Download the Complete Report Here

Beyond Oil Ltd. (BOIL/BEOLF)

Beyond Oil Ltd. (BOIL/BEOLF)

Revenue Execution Phase Begins as U.S. Foodservice Adoption Advances

- Key Takeaways:

- Revenue increased to $1.26 million (+24% y/y), maintaining a ~$5.0 million run-rate ahead of expected 2H26 U.S. rollout acceleration.

- Gross margin expanded 240 bps y/y to 53.1%, reinforcing product-level economics despite higher commercialization spend.

- Strategy now prioritizes direct strategic accounts and targeted distribution, improving control over rollout execution, customer adoption, and recurring revenue visibility.

- New U.S. fast-food chain sales add another strategic validation point following pilots, with initial rollout across three states.

- Valuation reflects revenue-scaling potential rather than current revenue alone, with the case dependent on faster conversion into existing capacity and improved opex absorption.

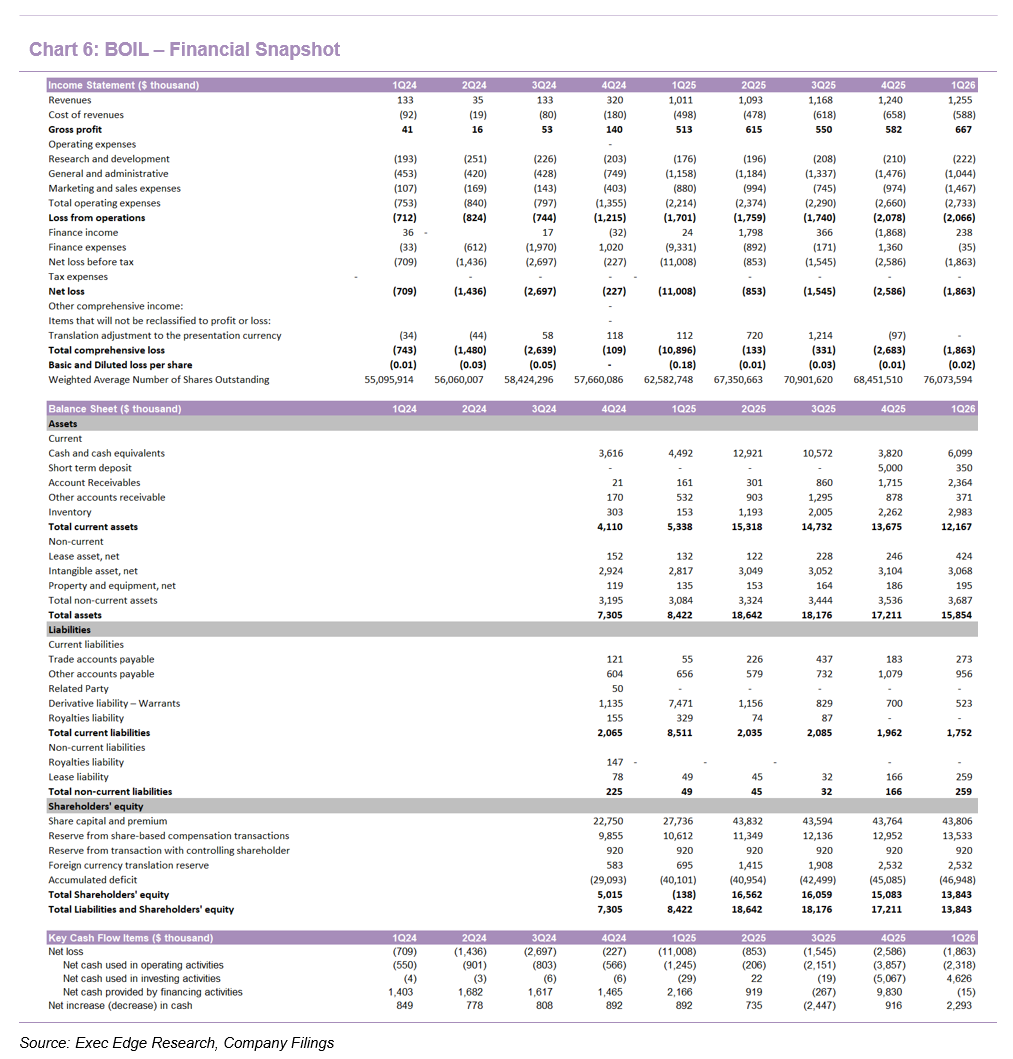

- Revenue growth remained positive in 1Q26, though the quarter primarily reflected continued early-scale execution rather than a step-function inflection. BOIL reported revenue of $1.26 million in 1Q26, up 24% y/y from $1.01 million and modestly above $1.24 million in 4Q25, implying an annualized run-rate of ~$5.0 million. The sequential increase of ~1% was limited, but the y/y growth confirms that commercial revenue is sustaining at a materially higher level than the prior-year base. The revenue increase reflected distributor revenue, additional revenue-generating agreements, and increased marketing efforts intended to expand global exposure, suggesting BOIL remains in the early phase of converting channel and customer development into recurring product demand.

- Margin performance remains encouraging, with gross margin expanding despite a still-developing commercial base. Gross profit increased to $0.67 million from $0.51 million, while gross margin improved to 53.1% from 50.7% y/y. Cost of revenue rose 18% y/y to $0.59 million, below the 24% revenue increase, suggesting improved product economics and scale benefits even at a quarterly revenue base of only $1.26 million. The higher gross margin is important because BOIL’s recurring consumable model should support operating leverage as revenue scales across foodservice workflows, with incremental growth better positioned to absorb the expanded commercial infrastructure.

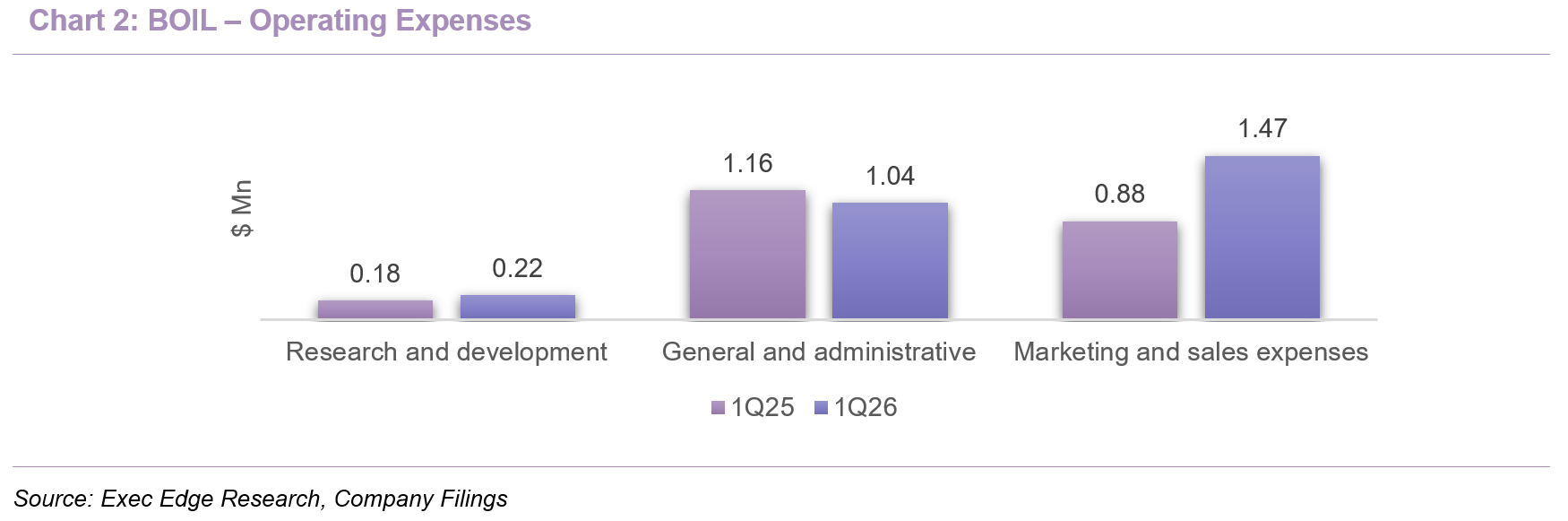

- Operating expenses continued to scale with commercial build-out, with sales and marketing now the largest opex category. Total operating expenses increased 23% y/y to $2.73 million from $2.21 million, broadly in line with revenue growth, but mix shifted further toward commercialization. Sales and marketing increased 67% y/y to $1.47 million from $0.88 million, reflecting customer acquisition, rollout support, and direct sales investment. G&A declined 10% y/y to $1.04 million, while R&D increased 26% to $0.22 million.

- Strategic direction is now more clearly centered on revenue execution, customer rollout, and direct account-based selling. BOIL’s May strategic update reframes the next phase of commercialization around large strategic end customers, typically multi-location operators where the product can be deployed across dozens, hundreds, or thousands of sites. Target verticals include QSR, casual dining, other chain restaurants, hotels and hospitality groups, catering and institutional foodservice, supermarkets, and convenience-store operators. We believe this is a meaningful shift because it moves the commercial focus toward account-level penetration, operational integration, and repeat usage across high-value customers, while retaining targeted distribution support.

- Expanded direct sales capability should improve execution control in the U.S., which is becoming the primary growth market for BOIL. The May strategy update states that BOIL has expanded its direct sales organization, particularly in the U.S., which the company expects to be a primary growth market and a key strategic focus from 2H26. BOIL is now operating through two coordinated commercial units, North America and International, each supported by sales and customer-success teams. This structure is important because large foodservice rollouts require hands-on implementation, training, customer success, and procurement coordination, not just distributor access. The recent premium casual dining customer and top-tier supermarket entry provide early examples of the type of strategic account base BOIL is attempting to scale.

- Partnership refinement is an important post-quarter strategic development and should improve visibility into higher-quality revenue, even if it reduces headline contract optionality. Subsequent to quarter-end, BOIL discontinued its agreement with Latitude in the U.S. and Ukraine as part of a transition away from master-distributor structures that relied on layers of sub-distributors. The company also discontinued its agreement with T&J Oil in Australia and is now working with alternative non-exclusive partners in that region. In India, YMS Frying remains a non-exclusive distributor, but the previously disclosed agreement structure, including projected contract values and original commitment terms, will not be entirely fulfilled and is no longer considered strategic or material. The reset should improve commercial discipline by prioritizing partners that can support measurable adoption, direct customer engagement, and repeatable rollout execution.

- The new U.S. fast-food chain rollout adds another important validation point for the direct-sales strategy. BOIL commenced commercial sales with a medium-sized American fast-food chain after a pilot validation program that began in late 2025 and expanded into a multi-location pilot in 1Q26. Initial commercial deployment has started with three franchisees across three U.S. states, while the broader chain has hundreds of locations across the U.S. and international markets. Although still early, the structure is attractive because it shows a clear progression from pilot validation to paid commercial sales, which is the key conversion point for BOIL’s refined go-to-market strategy. The announcement also came shortly after BOIL outlined its shift toward direct engagement with large multi-location operators, making the fast-food rollout an early example of account-level penetration with strategic U.S. customers.

- 1Q26 progress and recent commercial actions extend BOIL’s direct-account strategy from validation into broader U.S. rollout activity. The new fast-food chain rollout builds on 1Q26 and recent U.S. commercialization progress, including supermarket entry through an initial 13-location deployment and premium casual dining expansion through an initial 70-restaurant rollout following a 13-location validation. Together with Sysco Los Angeles onboarding, which introduced product showcasing, training, pilots, and co-marketing within a scalable distribution platform, these developments support BOIL’s shift toward strategic multi-location customers and more repeatable rollout playbooks across U.S. foodservice and food retail.

- 2H26 is shaping up as the key period for BOIL to convert recent commercial progress into stronger revenue growth and operating leverage. The strategy update points to acceleration as customer deployments expand, particularly in the second half of 2026, with recent U.S. activity adding several multi-location pathways beyond the existing distributor base. This matters because 1Q26 revenue of $1.26 million already supports a ~$5.0 million annualized run-rate, but the current commercial investment base is built for a larger revenue opportunity, with sales and marketing expense of $1.47 million in the quarter. As chain, supermarket, premium casual dining, and distributor relationships progress from pilots and initial rollouts into broader location coverage, repeat orders, and standardized daily usage, BOIL should be better positioned to demonstrate the operating leverage embedded in a recurring consumable model. Key 2H26 proof points include expansion across the new fast-food chain’s U.S. network, continued progress with supermarket and premium casual dining customers, improving reorder cadence from existing partners, and evidence that the refined partner portfolio is producing cleaner sell-through.

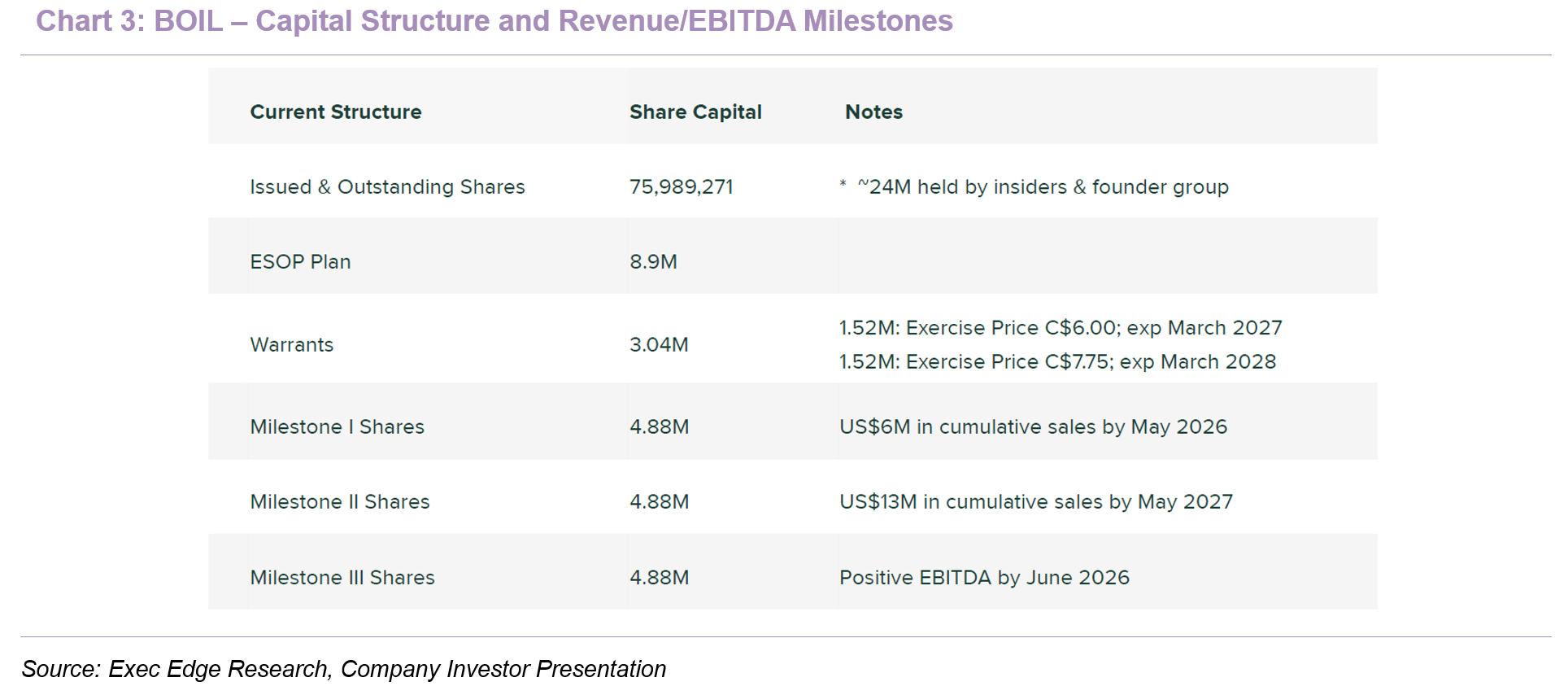

- Milestone framework remains relevant, but the incremental focus has shifted from sales validation to EBITDA conversion. BOIL has already cleared the $6 million cumulative sales milestone, and the next sales marker remains $13 million of cumulative revenue by May 2027. With 1Q26 revenue of $1.26 million, gross margin of 53.1%, and new U.S. deployments now moving through the rollout funnel, the sales milestone remains achievable, but the more important near-term proof point is the positive EBITDA milestone by June 2026. Achieving that milestone will require faster revenue conversion from current rollouts, sustained gross margin, and better opex absorption after 1Q26 operating loss of $2.07 million and operating cash usage of $2.32 million.

- Net loss improved meaningfully, but the improvement was largely financial rather than operational. Net loss narrowed to $1.86 million from $11.01 million, while loss per share improved to $0.02 from $0.18. The y/y improvement was driven primarily by finance expense falling to $0.04 million from $9.33 million, as the prior-year period included $9.13 million of fair-value adjustments on derivative liabilities. Finance income also increased to $0.24 million from $0.02 million, including $0.17 million of fair-value adjustments and $0.07 million of interest income. As a result, operating loss, gross margin, sales and marketing productivity, and cash burn remain more useful indicators of underlying progress than reported net loss in this quarter.

- Balance sheet liquidity remains adequate, but working capital is becoming more important as commercial activity scales. BOIL ended 1Q26 with $6.10 million of cash and $0.35 million of short-term deposits, or $6.45 million combined, compared with $8.82 million at year-end 2025. Current assets were $12.17 million against current liabilities of $1.75 million, implying working capital of $10.42 million and a current ratio of ~6.9x. Inventory increased to $2.98 million from $2.26 million at year-end, while accounts receivable increased to $2.36 million from $1.72 million, indicating that the commercial ramp is increasing working-capital intensity alongside revenue growth.

- Cash usage increased as BOIL invested behind sales execution and inventory. Cash used in operating activities was $2.32 million in 1Q26 versus $1.25 million in 1Q25, driven mainly by higher sales and marketing expenses and an increase in inventory. Investing activity provided $4.63 million, primarily from the release of short-term deposits, while financing activity used $0.02 million. The company states that existing cash, cash equivalents, and short-term deposits, along with growth and revenue-generation plans, are sufficient to continue operations for at least 12 months from the approval date of the financial statements.

Valuation Reflects Revenue Conversion Potential, Not Current Scale Alone

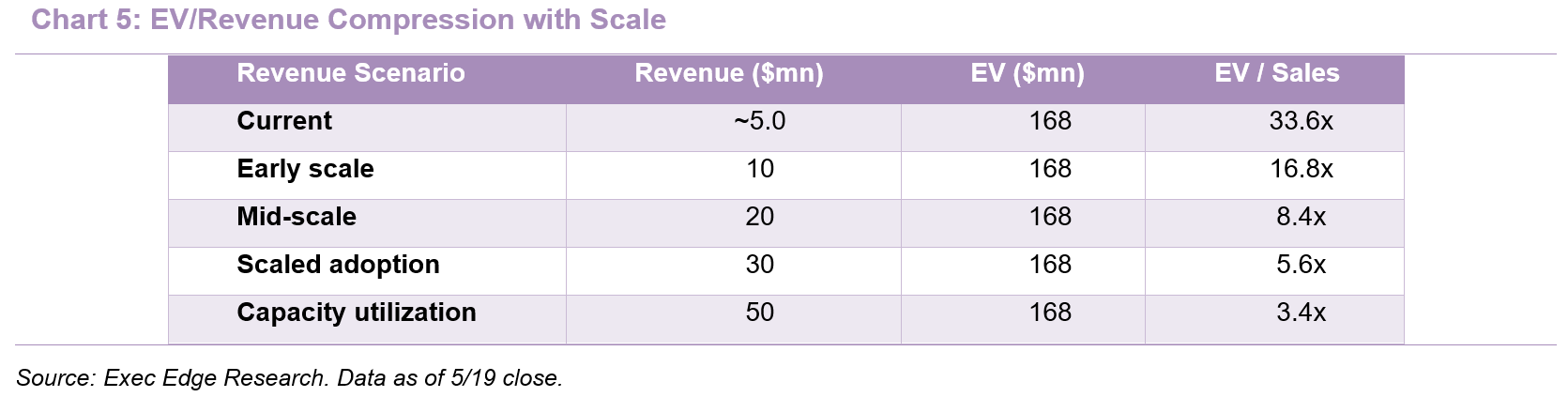

- Our analysis suggests that BOIL’s current valuation framework can be supported, with potential upside driven by revenue scaling into its operating capacity. Please note that the following analysis is for illustrative purposes only and does not constitute a stock recommendation, price target, or a buy/sell/hold view. Our approach focuses on scenario-based valuation anchored in run-rate revenue and stated production capacity, rather than conventional peer-based multiples alone. Any upside referenced reflects illustrative outcomes under different revenue scenarios and should not be interpreted as a price target.

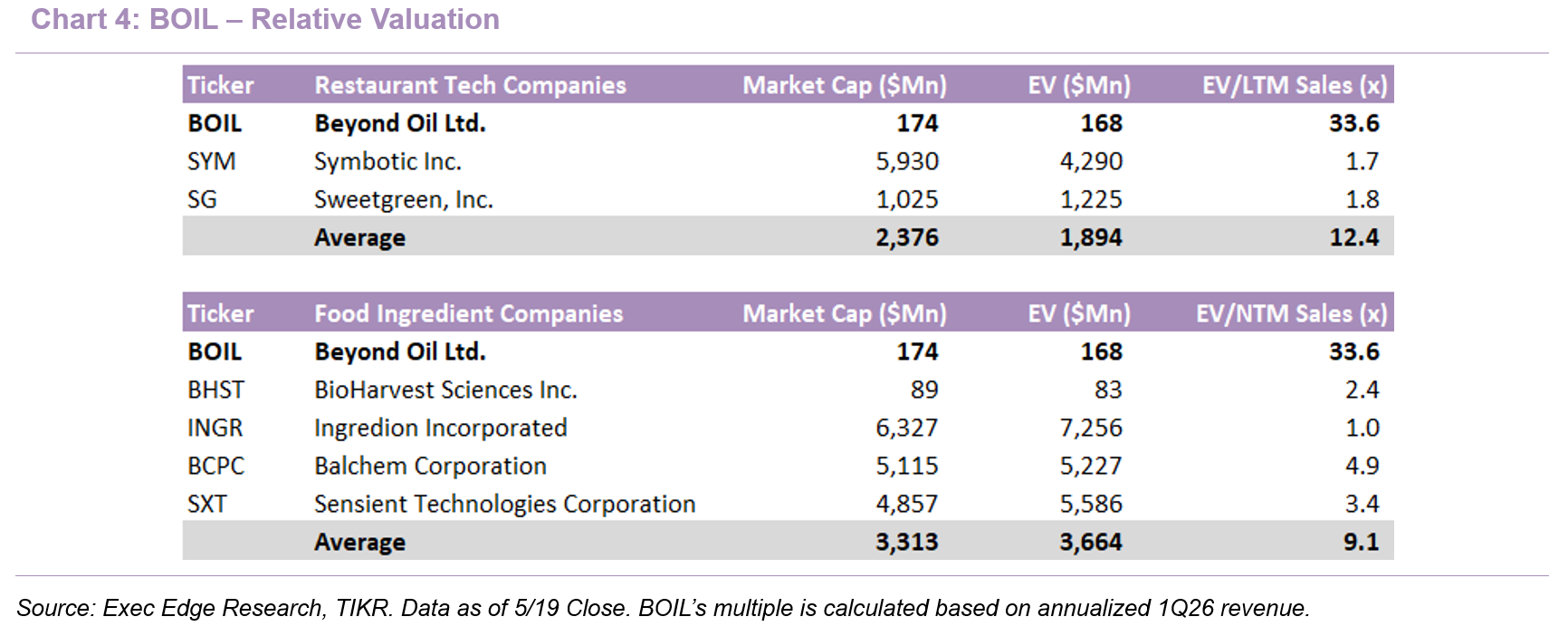

- BOIL’s valuation remains premium on current revenue, but the relevant question is how quickly recent commercial activity converts into a larger recurring revenue base. Based on an enterprise value of approximately $168 million and 1Q26 revenue of $1.26 million, or an annualized run-rate of roughly $5.0 million, BOIL trades at approximately 33.6x run-rate sales. This is elevated relative to traditional food ingredient and distribution peers, but BOIL remains an early-stage commercialization story where valuation is driven less by current revenue scale and more by the pace of multi-location rollout conversion, repeat ordering, and operating leverage as revenue expands.

- The valuation case is best framed through revenue scale rather than near-term peer multiples alone. BOIL’s current run-rate revenue remains small relative to the commercial opportunity, while recent U.S. activity across fast food, supermarkets, premium casual dining, and targeted distribution creates multiple pathways to recurring consumption. At the current EV, the revenue multiple compresses materially as annual revenue scales, highlighting that valuation support depends primarily on revenue growth and opex absorption rather than further multiple expansion. The $50 million scenario is supported by previously disclosed scalable manufacturing capacity, which provides room for revenue growth without requiring proportional capital investment.

- BOIL’s premium is tied to the quality of its revenue model, but execution now has to validate the multiple. The company is commercializing a recurring consumable that can be embedded into daily fryer workflows, creating the potential for repeat usage across multi-location foodservice and food retail accounts. The refined go-to-market strategy, which prioritizes direct strategic accounts and targeted distribution, should improve control over customer implementation, rollout cadence, and reorder visibility. Sustaining the current valuation will require evidence that pilots and initial deployments are converting into broader location coverage, recurring consumption, stable gross margins, and better absorption of the expanded sales and marketing base.

- Overall, BOIL remains an execution-driven valuation story. Upside is less dependent on multiple expansion than on revenue scaling into the existing commercial and operating infrastructure, allowing the current premium to compress as throughput increases. If BOIL delivers stronger 2H26 revenue conversion from U.S. strategic accounts, supermarket and casual dining deployments, and targeted distribution partners, the valuation framework can remain supported. Conversely, slower rollout conversion or inconsistent reorder activity would make the current premium more difficult to sustain.

Download the Complete Report Here

Read Exec Edge’s Initiation on Beyond Oil Ltd. Here

Subscribe to our Weekly Newsletter to Receive All Research

Contact: