Download the Complete Report Here

SOL Strategies Inc. (STKE)

SOL Strategies Inc. (STKE)

Moving Up the Solana Stack as Darklake and Houdini Add Middleware Monetization

- Key Takeaways:

- Darklake/Zyga and Houdini move STKE up the Solana stack into privacy execution, APIs, routing, and middleware monetization.

- Core staking and validation rewards remained resilient in SOL terms, reinforcing unit compounding despite SOL price-driven CAD revenue pressure.

- Validator scale continues to support the infrastructure thesis, with 3.8 million SOL of AuD and 100% uptime.

- STKESOL reached ~768,000 SOL of deposits by quarter-end, validating liquid staking as a scalable fee-bearing layer.

- Valuation increasingly depends on converting infrastructure scale into recurring fee revenue.

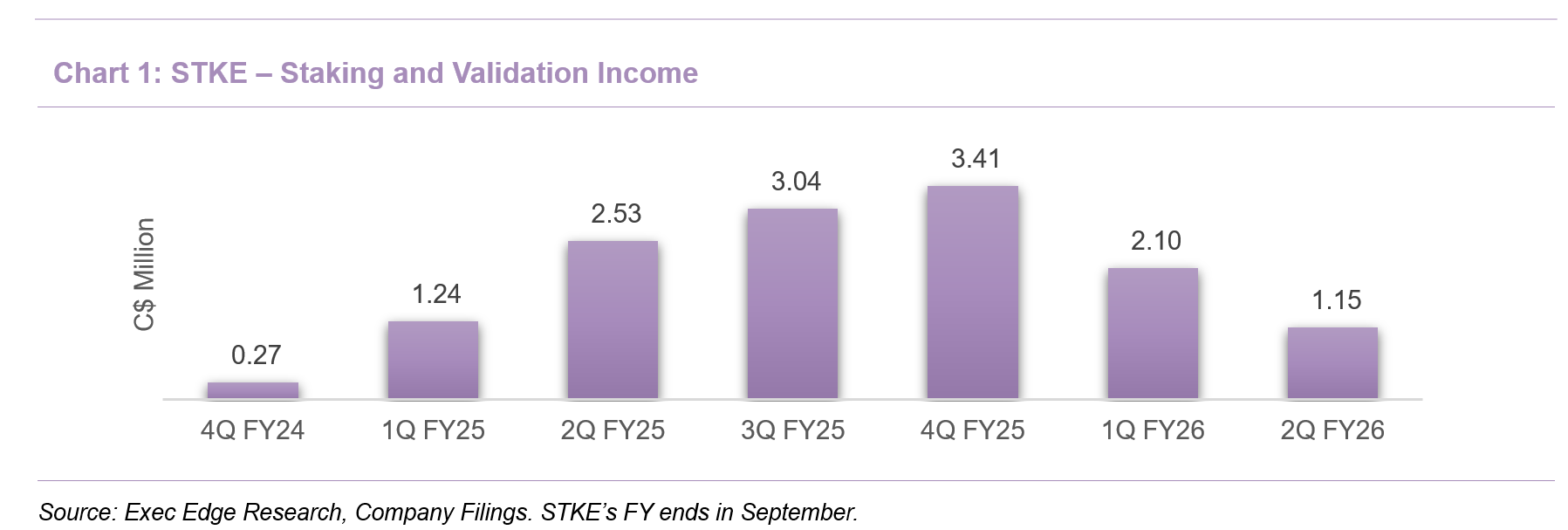

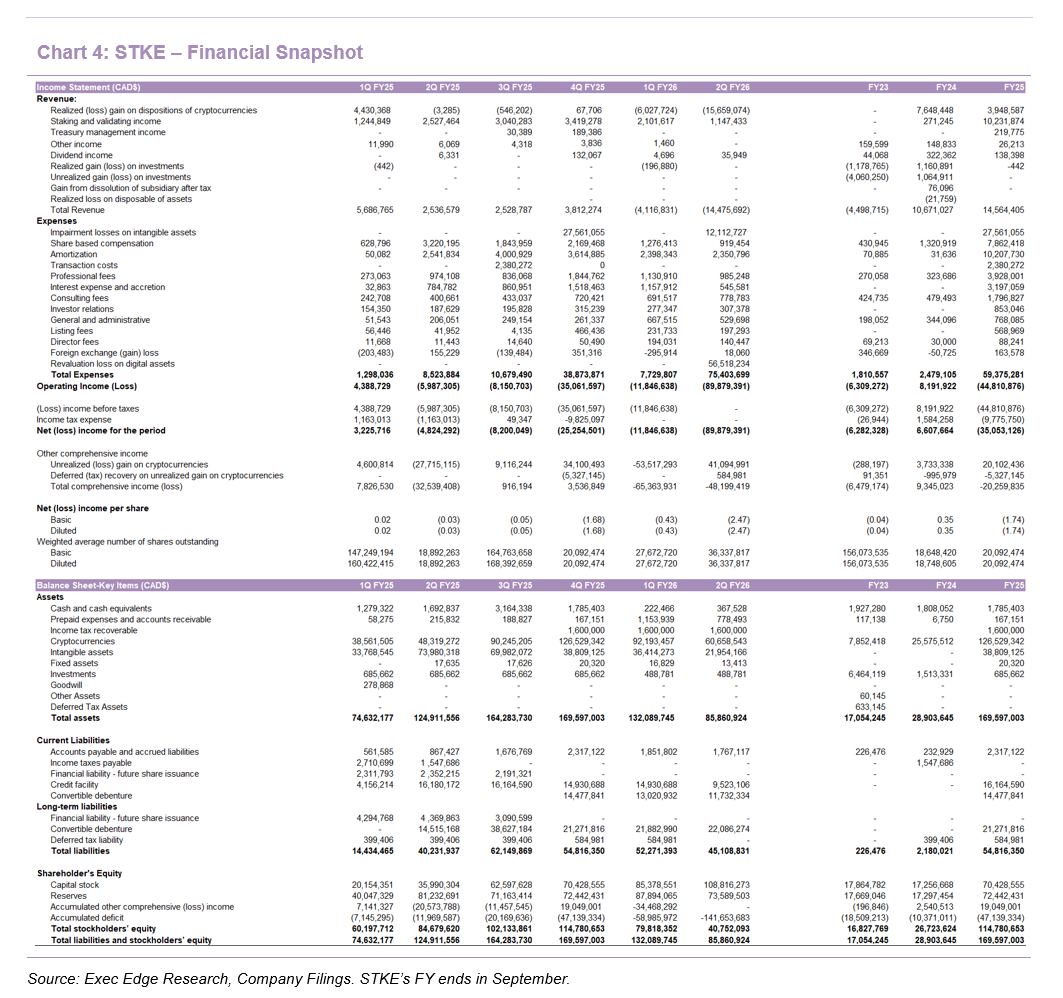

- STKE’s DAT++ model is expanding from validator economics into a broader Solana infrastructure stack. STKE’s 2Q FY26 (quarter ending March 2026) was defined less by CAD-denominated revenue and more by its transition from a validator-led DAT++ vehicle into a broader Solana infrastructure platform spanning staking, liquid staking, privacy-enabled execution, and cross-chain routing. Core rewards remained resilient, with 5,650 SOL of staking rewards and 3,521 SOL of validation rewards, bringing total rewards to 9,171 SOL, down only 6% q/q, even as CAD-denominated staking and validation income fell 45% q/q to C$1.15 million on lower SOL prices. We believe the divergence reinforces the thesis: STKE is building value through SOL units, fee-bearing assets, and transaction-layer revenue, not simply balance-sheet exposure to SOL.

- Strategic execution in 1H FY26 supports the move from passive SOL exposure toward infrastructure monetization. The first half included capital-structure clean-up, Michael Hubbard’s permanent CEO appointment on March 31, the January launch of STKESOL, the April Darklake/Zyga acquisition, and the definitive agreement to acquire Houdini Swap for $18 million. Collectively, these actions extend the model beyond proprietary staking and delegated validation into liquid staking, private execution, APIs, routing, and transaction distribution, with Darklake and Houdini representing the clearest steps toward a higher-margin Solana middleware platform.

- The core thesis remains unit compounding, but mark-to-market pressure was significant. STKE ended March with 441,915 SOL, 82,314 STKESOL, and 52,182 JTO, worth C$60.7 million versus C$126.5 million of crypto holdings at September 30, as SOL fell 60% from $208.74 to $83.11. The offset was unit growth: SOL-equivalent holdings increased to roughly 524,000 from 435,159 at fiscal year-end, AuD reached 3.8 million SOL, and the validator network served 34,000+ wallets with 100% uptime and a 6.08% peak APY versus the 5.74% network average. The quarter therefore reinforced the DAT++ thesis at the unit and product levels, even as SOL-price compression drove a C$89.9 million quarterly loss and C$48.2 million total comprehensive loss.

- Darklake expands STKE into Solana-native privacy infrastructure and zero-knowledge execution. In April, STKE acquired Darklake Labs for $1.2 million, including $200K in cash and $1.0 million in common shares subject to a four-month lock-up. The transaction brings Zyga, a Solana-native dynamic zero-knowledge proof engine designed to enable private transaction execution while mitigating front-running and sandwich attacks, alongside an application layer focused on dynamic slippage protection and improved trade execution quality. Darklake adds a team with prior experience at Meta, IBM, Coinbase, and Coincover, plus ecosystem validation from a second-place finish in the Solana Radar Global Hackathon DeFi track, Colosseum Accelerator participation, two Brazilian university partnerships, and an ongoing patent process. Strategically, the acquisition moves STKE beyond validator ownership into proprietary Solana technology development, with privacy and execution quality becoming potential product layers on top of the core staking and validation platform.

- Pending Houdini acquisition adds cross-chain transaction infrastructure and software-based revenue. In May, STKE entered into a definitive agreement to acquire Houdini Swap for $18 million, consisting of $8.25 million in cash, a $5.75 million promissory note, $4 million in common shares, and additional warrant consideration, with closing expected by the end of May subject to customary approvals. Houdini is a non-custodial, privacy-enabled cross-chain swap aggregator operating across more than 100 blockchain networks and over 30 centralized and decentralized exchanges, enabling users to access competitive swap routes without taking custody of funds. The platform generated ~$13 million in revenue during 2025, has processed more than $2.5 billion in cumulative transaction volume, and had more than half of trailing 12-month volume touch Solana, making it directly relevant to STKE’s Solana-first infrastructure strategy.

- Houdini moves STKE further up the stack from validation into transaction routing, APIs, and middleware monetization. The acquisition would add a fifth revenue stream and extend the business beyond proprietary staking, delegated validation, and STKESOL into software-driven transaction infrastructure across 100+ blockchains and 1 million+ supported tokens. The strategic value is not only Houdini’s standalone revenue base; it is the potential to connect cross-chain routing, public and private swaps, API products, and Solana transaction flow with STKE’s validator and staking foundation. If closed and integrated well, we believe Houdini could broaden STKE’s monetization model from asset-linked staking economics toward higher-margin transaction and software revenue.

- Zyga and Houdini together create the clearest near-term product integration opportunity. Darklake’s Zyga technology brings zero-knowledge privacy and slippage-protection capabilities, while Houdini brings existing distribution, routing infrastructure, public and private swap functionality, and API-based integrations across 100+ blockchain networks and 1 million+ supported tokens. Combining the two could improve private swap execution, support value-added services for users, and expand B2B API offerings for partners, with Houdini Pay creating an additional path into private wallet-to-wallet transfers. The opportunity is to turn these assets into integrated products that expand transaction volume, fee capture, and margin contribution, while using Houdini to drive users into STKE’s staking ecosystem and preserving execution quality across the core validator platform, 3.8 million SOL of AuD, and the January-launched STKESOL fee layer.

- STKESOL is validating the DAT++ model by converting staked SOL into a liquid, fee-bearing asset. Launched in January, STKESOL gives SOL holders a receipt token representing their staked position while continuing to accrue staking rewards, allowing users to hold, trade, collateralize, or deploy the asset in DeFi instead of waiting up to two days to unstake native SOL. Early adoption was strong, with deposits reaching approximately 768,000 SOL by March 31, equivalent to roughly $61 million or C$83 million at the time, and STKE earns a 5% commission on the staking rewards generated by the pool without taking a fee on staked principal. The traction matters because STKESOL adds an asset-linked fee stream alongside treasury staking and delegated validator commissions, while positioning STKE at the aggregation layer between stakers, validators, and DeFi applications.

- Scalability depends on validator selection, liquidity depth, and DeFi utility reinforcing each other. The product allocates deposits across up to 75 validators using the company’s Wiz Score methodology from Stakewiz.com, which ranks validators based on performance, security, and decentralization metrics. That design reduces single-validator risk, improves diversification, and makes the product less dependent on STKE’s own validator capacity. Once integrations and liquidity are established, incremental deposits should add fee-bearing assets with relatively limited incremental operating cost compared with balance-sheet-funded SOL accumulation. The key monitorables are TVL retention after launch incentives, DeFi venue depth, realized fee contribution, and whether LST growth expands the total addressable fee base rather than cannibalizing proprietary staking.

- Leadership additions deepen blockchain, public-company, and capital-markets capabilities as STKE expands its platform ambitions. During the quarter, STKE added industry veteran Les Borsai and public company executive Dennis Logan as Directors, appointed Jon Matonis as Chairman, formalized Michael Hubbard as permanent CEO effective March 31, and appointed Steve Ehrlich as Chief Strategy Officer. The changes add blockchain expertise, public-company experience, and capital-markets depth at a point when the company is moving beyond validator infrastructure into STKESOL, Darklake/Zyga, and the pending Houdini transaction.

- CTO transition should be manageable given the existing engineering and infrastructure base. Max Kaplan resigned as Chief Technology Officer effective April 30, 2026, after leading validator integrations, supporting SOC 1, SOC 2 Type 2, and ISO 27001 certifications, and helping build STKE’s engineering and automation framework. The engineering team remains in place, and the company does not currently plan to fill the role, suggesting validator operations, staking services, and core infrastructure should continue without near-term disruption.

- Reported losses were dominated by accounting and noncash items rather than cash operating deterioration alone. STKE reported a C$89.9 million net loss in 2Q FY26 versus a C$4.8 million net loss in the March 2025 quarter, while the six-month net loss was C$101.7 million compared with C$1.6 million a year ago. The six-month loss included C$21.7 million of realized cryptocurrency disposition losses, C$56.5 million of digital-asset revaluation losses, C$12.1 million of intangible-asset impairment losses, C$4.7 million of amortization, C$2.2 million of share-based compensation, and C$1.7 million of noncash interest and accretion. The scale of noncash and mark-to-market charges drove the reported loss profile, masking continued SOL-denominated reward generation of 18,957 SOL and C$3.25 million of six-month staking and validation income.

- Validator economics remained resilient in SOL terms, but competition remains a margin watch item. STKE generated 9,171 SOL of total staking and validator rewards in 2Q FY26, down only 6% q/q, while CAD-denominated income fell 45% q/q to C$1.15 million on lower SOL prices. Increased validator competition and higher incentives to retain delegated stake make net contribution from 3.8 million SOL of AuD a key operating-leverage variable.

- The path to profitability is tied to converting platform scale into higher-margin fee contribution. Adjusted EBITDA loss was approximately C$3.0 million for the six months ended March 31, 2026 versus positive C$1.2 million in the prior-year period. As STKESOL, Darklake, and Houdini mature, the operating model should increasingly depend on fee-bearing assets, transaction volume, and software revenue rather than only SOL price realization, with 3.8 million SOL of AuD and 768,000 SOL of STKESOL deposits providing the starting base.

- Balance-sheet simplification improved flexibility, while financing capacity remains tied to token collateral and market access. STKE had C$60.6 million of cryptocurrencies, C$22.0 million of intangible assets, and C$0.35 million of cash at March 31, while total assets declined to C$85.9 million from C$169.6 million at September 30. Shareholders’ equity fell to C$40.7 million from C$114.8 million over the same period, reflecting reported and unrealized digital-asset losses, partially offset by capital raising. The company also repaid roughly C$9 million of debt to the former chairman, ended the quarter with 81,236 SOL and 82,137 STKESOL pledged to Kamino, and has a base shelf allowing up to $150 million of future offerings. The financing stack is cleaner and more flexible, but liquidity remains dependent on SOL collateral values, market windows, and capital raises that preserve SOL-per-share economics.

Valuation: DAT Metrics Anchor the Debate; Middleware Execution Drives the Premium Case

- Valuation should frame STKE’s transition from NAV-linked treasury exposure to infrastructure-led monetization. Exec Edge does not provide estimates, price targets, or buy/sell/hold ratings, and the analysis below is intended to frame valuation positioning and potential rerating drivers rather than imply a specific fair value.

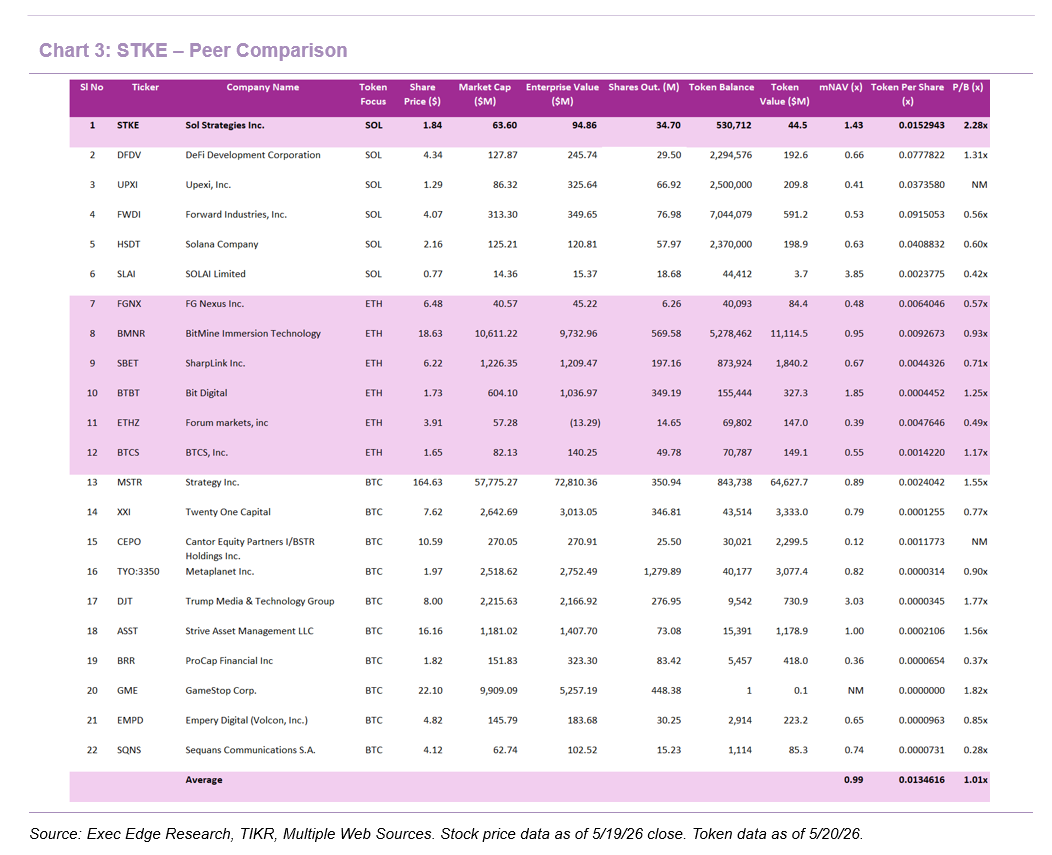

- We believe STKE’s valuation should now be viewed through a DAT-plus-infrastructure lens. STKE trades at 1.43x mNAV versus the peer average of 0.99x, suggesting the stock is no longer being valued as a simple discount-to-NAV treasury vehicle. That premium is best understood as early credit for the company’s operating infrastructure, including validator rewards, 3.8 million SOL of AuD, STKESOL liquid-staking fees, and the pending expansion into transaction routing through Houdini. On a pure DAT framework, STKE’s SOL-equivalent holdings remain the valuation anchor; on an infrastructure framework, the debate shifts to whether those assets can support recurring, scalable fee revenue beyond token appreciation.

- Middleware expansion strengthens the case for an operating premium over passive DAT peers. STKE combines SOL treasury exposure with delegated validator economics, 768,000 SOL of STKESOL deposits, and a developing software and transaction layer through Darklake/Zyga and Houdini. Houdini is particularly important because it generated approximately $13 million of 2025 revenue and processed more than $2.5 billion of cumulative transaction volume, creating a potential software-revenue stream that passive DAT peers do not have. While STKE is not the largest SOL treasury in the peer set, the valuation argument is increasingly about recurring infrastructure monetization rather than balance-sheet SOL density alone.

- Rerating drivers are now tied to execution across the infrastructure stack rather than SOL price alone. Continued SOL-equivalent unit growth, AuD expansion with stable validator margins, STKESOL deposit retention and fee contribution, Houdini closing and revenue contribution, and Zyga-enabled private execution products are the key catalysts. As fee-bearing assets and transaction revenue become more visible, STKE should be better positioned to sustain a valuation framework above NAV-only DAT treatment. The upside case is that STKESOL, delegated validation, and Houdini/Zyga convert the SOL treasury into a broader infrastructure platform with recurring revenue and higher-margin monetization. The key risks to that framework are limited STKESOL fee contribution, validator incentives weighing on net economics, or slower Houdini integration, any of which would keep valuation more closely tied to DAT peer multiples and SOL NAV.

Download the Complete Report Here

Read Exec Edge’s Initiation on STKE Here

Subscribe to our Weekly Newsletter to Receive All Research

Contact: