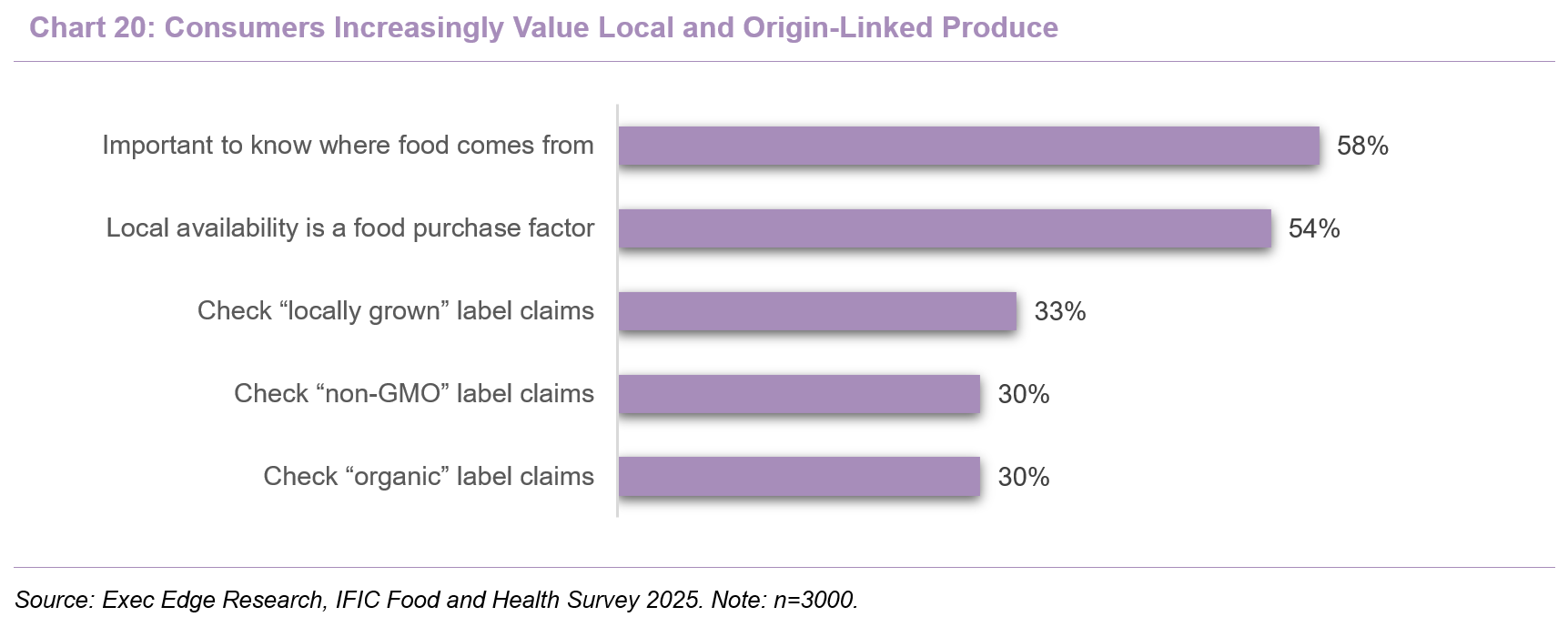

- Consumer preference is reinforcing local sourcing as a produce-department priority, giving retailers another reason to diversify toward regional supply models. Local produce has evolved from a seasonal merchandising claim into a shopper-facing attribute tied to freshness, transparency, and confidence in food origin. FMI’s Power of Produce 2025, cited by Supermarket News, found that 60% of consumers want produce departments to carry more locally grown items, while 43% said knowing where produce was grown can be a purchase priority. That finding is consistent with IFIC’s 2025 Food & Health Survey, which found that approximately six in ten Americans say it is important to know where their food comes from, up 8 points from 2017, while 54% cite local availability as a food purchase factor. IFIC also found that 33% of consumers check for locally grown claims, compared with 30% for organic and 30% for non-GMO. For retailers, regional supply therefore supports both operating resilience and shopper relevance. A produce department that can offer local products more consistently may be better positioned to communicate freshness, reduce distance-to-shelf, and differentiate assortment in a category where origin, quality, and trust influence purchase decisions.

- Local sourcing is becoming more attractive to retailers because fresh produce remains structurally dependent on refrigerated trucking, making distance-to-shelf a direct input into delivered cost, freshness, and service reliability. USDA AMS’ Agricultural Refrigerated Truck Quarterly, 1Q26 reported 7.76 million tons of U.S. truck shipments of fresh produce in 1Q26, with Mexico, the Pacific Northwest, Arizona, California, and Florida representing the largest shipment origins, highlighting how fresh produce supply chains regularly move large volumes across long regional corridors. The same report shows that refrigerated truck rates remain material across route lengths, with 501-1,500-mile rates increasing 15% q/q and 11% y/y in 1Q26, while USDA also notes that diesel fuel is a significant expense for fruit and vegetable movements and a proxy for truck-rate trends. Separately, a 2024 study summarized in 2025 found that trucks move 83% of U.S. agricultural products and 92% of dairy, fruit, vegetables, and nuts. For retailers, regional sourcing can reduce dependence on long-haul refrigerated freight, limit exposure to diesel and lane-rate volatility, and support the freshness and replenishment consistency that distributed CEA networks like LOCL are designed to provide.

- Oil and diesel volatility, and the rise in fertilizer prices due to the Iran war, further strengthen the freight-cost case for regional produce sourcing. Fresh produce is particularly exposed because many products move long distances in refrigerated trucks, making fuel costs a direct input into delivered cost, procurement volatility, and retail pricing pressure. Recent Middle East-related oil volatility and elevated U.S. diesel prices reinforce how quickly energy shocks can move into produce supply chains, particularly for retailers dependent on long-haul refrigerated freight from concentrated growing regions. While local sourcing does not eliminate freight or energy exposure, it can reduce dependence on the longest lanes, limit diesel-surcharge pressure, and improve replenishment flexibility. This increases the strategic value of regional production, as retailers look to build more resilient sourcing models around closer-to-market supply.

- We believe LOCL is well positioned to benefit from the retailer shift toward resilient local supply because its operating model is built around distributed, year-round regional production and direct retail relationships. The company serves ~13,000 retail doors across 35 U.S. states and evaluates future farm locations based on known customer demand and freight-route optimization, directly aligning with retailer priorities around freshness, replenishment reliability, and lower freight exposure. Recent commercial activity reinforces this fit: LOCL expanded retail presence in select southern markets with a new national retailer in 4Q25 and secured two additional accounts in 1Q26, including a large premier retail customer covering more than 250 stores with a six-SKU rollout. The company also received bid awards extending multiple national retail supply programs through 1Q27 across baby leaf lettuce and organic butter lettuce. In our view, this gives LOCL a clearer demand bridge from industry trend to company execution, as local supply needs translate into retail programs, SKU expansion, and capacity planning.

Management Team

Management Depth Supports LOCL’s Shift from Build-Out to Scaled Execution

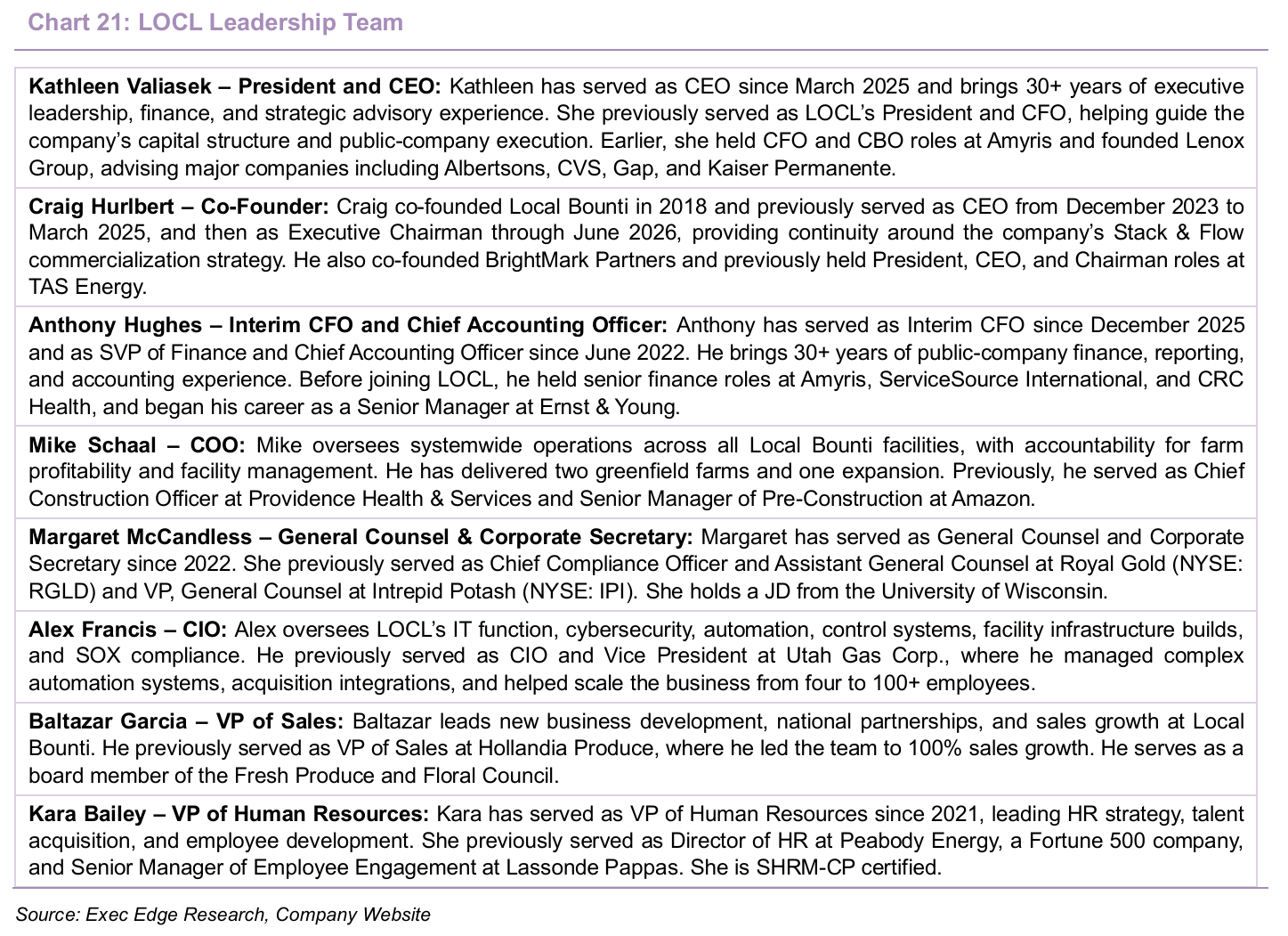

- Led by CEO Kathleen Valiasek, LOCL’s management structure combines finance and public-company expertise, operational scale-up experience, and co-founder board continuity. Kathleen brings 30+ years of executive leadership and prior CFO experience at Amyris and Local Bounti, where she has helped steer the company’s capital structure and growth since 2021. Co-founder Craig Hurlbert preserves direct continuity with the company’s Stack & Flow technology and commercialization history since its 2018 founding. Interim CFO and CAO Anthony Hughes adds 30+ years of public-company accounting and reporting experience, including a prior CAO role alongside Kathleen at Amyris. The operating bench, led by COO Mike Schaal, who has delivered two greenfield farms and one expansion, pairs construction, supply chain, sales, and marketing leadership drawn from Providence, Amazon, Clorox, CPG, and major retail backgrounds. The result is a leadership structure well matched to LOCL’s next phase of scaled CEA execution.

Growth Strategy

Disciplined Growth Strategy Prioritizes Yield, Mix, and Demand-Led Expansion

- LOCL’s growth strategy is centered on disciplined execution, with management prioritizing asset productivity, channel quality, SKU scaling, and demand-led capacity expansion over rapid footprint buildout. The company is leveraging its fully utilized production base and established retail relationships to improve yield, optimize customer mix, and expand product penetration across existing accounts. At the same time, LOCL is gating incremental capacity against retailer commitments and exploring strategic partnerships to align growth with capital efficiency. This approach reflects a shift toward higher-quality revenue growth, with improved visibility, stronger unit-economics potential, and reduced execution risk forming the core of the strategy. Financially, the strategy is intended to drive continued sequential revenue improvement, reduce the adjusted EBITDA loss rate, and move LOCL toward positive adjusted EBITDA through higher facility output, stable adjusted gross margins, lower adjusted G&A, price escalation, and yield increases driven by AI, rapid R&D, etc.

- The company is prioritizing growth from the existing production base, with yield improvement and facility efficiency positioned as the near-term path to higher throughput, revenue conversion, and margins. LOCL’s three Stack & Flow-enabled facilities in Georgia, Texas, and Washington are operating at full harvestable capacity, and the entire run-rate capacity is committed to customers, shifting the operating agenda from bringing assets online to extracting more output from assets already in service. The company’s tower upgrades across GA, TX, and WA were completed in 4Q25 and delivered an ~10% increase in run-rate yield capacity, helping the network reach the highest yields in company history. LOCL is also making selective efficiency investments in its California facilities, which management believes can improve yields by as much as 20%, resulting in increased throughput and enhanced margins. This strategy is reinforced by the Texas automated harvester, which doubled facility output, and by AI-driven plant-growth analysis deployed across Stack & Flow facilities.

- Improving Utilization: Before adding large amounts of new capacity, management is focused on improving utilization, labor productivity, and output per installed asset, which should support revenue growth and adjusted EBITDA improvement as fixed costs are absorbed across higher facility throughput.

- LOCL is shifting commercial growth toward higher-quality volume, using retail wins and supply extensions to improve demand visibility rather than chasing volume for its own sake. LOCL currently services ~13,000 retail doors across 35 U.S. states, primarily through direct relationships with blue-chip retailers including Albertsons, Sam’s Club, Kroger, Target, Walmart, Whole Foods, Brookshire’s, and H-E-B. Recent commercial activity supports management’s strategy of improving channel mix and customer commitment.

- LOCL expanded into select southern markets with a new national retailer in 4Q25, then secured and launched two additional accounts in 1Q26, including a large premier retail customer covering more than 250 stores with a six-SKU rollout and a large regional retailer. The company also received bid awards in 1Q26 and early 2Q26 that extend supply programs with multiple national retail accounts through 1Q27, spanning baby leaf lettuce and organic butter lettuce.

- Quality of Volume: This visibility matters because LOCL’s production model works best when capacity, SKU assortment, and retailer demand are planned together. LOCL is prioritizing account depth, renewal visibility, and product mix rather than simply adding doors without a clear margin or capacity rationale. The strategy is also consistent with the 1Q26 financial profile, where sales increased 15% y/y while adjusted G&A declined 30% y/y to $4.1 million. The combination shows the early operating leverage behind the strategy: LOCL is growing revenue while reducing adjusted G&A, suggesting that higher-quality volume can scale through the existing commercial and overhead infrastructure.

- Using product innovation to deepen retailer relevance, with salad kits, arugula, baby leaf, and organic butter lettuce extending the platform beyond core living lettuce. LOCL’s product expansion strategy is focused less on SKU proliferation and more on targeted assortment expansion, using existing retail relationships and facility capabilities to scale products where customer demand, supply reliability gaps, and shelf-space opportunities are most visible.

- The clearest recent proof point is the family-sized 10-ounce Romano Caesar Salad Kit in the Pacific Northwest, which recorded a 75% increase in baseline velocity, measured as units sold per store per week, during 4Q25 and earned an additional distribution center with a national retailer in 1Q26, scheduled to launch in May 2026.

- LOCL is also pursuing arugula growth following successful launches at Pasco, WA and Mount Pleasant, TX in 2025, with management highlighting conventional arugula supply as unreliable and insufficient.

- Shelf-Space Runway: The broader product strategy remains consistent with LOCL’s stated plan to explore fresh greens, herbs, berries, and other produce, while its current awards through 1Q27 span key lines including baby leaf lettuce and organic butter lettuce. We believe this creates a practical growth lever: new SKUs can increase shelf presence, improve account penetration, and help LOCL monetize fixed facility capacity through value-added product formats.

- The early financial proof point is sales productivity rather than absolute SKU count: 1Q26 sales increased 15% y/y, while sales and marketing expense rose only ~6% y/y, indicating that product expansion and deeper account penetration are being supported without a proportional increase in selling expense. This helps support the view that SKU scaling can improve account relevance while preserving operating leverage.

- Strategic partnerships could become a catalyst for capacity expansion, channel access, and capital-efficient growth. Ongoing strategic retail and partnership discussions remain central to LOCL’s long-term growth strategy, particularly after GA, TX, and WA reached full harvestable capacity and sold-out run-rate capacity in 4Q25. The strategic rationale is clear: as retailers and supply-chain partners increasingly treat CEA as a permanent part of fresh-produce infrastructure, LOCL can use its existing retail footprint, full-capacity operating base, Stack & Flow platform, and AI-enabled growing optimization to pursue partnerships that align demand, capacity, and financing more efficiently. While disclosures around strategic partnership discussions remain limited, the $15 million investment from an existing strategic investor adds financial flexibility as LOCL evaluates partnership-led growth and capacity expansion opportunities. We view partnerships as an upside lever rather than the base case, but definitive agreements could materially improve visibility around LOCL’s next phase of capacity expansion and channel mix.

Fundamentals and Valuation

Operating Leverage Supports Positive EBITDA Path; Balance Sheet Discipline Remains Key

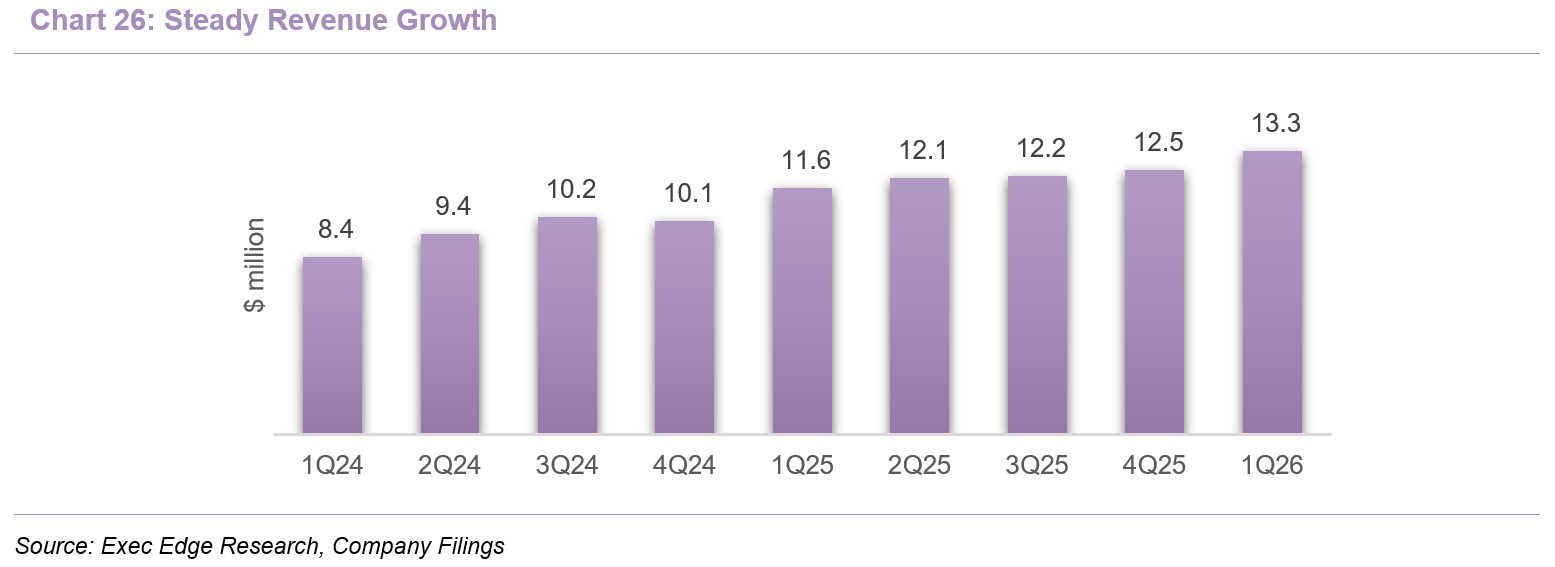

- Revenue growth shows LOCL beginning to monetize its fully utilized facility base. Sales increased 15% y/y to $13.3 million in 1Q26, supported by higher production and sales from the Georgia, Texas, and Washington facilities, and rose 7% sequentially from 4Q25. The sequential growth is important because the company had already reached full harvestable capacity and sold-out run-rate capacity across its three state-of-the-art facilities exiting 2025. Incremental growth is therefore increasingly tied to yield gains, mix improvement, retail wins, and SKU penetration rather than simply bringing new farms online. In our view, LOCL’s revenue narrative is shifting from capacity ramp to asset productivity, with upside increasingly tied to converting higher yields, stronger mix, and new product placements into repeatable retail volume.

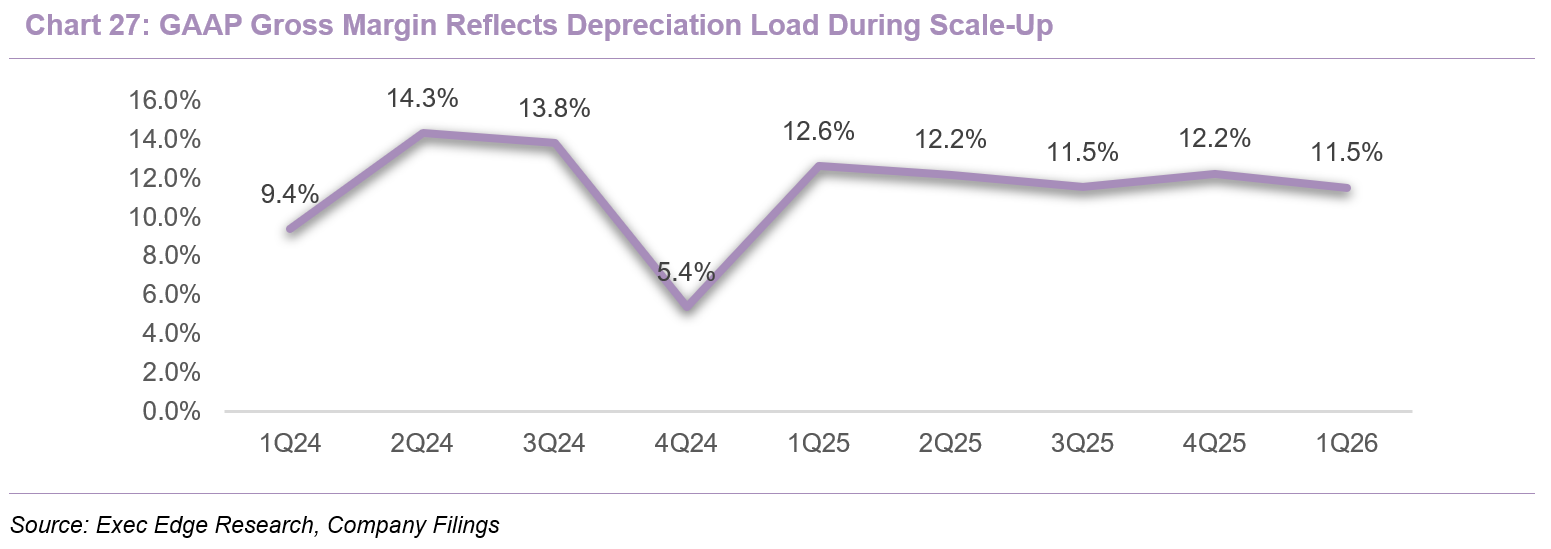

- Stable adjusted gross margin shows the production model is holding as revenue scales. Gross profit increased 5% y/y to $1.53 million in 1Q26, while adjusted gross margin remained stable at 29% versus both 1Q25 and 4Q25 after excluding depreciation, stock-based compensation, and other non-core items. This is the more relevant operating signal at this stage, as GAAP gross margin continues to reflect a meaningful depreciation load from LOCL’s asset base. GAAP gross margin was 11.5% in 1Q26 versus 12.6% in 1Q25 and 12.2% in 4Q25, with COGS increasing broadly in line with the production ramp across GA, TX, and WA. The key margin takeaway is that LOCL’s underlying production model is holding steady as revenue scales, while tower upgrades, California yield investments, higher throughput, better mix, and improved cost absorption provide the next levers for sustained GAAP margin expansion.

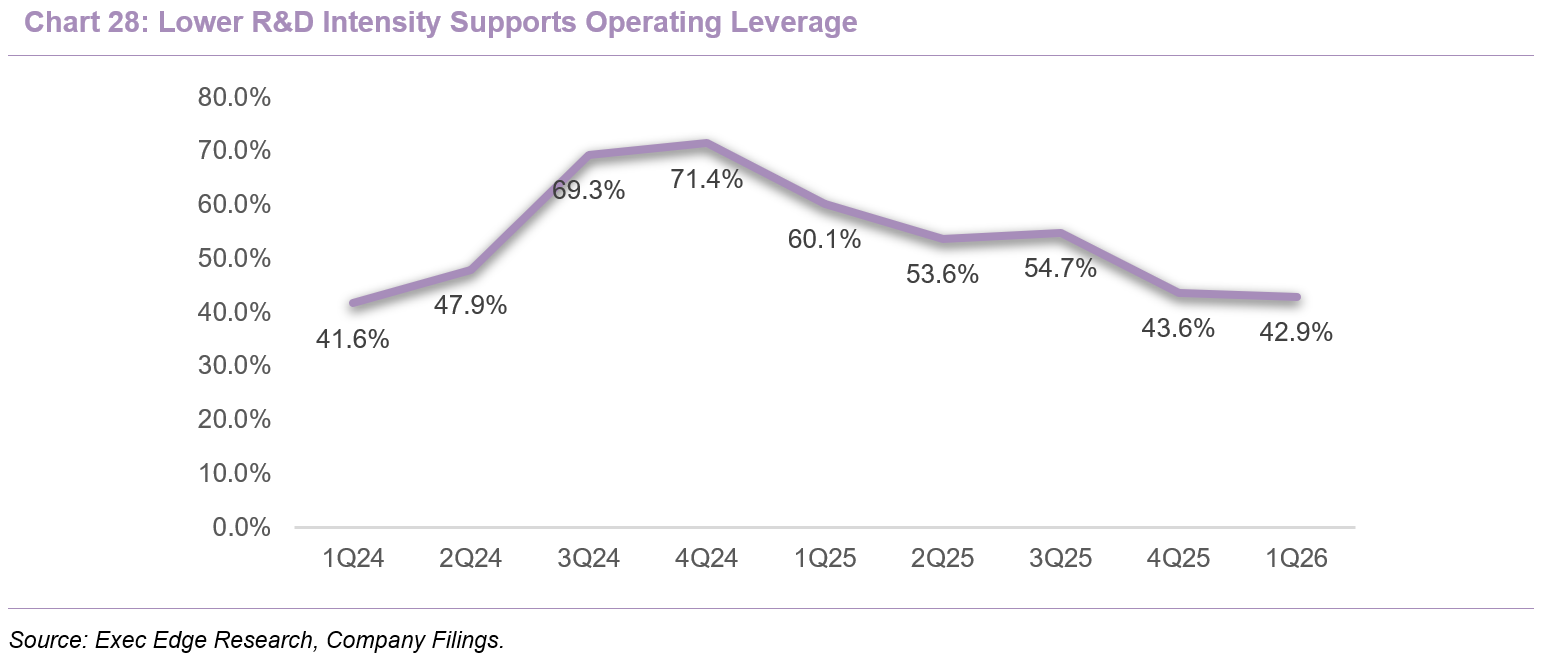

- Lower adjusted G&A and maturing R&D spend show operating leverage beginning to come through. Total operating expenses declined 10% y/y to $15.5 million in 1Q26, reflecting lower R&D and G&A as LOCL moved further into commercial-scale execution across WA, TX, and GA. R&D fell 18% y/y to $5.7 million, with the company attributing the reduction to the maturation of production, harvesting, and post-harvest packaging initiatives tied to Stack & Flow deployment. G&A declined 7% y/y to $7.5 million, while adjusted G&A was the cleaner signal, down 30% y/y to $4.1 million and modestly lower sequentially. This directly supports LOCL’s operating leverage story: as the existing network scales revenue and management reduces the fixed-cost burden, incremental growth should have a clearer path to narrowing adjusted EBITDA losses.

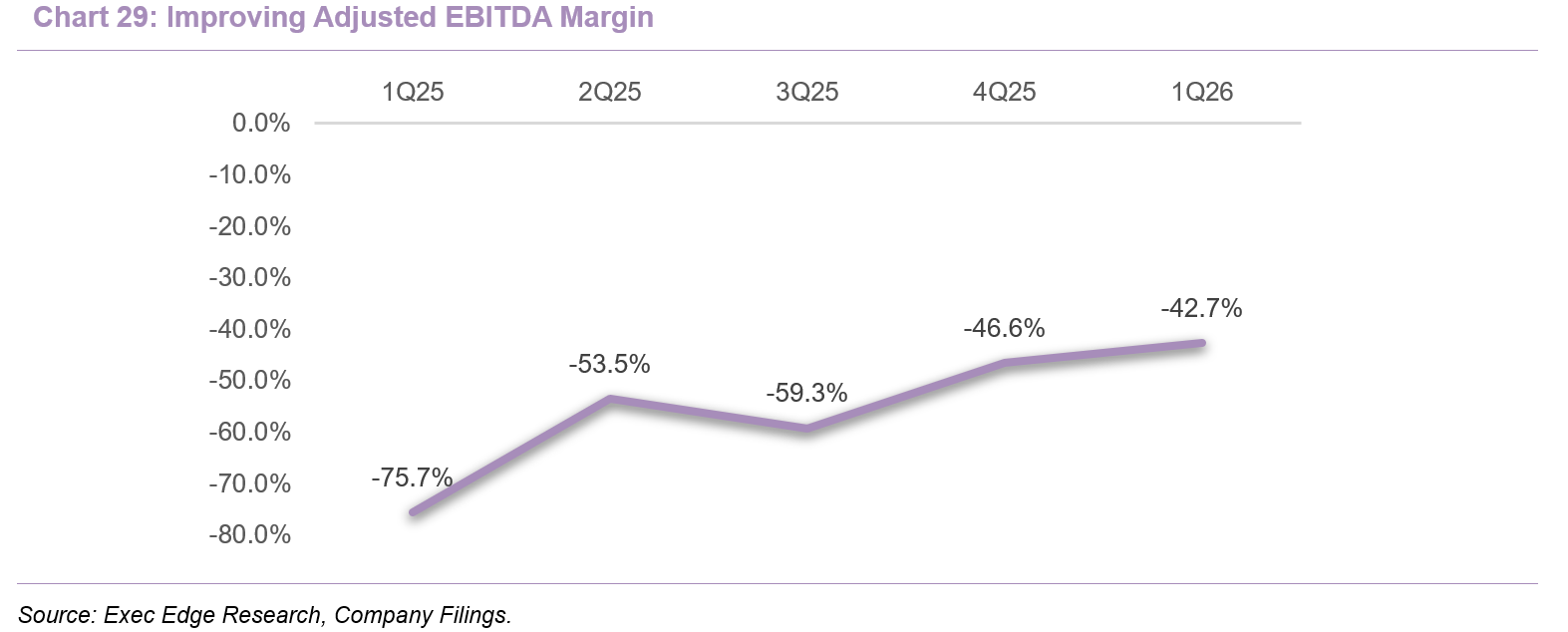

- Adjusted EBITDA is the clearest read-through on LOCL’s improving profitability trajectory. Net loss improved to $12.7 million in 1Q26 from $37.7 million in 1Q25, helped by lower net interest expense following the 1Q25 debt restructuring and a favorable warrant fair-value movement. However, we believe adjusted EBITDA is the more useful measure of operating progress at this stage because it excludes interest, D&A, warrant marks, and other non-core items. Adjusted EBITDA loss improved 35% y/y to $5.7 million from $8.8 million and was modestly better than the $5.8 million loss in 4Q25. The key takeaway is that revenue growth, stable adjusted gross margin, lower adjusted G&A, and maturing production processes are converging into a narrower loss rate, keeping LOCL on a clearer path toward positive adjusted EBITDA.

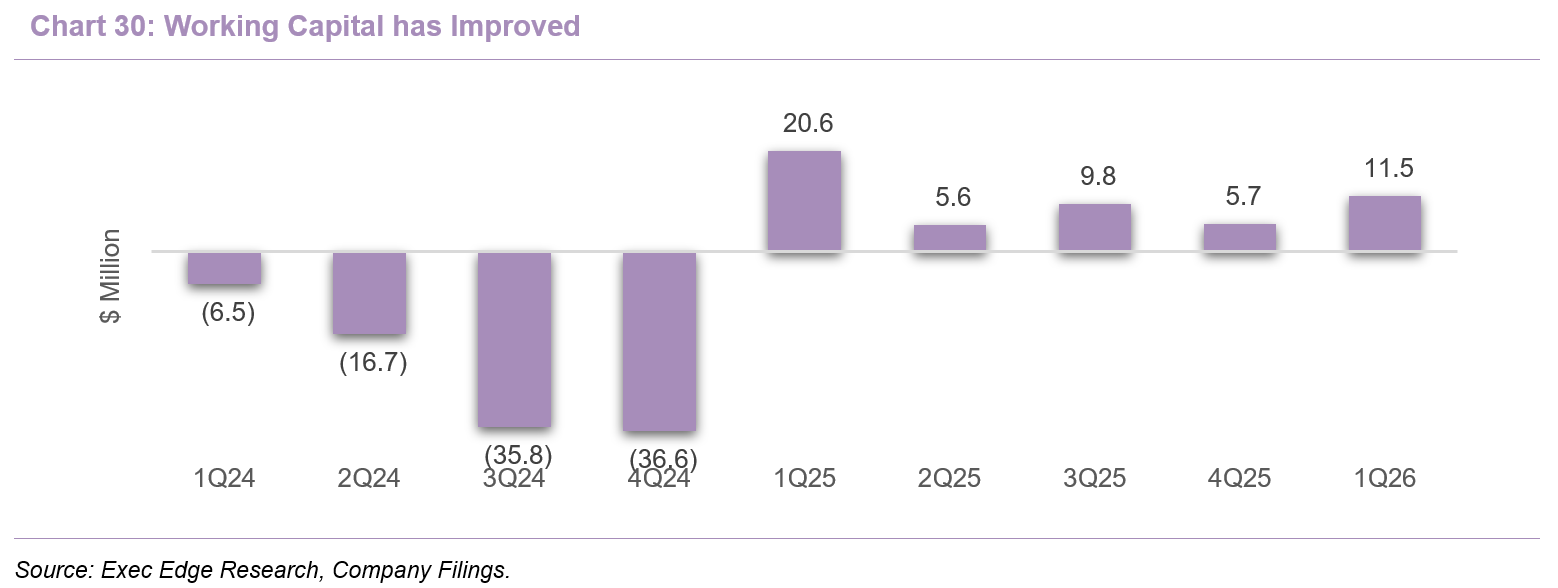

- Liquidity improved in 1Q26, giving LOCL more flexibility to support yield initiatives, retail launches, and strategic discussions. Cash and restricted cash increased to $18.8 million from $10.7 million at year-end 2025, supported by the $15 million convertible note investment from an existing strategic investor during the quarter, while working capital improved to $11.5 million from $5.7 million. The liquidity improvement gives LOCL more room to fund targeted facility and commercial initiatives while it remains below adjusted EBITDA breakeven. This is particularly relevant as management continues to invest in California yield improvements, new retail programs, and partnership discussions tied to future capacity planning. However, the balance sheet is still constrained by a debt-heavy capital structure and accumulated deficit, leaving the 2026 revenue growth and adjusted EBITDA improvement path as the key execution test.

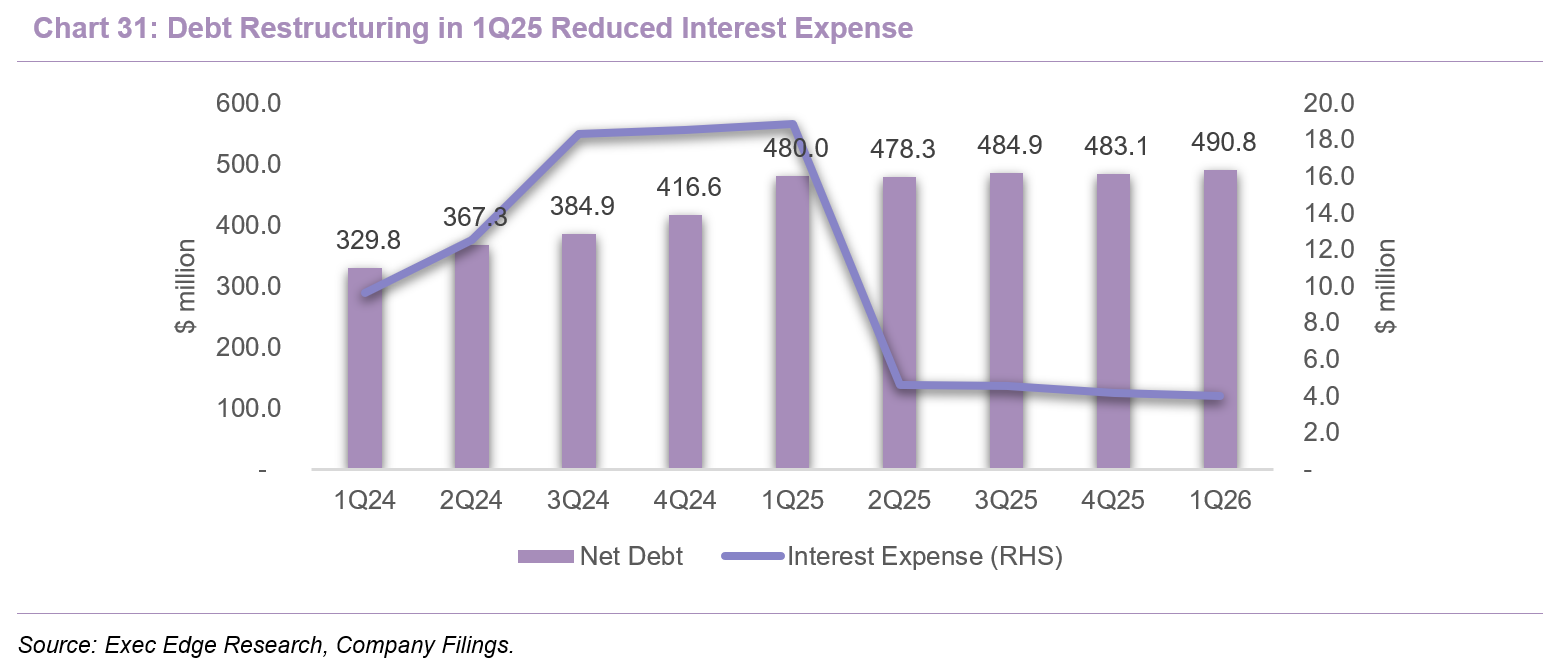

- The 2025 debt restructuring improved LOCL’s cash runway, but leverage remains the key balance sheet overhang. The March 2025 restructuring cancelled $181.7 million of principal and $15.4 million of accrued interest, reset the senior facility principal to $312.0 million, and materially lowered reported interest expense. However, the transaction did not fully de-risk the balance sheet: reported long-term debt remained elevated at $490.8 million in 1Q26, noncurrent accrued interest increased to $19.0 million, and total liabilities continued to exceed total assets. The restructuring therefore improves liquidity and the cash-interest profile but does not fully resolve balance sheet risk; execution against 2026 revenue growth and adjusted EBITDA improvement remains the central deleveraging lever.

- Cash flow trends reinforce LOCL’s shift from construction-heavy expansion toward asset optimization. Net cash used in operating activities improved to $6.1 million in 1Q26 from $9.6 million in 1Q25, reflecting a narrower operating loss rate and the benefit of ongoing cost discipline. Net cash used in investing activities declined to $1.1 million from $5.0 million y/y, and was well below the elevated capital spending levels of prior build-out years, supporting the view that LOCL has moved past the peak facility-construction phase. Financing cash flow was positive $15.2 million, primarily reflecting the 1Q26 strategic investor financing, which drove an $8.1 million increase in cash and restricted cash during the quarter. LOCL is not yet self-funding, but the cash flow profile now better reflects the company’s stated priorities: monetize the existing asset base, keep capital spending disciplined, and narrow the adjusted EBITDA loss rate through revenue growth and cost control.

Execution Progress Supports Valuation Recovery Case

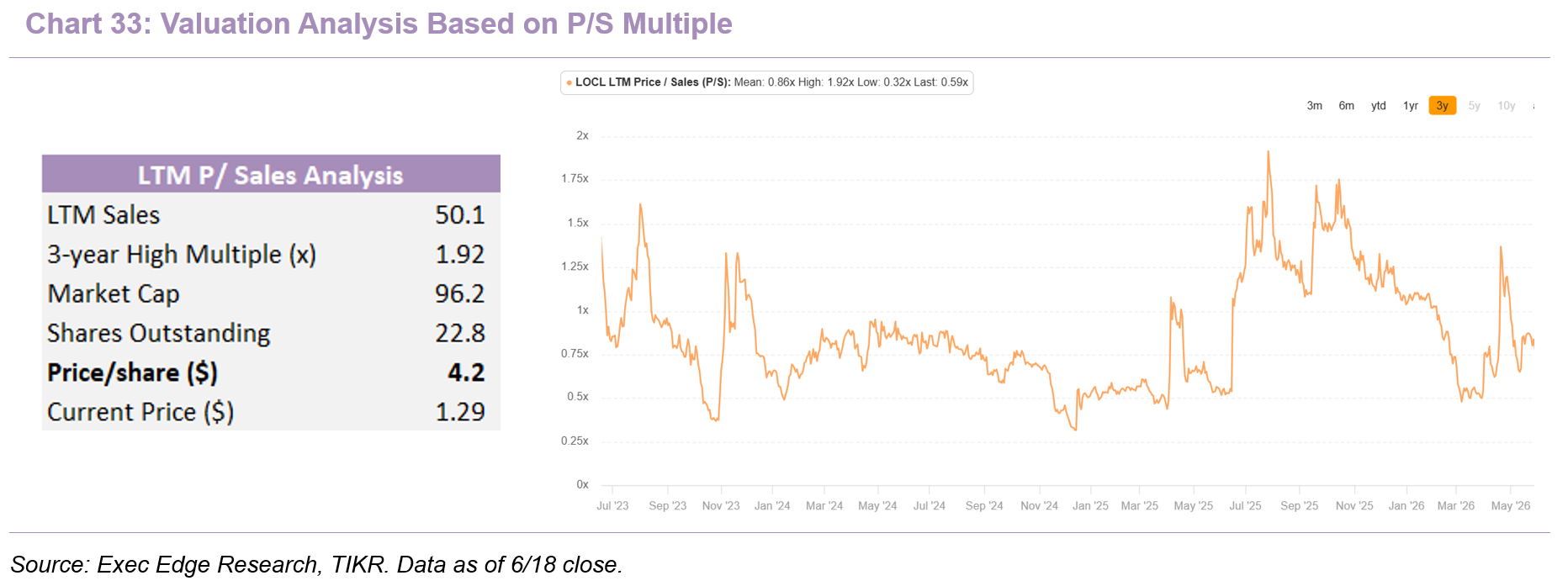

- LOCL trades near the lower end of its historical valuation range despite recent operating improvement. The analysis below is illustrative only and should not be interpreted as a stock recommendation, price target, or buy/sell/hold opinion. We assess valuation using multiple approaches, including LOCL’s own historical trading range and comparison with relevant public peers. While we do not assign a formal price target, the analysis suggests potential upside under select valuation scenarios. Any upside shown below is illustrative and reflects the assumptions used in our valuation framework, not a target price or investment recommendation.

- LOCL’s own trading history suggests room for valuation recovery if execution continues to improve. LOCL currently trades at 0.59x LTM sales versus a three-year high multiple of 1.92x and a three-year mean of 0.86x. Applying the historical high multiple to LTM sales of $50.1 million implies an illustrative market capitalization of $96.2 million, or $4.20 per share. Importantly this framework does not require aggressive forward revenue assumptions; rather, it reflects potential multiple recovery if investors gain confidence that LOCL’s recent execution improvements – higher revenue, stable adjusted gross margin, lower adjusted G&A, and narrowing adjusted EBITDA losses – are sustainable.

- Relative valuation is more nuanced within the CEA-linked peer set, while traditional fresh produce peers provide valuation discipline. LOCL trades at 0.59x LTM sales, below Village Farms at 0.96x and below the headline CEA-linked peer average, although that average is distorted by CEA Industries’ elevated multiple. The stock trades at par with GrowGeneration at 0.58x and above Hydrofarm at 0.03x, which appears reasonable given LOCL’s stronger retail-facing CEA positioning, patented Stack & Flow platform, 13,000-door retail footprint, and improving EBITDA trajectory. Traditional fresh produce peers average 0.52x LTM sales; LOCL’s premium to that set is defensible if investors view the company as a higher-growth, technology-enabled CEA platform rather than a conventional produce distributor.

- The key re-rating triggers are execution-led rather than purely multiple-led. Continued sequential revenue growth, stable adjusted gross margin, further adjusted G&A discipline, and progress toward positive adjusted EBITDA would provide the clearest support for valuation recovery. Strategic investor support also helps the setup: the recent $15 million convertible note and warrant investment from U.S. Bounti, LLC, an entity managed by Charles R. Schwab, signals continued confidence from a long-standing investor and adds financial flexibility as LOCL pursues yield initiatives, retail launches, and strategic partnership discussions. At the same time, balance sheet discipline remains important, and any valuation re-rating will likely depend on LOCL converting its fully utilized facility base into sustained revenue growth and a narrower adjusted EBITDA loss rate.

Subscribe to our Weekly Newsletter to Receive All Research

Contact: